Company Insights

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Bank of China (Group financials)- An overview as of 31st December 2020

| Bank Name | Bank of China (BOC) |

| Headquarters | Beijing |

| Operating revenue | USD 86.9 billion |

| Group net profit | USD 37.6 billion |

| Total assets | USD 3.73 trillion |

| Employees | 309,084 |

| Countries in operation | 61 |

| Number of branches | 10,991 |

| ICT spend | USD 2.5 billion |

| Number of customers | Not Available |

| Market capitalisation | USD 128.4 billion |

| Operating revenue CAGR growth (2016-2020) | 3.17% |

2. Conversion rate to USD as of 31st December 2020 – 0.1531 USD

Shareholder value (31st December 2020)

| Return on equity (as of 31st December 2020) | 10.61% |

| Total shareholder return (1-Year) | 10% |

| Net income ratio | 18.06% |

| Common equity Tier 1 ratio | 11.28% |

| Price-earnings ratio (as of 31st December 2020) | 4.64 |

Awards

| 2020 | Financial Stability Board (FSB): Global Systemically Important Bank The Banker: Ranked 4th in Top 1,000 World Banks, Ranked 4th in Top 500 Global Banking Brands FORTUNE: Ranked 43rd in Global 500 (2020) Forbes: Ranked 10th in Global 2000 Asiamoney: Best Overall Chinese Bank for Belt and Road Initiative, Best Transaction Bank for Trade Finance, Best Transaction Bank, Best Bank for Leveraged Finance Finance Asia: Best DCM House The Asian Banker: Best AI Initiative in China, Overseas Wealth Management Service of the Year in China Asian Private Banker: Best National Private Bank in China (State-owned Banks) |

BOC and its strategic focus areas

Bank of China (BOC) aims to administer reform and innovation as its driving force to build a new development pattern, one which would meet growing customer demands for better lives financially. The bank plans to make progress while ensuring stability for its businesses.

BOC also wants to foster a development pattern that focuses on domestic commercial banking in China, invigorated through the bank’s global reach and integrated operation divisions. It aims to become a top-tier global banking group by adapting the strategic approach of bolstering and adapting change to drive major breakthroughs. Some key objectives include:

- Enhancing supply-side structural reforms in the financial sector

- Expediting digital transformation and facilitating high-quality and sustainable developments

- Mobilising resources to focus more on technology finance, inclusive finance, green finance, wealth finance, cross-border finance, consumer finance and county-level finance

- Prioritising risk control and management and applying prudence and compliance in all operations

- Customer experience

BOC strives to accelerate the link between business and technology in serving customers. By upgrading household technology consumption and contributing to a new development paradigm, BOC aids its domestic and international circuits, thereby reinforcing and simultaneously reaching the bank’s ultimate goal of becoming a top-tier global bank. In doing so, BOC gets customers to follow the direction of a mobile, scenario-based, asset-light, and integrated development, a move that shows that the bank puts its best foot forward for the clientele.

BOC aims to follow the strategies below to achieve its goals:

- The bank plans to launch flexible products and services by keeping new technologies and consumption modes in tandem. It will enhance the expansion and analysis of scenario cooperation while using platforms like smart home, smart community, etc. By doing so, BOC will be able to provide whole-chain and customised consumer financial services such as remote applications, smart face-to-face interviews, intelligent approvals, instant loan granting, and smart repayments.

- It will expand financial services to consumer groups in counties and rural areas and cover all aspects of financial needs in a customer’s life, while closely following green finance and rural revitalisation plans.

Although the bank has set forward-looking goals for integrated development, it undertook many initiatives to get closer to the end goal. In view of this, as of 31 December 2020, the number of active mobile banking customers reached 211 million from 181 million in 2019, an increase of 16.44%. This success is due to the following factors:

- Launched “thousand customers, thousand faces”, intensively customised service with over 200 different features to function, experience, scenario, and technology application

- Initiated the embedding and standardising of “open banking” concepts, which covered 13 financial service types, including gold, cross-border, financing, and payments on the national government affairs and 12306(railway tickets) platforms

- Deepened efforts to enrich products and services by looking at the consumer consumption demands and patterns closely. BOC then provided an assortment of consumer credit products covering clothing, food, shelter, transportation, medical care, learning, tourism, and entertainment

