New players will encourage competition and disruption in the local banking industry, open more opportunities to Thais to access financial services, improve financial inclusion, and develop the financial ecosystem in the overall market – Ronadol Numnonda, Deputy Governor for financial institutions stability

Regulatory initiative:

The banks in Thailand follow a rather traditional and conservative view towards digitalisation. However, the success of direct customer engagement from industry disruptors in other sectors is encouraging banking and non-banking players to offer tailored and customer-centric digital banking services. Many fintech firms leverage the 72% mobile penetration rate to offer digital banking services such as e-wallet and e-commerce payments to keep up with the paradigm shift in consumer preferences and the growing demand for more personalised services.

In a bid to serve the largely unbanked and underbanked population of the country, 18%, and 45% respectively, the Bank of Thailand announced its decision to study the types of licenses that could be granted to the neo banking sector. This move will encourage competition in Thailand’s banking industry, drive financial inclusion, and grant Thais access to an enriched and customised banking experience.

Snapshots of Thailand’ neobanks:

Table 1: Profile for Thailand’s neobanks

| Annual revenue name | Year | CEO | Funding round |

| Aspire | 2018 | Andrea Baronchelli | US$536K (FY18) |

| TMRW* | 2019 | Kevin Lam | Not available |

Table 2: Learning list of Thailand’s neobanks funding capital

| Name | Aspire |

| Total funds raised | US$ 41.5 Million |

| Seed round | US$ 32.5 Million (Aug 2019) |

| Series A | US$ 9 Million (Mar 2018) |

In-depth neobank analysis on the 5-building block framework

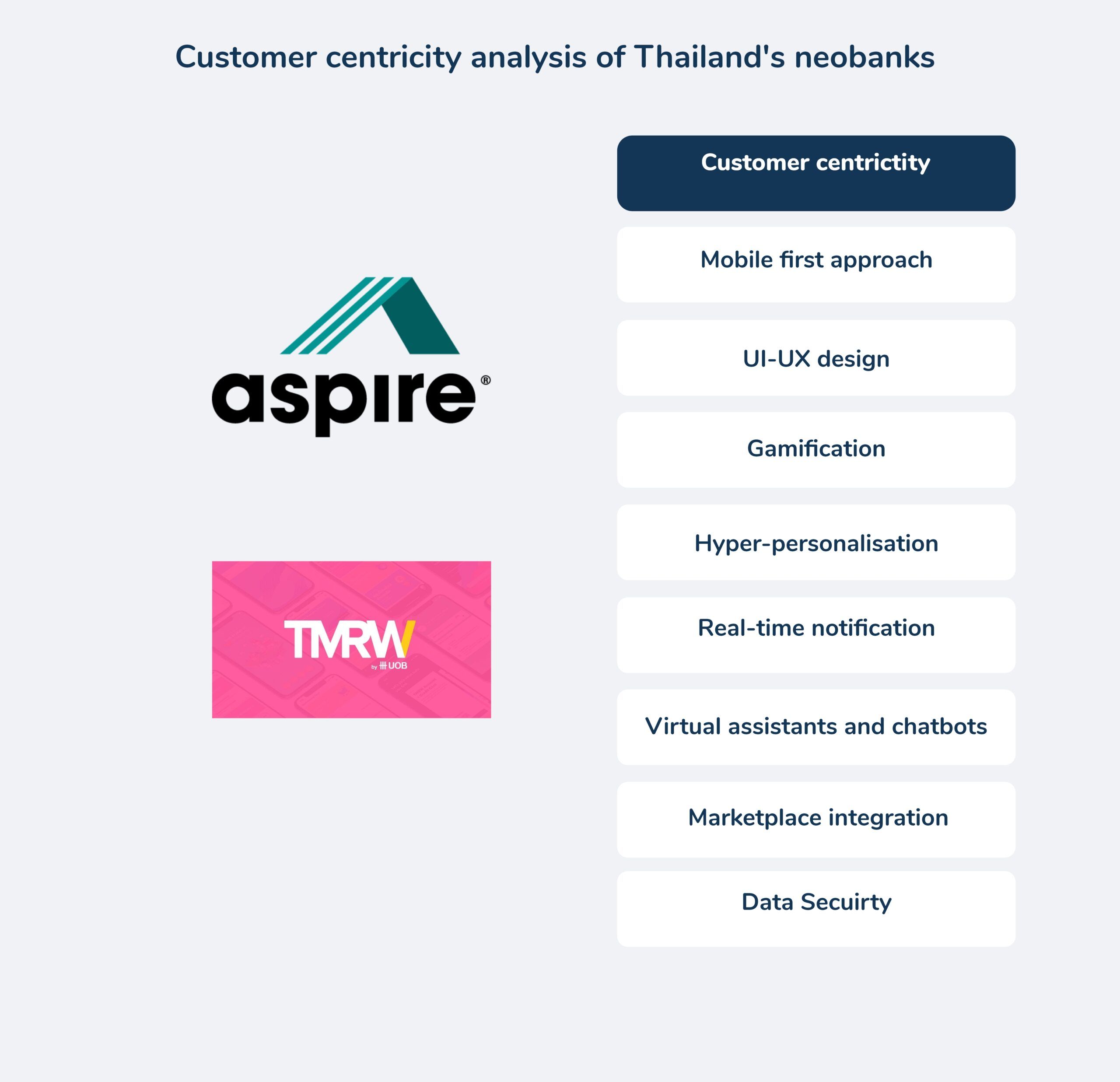

Customer centricity:

- TMRW uses unique AI algorithms and data analytics in order to anticipate the users’ needs and serve them hyper-personalised services. Moreover, it provides its customers with gamified tools to encourage them to save more and design their own cards.

- Both banks follow a mobile-first approach by using UI-UX design to create lucrative and user-friendly tools and offer their customers 24*7*365 assistance and real-time notification alert.

