Company Insights

twimbit Purpose Index

Bank Rakyat Indonesia (Group Financials)- An overview as of 31st December 2020

| Bank Name | PT Bank Rakyat Indonesia (Persero) Tbk |

| Headquarters | Jakarta |

| Operating income (31st December 2020) | USD 7.8 billion |

| Group net profit (31st December 2020) | USD 1.3 billion |

| Total Assets | USD 108.32 billion |

| Employees | 88,184 |

| Countries of operation | 6 |

| Number of branches offices | 462 |

| Computers and software expenditure (31st December 2020) | USD 1.06 million |

| Number of customers | Not available |

| Market capitalisation (31th December 2020) | USD 29.3 billion |

| Operating revenue CAGR growth (2016-2020) | 5.6% |

2. The IDR to USD dollar conversion rate used is 0.00007165.

Shareholder Value (31st December 2020)

| Return on Equity (31th December 2020) | 11.05% |

| Total Shareholder Return (1-Year) | 30.8% |

| Net Income Ratio | 17.17% |

| Common Equity Tier 1 Ratio | 20.09% |

| Price Earnings Ratio (as of 31th December 2020) | 2.596% |

Awards

| 2020 | The Asset Best Issuer for Sustainable Finance Best Sustainability Bond The Banker Top 1000 World Banks: BRI ranked 1st in Indonesia Top 1000 World Banks: BRI ranked 112th in the global ranking (Highest in Indonesia) Forbes magazine 1st Indonesia’s Largest Public Company Global 2000: The World’s Largest Public Companies (Rank: 347th, Highest in Indonesia) The Asian Banker The Best Retail Banking in Indonesia |

BRI and its strategic focus areas

- Business strategy

The bank has formulated its business strategy in accordance with the macroeconomic forecasts post the Covid-19 pandemic. Therefore, its working plans for 2021 include selective growth projections such as:

- Asset Quality Improvement– Optimising the post-pandemic recovery rate by improving credit quality and monitoring non-performing loan restructure to minimise allowance for impairment loss.

- Strengthening BRI Group Synergy

- Enhancing business and non-business synergy between BRI (the parent company) and its subsidiaries and between subsidiaries through several programs.

- Improving services and enhancing transaction convenience to facilitate low-cost funds acquisition

- Tailoring products to suit millennial needs who are tech-savvy and unbanked

- Increasing transactions

- Boosting transactions to increase fee-based income and CASA potential.

- Developing value chain business and transaction banking in all segments and implementing digital banking services to optimise fee-based income.

- Micro-business strategies

- Efficiency through CASA improvement and operational efficiency of business processes

- Assets Quality through loan recovery improvements

- Community Development through empowerment and increasing the capacity and capability of Micro Business customers

- Carry out “SOLID Survival Strategy” by increasing fee-based income, strengthening recovery, expansion into low-risk products and facilitating new growth sources.

- SME business strategies

- Selective growth, focusing on the expansion of economic sectors that are still good and growing in order to maintain loan quality.

- Enhancement of business process digitisation through BRIspot Retail, Loan Invoice Financing and the Sales Planning System.

- Optimising the use of BRIspot Small Loan to increase the effectiveness and productivity of loan.

- Supporting SME upgrades through boosters programs.

- BRILink (branchless banking service) Strategies

- Improving the quality of agents will be the key to achieving of BRILink targets in 2021. BRI continues to show commitment in growing the availability of banking and financial services, targeting to cover at least 75.6% of the total villages in Indonesia.

- A cooperation between BRI, Pegadaian, and PNM is in place, integrating state-owned enterprises (SOEs) in Ultra-Micro (UMi) financing through the distribution of UMi products at BRILink Agents. There is also data exchange to strengthen analytics and co-location to increase coverage and cross-selling of products through digital platforms.

- BRILink will also continue to improve the quality of services by adding product and service features. It will also maximise collaboration with startups that have services and products worth selling and needed by the people, along with digital business penetration.

Business strategy initiatives in 2020

- Microbusiness innovation initiatives in 2020

- Kredit Ekstra Cepat (KECE)- BRI launched this program to upgrade Lower-Micro entrepreneurs to Micro entrepreneurs. By December 20200, it provisioned to more than 36000 debtors

- Integration of the Micro Insurance Sales Platform

- BRI Micro-Business collaboration with e-Commerce and fintech companies – In order to increase the scope of productive loan marketing of the Micro segment, BRI collaborated with

- some renowned E-Commerce and Fintech businesses, such as Amartha, Modalrakyat, Grab, Gojek, Tokopedia, and Shopee. As a result, in less than six months in 2020, this collaboration successfully delivered productive Micro segment loans to more than 525 debtors.

- BRILink Initiatives in 2020

- In 2020, BRILink implemented a delivery channel expansion strategy by focusing on the quality of BRILink Agents utilising BRIsat (the bank’s very-own satellite) technology to reach areas where cellular service did not cover as yet.

