Company Insights

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Bank Negara Indonesia (Group financials)- An overview as of 31st December 2020

| Bank Name | Bank Negara Indonesia (BNI) |

| Headquarters | Jakarta |

| Operating revenue (31st December 2020) | USD 3.7 billion |

| Group net profit (31st December 2020) | USD 235 million |

| Total assets | USD 63.8 billion |

| Employees | 27,202 |

| Countries in operation | 7 |

| Number of branches | 2,219 |

| Information and Communication Technology (ICT) spend (31st December 2020) | USD 96.2 million |

| Number of customers | Not Available |

| Market capitalisation (31st December 2020) | USD 82.4 trillion |

| Operating revenue CAGR growth (2016-2020) | 4.7% |

2.Conversion rate IDR to USD as of 31st December 2020 – 0.00007165 USD

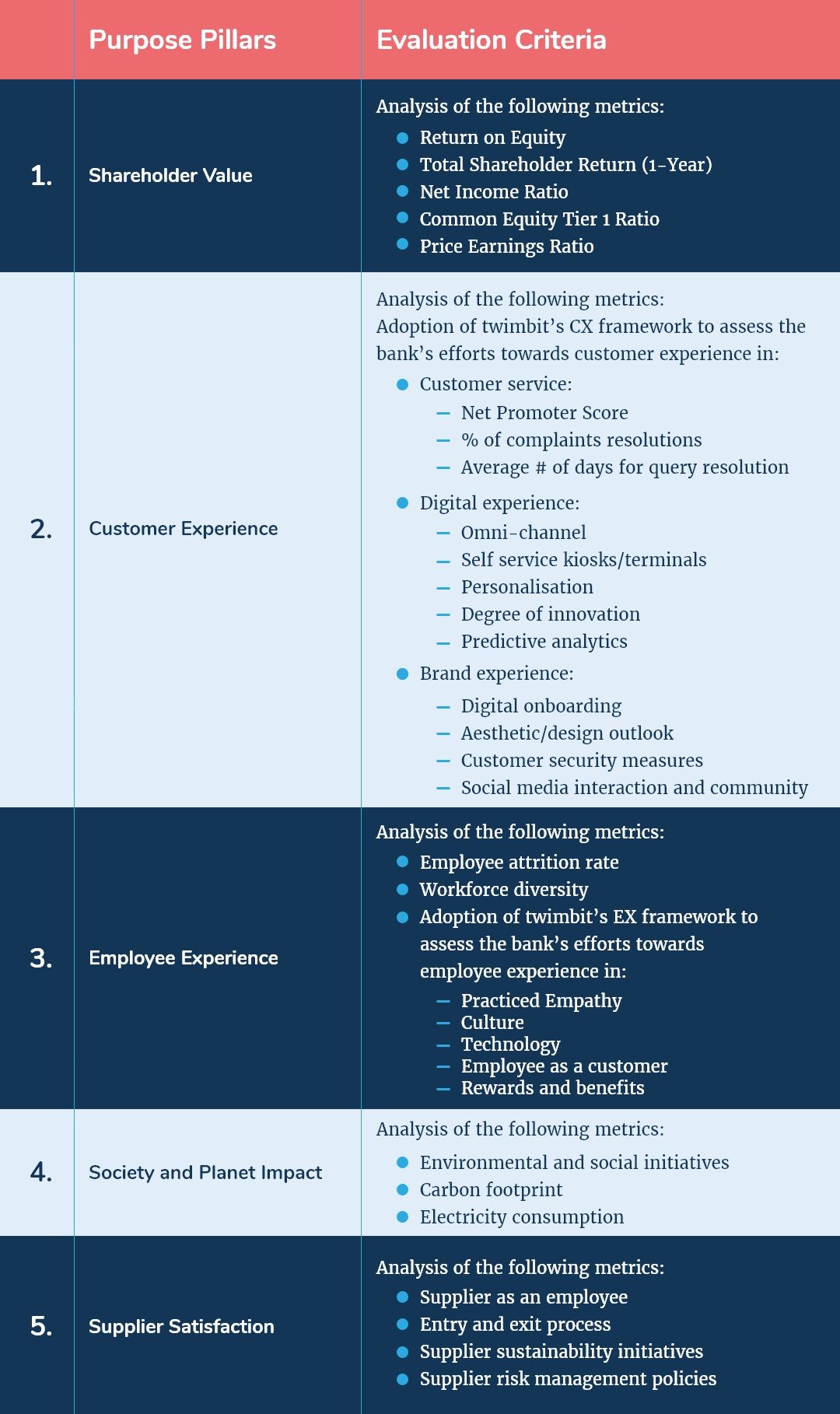

Shareholder value (31st December 2020)

