Company insights

twimbit Purpose Index

Maybank (Group financials) – An overview as of 31st December 2020

| Bank name | Malayan Banking Berhad (Maybank) |

| Headquarters | Malaysia |

| Operating income (31st December 2020) | USD 6.1 billion |

| Net Profit after Tax (31st December 2020) | USD 1.7 billion |

| Total Assets (31st December 2020) | USD 211.5 billion |

| Employees | 45000 |

| Country of operation | 20 |

| Number of branches | 2,677 |

| Information and communication technology (ICT) spend (31st December 2020) | USD 220.6 million |

| Bank ranking in a particular country | Ranked 1st in Malaysian-listed companies |

| Number of customers | 22 million |

| Market capitalisation | USD 24 billion |

| Operating revenue CAGR growth (2015-2019) | 6.8% |

Shareholder value

| Return on equity (31st December 2020) | 10.9% |

| Total shareholders’ return (1 year) | (3.90%) |

| Net income ratio | 34.25% |

| Common equity Tier 1 ratio | 15.73% |

| Price-earnings ratio (31st December 2020) | 11.54% |

Awards

| 2020 | Global Private Banking Innovation Awards 2020 -Best Private Bank Overall (ASEAN) – Winner -Most Innovative Business Model – Winner Global Finance -World’s Best Bank For 2020 -Best Trade Finance Provider 2020 in Malaysia -World’s Best Consumer Digital Bank in Malaysia and Indonesia for 2020 |

Maybank and its strategic focus areas

- Customer experience

Maybank strives to continuously improve customer experience and deliver value to all the key stakeholders, as well as maintain its strategic focus areas in SMEs, Wealth Management and Digital Banking. The bank aims to enhance the way it leverages digital innovation to create an unmatched customer experience by:

- Providing simple, convenient, and hassle-free access to financial solutions

- Offering financial advice that addresses customers’ unique pain points

- Protecting customers against fraud and scams

- Enabling SME growth through continued efforts in making their access to financial services easy

- Enriching customer experience by scaling digitalisation efforts to new heights

- Delivering market-driven wealth and investment solutions

Initiatives taken by Maybank to enhance customer experience:

- Revamped Maybank2u Mobile App, which enhanced payment capabilities and user experience. It also enabled overseas fund transfers and allowed customers to generate dynamic PayNow QR codes for requesting payments.

- Introduced customer analytics and data-led decision-making at its Maybank Kim Eng (MKE) Institutional Brokerage business for holistic insight into a customer’s behaviour.

- Launched the MAE (Maybank Anytime, Everyone) by Maybank2u App, enabling customers to use their e-wallet and undertake a full suite of banking activities. Customers could enjoy enhanced financial management tools and new lifestyle features simultaneously.

- In the Philippines, the bank launched iSAVE CASA STP, one of the country’s first digital savings accounts.

- Unveiled SME Digital Financing, the first end-to-end digital financing for SMEs in Malaysia with straight-through processing, from application to approval and disbursement. This initiative provides quick and hassle-free financing to SMEs during the recovery period from COVID-19, when liquidity is crucial. Customers receive the loan approval status in 10 minutes, with funds disbursed within a minute of accepting the bank’s offer.

- Employee experience

The bank always focuses on nurturing a safe, caring, and inclusive work environment. Maybank redesigned solutions, enabling employees to navigate through the uncertainties and challenges during the pandemic. Ultimately, it seeks to keep employees connected, engaged and productive while helping them deliver on the bank’s performance expectations for business continuity. Steps taken include:

- Offering development and training opportunities that support employees in achieving their full potential

- Focusing on developing digital and analytical capabilities to serve its customers better

- Providing greater flexibility to perform daily functions and enhance productivity by enabling Work-from-Home (WFH) with Flexible Work Arrangements (FWA) and Mobile Work Arrangement (MWA) policies

- Supporting employees’ overall wellbeing by promoting mental, physical, emotional, and performance fitness in its policies and culture.

Initiatives taken by Maybank to boost capabilities and promote a healthy work environment include:

- Introduced the MWA policy and identified employees with jobs or roles that can go remote, allowing employees to work from home, on-site and or at split locations. In 2020, 2000 employees onboarded to MWA.