- BRI also standardised the devices used by agents that rely on Android-based operations.

- It performed several strategic initiatives, including the development of digital ecosystems to improve effective and efficient services, especially for Micro customers.

- The Micro financial ecosystem solution can perform end-to-end purchase and payment transactions for Micro Business players, due to the convenient account opening process and loan referrals on the BRILink application.

- Customer Experience

- Digitalisation and automation of complaint management– The bank aims to automate transaction analysis, investigation, and settlement processes to minimise turnaround times for customers.

- Digital onboarding– The bank launched customer onboarding on the digital savings platform to accommodate easy savings account openings. The service uses two security technologies, namely face recognition and digital signature, saving customers the time from physically visiting a branch office. The platform also allows customers to do immediate transactions by automatically linking the customer with the BRImo app.

Customer Experience initiatives in 2020

- WeAreShine Service– Aims to maintain consistent service quality in every touchpoint, including BRI branch offices, contact centre, and electronic channels.

- Complaint Management– Convenient, quick, and accurate are the added values from the service recovery that BRI provides for customers who experience trouble in their transactions.

- Development of “Sabrina”, the Artificial Intelligence Chatbot– An artificial intelligence (AI) chatbot, Sabrina provides information on products, promo and events, and BRI offices. It also connects customers to agents in the contact centre. Sabrina aims to ease customers in communicating and getting information on BRI.

- Employee Experience

The bank’s employee strategy focuses on strengthening its employer brand to attract and retain talent. The bank wants to retain its position as the place to work for young professionals with superior competencies:

- Increase employee engagement with a clear rewards system and career pathway.

- Use People Analytics and data to support Human Capital management decisions.

- Improving the quality of performance in 2021 is a major concern in facing increasingly fierce business competition and recovering from COVID-19. Therefore, BRI needs to establish a more advanced and integrated human capital management system to become a World-Class Human Capital System and Practice. In order to support business performance, BRI Human Capital strives to become a strategic business partner by providing a reliable and responsive system that can sustain any challenge faced by the company.

- As BRI deals with various disruptions, cultural transformation becomes one of the keys to the success of its human capital management. Therefore,

- BRI consistently carries out cultural transformations to create an internalisation of work culture, at every level.

Employee experience initiatives in 2020

| BRILiaN Banking Officer Program (BBOP) | A recruitment and education program to prepare new employees at the Corporate Title Assistant level to be able to deliver optimal performance. |

| BRILiaN Future Leader Program (BFLP) | Educational programs to prepare employees from external sources at the Corporate Title Assistant level to be able to deliver optimal performance. |

| BRILiaN Next Leader Program (BNLP) | Educational programs to prepare employees from internal sources at the Corporate Title Assistant level to be able to deliver optimal performance. |

| BRILiaN Leader Development Program (BLDP) | Educational programs to train employees to become great leaders through sustainable and comprehensive leadership development. They emphasise on character building, awareness of the nation, global insight, business and banking insights, as well as technology insight. |

| BRILiaN Specialist Development Program (BSDP) | A sustainable and comprehensive technical competency development education program that focuses on attaining the required competency, knowledge, and skills to become specialists in particular fields, as needed by BRI. |

| BRILiaN Global Development Program (BGLP) | A special development program to prepare Top Talents who are members of BRILiaN Society Member (BSM) Band 3 (Corporate Title at Assistant Vice President / Senior Manager level) and Band 4 (Corporate Title at Manager level) as prospective Global Leaders with competence and global business insight. |

| BRILiaN Society Elite Program (BSEP) | A special development program to prepare Top Talents in the BRILiaN Society Member (BSM) Band 2 (Corporate Title at the level of Vice President) and Band 1 (Corporate Title at the level of Executive Vice President / Senior Vice President) to assume more complex Leader roles. |

| BRILiaN Bright Scholarship Program (BBSP) | An education program for BRI Permanent Employees to pursue a Masters’ Degree, sponsored by the bank. |

| BRILiaN Leader Retirement Program (BLRP) | Prepares employees who are about to enter retirement by providing them with the knowledge, insights, and skills needed to sustain retirement. |

The bank has also deployed technology to enhance its human resource management processes. The BRISTARS integrated application that implemented operational efficiency contains the following integrated applications:

- e-Recruitment, a facility for prospective employees to join BRI via this online job application channel

- Digitalised assessment app, online employee competency assessment.

- e-Mutation, the automated processing of employee transfer between BRI work units.

- Automated employee database

- e-Leave, leave application submission and online approval process by supervisors.

- e-SPJ, paperless business trip application for trip documentation and approval of decision-makers.

- e-Loan Facility for employees to apply for a loan online.

- e-Health Insurance, an online facility for employees to apply for the reimbursement of medical expenses.

- e-Overtime, a facility to issue overtime work orders online and automate overtime payments

- Society and planet impact

The strategy BRI has in implementing sustainable finance aims to ensure that BRI runs responsibly for the long term. Its sustainable finance observes the following principles:

- Energy-saving, environmental conservation, attention to social aspects and good governance.