| Return on equity (31st December 2020) | 2.9% |

| Total shareholder return (1-Year) | 15.26% |

| Net income ratio | 6.3% |

| Common equity Tier 1 ratio | 15.7 % |

| Price-earnings ratio (31st December 2020) | 72.7% |

Awards

| 2020 | Treasury & FX Awards 2020: Best FX Bank for Structured Hedging Solutions and Proprietary Trading Ideas, Best Corporate Treasury Sales and Structuring Team 14th Annual Alpha Southeast Asia Awards 2020: Best International Banking Division, Best Cash Management Bank in Indonesia Best Financial Institution Awards 2020: Best Cash Management Bank in Indonesia” VA Debit Cardless Withdrawal Asiamoney Awards 2020: 1st for Market Leaders in Indonesia among domestic banks (as voted by corporations), 1st for Best Service in Indonesia among domestic banks (as voted by corporations) Euromoney Awards 2020: No.1 Indonesia Domestic Market Leader (category Overall) voted by Non-FI, No.1 Market Leader in the Asia Pacific for Indonesian Rupiah Transaction as ranked by Financial Institution in the Euromoney 2020 Cash Management Survey. JCB Indonesia Award 2020: Best Issuing Sales Volume in Indonesia 2019, The 3rd Best Issuing Sales Volume in Southeast Asia Countries 2019 2020 Global Top-Ranking Performers Awards: Best Technology Innovation – Internal Solution, Silver Winner for Best Recruitment Campaign Devportal Awards 2020: Best Overall Developer Portal Community Prize |

BNI and its strategic focus areas

BNI has included a timeline for the implementation of key strategic objectives over the next five years. The bank entered its “business expansion through digital corporate and retail ecosystem” phase in 2020, in line with its 2019-2023 Corporate Plan. BNI executed strategic initiatives in this period to drive growth across all business lines. It is also expanding into new concepts, such as digital attackers and ecosystem solutions.

The strategic initiatives that BNI focused on in 2020, according to the BNI Long-Term Plan outlined in the Corporate Plan, are as follows:

- Improve credit quality by implementing risk management and credit reorganisation.

- Optimising liquidity by formulating an efficient funding mix to support business.

- Improving cost-effectiveness by prioritising work projects and activities.

- Enhance CASA through digital transactions and collaboration with third parties.

- Strengthening its human capital and IT abilities to support work initiatives and programs.

- Customer experience

To remain competitive in the banking industry, one strategy that BNI swears by is customer-centricity. It is always working towards improving business processes to provide a positive customer experience. In light of this, one of the bank’s focus areas is customer experience. BNI bank follows the following measures to keep up with the industry:

- Continues to improve its digital opening account service, thereby making it easier to open BNI savings accounts anytime and anywhere using only a smartphone with facial recognition technology.

- BNI Contact Center enhances customer experience through its integrated omnichannel platform, which has high flexibility and dynamic technology such as:

- BNI Call Virtual Assistant Application, which works with Artificial Intelligence (AI), Voice Command and Natural Language Processing features (NLP), provides the best service to customers.

- Adding more transactions and digital complaint resolution monitoring features to the BNI Call Virtual Assistant Application.

- The application also provides information on BNI products and services as well as the most up-to-date general information. It helps to improve customer experience by providing easy access to the BNI Call service.

Initiatives taken by BNI in 2020 to elevate customer experience:

- BNI customers can use the Interactive Voice Response (IVR) feature or speak directly to a BNI Call Officer 24×7 by accessing BNI Call 1500046 services. They can also use the bank’s mobile apps to access BNI Call 1500046 and Digital Contact Center services, available on Playstore and Appstore.

- BNI Contact Center officers handle requests for information and complaint resolution via social media immediately, giving customers the same experience as if they were communicating in person.

- Verbal customer complaints are resolved within five working days, while written complaints at a maximum of 20 working days.

- ATM for People with Disabilities- BNI has a network of 3,234 ATMs. These ATMs come equipped with various features such as a wheelchair-friendly access road to the ATM gallery, an automatic door, and so forth, making it accessible to people with disabilities.

- BNI created a variety of programs to assist and optimise business processes, as well as to make it easier for customers to use BNI products and services, such as:

- BNI Orange Magz is a mobile application that allows clients to scan the QR code located at each branch and learn more about BNI products and services.

- E-BSS (E-Branch Sharing Session) serves as a platform for all frontline employees to obtain information on BNI products and services, programs, promotions, provisions, and other pertinent information. It helps employees improve the transaction experience by providing the customers with the latest information on products and services.

- Customers can submit their feedback or assessment on the quality of BNI services at each outlet using the BNI Service Rating system. They can rate the quality of service received from both officers and non-officers using a QR code accessed straight from their cell phone.

- Employee experience

BNI is dedicated to constantly broadening its operating activities. Steps taken include partnerships or equal work opportunities with highly competitive and determined individuals, as well as taking on difficulties and overcoming hurdles.