- Launched Agility@Home to make it easy for employees to shift from physical to remote working. Maybank provided advice and best practices on productivity and collaboration tools, team communication strategies, and time management skills to enhance collaboration in remote teams.

- Noon talks via live webinars Maybank held these webinars to help employees gain knowledge and tips on staying mentally and physically fit and to encourage them to take ownership of their wellbeing. There have been over 3700 instances of participation across 25 webinars.

- Maybank continues to support employees through the “GO Ahead. Take Charge!” platform. Employees can have control of their careers by reskilling, customising their working arrangements, and pursuing entrepreneurial opportunities using the platform.

- The bank launched an internal gig platform- Crowdtivation. This platform allows employees to learn, collaborate, try out new ideas, and participate in internal jobs while maximising internal resources

- Collaborated with a world-renowned business school to develop a customised online analytics programme – the AI Learning Hub. The AI Learning Hub allows employees Group-wide to upskill themselves and get involved in Analytics, Machine Learning (ML) and Data Science areas from the basics right up to advanced levels of expertise.

- Rolled out various new analytics modules such as R Programming, Structured Query Language (SQL), and Python Programming courses.

- Society and planet impact

Maybank set out a 20/20 Sustainability Plan that focuses on three key areas that contribute to the group’s long-term values: community and citizenship, people, and access to products and services.

- Community and citizenship: The objectives under community and citizenship focus on education, community empowerment, arts and culture, environmental diversity, healthy living, and disaster relief.

- People: Strategies under this segment include employee engagement, learning and development safety, health and wellbeing, talent and leadership diverse and inclusive workplace.

- Holistic mindset: Maybank focuses on commitment to the environment, customers, digitalisation, and product stewardship.

Some initiatives taken by Maybank to facilitate sustainable development include:

- Maybank Foundation extended the partnership it held with the ASEAN Foundation for three more years for the eMpowering Youths Across ASEAN program.

- Maybank initiated an ESG Employee Activitism Campaign to promote broader awareness and mindset shifts among the workforce.

- The bank facilitated the issuance of four separate sustainable investment securities within the region to finance green infrastructure development.

Digital strategy

As part of Maybank Group’s Maybank2020 strategic objectives, the group wants to make Maybank “The Digital Bank of Choice”. The group aims to accomplish this by:

- Engaging with customers to obtain direct feedback on Maybank digital platforms and adapting their needs into future designs. This move ensures that the products and services offered add value and enhance a customer’s proposition.

- Learning customer lifestyle patterns to identify expansion opportunities in mobile and online banking solutions. Maybank designed its existing digital ecosystem to deliver a hassle-free, lifestyle enriching experience.

- Collaborating and forming a digital alliance with fast-moving technology companies that engage a large and complementary digital customer base. Through these initiatives, Maybank Group seeks to improve its scale and reach and digital ecosystem.

Initiatives taken by Maybank Group to strengthen its digital strategy are:

- QRPay: The first bank to promote a cashless payment solution using QR codes.

- Maybank Trade: A mobile trading app developed with enhanced features to simplify portfolio management.

- E-CLEVA: A real-time video-assisted claims-handling system for motor and fire insurance allows the bank to process claims within 15 minutes via video conversation in 2018.

- MAE e-wallet: Seamlessly integrates online banking with lifestyle needs with features such as the in-app virtual debit card and QRPay in 2019.

- Live Chat: Maybank2u and Maybank mobile app launched live-chat to provide real-time answers for Premier Wealth customers in Malaysia in 2019.

- SWIFT gpi: Allows customers to enjoy faster, more convenient, and secure cross-border remittances.

- Maybank formed a strategic partnership with Grab to drive the acceptance and use of cashless payment in 2018.

- Permodalan Nasional Bhd (PNB) – A Malaysian government-linked investment company – in partnership with Maybank, launched ASNB e-channels via the bank’s digital platform. This collaboration enables ASNB customers to make transactions and view their account balances via Maybank ATMs and Maybank2u (M2U) in real-time.