- Came up with different credit loan services for various customer categories, consisting of:

- BOC E-Credit: a pure credit service product, which uses scenarios and big data to deliver online personal credit services

- Pledge products based on deposit certificates, government bonds, and wealth management accounts

- Youth E-Credit: a credit service product specifically for students

- BOC Smart Loan: a credit service product for premium BOC customers

- Upgraded the functionalities of BOC digital credit cards, created the “BOC Auto Zone,” and strengthened online platform building to improve the online experience of scenario-generated customers and promote customer vitality

- Enforced education activities in various interesting forms at outlets and through online media platforms such as WeChat, Weibo, official website, mobile banking, and TikTok

- Established featured services consisting of foreign exchange settlement, international settlement documents services and L/G inquiry services, as well as rolled out To-do Centre, Info Centre, corporate cards, tax ID inquiry and other user-oriented services to boost customer experience

- Introduced several scenarios with local aspects for government affairs and people’s livelihood, and supplied over 100 convenient services such as provident fund, social security, and civil affairs, effectively expanding its capacities in serving people’s livelihood

- Introduced a one-stop social security card issuance service, in which cards may be open with both a financial and a social security function and claims can be made on the spot, considerably boosting service efficiency and customer experience

- Introduced tablet-based smart counters, which use more flexible and accessible technologies to provide clients with a more thoughtful and personalised “one-to-one” service experience in a variety of situations

- Carried out ‘3.15’ consumer protection education and publicity campaigns against illegal fund-raising, the “Protecting Personal Wealth” campaign, and the “Financial Knowledge Popularisation Month” using its official website, WeChat official account and in workplaces

- Employee experience

BOC strives to endow employees with greater capability and competence, to work in the spirit of craftsmanship, and to encourage them in working towards perfection. In order to help its employees realise their career goals and initiate the growth mindset, the bank applied HR input in key strategic areas, business lines, and professional talent teams. It adhered to HR efficiency improvement ideas that consist of the following initiatives:

- Adapting to the trend of intelligent outlets and aiming to promote personnel transformation, the bank made full use of its human resources. This happens through standard counter allocation, authority integration, appraisal reform, position combination innovation, and other measures. It helped to reshape production relations at outlets and stimulated staff vitality to improve outlet efficiency

- Organising learning activities with broad impact, such as a staff learning day, Teachers’ Day, and a new employee development community through community learning and action learning

- Refining all employees’ compliance knowledge and abilities by improving the AML and sanctions compliance training management processes and conducting various forms of compliance training

- Followed employee health protection measures during the pandemic and adopted online office and online services to maintain smooth and orderly business operations across the globe

- Established BOC University and strengthened the training system for all employees by creating an Education & Development Department at the Head Office. It also introduced the BOC University cloud platform to arrange training programmes according to new ideas and concepts

- Making efforts to cultivate its talent pool, promoting qualified young individuals to management positions and expanding intra-group rotation programs

- Adopting special recruitment plans to ensure stable employment, to hire impoverished college students and children of medical staff working in COVID-19 prevention and control as frontliners

- Remuneration distribution policy that BOC follows is principle of “remuneration by post, payment by performance”. It consists of basic salary, performance remuneration and benefits. The basic salary lies in the value of the position and the ability of employees to perform their duties, whereas performance remuneration runs parallel to performance evaluation results as well as risk, internal control, ability and other factors. BOC also pays supplemental retirement benefits to employees, including supplemental pension payments and medical expense coverage

- Society and planet impact

BOC has a couple of plans to grow its contribution to society and the planet. On the society end, it is increasing efforts in creating value for stakeholders, taking on more responsibilities to accelerate economic and social development, and providing stability and security for SMEs. Planetary initiatives include inculcating development that is innovative, coordinated, green, open, sustainable, and shared. Thus, the end goal for BOC is to build its economic, social, and environmental influences.

Driven by these plans, the bank undertook the following initiatives in 2020:

- In order to fight the pandemic, the bank refined the supply of credit resources, formulated credit policies, and satisfied credit demands for key industries involved in pandemic prevention and control.