- Design communications and public relations strategy to support the bank’s corporate image through energy efficiency

- Undertake operational initiatives such as paperless, e-office, green building, green IT infrastructure, digital operation, E-Learning, facilitate bike parking “Bike to Work” and others.

- The bank plans to collaborate with Indonesia’s School of Business and Management ITB to set up venture capital courses for the institutes. These courses will help students understand basic principles and give them exposure of the start-up ecosystem. This will also create fresh job opportunities for the students and thus bring a paradigm shift in the economy.

Initiatives by BRI for society and planet impact in 2020

- First mover on sustainable finance in Indonesia- The bank, along with seven other banks, participated in establishing the Indonesian sustainable Finance Initiatives

- Lending for sustainable business activities- The loan portfolio BRI has for sustainable business activities increased by 14.1% Y-o-Y from USD 35.3 billion (57.3% of total loans composition) in 2019 to USD 40.27 billion (63.9% of total loans composition) at the end of 2020.

- Sustainability bonds- The bank issued sustainability bonds worth USD 500 million under its commitment to include ESG in bank financing activities. It allocated the proceeds from these bonds to social and green projects.

- Community empowerment- The bank introduced ‘green business’ related to education and training activities conducted by 5 Rumah Kreatif BUmN (RKB). BRI conducted 476 RKB trainings in various cities such as Malang, Jakarta, Jogja, Bandung and Solo.

Digital Strategy

In 2016, the bank initiated its 2016-2020 corporate plan, BRIVolution, with the objective of digital and cultural transformation. Its digital strategy follows a hybrid company model, focusing on innovation driven towards customer experience. The bank’s digital strategy theme for 2021 is to do more with less, through an automation and data-driven culture.

- Digitising core– Digitise existing services and transactions (business process engineering)

- Optimise existing channels

- Integrated digitised operationss

- A simplified and standardised system

- Digital ecosystem– Build an ecosystem to offer products and services beyond the core business.

- A digital platform for business transactions

- Build a new business model

- Partnership/collaboration with fintech and e-Commerce

- New digital propositions– Create and launch an independent greenfield digital bank in Indonesia.

- A mobile-first channel

- Fully digital products for untapped markets

- Building new digital capabilities

| GRAND STRATEGY: | 2020 | 2021 | 2022 |

| Facilitate breakthrough innovations | Innovative Digital & Open Financial Solution | Digital Financial Supermarket | The Most Innovative Digital Financial Ecosystem in Southeast Asia |

| Build a resilient IT platform | Robust and Secured Digital Architecture and Infrastructure | Highly Scalable, Open Banking capabilities and a Composable Architecture | World-Class Digital Infrastructure |

| Create a data-driven organisation | Improved Data Management Process and Big Data Analytics | Decisions driven by data analytics | World-Class Data Company |

Digital strategy Initiatives for 2020

- BRILink Mobile– Following the growth of the Internet of Things, BRILink Agents have started to drive the acquisition of agents that operate with an Android-based mobile platform, BRILink Mobile. It is secure, efficient, and reliable. BRILink Mobile also expects to attract the interest of millennials in supporting financial inclusion. In this platform, BRI develops service features and increases back-end reliability. New and innovative services are now available via BRILink Agents, such as referrals for ultra-micro loans and gold savings top-ups, in addition to existing services and features.

- PINANG– BRI, through its subsidiary BRI Agro, launched PINANG, the First Digital Lending Banking in Indonesia. By combining digital technology, PINANG speeds up the application process to disbursement to less than 10 minutes. By using a fast, affordable and secure process as well as a competitive ceiling, PINANG will provide extra convenience for customers to apply for loans.

- BRIMO– BRIMo is an Internet-based digital financial application using the newest UI/UX. It provides attractive features e.g. online opening of accounts, cardless cash withdrawals, and fingerprint or Face-ID logins

- BRISPOT– A mobile-based application with a one-stop service concept for the Account Officer to conduct the end-to-end lending process. This technology significantly shortened the loan process from 2 weeks to two days.

- Pasar.id– This platform is a web-based marketplace developed to arrange the interaction between sellers and buyers of traditional markets digitally.

- BRIZZI– An electronic money that serves as a payment tool in shopping transactions or other transactions with merchants. All BRIZZI transactions can take place at all merchants using the BRI EDC machine. It also allows top-ups at partner merchants, such as Alfamart, Indomaret, Alfamidi, yomart, etc. In addition, the BRIZZI card can also be used for toll road payments, train ticket purchases, parking payments, and to access public transportation, such as Transjakarta.

- CERIA– is an application on smartphones that provides customers with the ease of obtaining financing in e-commerce transactions. There is a maximum limit of USD 1400. CERIA has taken advantage of digital verification, credit scoring, and digital signature technology. It can process loan applications in less than 10 minutes with choices of loan tenors for up to 12 months. The loan application can be done digitally without direct interaction with a branch office or face-to-face meetings with bank employees.