- Maybank PayBand: Maybank Payband is a contactless payment service that uses a VISA pre-paid card account.

- Etiqa’s Smile App, an all-in-one app that gives customers access to their policy details, the panel of service providers, submit claims, and more.

IT Strategy

We place great importance on upskilling our workforce with digital capabilities, while improving our processes and infrastructure to enhance customer experience and operational efficiencies. – Dato’ Amirul Feisal Wan Zahir

In line with the aspiration to become the “Digital Bank of Choice”, Maybank continuously utilises evolving technology to improve service delivery capabilities. This move helps the organisation to explore, embrace, and deploy cutting-edge technologies to achieve business outcomes at speed. Maybank aims to deliver customer-centric products in a fast, secure, and easy manner. It continues to innovate and enhance its systems as well as digital capabilities to be future-ready. The bank has taken the following initiatives to strengthen its IT infrastructure:

- Streamlined back-end processes by deploying ML for effective credit decision-making and leveraging enhanced analytics for personalised customer engagement.

- Reinvented the technology stack across all layers of banking operations. By adopting technology such as robotic process automation (RPA) and application integration for specified operations, the bank implemented self-service capabilities as well as automated middle and back-office procedures. This goal is to achieve higher straight-through processing (STP) rates and considerably improved turnaround times for certain operations.

- Placed greater emphasis on upgrading the data centre, rearchitecting applications on modern digital stacks, and building reusable business services.

- Leverages Application Programming Interfaces (APIs) for seamless integration with partners to support Open Banking initiatives.

- Deployed and continuously upgraded best-in-class cybersecurity defence mechanisms.

- Launched a fully digital CASA STP/Know-Your-Customer (KYC) capability through the new Maybank2u App in Indonesia, enabling onboarding KYC through video calls.

- Launched Artificial Intelligence (AI) for Anomalous Parts Detection to investigate and detect anomalies in vehicle parts proposals in claims submissions.

Maybank ICT contracts

- Maybank has partnered with Liquid Group to launch the QR Payment Terminal solution that supports the adoption of QR payment via PayNow.

- The bank deployed Microsoft Dynamics CRM as a single source of customer information and to facilitate improved tracking and follow up from marketing campaigns.

- Maybank and Western Union, a global payment services provider, launched the first digital remittance service in Malaysia via the Maybank2u (M2u) mobile banking app and website.

8 Innovation and growth opportunities

- Cost to serve

- The Group continues with its cost discipline and managed to lower the overhead expenses by 2.7% Y-o-Y to USD 2,781.3 million compared to USD 2,860 million in FY2019. This decline resulted in an improvement in the cost to income ratio to 45.4% from 46.7% in FY2019. The bank can further improve its cost to income ratio by maintaining it in the range of 40% – 43% to achieve strong bottom-line growth.

- The Group net interest income deteriorated by 8.3% (USD 248.4 million), as the net interest margin compressed 17bps YoY to 2.1%, driven by sharp policy rate cuts during the financial year across home markets.

- The net impact was due to alterations done on fixed-rate loans or financing due to the automatic moratorium granted to borrowers and customers in Malaysia between April to September 2020.

- There is an opportunity for Maybank to manage its income in the low-interest-rate environment by:

- A sound net interest margin management is achievable by identifying repayment risk in loans and attrition risk in deposits. The bank can use predictive behavioural models to revise its interest-rate risk models and hedging strategies continuously.

- Monitoring its contribution to operational profitability from non-interest fees and income from other sources closely.

- Personnel expenses, representing 58.4% of total overhead expenses, decreased marginally by 0.9% Y-o-Y to USD 1623.46 million in FY2020 from USD 1638.75 million in FY2019. The bank should further try to reduce this cost item by:

- Removing duplication of tasks, roles, and functions by using blockchain and quantum computing

- Adopting a holistic cloud implementation strategy that centralises business as usual activities and eliminates data centre management.