- BOC actively bolstered the production and supply of medical materials. Also, it provided supplies and necessary living assistance to Chinese students stranded overseas, neighbouring countries, countries along China’s Belt and Road government initiative, and key overseas markets.

- The bank also focused on poverty alleviation by channelling resources to poverty-stricken areas and carrying out livelihood programs covering education, healthcare, care for the elderly, housing, drinking water safety, etc., to further boost the quality of life there.

- It introduced comprehensive products such as loans for industries involved in poverty alleviation, loans for programs engaged in poverty alleviation, government-sponsored student loans, and poverty alleviation bonds.

- It focused on credit granting opportunities for areas such as urban rail transit and railway construction, key water conservancy projects, land transfer, urban renewal, the renovation of old urban communities.

- The bank is heavily invested in the green development concept and has integrated green finance into its entire business process. Such initiatives include:

- Setting up the Green Finance Management Committee to coordinate the development plan

- Establishing businesses such as green credit, green bonds, climate investment and financing, and green bills

- Building a multi-tiered and three-dimensional green financial business system to support green industries and projects vigorously

- Contributing USD 1.2248 billion to the China National Green Development Fund

- Monitored the climate and environmental risks and conducting stress tests in some high-carbon industries and sensitive areas

- The bank set up BOC Charity Foundation to provide charitable assistance to the poor and vulnerable.

- It also developed the Bank of China Philanthropy Mutual Assistant Platform for Elderly Care concerning time banking and other practices and created innovative models of elderly care services to support public welfare pension undertakings.

Digital Strategy

BOC wants to strengthen its basic capabilities and encourage innovation to accelerate digital transformation. The bank plans to construct enterprise-level architecture and transform its technology system, deepen the integration of technology and business, and improve responsiveness and output efficiency. Thus, to take a step forward towards the transformation, BOC embraced its “Mobile First” strategy and increased efforts to boost mobile banking services as well as expand on online channels.

In 2020, almost 95.31% of the transactions transpired through e-banking channels. This success is due to the following initiatives:

- Established a mobile portal to host integrated financial services for corporate banking customers

- Relied on its Intelligent Global Transaction Banking (IGTB) service platform to deliver mobile value-added services for SMEs

- Enhanced fintech applications, integrated service schemes, the functions of cross-border e-commerce products and e-commerce export functions

- Made use of both Artificial Intelligence (AI) and big data to launch “thousand customers, thousand faces”, an extensively customised service based on user labels and browsing behaviour. This service featured four zones, namely cross-border, education, sports and silver economy with relevant scenarios, thus becoming a one-stop financial and lifestyle service

- Upgraded the digital risk control capacity for its online channels and used the “Cyber Defence” smart risk control and prevention system to monitor e-banking transactions

- Made strides towards the digitalisation of branch outlets, which was possible due to the following steps:

- Pushed development for branch transformation and smart operations by forging an intelligent service system featuring smart branch outlet services, diversified staff composition, refined management, and a marketing service ecosystem encompassing all channels and scenarios

- Launched smart screens and standardised three-dimensional displays of various products and promotional information in branch outlets

- Created a staff channel and a digital outlet management platform to visualise and panoramically display the operational results and business data of outlets, thereby propelling outlets to evolve from smart processes to digital processes, services, marketing, and management

IT Strategy

BOC aims to build a digital sharing platform at a global level to provide accurate customer services, dynamic innovation in products, comprehensive and efficient operation, as well as smart and flexible risk management. The end goal is to reach the top tier in cloud computing, artificial intelligence, 5G and the internet of things.

To achieve this feat, the bank invested USD 2.558 billion in IT and made further efforts towards enabling advancement through technology and formulating an IT development plan. In addition, to accelerate the IT digital transformation strategy, BOC implemented the ‘NeoBOC+’, a technological innovation strategy that focuses on advanced enterprise-level business architecture and IT architecture transformation.

This specific strategy helped build the bank’s IT capabilities in business digitisation, scenario ecosystem, and platform-oriented technology. It became a reality through the following initiatives:

- Made moves towards the OASIS project, which revolves around blockchain technology, to move closer towards developing a digital bank

- Initiated BOC Global Matchmaking System (GMS), which provides full-process services, including cloud negotiation, cloud contracting, and cloud live broadcasting, to ease supply-demand negotiations despite geographical restrictions.

