In this report, twimbit seeks to highlight and celebrate the successes of telecom service providers (telcos) who have managed to diversify their businesses beyond the core connectivity services such as mobile or broadband. The future growth opportunities exist in the market adjacencies. They are harder to execute but immense in potential. Our study revealed 6 key insights.

#1 50% of telcos in APAC have managed to establish and grow non-connectivity businesses

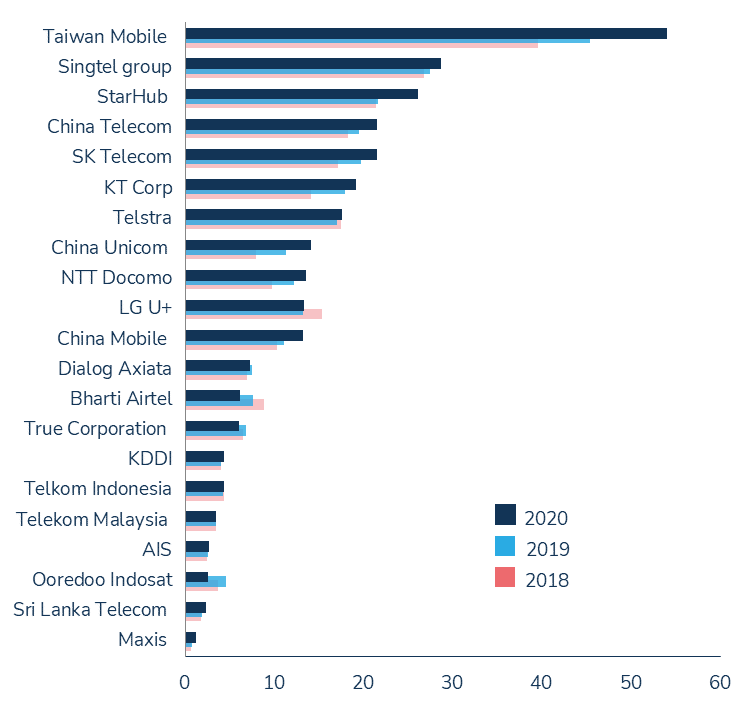

We studied 40 telcos across 15 key markets who provide consistent detailed updates on their business progress. 21 out of the 40 have made progress in establishing and reporting their non-connectivity business revenues. Of the 21 who have established the highest percentage contribution to the total business is from Taiwan Mobile at 54 percent.

Source: operator’s financials, twimbit analysis

Non-connectivity services (excluding voice, broadband, enterprise connectivity (IP-VPN, SD-WAN, etc) can broadly be classified into four distinct categories.

- E-commerce

Many service providers were quick to spot the growing opportunity with e-commerce. Early to market is an important prerequisite to success in this category. We see a tailwind in operators having their own online portals to facilitating commerce. - Enterprise non-connectivity

(Cloud, managed services, IoT, cybersecurity)

Enterprises – both large and small, are rapidly transforming to leverage digital capabilities. 5G in particular is going to be enterprise-led. This will be a key growth engine in the coming decade. Review twimbit’s study which deeply discusses the pillars of enterprise readiness of telcos in the region. - Content and Media

(IPTV, pay-TV, content leasing, OTT services)

Telcos benefitted from both OTT and IPTV services. Collaboration with giants like Netflix and Amazon prime helped generate revenue in the OTT segment. Bundling broadband services with IPTV has helped improve the ARPU per household. - Others

(Financial services, gaming, digital marketing, analytics, telehealth, education, etc)

Telcos have succeeded in diversifying into many of the other adjacencies based on the peculiarities of their respective markets. The foray into digital marketing was one of the early bets for many. Financial services are currently the fastest-growing opportunity for telcos, albeit the hardest to win and execute.

#2 Twimbit’s Top 10 operators to ace non-connectivity revenues

The objective was to identify top 10 operators who have excelled in providing services beyond connectivity. We reviewed three parameters to rank the operators. Each parameter was given equal weightage (33 percent). We also excluded telcos whose non-connectivity businesses had less than 3 percent of total or had a negative absolute change in non-connectivity revenues.