- Streamline the regional management team by expanding regional management territory, which will help in significant cost savings and can be adopted easily with little risk

- Transformation of the branch and branch network

- Maybank has a branch network of 2400 branches and over 3400 ATMs across 20 countries. To maintain and run this branch network, the bank spends USD 137.5 million on its premises’ repair, rental, and depreciation. The overwhelming costs create an opportunity for the bank to reduce the underutilised and underperforming branches in its international and home regions.

- The bank should consider focusing on the digital transformation of branch network by:

- Reducing the overall count of the fully-fledged bank branches based on the low footfall and business volume of a particular branch

- Redesigning the entire branch outlook and make it more community-centric like cafes or community centres. Customers can, therefore, easily identify various customer touchpoints and freely socialise with other customers within the branch

- Integrating both augmented reality (AR) and virtual reality (VR) to create a virtual branch experience using AR/VR tools for remote support services

- Deploying smart robots in-branch to handle daily queries

- Creating self-service kiosks at fast-moving work complexes, student hangouts and market lanes

- Promoting online engagement with the bank’s staff in the form of in-app video conferencing or virtual assistants rather than a physical branch visit

- Customer experience

- The bank has a clear vision on how it wants to enhance customer experience. It has introduced many apps (like Maybank2u, Maybank wealth app, Maybank2e, and MAE lifestyle app by Maybank2u) to be the digital bank of choice by putting customers’ preferences first and transforming to deliver next-generation customer experience.

- This shift creates an opportunity for the bank to develop a super-integrated application by bringing together all the features of these applications, making it easy for customers to access their financial products in one place instead of different applications. Doing so will help the bank target wider customer segments and expand its operational boundaries using a standalone application.

- The bank also needs to focus on the following areas for superior customer experience:

- Extending the predictive analytics capability from the Maybank wealth management app to retail and SME customers. For retail customers, the bank can personalise insights into their spending and saving patterns with specific recommendations to help them meet the financial goals that they set in their goal-saving plan on the Maybank2u app. For SME customers, the bank can use analytics to provide a dynamic representation of cash flows and reconciliation for effective working capital management

- Employing behavioural algorithms to understand customers preferences and journeys for identifying relevant products and services

- Gamifying Maybank2u app user interfaces with customised views and modes to make the customer experience more personalised and interactive.

- Artificial Intelligence (AI) in everything

- The bank transformed and accelerated auditing in the digital space by incorporating AI and ML for better decision-making and determining emerging risk. It deployed 132 Robotic Process Automation systems to replace 1,379 manual tasks.

- Maybank should also invest in consumer behaviour analytics to identify preferences and deliver timely and compelling offers. This move will help the bank to add revenue from non-interest income sources through third-party integration.

- To further broaden the application of AI, Maybank can focus on the following areas:

- Integrate AI to predict future scenarios by analysing past behaviours. AI can help Maybank predict future outcomes and trends. This move will help it to identify fraud, detect anti-money laundering patterns and make customer recommendations.

- Enhance existing data quality and unify the data sets by supporting proactive and reactive data maintenance. In addition, such improvements will make the data silos more conducive for machine learning and AI algorithms.

- Migration of workloads to the cloud

- Maybank must migrate its data centres to a dedicated cloud storage platform for systematic and scalable data management processes, ultimately bringing a substantial change in its business operations.

- Maybank relies on a third party to host the cloud storage and spends USD 97,000 monthly to maintain its cloud infrastructure. The bank can self-host its major applications to have higher control over its data silos. It should begin with a private cloud strategy and incrementally move towards a hybrid cloud platform with a substantial workload on the public hosting infrastructure. Maybank can forge sustainable partnerships with cloud partners for a cost-effective cloud strategy.

- The bank can integrate its cloud infrastructure by extending data storage and data-driven activities across security, regulatory compliance, auditing, and pan-organisation communication pipelines to transform its overall operational model.

- The bank can adopt a customer-centric cloud-based strategy that allows it to create a productive environment for developers to seamlessly create, test, and deploy various services through a microservices mesh architecture. Maybank can easily pilot these services with soft launches and manage its successes or failures without hitting cost structures.

- Neo banking

- Maybank is in a strong position when it comes to digital banking apps, as it offers a wide expanse of digital products and services through Maybank2u. However, the bank should consider merging the group’s entire product portfolio into one strong digital proposition which resonates with the tech-savvy customer mindset.