- Continued to improve its IT delivery capability. BOC embraced the concept of “multi-centre multi-location” and advanced the construction of computer rooms and cloud centres to build a better digital bank

- Pushed the creation of a comprehensive risk management portal and intelligent risk data, as well as setting up monitoring and early warning mechanisms

- Implemented digital transformation by applying emerging technologies such as big data, artificial intelligence, blockchain and biometric authentication, and enhancing its digitalisation and intelligent development capacities continuously.

ICT contracts

- Partnership with Tencent Holdings for the Tencent Cloud technology to develop a risk analysis model based on client data

- Collaboration with Eikon to release DeepFX, an artificial intelligence-based foreign exchange trading signal prediction application

- Association with IBM to create innovation labs for technological advancement and the incubation of financial innovation

9 Growth and Innovation Opportunities

- #1 Cost to serve

BOC faced the problem of an increase in operating expenses to USD 31 billion from USD 30 billion and a decrease in the operating profits to USD 37.6 billion from USD 38.2 billion. The decrease was a consequence of rising impairment losses of 16.51 per cent as a mitigating mechanism for industries affected by COVID-19. Despite the pandemic, the bank’s Cost to Income Ratio (CIR) dipped to 26.73% compared to the 28% in 2019.

The bank cut down on its operating expenses for personnel in 2020 to USD 13.6 billion from USD 13.8 billion in 2019. This cost reduction was mainly because of a marginally high cut in retirement benefits and social insurances. On the other hand, salary and welfare assistance continue to increase compared to 2019. It also witnessed a significant reduction in general operating and administrative expenses to USD 5.9 billion in 2020 compared to USD 6.4 billion in 2019.

While the bank is making efforts to become digitally efficient internally and externally – it must take stringent measures to manage its operating revenues. With skimmed net interest margins, BOC can concentrate on the following significant areas to optimise cost efficiency:

- In a low-interest-rate environment, BOC should detect payback risk in loans and attrition risk in deposits to manage a good net interest margin. In addition, BOC can use predictive behavioural models to continuously adjust the bank’s interest-rate risk estimates and hedging strategies.

- The bank can focus on non-interest income and complementary revenue streams to offset the impact of substantial impairment costs.

- BOC can apply RPA-enabled audit trails for red-flagging any high-cost inflexions by implementing transaction-level transparency.

- #2 Transformation of the branch and its branch networks

The bank pushed development patterns towards branch transformation and smart operation by forging an intelligent service system featuring smart outlet services, thus providing ease of use and helping customers become self-reliant. BOC also introduced tablet-based smart counters, which use more flexible and accessible technologies to provide clients with a more thoughtful and personalised “one-to-one” service experience in various situations.

From 2019 to 2020, BOC reduced its physical network costs from USD 2.08 billion to USD 1.9 billion by shutting down ATMs (33,314 from 37,331), Self-service terminals (855 from 1,875) and increasing Smart counters (31,960 from 30,425).

This move provides a 6% reduction in the maintenance cost of branch networks. The bank should continue its efforts to reduce any non-performing branches or ATMs and focus on transforming the network through:

- BOC can replace ATMs with Interactive teller machines (ITMs), making it easier for consumers to make deposits and withdrawals. This also helps customers to do their transactions and cash deposits more quickly.

- The bank should transform high business volume and high-customer-headcount branches into flagship digitalised community hubs that enhance the in-branch experience and redefine customer engagement. To accomplish this, BOC should:

- Increase the capability of smart counters – Many services done by personnel can be moved to smart counters, reducing the need for human tellers to work in bank branches. Furthermore, smart branch technology enables a personalised sales strategy and 24/7 access to the bank branch.

- It can establish an omnichannel user experience, one that will link BOC Internet Banking, Mobile Banking and physical branches with Virtual Assistants. This holistic channel will provide customers with a consistent experience, whether online, on a mobile device, or at the branch. It will also result in greater efficiency at the bank branches.

- While bank staff are a necessity in high-traffic, high-visibility urban locations, BOC can establish fully self-serviced branches for greater physical footprint penetration at lower costs. These branches will be able to provide complete services through video conferencing.