- Absolute change in revenue from non-connectivity services between 2019 to 2020

- Percentage change in Non-Connectivity Revenues (NCR) from 2019 to 2020

- Revenue coming from non-connectivity services as a percent of the total.

| Rank | Telco | NCR 2020 USD million | NCR 2019 USD million | Change USD million | % change Y-o-Y | NCR % of total revenue |

| 1 | Taiwan Mobile | 2,586 | 2,034 | 552 | 27.2 | 54.1 |

| 2 | China Telecom | 13,568 | 11,732 | 1,836 | 15.7 | 21.6 |

| 3 | China Unicom | 6,835 | 5,258 | 1,578 | 30.0 | 14.1 |

| 4 | China Mobile | 16,166 | 13,207 | 2,959 | 22.4 | 13.2 |

| 5 | SK Telecom | 3,609 | 3,153 | 456 | 14.5 | 21.5 |

| 6 | NTT Docomo | 5,819 | 5,154 | 665 | 12.9 | 13.5 |

| 7 | KT Corp | 3,086 | 2,929 | 157 | 5.4 | 19.2 |

| 8 | StarHub | 403 | 384 | 19 | 5.0 | 26.1 |

| 9 | LG U+ | 1,607 | 1,471 | 136 | 9.3 | 13.3 |

| 10 | KDDI | 2,085 | 1,922 | 163 | 8.4 | 4.3 |

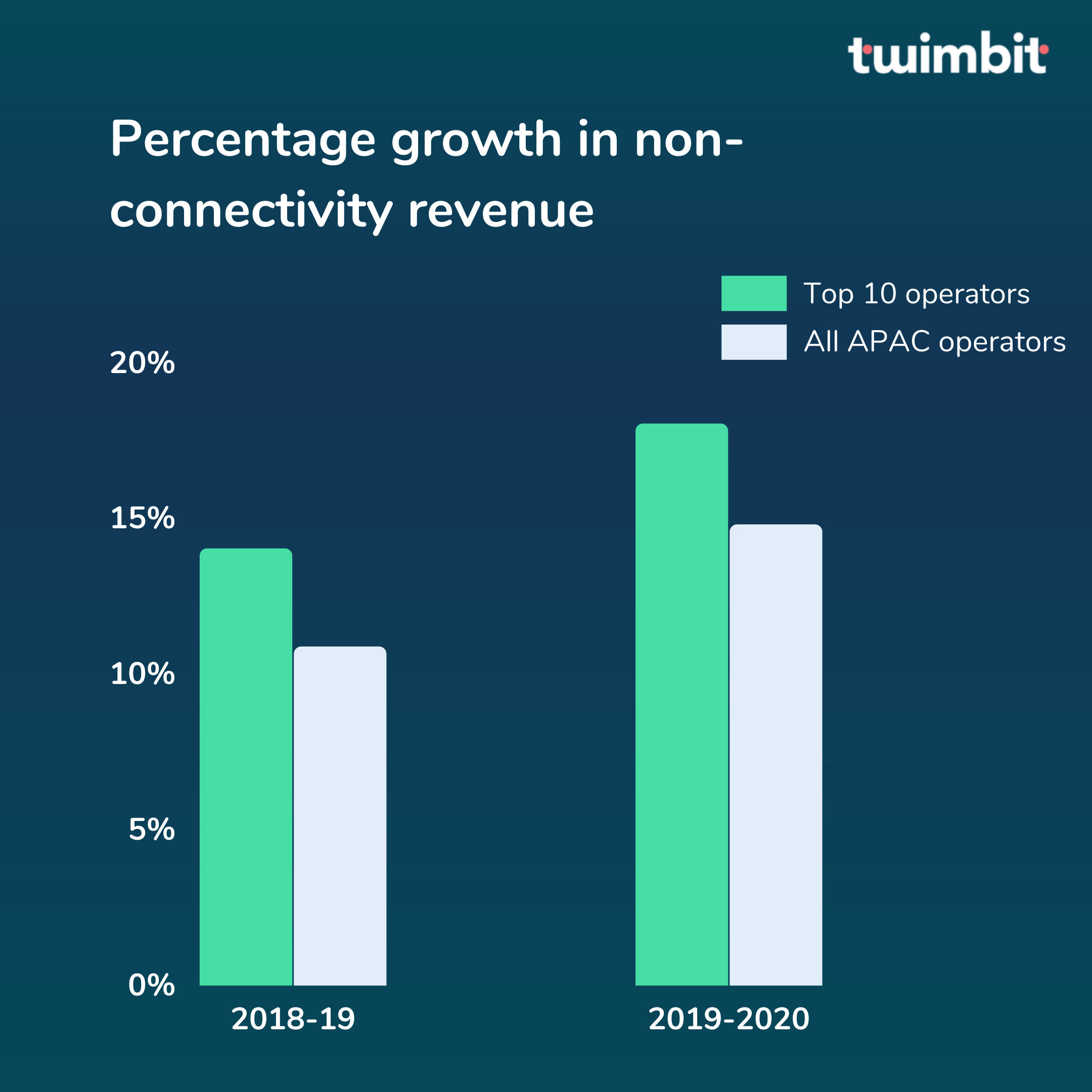

| All APAC- Total | 64,013 | 55,759 | 8254 | Avg. 8.8 | Avg. 13.4 | |

| Top 10- Total | 55,764 | 47,242 | 8522 | Avg. 15.0 | Avg. 20.0 |

#4 Enterprise is the natural adjacency for most telcos

The analysis of the revenue by segment type reveals interesting insights.