- Maybank can further incorporate the following elements in its digital app:

- Recreating the design outlook of existing products by introducing things like trendy ATM card designs, virtual cards, and an animated banking app interface

- Introducing byte-sized loan and investment products which gives the customers increased flexibility to navigate through different product options

- Innovating product delivery channels by combining multiple product offerings as per the customer’s preferences

- Gamify various customer touchpoints, like awarding badges with the increased use of products, giving discount coupons to loyal customers, a leaderboard between friends and colleagues based on product purchases, and highlighting trending products

- Security

- Maybank is mitigating the risks to its business and customers that come with the expansion of digital channels by developing a robust cybersecurity infrastructure, including internal governance, human knowledge, and network strength.

- The bank’s Regional Security Operations Centre centrally manages the security of systems at an operational level through security information and event management software. This improvement allows real-time monitoring to detect and quickly respond to internal or external cyberattacks to digital systems.

- To further strengthen security measures, the bank should focus on the following areas:

- Test its internal security framework by exposing it to regular stress tests. These tests will give the bank a better understanding of its security crisis readiness and objectively locate loopholes in its security strategy.

- Automate regular security functions threat monitoring, identity access management, controlling and reporting mechanisms to make the overall security framework more transparent and smoother.

- Maybank can use ML to improve the ability of predictive risk intelligence that identifies any emerging risks for the bank.

- Experiment with own hypothesis generation via advanced AI tools to assess cyber threats and identify recommended strategies for mitigation.

- Integrate Cognitive Process Automation (CPA) to develop and test new security strategies. In turn, CPA will help determine appropriate response mechanisms to account for the dynamic and varied nature of security threats.

- Society and planet contribution

- Maybank understands the need for economic growth and social inclusion within a low-carbon economy. It believes in realising positive environmental impacts through its financing and investment activities.

- Moving in the direction of protecting the environment, the bank reduced its paper consumption by 15%, electricity consumption by 8.4%, and water consumption by 11.7% compared to FY2019. The bank can reduce its carbon footprints further by:

- Adopting renewable sources of electricity (solar powerplants and windmills) in branch operations

- Using eco-charges, smart sockets, programmable thermostats, and indoor motion sensors to reduce electricity consumption

- Shifting toward green products such as virtual cards, pulper cards, eco ink, and carbon control press machines will help the bank reduce the direct impact of its business activities on the environment.

- Minimising the amount of paper and plastic waste within the branches and instituting the ‘3R’ policy of reducing, reusing, and recycling waste management.