- Community centre- There is a need to adopt a branch model that is more appealing than the conventional one. Branch visits should go beyond processing transactions and resolving questions to add delight. For example, BOC can transform its traditional branches into community hubs, where people can socialise, relax, and bank – all at once.

- #3 Customer experience

The bank plans to enhance the expansion and analysis of scenario cooperation while making use of platforms like smart home, smart community, etc. This is to provide customers with services such as remote application, smart face-to-face interview, intelligent approval, instant loan granting, and smart repayment.

The bank can further leverage its capabilities through AI and machine learning (ML) and work in these areas to optimise the customer experience journey:

- BOC provides customer support 24/7. It can, however, work on the day complaint resolution by prioritising Chatbots, virtual assistants, and video conferencing to increase the count of complaints handled.

- It can provide insights for customers into their saving and spending patterns with specific recommendations to help them meet their financial goals.

- A gamified user interface to make the customer experience interactive instead of a monotonous experience with a dull interface.

- #4 Business segment expansion

BOC issued dual currency special bonds worth USD 6.23 million for SMEs. It also launched various relief measures and loan schemes for SMEs to help support their financing and address business challenges during COVID-19. The bank can further work on its SME financing strategies. It can:

- Identify and establish a line of credit for SMEs that are first-time borrowers who do not have access to typical bank lending

- Develop business advisory and management solutions to help SMEs make informed investment and banking decisions using digital platforms

- Work with e-commerce websites to provide credit to small businesses looking to access the market

- Reduce merchant interchange reimbursement rates and put out strategic card acquisition and usage initiatives, including reduced merchant discount rates

- Provide personal and business overdraft facilities, along with basic lending services to the SME sector

- #5 Employee experience and productivity

BOC has made significant investments in employee development and offers a flexible work atmosphere. However, the bank should consider the following:

- Design personalised employee upskilling programs based on the employee level and adopting effective leadership development coaching to prepare them for future roles

- Expand its employee wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs

- Create a platform or forum where employees can reach the BOC leaders easily. They can then have face-to-face discussions with leaders and influential external speakers, share their aspirations and extend their horizons beyond the workplace.

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Giving employees the option to work on cross-department projects for lateral career advancements

- Periodical career breaks and approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food and medical support work, as well as cleaning drives

- Provide hassle-free student loans to new hires for controlling attrition rates among the said hires, hence increasing employee loyalty

- #6 Migration of workload to the cloud

BOC Global Matchmaking System (GMS) provides full-process services, including cloud negotiation, cloud contracting and cloud live broadcasting. However, the bank can amplify its cloud capability by using these strategies:

- BOC should use a cloud-based platform to streamline various talent management and HR-related tasks.

- In order to increase efficiency, cloud adoption improves a variety of additional activities beyond customer and employee experience. The bank can extend data storage and data-driven activities across security, regulatory compliance, auditing, and pan-organisation communication pipelines to modernise its overall operating model.

- #7 Cybersecurity

The bank strengthened its anti-money-laundering (AML) policies and procedures, optimised AML resource allocation, established a robust management framework for overseas compliance, improved the compliance risk assessment program, and enhanced the review mechanism for internal transactions.

It has also upgraded the transaction monitoring and management system and promotes the application of operational risk management tools, including Risk and Control Assessment (RACA), Key Risk Indicators (KRI) and Loss Data Collection (LDC), etc., to identify, assess and monitor operational risk. The bank can, however, work in these areas to improve security measures:

- The bank needs to develop new risk capabilities to account for non-financial risk, especially with respect to black swan events like COVID-19.

- BOC needs to periodically redefine its risk appetite, detect new potential risks and existing inefficiencies in controls, and devise a dynamic risk management approach accordingly.

- It can use advanced analytics and natural language processing (NLP) for credit underwriting to identify potentially high-risk accounts.

- Increased incorporation of AI calls for specific attention by BOC to account for a host of security concerns like privacy violations, erroneous automated processes, and discrepancies in model outcomes.