Figure 1: Thailand’s neobanks represent all customer centricity parameters

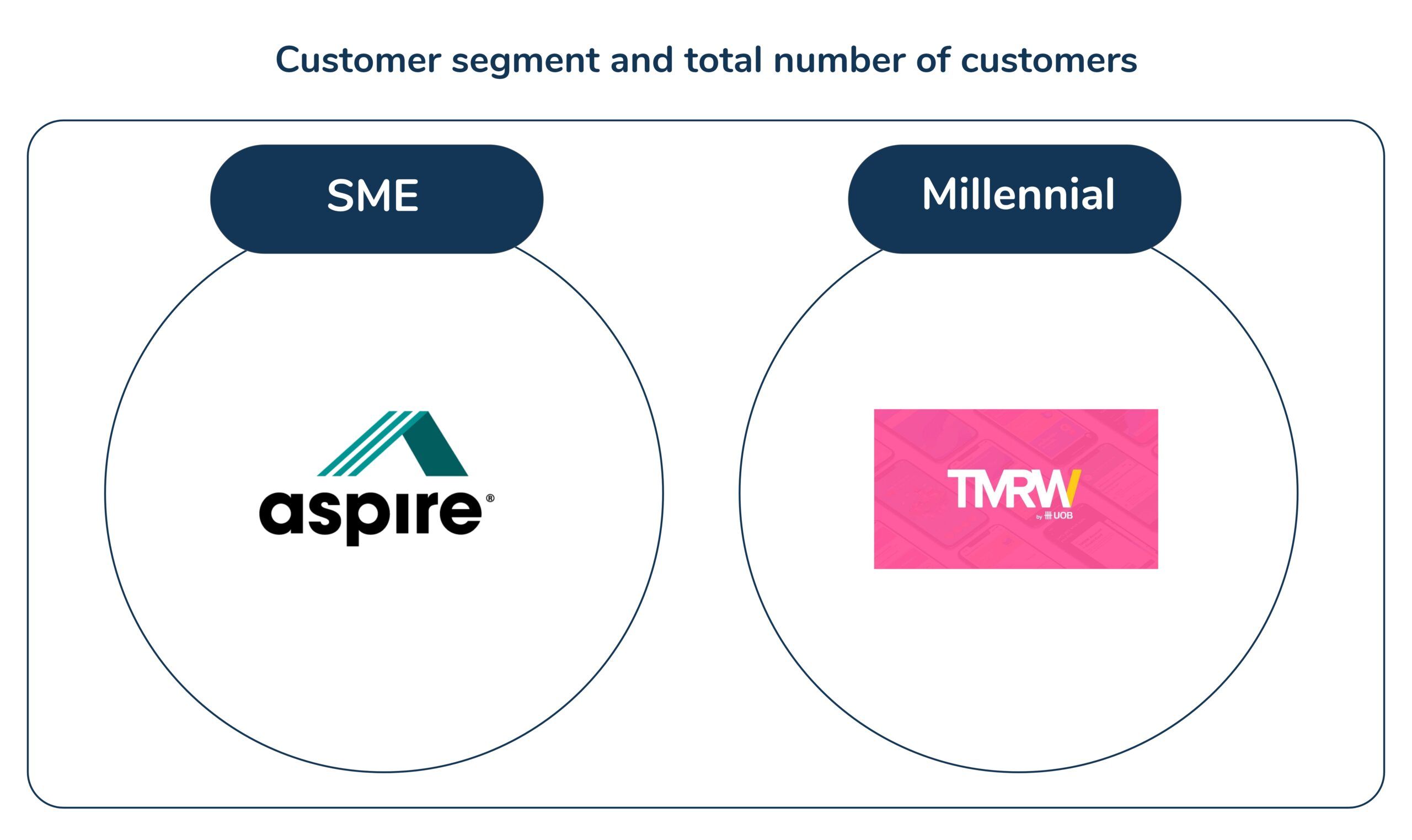

Customer reach:

- Aspire focuses on serving the SMEs in Thailand

- TMRW targets the millennial as well as the Gen Z segment of the population

.