- Traveloka Paylater Card– It is a synergy of BRI with Traveloka Paylater. It creates a comprehensive digital payment ecosystem. Traveloka PayLater Card registration can be done easily by customers from home and has the support of a quick verification system. The loan approvals go through an efficient and sophisticated credit assessment process.

- Indonesia Mall– The bank started an online marketplace, providing the MSME communities with the opportunities to go digital and sell their products in the wider market.

- Additional services and features under its ecosystem platform include BRISmart Billing and BRImola LPG Gas 3 kg Ordering System.

- Partnership ecosystem

- P2P Partnerships

- Investree- BANK Rakyat Indonesia (Bank BRI) announced it forged a partnership with Investree, one of Indonesia’s peer-to-peer (P2P) lending marketplaces. The partnership is to support entrepreneurs in the creative industry seeking to secure working capital loans and thrive in the market. The bank’s creative industry lending takes the form of invoice financing, thus not requiring borrowers to put up traditional forms of collateral.

- E-commerce partnerships

- Collaborated with e-commerce platforms Shopee, owned by Sea Group.

- Tokopedia is a government-sponsored, subsidised loan framework where users can apply for BRI loans through these platforms.

- Ride-hailing partnerships

- Grab- The bank partnered with Grab to launch a low-interest loan for the latter’s drivers and merchants affected by the COVID-19 pandemic. The drivers are eligible for a low interest up to USD 336, and merchants are eligible for a micro-credit program worth up to USD 3360.

- Gojek- BRI partnered with Gojek for its drivers and food merchant partners affected by the pandemic. As a result, the drivers are eligible for a low interest up to USD 336, and the merchant partners can borrow a maximum of up to USD 1400.

- P2P Partnerships

IT Strategy

BRI continues to improve the capability of its IT technology to make it more scalable, reliable & secured to support the bank’s business growth by developing:

- BRI is preparing its data centres to accommodate new technologies, such as virtualisation and private cloud.

- The bank aims to strengthen IT infrastructure to manage operational risks arising from insufficient internal processes, human resources, systems or external events. It is adopting technologies such as big data analytics equipped with Fraud Detection System

- and Early Warning System features that can proactively anticipate fraudulent behaviour and launch preventive measures.

- The bank is also constantly improving its IT security capability by developing big data and AI-based fraud detection systems.

- BRI has carried out several initiatives to excel as a data-driven organisation.Among others, its implementation of master data management aims to strengthen the bank’s capability in managing big data groupwide.

- BRI also continues to strengthen data usage by constantly building its intelligent data analysis for business development, utilising big data and AI technology.

IT Strategy initiatives in 2020

- BRIBRAIN– An AI developed to record, process, and consolidate all information from various sources. BRIBrain is the ‘brain’ for BRI, in taking accurate and precise business decisions to enhance the quality of products and services offered through its application development.

- BRI API- An open-banking platform that enabled BRI to cooperate with fintech and e-commerce in a more convenient and faster way.

BRI and its ICT Contracts

- Partnership with Apigee for agent onboarding

- Collaboration with Cloud vision API for customer verification

- Partnership with Infosys Finacle for digital banking support

- Collaborated with Everest as the bank’s partner in life insurance market development

- Collaborated with FWD insurance as its SME lending partner

9 Growth and Innovation opportunities

- #1 Cost to serve

- The net profit for BRI saw a significant decline, as it accounted for USD 1.337 billion in 2020, decreasing by 45.78% compared to USD 2.465 billion in 2019. This is because the bank increased its allowance for impairment losses as an effort to mitigate the possible deceleration of credit quality due to Covid-19.

- The bank’s cost to income ratio (CIR) recorded a 13.4% rise from 40.03% in FY2019 to 45.4% in FY2020. This growth was primarily due to lower Net Interest Income, resulting from the slowdown in loan growth caused by the pandemic.

- The bank’s focus for 2021 is to enhance its total income by emphasising improved fee-based incomes. It aims to do so by continuously improving digital and transactional banking activities for corporate customers. However, the bank should also focus on identifying repayment risk in loans and attrition risk in deposits to strengthen the net interest margin:

- The bank can use predictive behavioural models to revise its interest-rate risk models and hedging strategies continuously.

- Increase focus on non-interest income and complementary revenue streams to offset the impact of high impairment charges.

- The implementation of transaction-level transparency through RPA-enabled audit trails for red-flagging any high-cost inflexions.

- The bank also saw a steep rise of 5.2% in its manpower expenses from FY2019 to FY2020. This incline was primarily due to an increase in the number of employees following the bank’s business expansion strategy. Therefore, when further expanding its scale, BRI should focus on:

- Automating labour-intensive back-end and iterative daily tasks, like document collation, book-keeping, sales recording, etc., through robotics process automation. This automation reduces labour redundancy and increases overall operational efficiency.