- #8 Artificial Intelligence (AI) in everything

BOC is making significant strides in adopting artificial intelligence (AI) into its business model. The bank could begin with the following to maximise AI potential:

- A sophisticated and forward-looking credit profiling method for e-credit business banking customers as well as youth and other premium customers. It uses predictive analytics to assess loan credibility beyond one’s financial statement analysis. Other essential criteria that can be a part of the profiling mechanism include economic KPIs, market and industry trends, bank and system facility overviews, and more.

- The use of AI and ML at various customer touchpoints, such as digital biometric customer verification for customer profiling of different customer categories and the identification of potential customers for cross-selling and upselling products and solutions.

- BOC can leverage data analytics capabilities to seek contextualised data insights that it can use to innovate product offerings and delivery channels.

- #9 Society and planet contribution

BOC has steered investments in renewable energy, improved energy efficiency, pollution prevention and control, clean transportation, sustainable water resources and wastewater management, green building, affordable service infrastructure, entrepreneurship and employment, and other areas with significant environmental and social benefits.

The bank has a comprehensive strategy to save electricity and fuel via its environmentally friendly green office infrastructure. However, it should aim to reduce its carbon footprint by:

- Building on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid

- Utilise energy-efficient devices by making one-time investments and saving costs in the long-term

- Use excess energy during low or off-peak times to decrease energy usage

- Reduce its carbon footprint by switching to pulper cards, eco ink and carbon control press machines