Figure 2: Customer segment and total number of customers

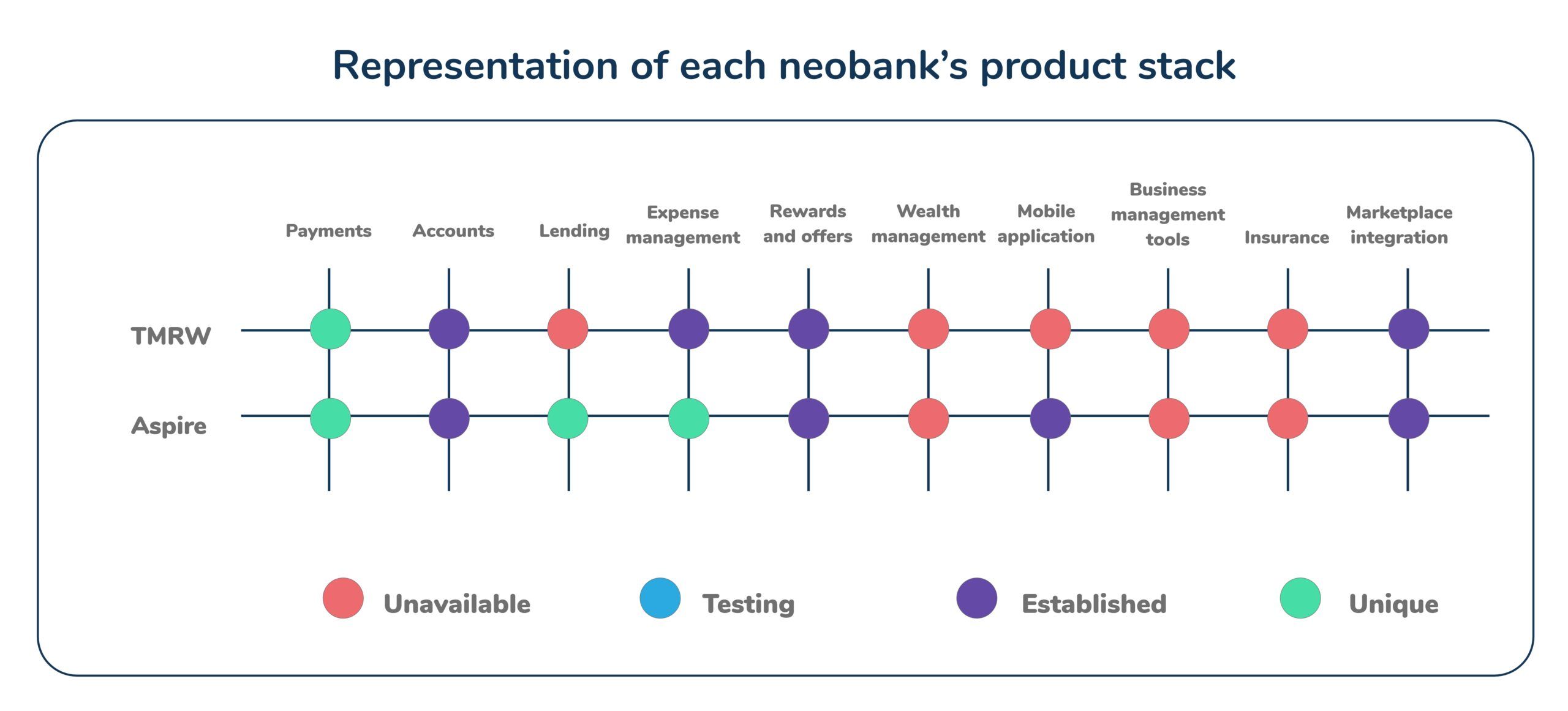

Product stack (Banking solutions):

- Both banks have 50% or more products catering to the customer journey.

- Both banks offer unique payments solution such as virtual cards and split payments.

- Aspire also offers its customers unique lending options which include business overdraft facilities and credit line.

Methodology:

Each neobank product stack is a representation of 4 key parameters across 11 product types

- Unavailable: Does not have a product type in their stack

- Testing: The product is currently in the pilot-testing phase, not live to all customers

- Established: The product is a part of their stack and fully available for customers

- Unique: A unique offering within a product type which is exclusively provided by the neobank