- Taiwan Mobile is an exception with incredible success in e-commerce. Several others did attempt to make a play but have failed. We do not recommend this as an adjacency to pursue unless via a partnership.

- SK Telecom gets the award for being the most diversified business with good revenue contribution from three distinct segments. They are undoubtedly one of the region’s most innovative telcos.

- Content is emerging as a very strong growth opportunity with a high ability to execute. Markets with high levels of consumption of local language content represent an easier opportunity to build differentiation from global giants such as Netflix, Apple and Amazon.

- Enterprise is the biggest and most important opportunity to prioritize. While many have made good progress with the enterprise connectivity business, its services such as cloud, security and cloud that need new capabilities, especially for go-to-market.

| Telco | Enterprise | Content | E-commerce | Others |

| Taiwan Mobile | – | 3.4 | 50.5 | – |

| China Telecom | 21.46 | – | – | – |

| China Unicom | 14.0 | – | – | – |

| China Mobile | 13.1 | – | – | – |

| SK Telecom | – | 10.0 | 4.3 | 7.1 |

| NTT Docomo | 0.4 | 13.0 | – | – |

| KT Corp | 9.5 | 9.6 | – | – |

| StarHub | 16.8 | 9.2 | – | – |

| LG U+ | 4.7 | 8.5 | – | – |

| KDDI | 3.81 | – | – | 0.5 |

#5 11 telcos exceed a billion dollars from non-core business in 2020

- 11 telcos have managed to drive revenues over US$1 billion in non-connectivity businesses.

- SingTel is a notable mention in diversification with a good mix of revenues from enterprise, content as well as other adjacencies. They have recently forayed into financial services in partnership with GRAB. Their investee companies Globe and Airtel will be interesting to watch in the coming years. SingTel had a weak 2020 and the lack of growth resulted in them not making into the Top 10.

| Telco | Non-connectivity revenue 2020 USD million | Total revenue 2020 USD million | % of non-connectivity revenue to total revenue |

| China Mobile | 16,166 | 122,891 | 13.15 |

| China Telecom | 13,568 | 62,970 | 21.55 |

| China Unicom | 6,835 | 48,614 | 14.06 |

| NTT Doc | 5,819 | 42,999 | 13.53 |

| SK Telecom | 3,609 | 16,762 | 21.53 |

| Singtel Group | 3,407 | 11,889 | 28.66 |

| Telstra | 3,198 | 18,257 | 17.52 |

| KT Corp | 3,086 | 16,091 | 19.18 |

| Taiwan Mobile | 2,586 | 4,783 | 54.07 |

| KDDI | 2,085 | 48,345 | 4.17 |

| LG U+ | 1,607 | 12,076 | 13.3 |

#6 Twimbit takeaways

- The opportunities to diversify are many for the telecom service providers. The challenge is the ability to execute and win.

- Enterprise business represents the must-win area for most service providers. This takes on more importance given the extensive investments in 5G which will be enterprise-led.

- Media and Content – This is the closest adjacency for the service providers and one that they have had most success with. Bundling content with broadband connectivity has helped across the board. Some service providers have been bold enough to develop localised content. This is again a must-compete segment for telcos.

- Payments – This represents a new growing opportunity. You can review our upcoming study on the Top 5 global telco’s to ace financial services. The majority of the success stories have been in emerging markets.

- E-commerce – In the early days of the e-commerce boom, many service providers rushed to participate in it. A handful of them have succeeded in establishing this business.

- Others – Gaming, Digital Marketing are some of the other non-connectivity revenues pursued by the telcos. Success has been very market specific.

- Partnerships – Given the very varied success rates of diversification, telcos are now partnering to help improve the chances of success.

As we look into the future, we do strongly believe that diversification from connectivity will be essential. Telcos are at the epicentre of enabling the mobile led economy, yet in most parts they have missed the massive growth opportunities provided by the ecosystem. The diversification opportunities will need telecom service providers to build completely new set of capabilities. This can only happen with a change in the culture and approach to innovation.