- Policy: Leadership, career path, reward and remuneration, organisational policy, employee training and development, performance management, work environment, work-life balance, and work infrastructure have become benchmarks for highly qualified employees at BNI.

- Welfare: Employees have the right to express their thoughts and share their opinions in the workplace. Business processes, organisations, technologies and a task delivery culture influence their productivity.

- Health: BNI cares for its employees’ health by providing facilities for maintaining health and treating diseases. Employees are entitled to an annual medical check-up, scheduled as needed through the company’s flexible benefit application.

- Rewards: BNI offers varying insurance options, including the national social security programs such as BPJS, BPJS Employment, and other private insurances. It also has a Retirement Health Fund Program (DKMP) for employees who are approaching retirement.

The impact of the bank’s human capital strategies is visible through its employee engagement score – it stood at an astounding 95% in 2020, an increase of 5% from 2019. This score is the result of the following initiatives that the bank undertook:

- The bank offers employee welfare initiatives in both material and non-material forms. Employee performance links intimately to material programs such as transportation allowances, pension money, education money, medical expenditures. Non-material programs are employee welfare initiatives that provide facilities and services to all bank workers without discrimination.

- The bank has started using the Daily Planner and a mobile application named DigiHC as tools to track employee performances. The features help boost employee productivity.

- BNI provides an assortment of modern amenities and workspaces that cater to the preferences of millennials, as they account for more than half of the bank’s workforce.

- BNI employees have access to a gym centre with several workout equipments and qualified instructors conducting classes.

- The company provides various training and education programs with partners from the finest national and worldwide campuses. The aim here is to promote employee competence. They also have learning programs offered through the BNI Corporate University or BNI CorpU, namely the Core Credit Skill program, Smart CA, Officer Development Program (ODP) and Leadership.

- BNI extends training to employees who will be starting their pre-service period. This program helps employees approaching retirement by providing information on their health, finance and psychology.

- BNI uses an Employee Engagement Survey to track employee engagement regularly (EES). The results of this survey work as input in the process of reviewing the HR management system. It helps in developing policies that align with the goals of the employees.

- The Human Capital (HCT) branch of BNI has a system in place for employee grievances. It handles employee complaints using the following procedure:

- Employees can file grievances through their immediate supervisor, who decides on a solution through deliberation.

- The issue passes to a higher rank in case the supervisor fails to reach a settlement.

- If the matter still requires resolution, the employee has the choice to take it up with the trade union managers, who discuss it with the Chairperson in stages.

- Employees, leaders, and trade unions seek a solution to avoid industrial problems.

- Society and planet impact

BNI dedicates itself to putting corporate social responsibility (CSR) strategy into action. The bank’s CSR Program demonstrates its commitment to public and environmental preservation, as well as long-term economic development.

- BNI for Indonesia: The bank’s applies effort to assist sustainable development in Indonesia, particularly for BNI partners. BNI promotes environmental protection, social welfare improvements, and community economic empowerment.

- BNI for customers: BNI applies the principle of responsible investment. The bank understands the importance of managing money responsibly. As a result, BNI has formed mutually beneficial partnerships while focusing on economic, social, and environmental issues through good governance.

- BNI for Employees: BNI commits itself to create a proud workplace that encourages all employees to reach their full potential.

- BNI for the Community: As a State-Owned Enterprise (SOE), BNI engages in social responsibility (CSR) that empowers people and improves their lives according to the Company’s Mission.

- BNI for the Environment: The company has started the ‘BNI Go Green’ program to help with environmental protection and promote love for the environment.

The bank’s CSR program and activities have a significant effect on the public’s welfare and the environment. Effects are visible through the initiatives that they have taken up. The bank allocated 1% of its total revenue towards the community development program, amounting to USD 1.2 billion. These are the initiatives that significantly impacted the bank’s sustainable development efforts:

- BNI has used the Green Banking initiative in its lending efforts. Green Banking is a set of activities carried out by a financial organisation that prioritises environmental sustainability in its operations.

- It continues to improve energy efficiency, particularly in the Head Office, by instituting measures such as turning off the lights for one hour.

- The bank uses a cooler with magnetic-bearing technology in the Plaza BNI to improve energy efficiency. A magnetic field is its main driving component, allowing minimal friction between driving components when working.

- It has also begun to use solar energy directly for lighting to improve energy efficiency.

- BNI applies a vehicle-sharing system between office locations, such as shuttle and carpools, to reduce fuel consumption.

- The bank has transferred printed documents and communications to digital forms, including correspondence, attendance, BNI e-PP, and e-billing programs to reduce its paper consumption.

- The bank has established a financial inclusion program based on a company model that combines financial literacy with partnership business governance. It includes BNI Smart goods, BNI Student Savings, and Agen46 technology services with community-based waste management.

- The bank partnered with the Organic Forest Group to plant trees and improve the environment quality.

- It also carried out rhino species conservation acts and community development projects.