Figure 3: Representation of each neobank’s product stack

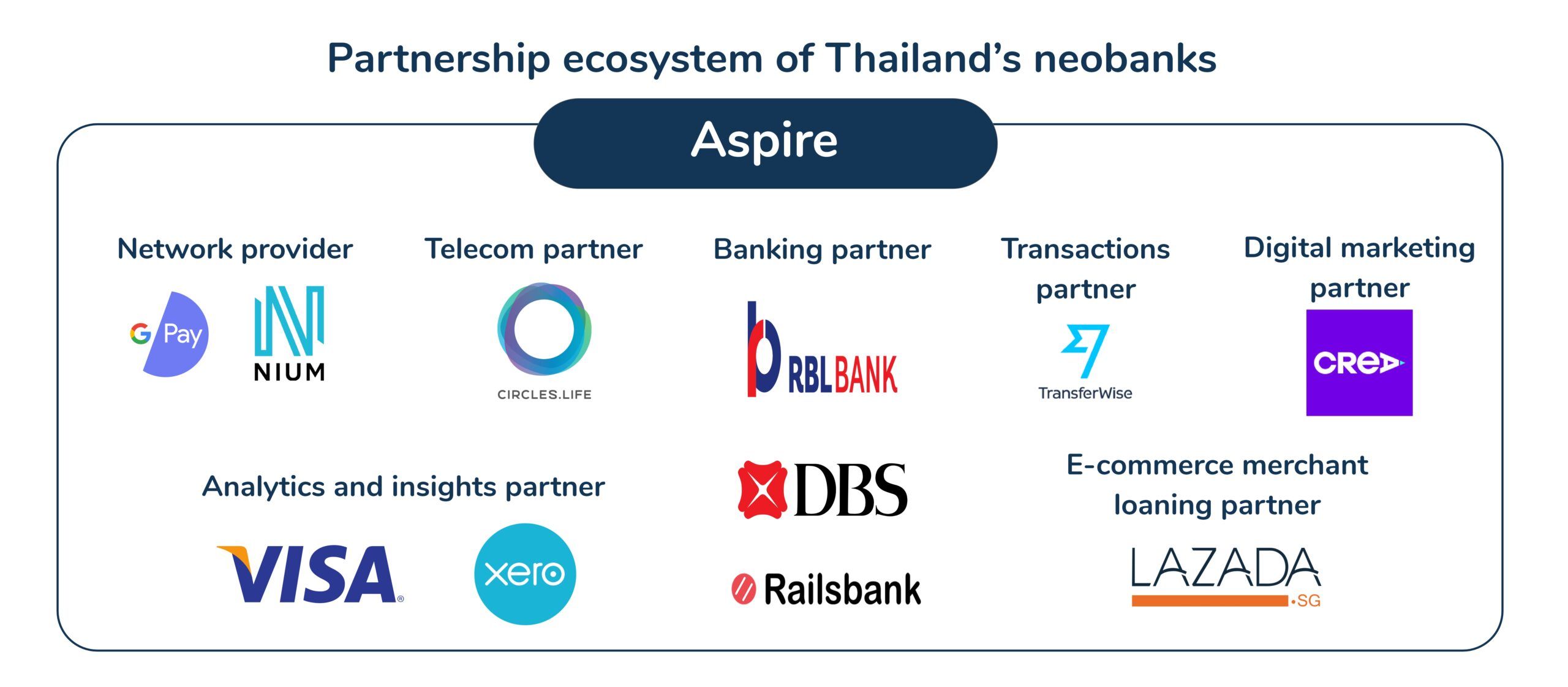

Partner ecosystems:

- Aspire partners with RBL Bank, DBS, and Railsbank to offer banking services to its customers using the traditional banks’ banking licence.

- Aspire’s technology partnership focus on:

- Analytics and insights

- Digital marketing

- Digital transactions

- Other forms of partnerships include network providers, telecom partner and e-commerce merchant loaning partner.

Figure 4: Partnership ecosystem of Thailand’s neobanks

Open banking:

- In Thailand, no regulations govern the open banking ecosystem yet. Thailand’s banks can establish open banking standardisation to boost fintech innovation.

- TMRW uses its parent bank’s API developer platform, UOB developer

- Aspire uses React open-source library ecosystem.

Table 2: API Developers for Thailand’s neobanks

| Name of bank | Sandbox/Platform |

| TMRW | UOB developer |

| Aspire | ReactJS Developer |

Thailand neobanks’ outlook:

- Firstly, partnering with fintech firms will help traditional banks build a strong BaaS and API-driven platform that enables them to offer personalised services to its customers without investing much in changing the core infrastructure and accelerating financial inclusion.

- Banks can also leverage the increase in mobile usage by Thais to expand the services provided by them to 74% of Thais accessing banking services via mobile devices (number one in the world in this particular category).

- Furthermore, the neo banking market in Thailand will witness a more targeted approach catering to the needs of the rural population and SMEs in the near future.

Annexure:

Table 3: Names Thailand’s neo banking investors

| Name of bank | Investors |

| Aspire | Pioneer Fund and Arc Labs, Hummingbird Ventures, Beacon Venture Capital, Picus Capital, MassMutual Ventures Southeast Asia (MMV SEA), Y Combinator, David Langer, Wavemaker partners |

End notes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

Akshita Maruthavanan, Research Intern, contributed to this research by assisting in writing, conducting preliminary analysis and conceptualizing the topic.