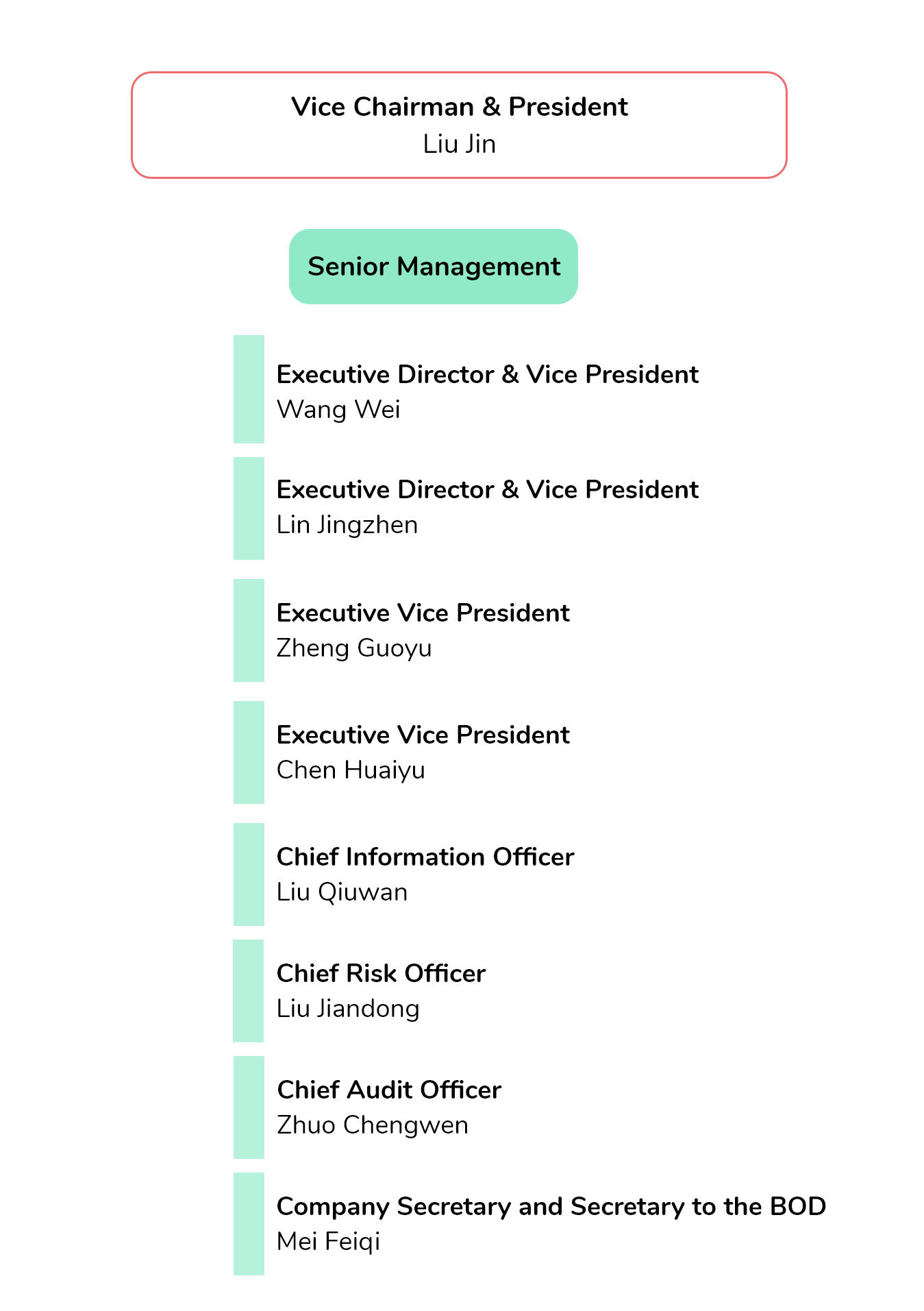

Organisation structure: Leadership

Executive Profile

Liu Jin

Vice Chairman & President

Liu Jin is the Vice Chairman of the Board of Directors since June 2021 and the President of the Bank since April 2021. He has graduated from Shandong University in 1993 with a Master of Arts degree. He is a Senior Economist as well.

Quote

- Employee Productivity, Annual Report 2020

Reform is the only way to liberate and develop the productive forces and fundamental drivers of business development.

Wang Wei

Executive Director &Vice President

Wang Wei is the Executive Director of the Board of Directors since June 2020 and Executive VP of the bank since December 2019. He holds a graduation degree from Shannxi Institute of Finance and Economics and a Doctor’s Degree in Economics from the Southwestern University of Finance and Economics. He is a Senior Economist as well.

Lin Jingzhen

Executive Director &Vice President

Lin Jingzhen is the Executive Director of the Bank since February 2019 and Executive Vice President of the Bank since March 2018. He has graduated from Xiamen University in 1987, and obtained an MBA Degree from Xiamen University in 2000.

Zheng Guoyu

Executive Vice President

Zheng Guoyu is the Executive Vice President of the Bank since May 2019. He has graduated from Wuhan Institute of Water Transportation Engineering in 1988, and from Huazhong University of Science and Technology as a MBA Degree in 2000. He is a Senior Economist.

Chen Huaiyu

Executive Vice President

Chen Huaiyu is the Executive VP of the Bank since April 2021. He has graduated from Beijing Foreign Studies University in 1992 and also obtained a Master’s in Economics in 1999 from University of International Business and Economics.

Liu Qiuwan

Chief Information Officer

Liu Qiuwan is the Chief Information Officer of the Bank since June 2018. He has graduated from Xi’an Mining College with a Bachelor’s Degree in Engineering in 1982. He is also a Senior Engineer.

Liu Jiandong

Chief Risk Officer

Liu Jiandong is the Chief Risk Officer since February 2019. He has a Bachelor’s Degree in Economics from Renmin University of China, and has also obtained a Master’s in Economics in 2000 from Renmin University of China.

Zhuo Chengwen

Chief Audit Officer

Zhuo Chengwen joined the bank in 1995. He has served as Chief Risk Officer of BOC Hong Kong from November 2019 to February 2021. He has graduated from Peking University with a Master’s Degree in Economics in 1995, and obtained an MBA in 2005 from the City University of New York. He is a Certified Public Accountant as well.

Mei Feiqi

Company Secretary and Secretary to the Board of Directors

Mei Feigi is the Company Secretary of the Bank since March 2018 and Secretary to the Board of Directors since April 2018. He has graduated from Chengdu University of Technology with a Bachelor’s Degree, and later received on-the-job postgraduate education. He is also a Senior Economist.