- Security strategy

One of the bank’s strategies to enhance its business capabilities and materialise the digital mindset includes strengthening cybersecurity measures. BNI took the following steps to ensure business continuity in the face of cybercrime:

- Consistently apply governance, regulation, and compliance to ensure that information security functions properly and according to the internal policy, current rules and regulations, as well as best practices.

- Using the Secure SDLC framework to develop security aspects into every application’s development.

- Creating an information security architecture for data, applications, endpoints, networks, and security perimeters is updated regularly to guarantee confidentiality, integrity, and availability.

- Applying a multilayer security device based on the international standards at national banks.

- Proactively monitoring cyber threats 24 hours a day, seven days a week.

- Collaborate with official state agencies (such as the Bank Indonesia, Otoritas Jasa Keuangan (OJK), and Badan Siber Dan Sandi Negara (BSSN)), the principal security apparatus, and the rest of the cybersecurity community. This move helps BNI learn about threats and weaknesses, the latest technology and products, and obtain assistance in case of an incident.

- Increase employee awareness of cybersecurity through education.

- Enhance the awareness through HR competency development programs regularly.

In addition to the concerns above and current cyber-attack trends that are targeting customers more, BNI employs several precautions on the customer side, including:

- Implementing various client protection systems against fraud transactions from malware banking and social engineering.

- Initiated a fake website detecting system.

- Created a mechanism to notify customers about their transactions.

- Continued customer education on password, internet banking, mobile banking and ATM transaction securities, as well as other forms of self-protection.

Digital Strategy

The bank’s mobile banking app became a major medium to conduct banking transactions. The user base saw significant growth from 2019 (4,878,000) to 2020(7,787,000). The number of transactions went up to 302 million from 202 million in 2019. BNI embraced the notion of going digital, and it seems to be working.

The strategies that the bank has come up with to expand in the digital space are:

- Building digital-based products and solutions that integrate into the BNI Cash Management System.

- Developed a digital-based business ecosystem that includes integrated notional pooling, cash distribution pooling, Eco-Smart and other integrated digital solutions. The aim is to enhance client transactions.

- Created automation tools with 24/7 service using chatbot tech to improve customer service.

- Continue to develop BNI Trade Online and Swift GPI as cross-border payment solutions in collaboration with its international division.

- Partnered with fintech and e-commerce as a sales channel, such as Paylater-Traveloka, DUMIFIDAC, Tokopedia, etc.

- Collaborated with e-commerce merchants with growing transactions with credit cards, including merchants such as Shopee, Blibli, Tiket.com, JD.id, Lazada and Zalora.

- Worked together with JD.ID, Doku Wallet, etc., for digital account openings so that customers can make transactions directly using BNI Mobile Banking.

- Collaborated with global players such as Amazon Web Services, Apple Distribution International, TikTok, Netflix, Microsoft Regional sales, and Zoom Video Communications as tax payment solution providers in Indonesia.

The growth of BNI in the digital medium is the fruit of initiatives in the past year. These initiatives include:

- Using digital marketing to become a domestic leader with a Transactional Platform of Choice, one that offers superior and innovative Cash Management, Value Chain, Bank Guarantee, and Trade features.

- Use of API-based and digital solutions to help the corporate, commercial, fintech, and e-commerce industries grow, such as platforms and channels for API-based transactions (open banking), onboarding, and digital account openings.

- BNI also developed an Autopayment solution, which is a collection facility offered by the bank to enable direct payment of transactions on the Biller website or app. It has a daily limit that is scalable. OTP functions to validate registrations.

- To make it easier for corporate and commercial customers to manage the composition of billing in different accounts, BNI has included the Virtual Account Billing Splitting Management functionality to the BNI Cash Management System. Bills can be automatically distributed to various accounts using the function. The BNI Virtual Account comes backed with a dashboard system that makes account management easier for corporate and commercial users.

- BNI has begun developing an omnichannel platform that will link BNI Internet Banking and BNI Mobile Banking to provide consumers with a seamless experience. Virtual Assistant services, Financial Management, Digital Loans, Entrepreneurship Services as well as other features and services are part of the development.

IT Strategy

BNI defined four strategic directions for IT: new digital proposition, governance toward performance, strive for operational excellence, and innovative and agile organisations. The directions were in place to support the corporate strategy from 2019-2023. Some strategies include:

- The use of both public and private cloud for application deployment, which is both cost and time-efficient.

- BNI has improved its cloud capability in support of Platform-as-a-Service (PaaS) technology, which also helps the company to execute DevSecOps.

- The bank uses digital tools, analytics and big data to analyse credit to optimise its business processes.

- BNI enhances communication network capacity in the outlets by adopting encrypted Software Defined Wide Area Network (SD-WAN) technology. It integrates the Internet network as the bank’s network alternative that is safe, reliable, and cost-effective. It also enhances the bank’s ability to provide products and services based on the Internet of Things (IoT).