- Using natural language processing (NLP) in research and analysis, customer document processing, and customer service activities such as its virtual assistant, Sabrina.

- #2 Transformation of the branch and its branch networks

BRI has a well-optimised branch network, consisting of Retail Channels (467 Branches, 611 Sub-Branches, 547 Cash Officees, 57 E-Buzz), microchannels (5,382 BRI Units, 504,233 BRILink Agents), and e-channels (16,880 ATMs, 5,809 CRMs, 198,785 EDCs, 20 Hybrid Machines, 100 Self-Service). The bank’s BRILink Agents are making way for financial inclusion in the country by adopting a branchless banking model. The bank can further adopt the following strategies for branch transformation:

- As the bank’s objective is to optimise the branch network, they can convert its mini mobile branches, E-Buzz, into self-serviced ‘robo-branches’. The bank can build these fully digitalised self-serviced branches for greater penetration via physical footprint at reduced costs. In addition, these branches can have full services available through video conferencing.

- In 2020, the bank saw a sudden spurt in digital transactions, which affected conventional e-banking transactions such as at ATM. The number of ATM transactions grew by only 0.59% (Y-o-Y), from 3.72 billion in 2019 to 3.75 billion in 2020. Since digitalisation is the future for the banking industry’s physical infrastructure as well, cash offices and ATMs can make way for Interactive teller machines (ITMs). These ITMs are capable of providing the same services without the need for in-person tellers. They can also contribute to reducing a branch’s size and consequently lower real estate costs for the bank.

- Revamping the bank branch into a community hub, where individuals can connect with executives and socialise. They will also have access to all banking services and facilities. Some of the options are cafes, lounges, and pop-up stores.

- Within the branches, the bank should increase the usage of tablets so that the tellers can provide personalised insights to customers.

- #3 Customer experience

- The bank’s existing digital framework primarily focuses on supporting customers with their transactional needs in order to conduct quick and convenient digital banking. However, BRI should focus on building personalised customer engagements on both physical and digital platforms.

- It must invest in understanding the customers’ behavioural patterns, life journey needs, and spending areas through AI and ML tools to create unique persona-based product packages.

- Moreover, as the bank’s data centres are accommodating new technologies such as virtualisation, it can go further to integrate Augmented and virtual reality (AR/VR) into its BRIMo app. This change will give the customer the experience of a virtual digital bank using AR/VR glasses.

- This integration can help the bank in engaging customers by providing personalised insights and attention with virtual assistance. Customers could have a 360-degree view of the branch without visiting a physical branch location. These virtual branches will be able to offer the same services but in an exclusively VR environment. It will enhance customer experience and reduce costs for the bank, as it no longer needs to invest in physical locations.

- BRI can also use AR in its mobile banking app to locate ATMs and visualise financial data for better budget management.

- #4 Business segment expansion

- The bank’s Wealth Management segment under its retail banking services showed a strong performance in FY2020 amid the pandemic. The 13.42% rise in Asset Under Management (AUM) and a 28.46% (Y-o-Y) growth in fee-based income from investment and bancassurance products drove the incline.

- In order to expand this line of service in 2020, the bank focused on preparing reliable and professional Relationship Managers (RM) from BRI Priority Service Center to provide advisory services. However, the bank should now focus on reinventing its wealth management business by pushing towards digitalisation:

- BRI should launch a mobile-based wealth management application for its high-net-worth customers to make transactions, monitor investment portfolios, and explore products such as mutual funds and bonds.

- The app should incorporate a digital dashboard with a 360-degree view of the customer’s entire financial situation, incorporating their financial life goals set against their assets and liabilities.

- The bank’s financial advisors should be able to co-browse the customer’s wealth management tool in real-time to provide quicker and more effective services.

- Adopting big data and analytics for providing more accurate data-driven financial advice than based on the human experience of the financial advisor.

- #5 Employee experience and productivity

- The bank has taken various initiatives for development programs for upskilling employees and preparing them to be future bank leaders. However, to prepare its people for the future of work, BRI should also conduct technological development training that focuses on low-code programming, design thinking, UI / UX, data analytics, and machine learning. In addition, BRI should also consider digital training for its senior employees.

- The bank should strengthen its performance-based reward system and career progression mechanism by focusing on people analytics. This step is to check on the unconscious bias that is unfairly impacting promotion and compensation decisions.

- Furthermore, the bank can improve its existing rewards and benefits offerings and financial support by:

- Providing personal development allowances

- Creating a monthly piggy bank for Netflix, Spotify, gyms, etc.

- Building customisable compensation plans to include flexible share incentives, as well as fixed and variable components

- Financial Support for Parents of Children with Special Needs

- Employee volunteering programmes sponsorships

- #6 Migration of workload to cloud

BRI is preparing its data centres to accommodate new technologies, such as virtualisation and private cloud. It has adopted the Cloud Apigee API Management Platform as the bank’s digital nucleus. BRI should consider transitioning further 80% towards the public cloud, depending on government regulations for data management in Indonesia. This transition will allow the bank to achieve greater scalability and cost-efficiency by:

- Integrating its cloud infrastructure by extending data storage and data-driven activities across security, regulatory compliance, auditing and pan-organisation communication pipelines to transform the overall operational model.