Appendix A

- twimbit Purpose Index

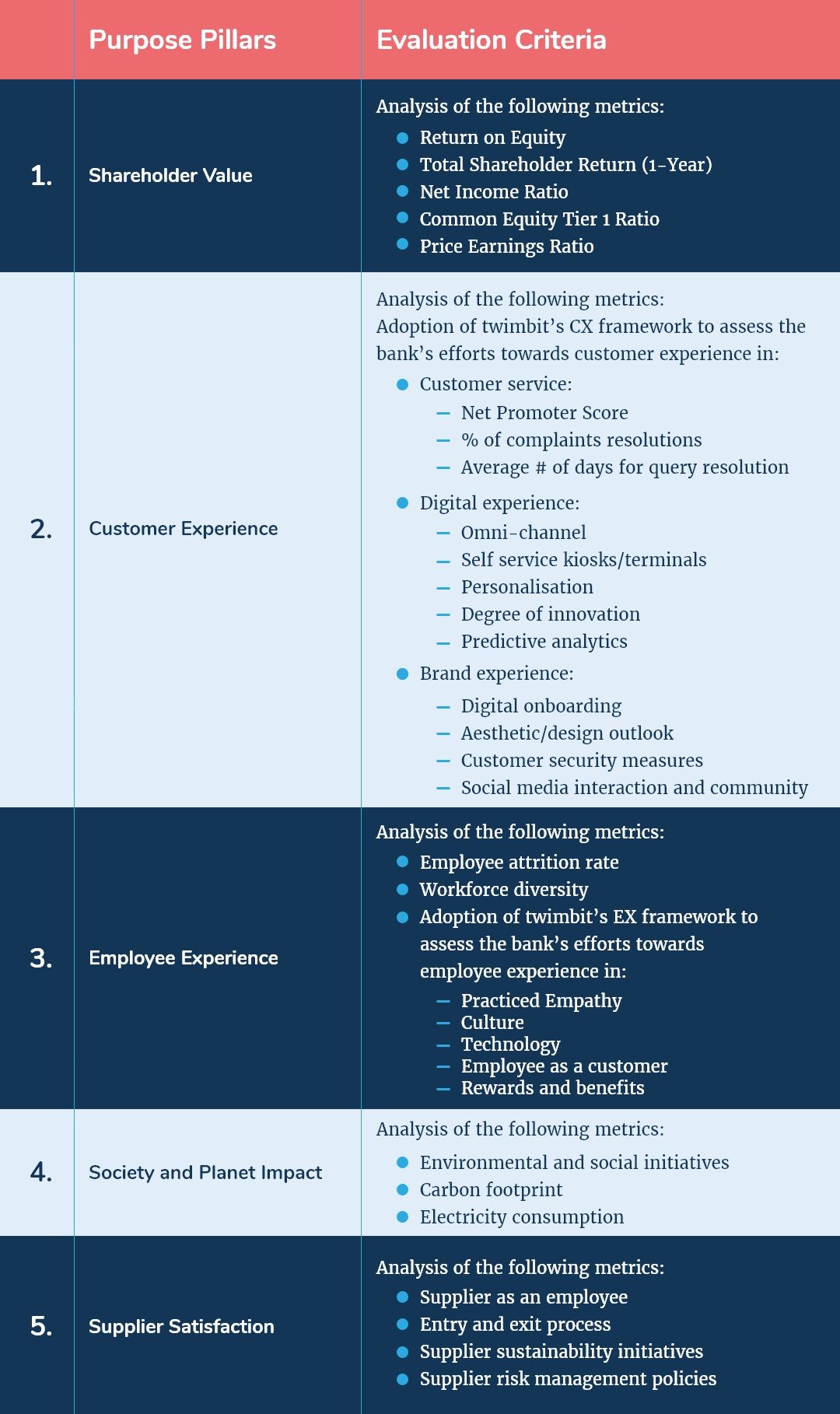

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Bank of China Ltd, (2020, December 31). Annual Report 2020.

https://pic.bankofchina.com/bocappd/report/202103/P020210327642434487221.pdf

Bank of China Ltd, (2020, December 31). Investor Presentation 2020.

https://pic.bankofchina.com/bocappd/report/202103/P020210330580561501326.pdf

Wall Street Journal. Bank of China Ltd financials. Retrieved June 24, 2021 from

https://www.wsj.com/market-data/quotes/CN/XSHG/601988/financials/annual/income-statement

Finextra. Company News. Retrieved June 24, 2021 from

https://www.finextra.com/pressarticle/81921/bank-of-china-deepfx-app-available-over-eikon

https://www.finextra.com/pressarticle/80065/bank-of-china-deepens-relationship-with-ibm