- BNI took the initiative to explore Blockchain technology and seek ways to incorporate it into its digital technology stack for the bank’s future growth in its digital business. Several R&D prototypes and blockchain-based digital business models have emerged from this initiative, with the potential to be developed and deployed as part of the bank’s digitisation strategy.

- The bank’s IT infrastructure actively supports the Work-from-Home (WFH) and Split Office programs. It continuously improves the communications network capability and provides supporting infrastructure to the bank’s employees, allowing them to contribute their best wherever they work from.

Some of the bank’s strengths in IT that can support its business are:

- Application programming interface (API), allows third parties such as start-ups and fintech businesses to integrate and collaborate with the bank. Due to this, customers can use the bank’s services securely and in real-time.

- BNI uses a data centre that has the support of a disaster recovery centre to ensure maximum service availability.

- BNI uses the BIMODAL technique, consisting of two independent work techniques that remain cohesive in creating IT solutions. The technique helps the bank provide optimal service.

- BNI has also established the Information Security Unit, which brings together multiple units to retain independence while focusing on reviewing, monitoring, and improving cybersecurity. It also participates in the application, development and operational information security lifecycle, including digital forensics and the handling of cyber-crime situations.

BNI and its ICT contracts

- Collaboration with Sang for Technologies, which specialises in Cloud Computing & Network Security for cloud services

- Partnership with Oceanfrogs for SAP technology

- Use of TCS BaNCS for the automation of cash settlement processes

9 Growth and Innovation Opportunities

- #1 Cost to serve

At the industrial level, BNI faced the challenge of rising operating expenses and declining operating profits. The bank’s operational revenue did not grow in 2020. However, operating expenses did, with provision for impairment losses rising by 155.6 per cent as a mitigating mechanism for industries affected by COVID-19. Due to the less-than-optimal revenue growth resulting from the pandemic, the bank’s Cost to Income Ratio (CIR) went from 43.9 per cent in 2019 to 44.2 per cent in 2020.

On the other end, the bank cut down on its operating expenses on personnel cost in 2020 to USD 69.8 million from USD 72.9 million in 2019. This cost reduction was mainly because of a marginally high cut in bonus incentives, physical training and development programs. On the other hand, salary and welfare assistance continue to increase compared to 2019. The bank also incurred an increase in general and administrative expenses and technology expenses. Technology expenses in 2020 were USD 96.2 million compared to USD 87 million in 2019.

While the bank is making efforts to become digitally efficient internally and externally – it must take stringent measures to manage its operating revenues. With skimmed net interest margins and the macro-economic characterisation of low-interest rates, BNI can concentrate on the following significant areas to optimise cost efficiency:

- In a low-interest-rate environment, BNI should detect payback risk in loans and attrition risk in deposits to manage a good net interest margin. In addition, BNI can use predictive behavioural models to continuously adjust the bank’s interest-rate risk estimates and hedging strategies.

- The bank can focus on non-interest income and complementary revenue streams to offset the impact of substantial impairment costs.

- BNI can apply RPA-enabled audit trails for red-flagging any high-cost inflexions by implementing transaction-level transparency.

- #2 Transformation of the branch and branch networks

The bank deployed BNI Sonic, a Digital Customer Service Machine, at numerous key locations, both in-branch and off-branch. Totalling 126 machines, the initiative provided convenience to clients and prospective customers seeking open self-service accounts. In addition, BNI has installed 182 Cash Recycler (T-Care) Tellers across 91 (ninety-one) branches.

From 2019 to 2020, BNI reduced its branch network. It closed 29 branches and 429 ATMs, thereby reducing the cost to maintain the physical network from USD 214 million in 2019 to USD 172 million in 2020. This move provides a 20% reduction in the rental and maintenance cost of branch networks. The bank should continue its efforts to reduce any non-performing branches or ATMs and focus on transforming the network through:

- BNI can replace Cash Recycler Teller with Interactive teller machines (ITMs) by delivering the same services without the requirement for in-person tellers. ITMs make it easier for consumers to make deposit withdrawals, and helps them serve transactions and cash deposits more quickly.

- The bank should transform high business volume and high-customer-headcount branches into flagship digitalised community hubs that enhance the in-branch experience and redefine customer engagement. In order to accomplish this, BNI should:

- Increase the capability of digital customer service machines – Many services done over the counter can be moved to BNI Sonic, reducing the need for human tellers to work in bank branches. Furthermore, smart branch technology enables a personalised sales strategy and 24/7 access to the bank branch.

- It can establish an omnichannel user experience, one that will link BNI Internet Banking, BNI Mobile Banking and physical branches with Virtual Assistants and other automation processes. This holistic channel will provide customers with a consistent experience – whether they are online, on a mobile device, or at the branch. It will also result in higher efficiency at the bank branches.