- Decreasing data storage costs by reducing the capital expenditure on its in-house physical storage infrastructure.

- Creating a robust, tightly controlled delivery program that allows developers to scale and embed microservices in the cloud architecture.

- Providing complete end-to-end protection for all confidential data stored in the cloud. This protection enables the bank to maintain the customers’ trust and confidence in obtaining, analysing, and sharing their personal information.

- Responding to market shifts, such as black swan events – examples include Covid-19 and the entry of non-bank players to the banking environment with the grant of digital banking licenses.

- #7 Artificial Intelligence (AI) in everything

- BRI has effectively adopted AI into its risk management and fraud detection systems.

- Moreover, the bank also uses BRIbrain, a tool powered by AI and ML technologies, to improve credit scoring and loan approvals by analysing information from various data streams.

- It can further enhance the capabilities of this tool to deploy a forward-looking credit profiling mechanism for business banking customers. This enhancement could incorporate predictive analytics to access loan credibility beyond the financial statement analysis to include other key parameters. Examples of parameters include economics KPIs, market and industry trends, bank and system facilities overview, and more.

- #8 Neo banking

The bank’s branchless banking initiatives have significantly contributed towards fostering financial inclusion amongst the unbanked population in Indonesia. While building upon its BRILink strategies, the bank should simultaneously also consider building a brand image that resonates with the country’s millennial population. The bank needs a transformational neo banking strategy to keep pace with the rising neobanks in the Indonesian market (TMRW by UOB, Digibank by DBS and Jenius by BTPN). BRI can focus on revamping its existing retail banking mobile app, BRIMo, to position itself optimally in the millennial and GenZ customer segment:

- Gamify various customer touchpoints, like awarding badges with the increased use of products, giving discount coupons to its loyal customers, leader board between friends and colleagues based on product purchases, and highlighting trending products

- Add features such as purchasing game vouchers, hotel, train and airplane tickets that appeal to the younger generation.

- To make the app aesthetically more appealing to millennials, BRI could allow for in-app customisation, such as theme settings, quick action menu and shortcuts for easier navigation.

- Unique payment options, such as virtual debit cards and credit cards.

- As the bank provides a smart billing feature to assess the monthly targeted expenditure and integrates an ecommerce shopping experience within the app, it can expand this capability to include other functionalities, such as:

- Budgetary tools for personal financial management

- Evidence-backed recommendations to reduce spending and manage savings

- #9 Society and planet impact

- BRI has undertaken various digital initiatives to reduce paper usages, such as BRISPOT (Digital Loan App), BRIMO (Mobile Internet Banking), BRISTARS (Digital Office), and BRISMART (Digital E-learning System). In addition, it can focus on recycling and upcycling existing waste wherever possible to reduce the burden on landfills.

- The bank’s overall electricity consumption and greenhouse gas emissions are much higher than the industry average in the Asia Pacific. In order to create a meaningful impact and fulfil its responsibility towards society as a stakeholder, the bank should inculcate the following in its sustainability strategy:

- Undertaking new community projects that enable accessibility of basic utilities and social services in rural communities, financial inclusion programmes for the unbanked and underbanked people, as well as health, education, employment, and environmental conservation programmes.

- Financing renewable projects that meet pre-defined sustainability targets and form meaningful long-term partnerships to drive sustainability agenda effectively and comprehensively.

- Building on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid

- Launching supporting projects in impoverished areas, which help to preserve biodiversity and drive reforestation while furthering local economic mobility.

- Using eco-charges, smart sockets, programmable thermostats, and indoor motion sensors to reduce electricity consumption