- Ban plastic use within office premises

- Use of own cups, bottles, and cutlery

- Recycle water in washrooms and pantry

- Reduction in paper used for documentation

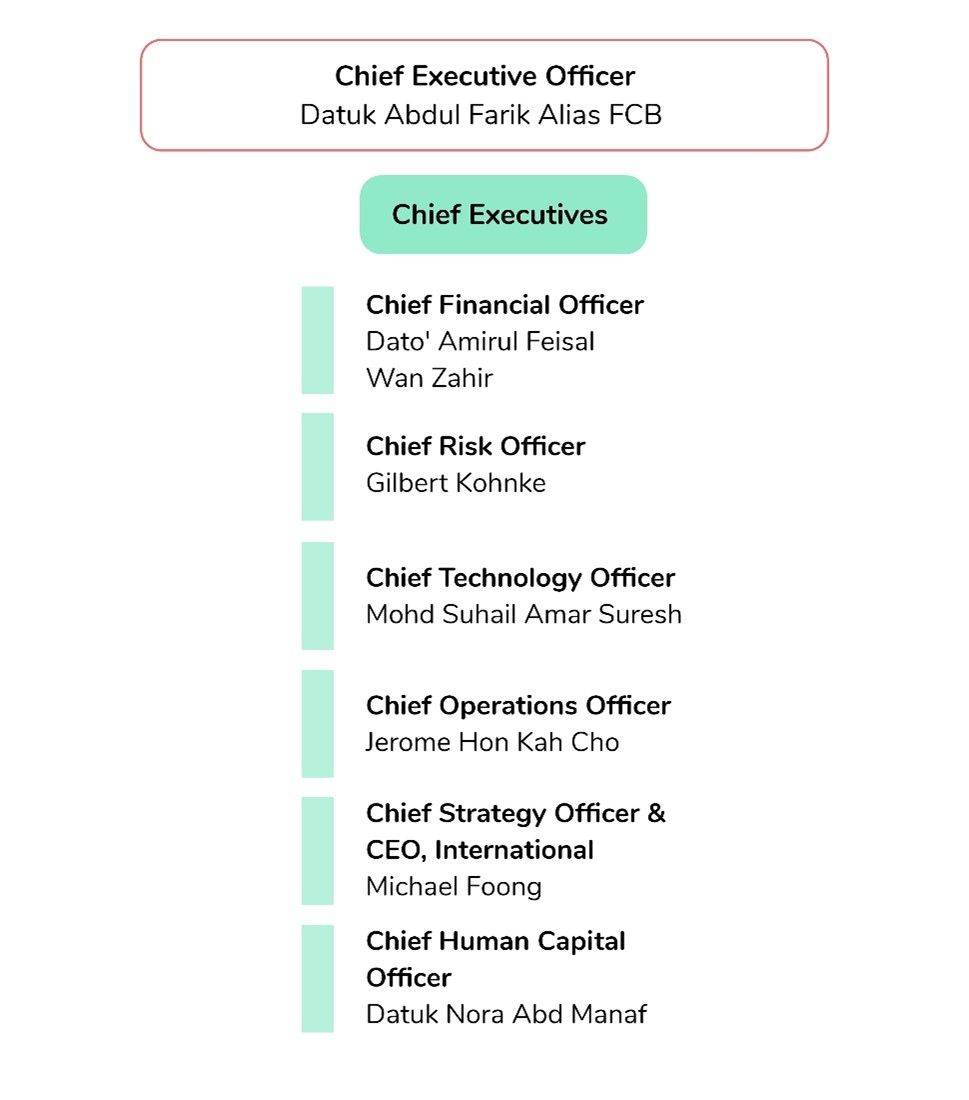

Organisational structure

Executive profile

Datuk Abdul Farid Alias

Group President & CEO

Maybank appointed Datuk Abdul Farid Alias as the Group President and the Chief Executive Officer and Executive Director on 2 August 2013. He takes charge of Maybank Group’s overall business expansion and regionalisation initiatives. He also ensures long-term value creation for shareholders, customers, workers, and all other stakeholders. Alias has over 25 years of experience in investment banking, corporate finance, and capital markets. He has previously been attached with several other institutions – these include Aseambankers, Schroders, Khazanah Nasional Berhad, Malaysian International Merchant Bankers and JP Morgan.

Quotes

- Sustainable finance, Sustainability report 2020

Within our efforts to deliver sustainable finance, digitalisation remains a major area of opportunity for enhancing the widespread availability of financial services.

- Humanising financial services, Annual Report 2019

Maybank is committed to doing its part in helping its customers and communities’ weather through this unprecedented event in line with our mission of Humanising Financial Services.

- Digital forefront, 04 April 2016

Today, everyone is talking about digitisation and the banking industry is witnessing a breed of digital players encroaching into the traditional banking business. Our customers are also changing the way they interact with us, as they are even more digitally savvy. How aptly, and quickly we respond and adapt will determine the fate of the Maybank brand in the future

Dato’ Amirul Feisal Wan Zahir

Group Chief Financial Officer

Dato’ Amirul Feisal Wan Zahir was appointed as the Group Chief Financial Officer of Maybank on 1 July 2016. He has over 20 years of global banking experience and worked in major Asian financial institutions. Dato’ Amirul Feisal Wan Zahir also holds more than 15 years of senior management experience, including heading a publicly traded chemical business and Maybank Group’s Global Banking franchise.