- Since BNI is already making headway with the virtual assistant application and its digital account opening service with face recognition technology, they can open up smaller, completely self-serviced ‘robo-branches’. It will help to expand the bank’s physical footprint. While bank staff are a necessity in high-traffic, high-visibility urban locations, BNI can establish fully self-serviced branches for greater physical footprint penetration at lower costs. These branches will be able to provide complete services through video conferencing.

- Community centre- There is a need to adopt a branch model that is more appealing than the conventional one. To add delight, branch visits should go beyond processing transactions and resolving questions. BNI can transform its traditional branches into community hubs, where people can socialise, relax, and bank – all at once.

- #3 Customer experience

The bank has made massive headway in delivering a seamless customer experience by investing in technologies such as a Virtual Assistant Application, which works with Artificial Intelligence (AI), Voice Command and NLP.

The bank can further leverage its capabilities through AI and machine learning (ML) and can work in these areas to optimise the customer experience journey:

- BNI provides customer support 24/7. It can, however, work on the day complaint resolution by prioritising Chatbots, virtual assistants, and video conferencing to minimise the turnaround time from 5-20 days to about 1-2 days.

- Personalised insights: Under its existing digital framework, the bank has heavily focused on including features that simplify transactional banking for customers, such as a virtual assistant. The bank should invest towards understanding its customer’s behaviour patterns, life journey needs and spend on Al and ML tools. An expanded understanding could aid in creating unique persona-based product packages, such as:

- Providing Personalised Product Stack/Portfolio – gives each consumer a personalised experience by addressing every key touchpoint.

- Customised offer – based on the next best recommendation model

- Individualised goal – transparency and clearly stated goals, founded on previous interactions with customers

- Personalised tracking – ease of engagement

- Insights for customers into their saving and spending patterns with specific recommendations to help them meet their financial goals

- A gamified user interface to make the customer experience interactive rather than monotonous

- Improve the capabilities of its virtual assistant to handle front-end customers

- Providing Personalised Product Stack/Portfolio – gives each consumer a personalised experience by addressing every key touchpoint.

- #4 Business segment expansion

The demand for working capital is bigger than ever as SMEs enter the COVID-19 recovery stage. BNI has come up with the e-Lo BCM app, which can accelerate a credit process up to USD 214,000 and SmartCA for credit up to USD 1.74 million for MSMEs. They also came up with the BNI Move application to help MSMEs to have more accessible financing. BNI can further work on its SME financing strategies:

- Identify and establish a line of credit for SMEs that are first-time borrowers who do not have access to typical bank lending.

- Develop business advisory and management solutions to help SMEs make informed investment and banking decisions using digital platforms.

- Work with e-commerce websites to provide credit to small businesses looking to access the Indonesian market.

- Reduce merchant interchange reimbursement rates and put out strategic card acquisition and usage initiatives, including reduced merchant discount rates.

- Provide personal and business overdraft facilities, along with basic lending services to the SME sector.

- #5 Employee experience and productivity

BNI has made significant investments in employee development and offers a flexible work atmosphere. However, the bank should consider offering the following services:

- Clearly define the expectations for all senior leaders to build a culture of clear accountabilities in its divisions.

- Design personalised employee upskilling programs based on the employee level, and adopting effective leadership development coaching to prepare them for future roles.

- Expand its employee wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs.

- Create a platform or forum where employees can reach the BNI leaders easily. They can then have face-to-face discussions with leaders and influential external speakers, share their aspirations and extend their horizons beyond the workplace.

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Giving employees the option to work on cross-department projects for lateral career advancements

- Periodical career breaks and approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food and medical support work, as well as cleaning drives

- Provide hassle-free student loans to new hires for controlling attrition rates among the said hires, hence increasing employee loyalty

- #6 Migration of workload to the cloud

BNI uses both public and private cloud for application deployment, which is both cost and time efficient. It has also improved its cloud capability in support of Platform-as-a-Service (PaaS) technology. However, the bank can amplify its cloud capability by using these strategies:

- BNI should use a cloud-based platform to streamline various talent management and HR-related tasks.

- In order to increase efficiency, cloud adoption improves a variety of additional activities beyond the customer and employee experience. The bank can extend data storage and data-driven activities across security, regulatory compliance, auditing, and pan-organisation communication pipelines to modernise its overall operating model.

- The bank’s long-term strategy should be to move most of its operations to the public cloud. This move enables BNI to secure end-to-end encryption on all their confidential data in the cloud, as well as achieve higher scalability and cost-efficiency.

- #7 Neo banking

BNI has added significant features into its mobile banking app to make it more appealing to millennials. Still, it needs a transformational neo banking strategy to keep pace with other rising neobanks in Indonesia. BNI can concentrate on launching a digital spin-off to position itself optimally in the millennial and Gen Z customer segments by:

- Collaborating with a suitable fintech firm to effectively position themselves among millennials.