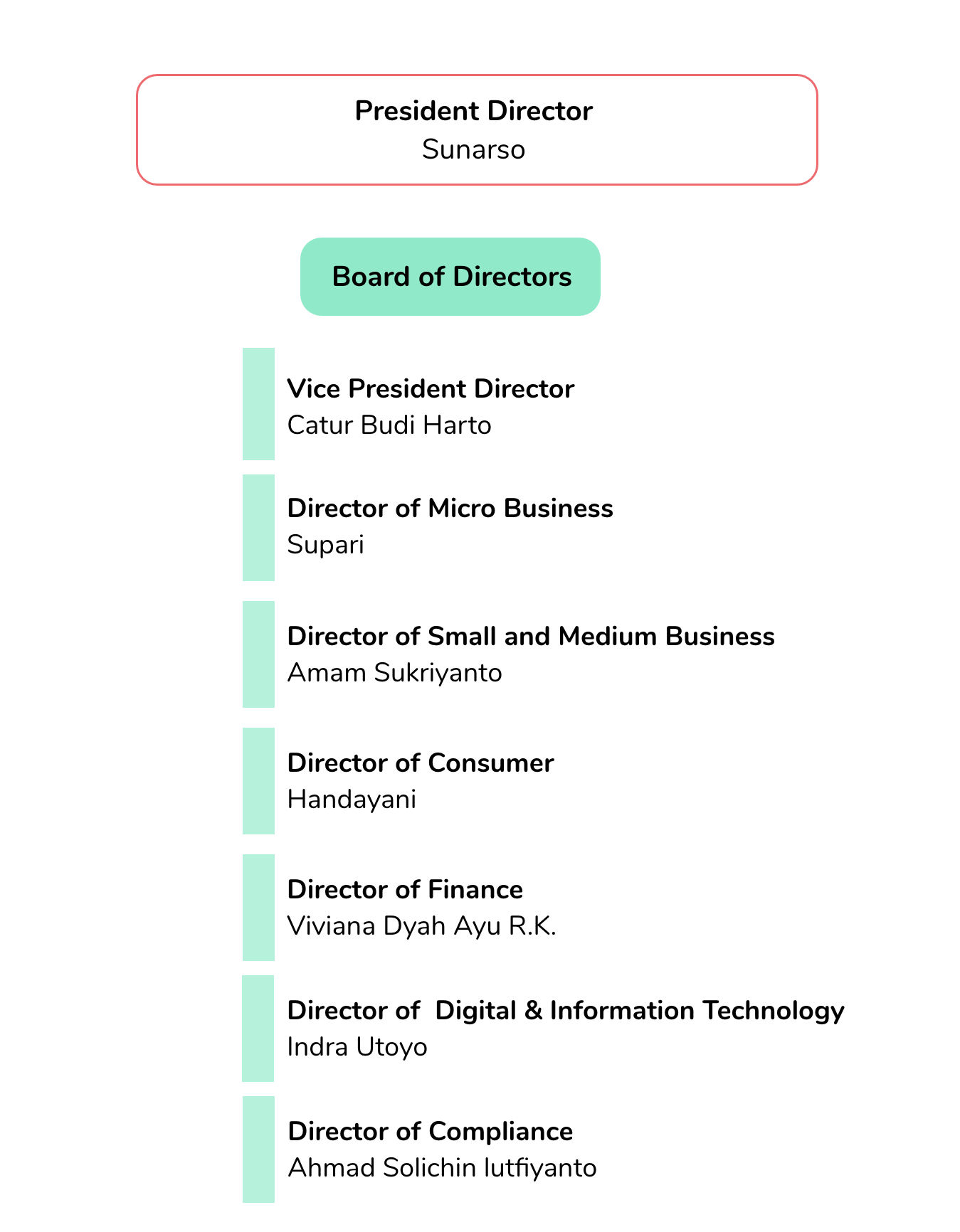

Organisation structure: Leadership

Executive Profile

Sunarso

President Director

He was appointed as the President Director pursuant to the EGMS on 2 September 2019. Previously, he held the position of Vice President Director BRI (2019); President Director of PT Pegadaian (Persero) (2017-2019); Vice President Director BRI (2015-2017); Commercial & Business Banking and Director of Bank Mandiri (2010-2015).

Quote

- Business Strategy (Annual Report, 2020)

Preserving MSMEs became the focus of BRI’s mission during the Covid-19 pandemic. Through restructuring and distribution of various programs from the Government, BRI became the Government’s leading partner in implementing the National Economic Recovery (NER) program.

Catur Budi Harto

Vice President Director

He was appointed as Vice President Director pursuant to the EGMS on 2 September 2019. Previously, he held the position of Director of Small Business and Network PT Bank Negara Indonesia (Persero) Tbk (2017- 2019); Director of PT Bank Tabungan Negara (Persero) Tbk (2016- 2017); and Senior Executive Vice President (SEVP) of PT Bank Rakyat Indonesia (Persero) Tbk (2016)

Supari

Director of Micro Business

He was appointed as Director of BRI for the first term since 22 March 2018 pursuant to the Annual GMS resolution. Before this, Suparithe positions of Director of Retail and Medium Business BRI (2018-2019); SEVP Transformation BRI (2017-2018); SEVP Network Management BRI (2017-2017); and SEVP Consumer SME BRI (2016-2017)

Amam Sukriyanto

Director of Small and Medium Business

He was appointed as Director of BRI for the first term since 21 January 2021 pursuant to the Extraordinary GMS resolution. Previously, he held the positions of SEVP Fixed Assets Management & Procurement Directorate BRI (2020-2021); EVP Corporate Secretary Division BRI (2020); and EVP International Business BRI (2018-2020).

Handayani

Director of Consumer

She was appointed as Director of BRI for the first term since 18 October 2017 pursuant to the Extraordinary GMS resolution. Previously, she held the positions of director of Consumer Banking BTN and director of Commercial PT Garuda Indonesia Tbk.

Viviana Dyah Ayu R.K.