Appendix A

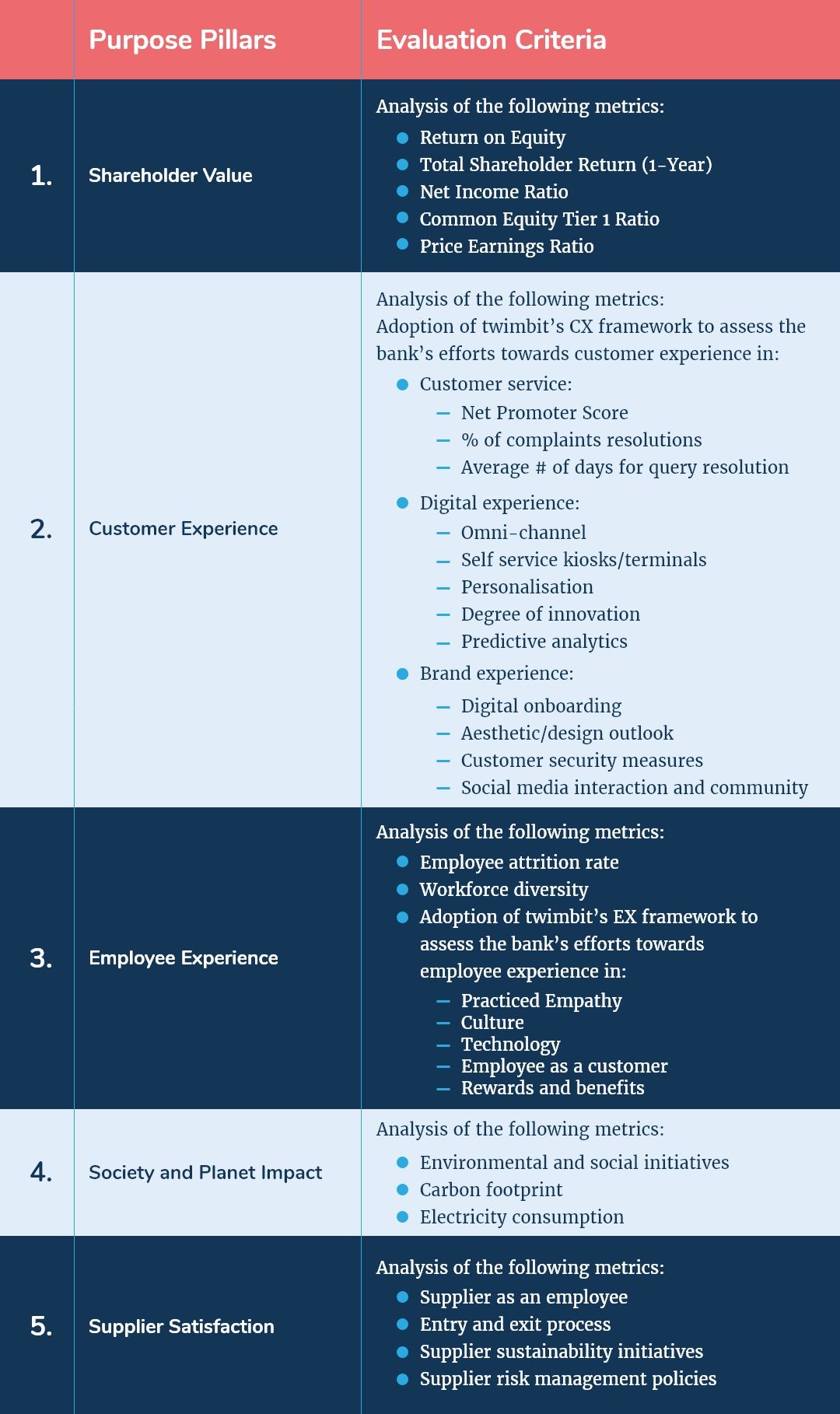

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Maybank, (2020, December 31). Annual report.

https://www.maybank.com/en/investor-relations/reporting-events/reports/annual-reports.page

Maybank, (2020, December 31). Sustainability Report.

https://www.maybank.com/en/investor-relations/reporting-events/reports/annual-reports.page

Maybank, (2020, December 31). Financial statements.

https://www.maybank.com/en/investor-relations/reporting-events/reports/annual-reports.page