- Strengthening its in-app virtual assistant’s ability to deliver proactive notifications, budgetary recommendations, as well as lending and investment choices to customers.

- Attempt to hyper-personalise its products to fulfil customers’ unstated and hidden demands.

- Introduce customised debit cards, credit cards, and virtual cards

- Introducing bite-sized loan and investment solutions, giving customers more flexibility when navigating through product possibilities.

- Gamifying numerous consumer touchpoints. These include awarding badges for increased product usage, providing loyal customers with discount coupons, creating a leader board between friends and co-workers based on product purchases, and showcasing trending products.

- #8 Artificial Intelligence (AI) in everything

BNI is at an early stage of adopting artificial intelligence (AI) into its business model. As in the early stage of adoption, the bank should begin with:

- Automating labour-intensive back-end and iterative daily tasks like customer onboarding, document collation, book-keeping, sales recording, etc., through RPA. This automation will reduce labour redundancy and increase the overall operational efficiency of the bank.

- A sophisticated and forward-looking credit profiling method for business banking customers. It uses predictive analytics to assess loan credibility beyond financial statement analysis. Other essential criteria that can be a part of the profiling mechanism include economic KPIs, market and industry trends, bank and system facility overviews, and more.

- Use of AI and ML at various customer touchpoints such as digital biometric customer verification for customer profiling and identification of potential customers for cross-selling and upselling products and solutions.

- Leveraging its data analytics capabilities to seek contextualised data insights that the bank can use to innovate its product offerings and delivery channels.

- #9 Society and planet contribution

BNI believes that augmenting sustainability is a critical component of a development that is only focused on economic factors while ignoring environmental and social concerns. Therefore, its sustainable development strategy focuses on three aspects – people, profit and the planet.

BNI has done well in some aspects with its sustainable financing initiatives, with a total sustainable portfolio of business activities of 41.2% from the past two years. But BNI can work more towards their Go Green program, as their energy consumption went up from 37,674,580 Kwh in 2019 to 41,806,992 Kwh in 2020. Therefore, BNI should seek to reduce its energy usage and carbon footprint by using these measures:

- Utilise energy-efficient devices by making one-time investments and saving costs in the long-term

- Use excess energy during low or off-peak times to decrease energy usage

- Reduce its carbon footprint by switching to pulper cards, eco ink and carbon control press machines