Director of Finance

She was appointed as Director of BRI for the first term since 21 January 2021 pursuant to the Extraordinary GMS resolution. Previously, she held the positions of EVP Subsidiary Management Division, BRI (2019) and VP Subsidiary Management Desk, BRI (2018-2019).

Indra Utoyo

Director of Digital & Information Technology

He was appointed as Director of BRI for the first term since 15 March 2017 pursuant to the Annual GMS resolution. Previously, he held the position of director of Digital & Strategic Portfolio Telkom Group PT Telkom (2012-2017).

Ahmad Solichin lutfiyanto

Director of Compliance

He was appointed as Director of Compliance BRI since 21 January 2021 pursuant to the Extraordinary GMS resolution. Previously, he held the positions of director of Network & Service BRI (2019-2021) and director of Compliance BRI (2018-2019).

Appendix A

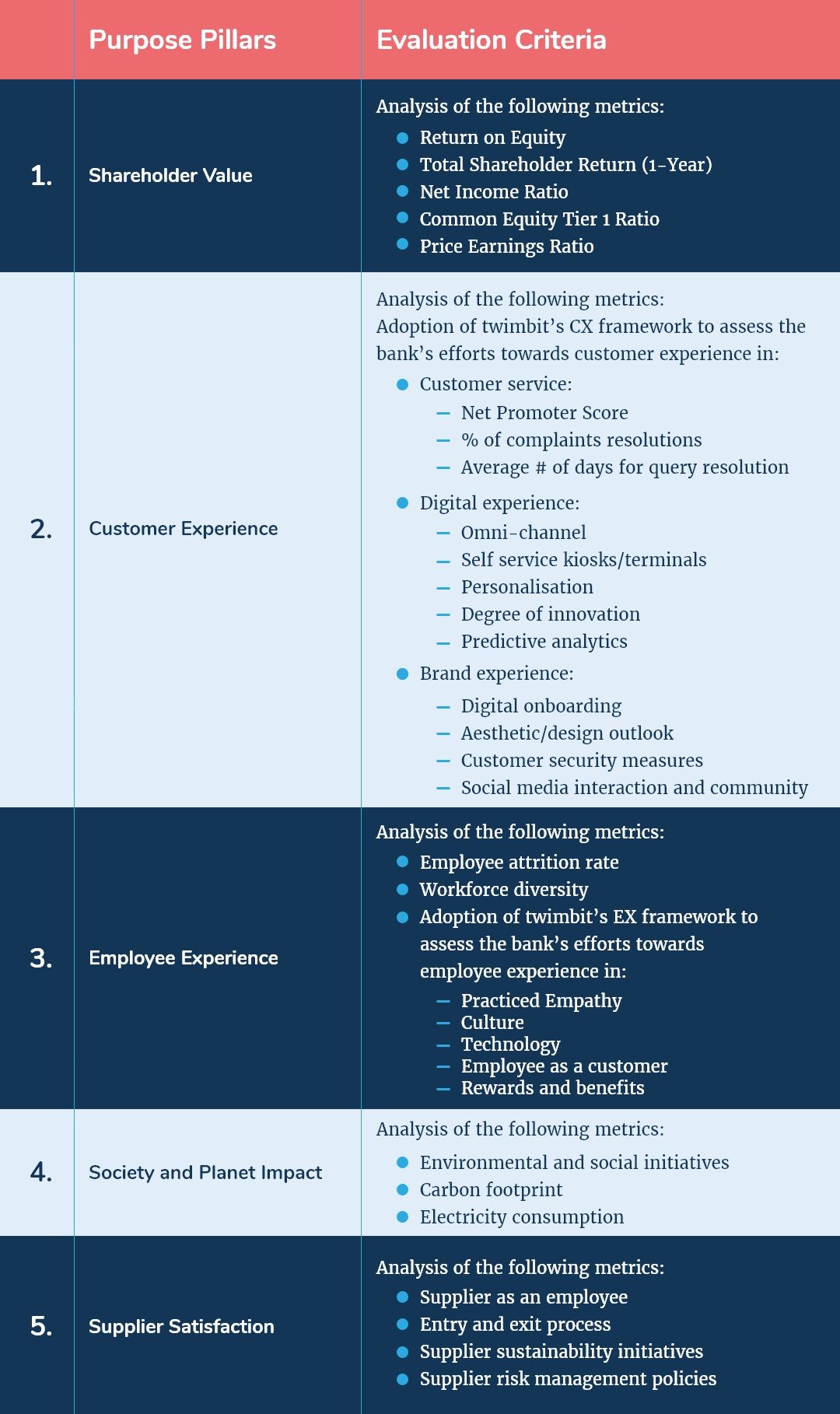

twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Bank Rakyat Indonesia, (2020, December 31). Group annual report.

https://www.ir-bri.com/misc/AR/AR2020-BBRI.pdf

Bank Rakyat Indonesia, (2020, December 31). YCharts.

https://ycharts.com/companies/BKRKF/price_to_book_value