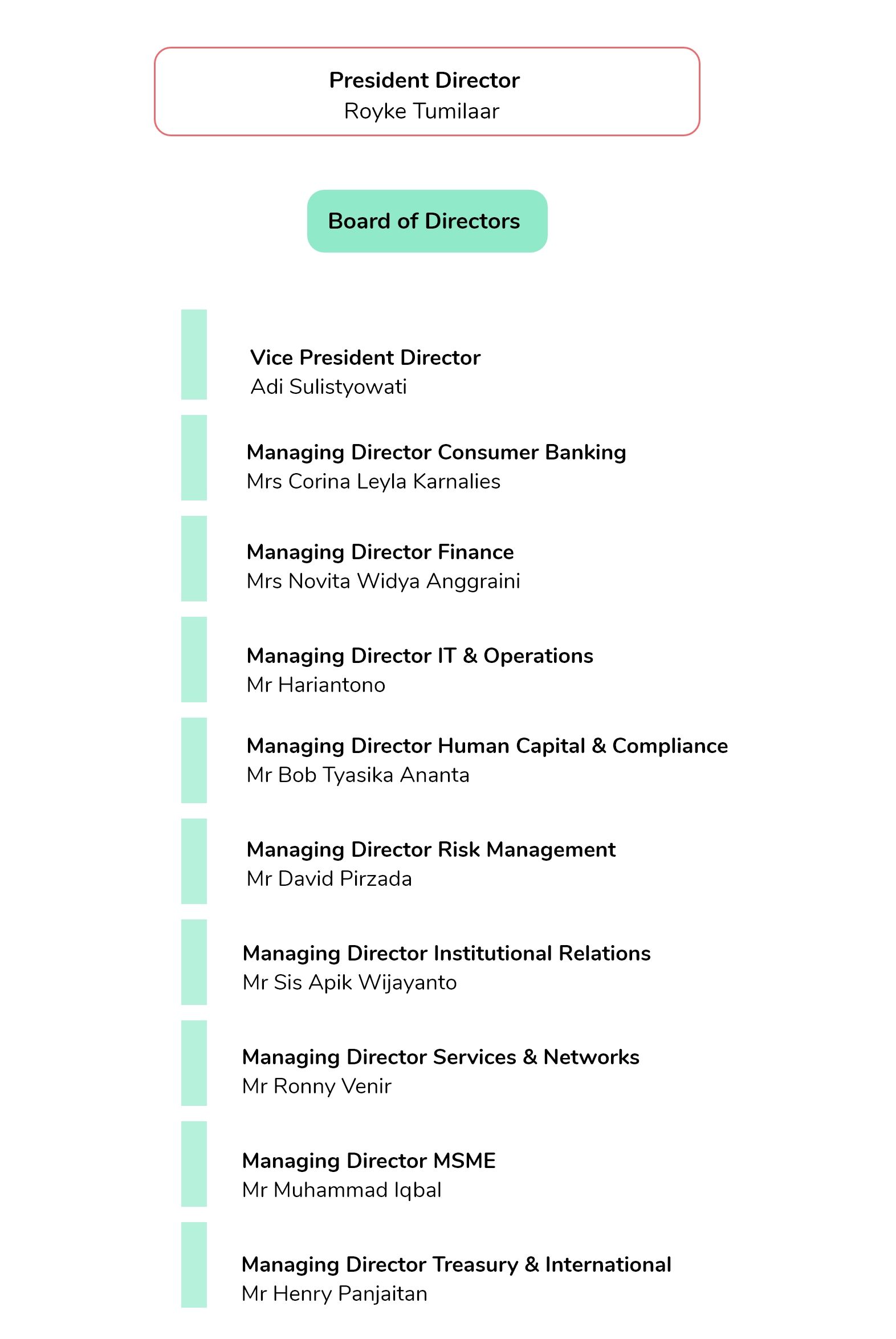

Organisation structure: Leadership

Executive Profile

Royke Tumilaar

President Director

He is the President Director and is responsible for the Internal Audit Unit, Corporate Communication & Secretarial Divisions, as well as the Strategic Planning Division of the company.

Quotes

- Business Strategy, Annual Report 2020

In 2020, we focused on developing the Bank’s digital business model and an ecosystem that places specific emphasis on improving productivity, asset quality, efficiency, and inter unit collaboration.

- Sustainability goals, Sustainability Report 2020

While we are in our best endeavours to pose mitigation acts towards the pandemic issue, we have not failed to remember BNI’s commitment as “First Movers” in sustainable finance to continue working for the achievement of sustainability goals.

Adi Sulistyowati

Vice President Director

He is the Vice President Director of the company and is involved in the Policy Governance Division of BNI.

Mrs Corina Leyla Karnalies

Managing Director Consumer Banking

She is the Managing Director of the company’s Consumer Banking Division and is responsible for the following divisions – Consumer Product Management, Card Business, Wealth Management and Marketing Communication.

Mrs Novita Widya Anggraini

Managing Director Finance

She is the Managing Director for Finance and is responsible for the following divisions – Budgeting and Financial Control, Asset Management and Procurement, Data Management & Analytics and Subsidiary Development.

Mr Hariantono

Managing Director IT & Operations

As the Managing Director of IT & Operations, he is responsible for the Information Technology Solutions Division, Information Technology Operations Division and the Information Security Unit.

Mr Bob Tyasika Ananta

Managing Director Human Capital & Compliance

He is responsible for Compliance, Legal, Human Capital Management as well as the BNI Corporate University.

Mr Silvano W. Rumantir

Managing Director Corporate Banking

He is responsible for the Corporate and Multinational Business Division as well as the Syndication and Corporate Solutions Division.

Mr David Pirzada

Managing Director Risk Management

He is responsible for the Bank’s Risk Management Division, Corporate Credit Risk Division, Medium & Small Business Credit Risk Division, Consumer Credit Processing & Billing Division and the Anti-Fraud Unit.

Mr Sis Apik Wijayanto

Managing Director Institutional Relations

He is involved in the Division of Institutional Relations, Division of BUMN & Government Institutions and the Value Chain Management Unit.

Mr Ronny Venir

Managing Director Services & Networks

He is responsible for Network Management Division, Sales Division, Quality of Service Unit, Customer Service Center Unit & Business Optimisation.

Mr Muhammad Iqbal

Managing Director MSME

He is responsible for the Medium Business Division and the Small Business Divisions of the company.

Mr Henry Panjaitan

Managing Director Treasury & International

He is responsible for the International Division of BNI.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

PT Bank Negara Indonesia Tbk, (2020, December 31). Annual Report 2020.

https://www.bni.co.id/Portals/1/BNI/Perusahaan/HubunganInvestor/Docs/AR-BNI-TB-2020-English.pdf

PT Bank Negara Indonesia Tbk, (2020, December 31). Sustainability Report 2020.

https://www.bni.co.id/Portals/1/BNI/Perusahaan/HubunganInvestor/Docs/SR-BNI-2020-US.pdf

Bloomberg L.P.PT Bank Negara Indonesia Tbk financial statement analysis in USD. Retrieved June 24, 2021 from https://www.bloomberg.com/quote/BBNI:IJ

Wall Street Journal. PT Bank Negara Indonesia Tbk financials. Retrieved June 24, 2021 from https://www.wsj.com/market-data/quotes/ID/XIDX/BBNI/financials/annual/income-statement