Company Insights

twimbit’s Purpose Index

Source: Refer to the methodology in Appendix A below

China Construction Bank Financials – An overview as of 31st December 2020

| Bank name | China Construction Bank Corporation (CCB) |

| Headquarters | Beijing |

| Operating revenue | USD 109.35 billion |

| Group net profit | USD 41.88 billion |

| Total assets | USD 4.307 trillion |

| Employees | 349,671 |

| Countries in operation | 31 |

| Number of branches | 14,741 |

| Fintech investment | USD 33.84 million |

| Number of customers | 317.48 million |

| Market capitalisation | USD 191.89 billion |

| Operating revenue CAGR growth (2016-2020) | 5% |

2. Conversion rate to USD as of 31st December 2020 – 0.1531 USD

Shareholder value (31st December 2020)

| Return on equity | 12.12% |

| Total shareholder return (1-Year) | -9.3% |

| Net income ratio | 38.30% |

| Common equity tier 1 ratio | 13.62% |

| Price earnings ratio | 4.2 |

Awards

| 2020 | The Banker: 2nd place of the top 1000 world banks’ ranking Fortune: Number 30 of Fortune Global 500 Global Finance: Best bank for cross-border trades The Asian Banker: Commercial bank of the year in China Asiamoney: Overall best national retail bank |

CCB and its strategic focus areas

- Business strategy

The Construction Bank of China (“CCB”) proactively practices New Finance and promotes the implementation of its Three Major Strategies – house rental, inclusive finance, and FinTech. Its New Finance initiative is people-centric and relies on technological innovation and digital operation to support the Three Major Strategies.

CCB plans to implement its “New Finance” strategy by:

- Making progress in the house rental business:

- By the end of 2020, the house rental service platform covered more than 96% of administrative regions across the country

- There were 24 million listed apartments in total

- The bank carried out a house deposit business with 1.2 million contracted apartments

- CCB initiated 230 “China Construction Bank (CCB) Home” projects, which provided 140,000 apartments through long-term lease contracts

- Growing into a leader in inclusive finance:

- By the end of 2020, the balance of inclusive finance loans was USD 222 billion, up from USD 147 billion in the previous year, an increment of 51%

- The growth in inclusive finance loans was the biggest among peers in terms of size and increments

- The bank’s digitally inclusive finance mode has become the blueprint for The People’s Bank of China to formulate the industry standard of inclusive finance

- CCB fought against poverty alleviation and set up 540,000 “Construction Bank of China Yunongtong”, which covers 80% of towns and villages in China

- Yunongtong is a comprehensive service brand for rural revitalisation which implements new finances through offline-inclusive finance service outlets and an online comprehensive service platform

- Empowering internal and external development with FinTech:

- The bank vigorously promoted the implementation of its FinTech strategy

- It responded rapidly to business needs, promoted the building of smart finance, and improved on risk control capabilities

- CCB formed an intelligent ecological service system that helped improve the capability of digital government governance while providing services to sectors including house rental, rural revitalisation, education, and medical care

- It empowered small and medium-sized financial institutions and provided risk control tools to 328 similar banks

- Customer experience

Adhering to the concept of innovation-driven development, platform-based operation, and sharing and empowerment, CCB continued to improve on the mechanism of inclusive finance services for its customers. The bank practices New Finance initiatives in fintech and promotes service function innovation vigorously, allowing personal and corporate customers to obtain services anytime and anywhere, through multiple channels.

- The Yunong quick loan for farmers integrated internal and external data to profile farmers accurately and reduced financing costs for agriculture-related loans effectively

- Loans granted by CCB stood at USD 551.16 billion at the end of 2020, benefitting more than 1.70 million customers

- The bank launched a “Finance + Scenario” approach, which is a real-time interactive service to help customers with their portfolio management

- The bank also launched the “CCB Start-up Station” to create an incubator platform for entrepreneurship and innovation

- The bank provided “CCB Yunongtong” financial services at the doorsteps of people of the Miao village in Guzhang, so they did not have to make arduous trips across hills and rivers

- The bank launched “CCB Huidongni”, which is a one-stop financial services platform for inclusive finance customers (small, micro, and individual businesses)

- CCB launched a special lightweight version of its mobile banking app for rural customers with easy listening, easy reading and barrier-free communication

- The bank diversified its digital product system, realised the rapid customisation of new products on demand, and launched a series of new products:

- Quick loan for small and micro businesses

- Yunong quick loan

- Quick loan for transactions

- Quick loan for personal business

- Employee experience

CCB values its employees as much as it values its customers. The bank ensures the rights of employees follow the laws and regulations within the country. The bank is committed to building a development platform for its employees and is doing this by:

- Setting up “CCB University”, which acts as a training base for employees

- Optimising the CCB University training system by focusing on the employees’ entire career path

- Organising more than 1,066 training programmes through the CCB University

- Launching various thematic training programmes, including “Your Future with CCB” programme for new recruits

- Establishing “CCB Jianrong,” a community that helps employees accommodation needs

- Provided training on protecting consumer information security to 198,000 trainees

- Conducted a position qualification exam, which over 253,000 employee attendees

- Providing induction training for new employees and annual security training for in-service employees

- Organising ESG (Environmental, Social and Governance) training sessions from multiple perspectives to help employees enhance their understanding and comprehension of ESG

- Conducted more than 19,000 in-house nucleic acid tests (to detect the virus that causes COVID-19) for employees

- Society and planet impact

CCB aggressively pushes forward the financial supply-side systemic reforms, with green finance in a more prominent position. In addition, the bank explores new concepts, models, and methods to develop green finance:

- Green finance – CCB continued to improve its long-term mechanism for green finance development. The bank increased its efforts to provide green credit by launching new products — “Energy Conservation Loans” and “Environmental Protection Loans.”

- Green credit – At the end of 2020, the bank’s green loans stood at USD 205.15 billion, an increase of USD 25.55 billion from the previous year, a 12.45% growth. The green credit supported projects resulted in savings of 35,064,800 tons of coal, a drop of 73,886,600 tons in carbon dioxide emissions, and the conservation of 113,338,700 tons of water.

- Green bonds – CCB issued green bonds worth USD 1.2 billion

- Green leasing – CCB announced its expansion in key areas of new energy automobiles, urban rail transport, passenger and freight rail carriage, clean energy, and water environment governance by forging a “green leasing” brand through its CCB Financial Leasing subsidiary. The subsidiary helped the manufacturing sector apply extensive application new technologies for energy conservation, emission reduction, and energy consumption cut to make its existing production units eco-friendly.

- Green trusts – CCB, through its subsidiary, CCB Trust, implemented several green finance projects through private equity investment, mergers and acquisition and asset securitisation to practice ESG concepts in the trust industry.

- Green operation – CCB attached great importance to green operations and established a group for energy conservation and emission reduction at its head office. Initiatives borne from this group include:

- Launched a package of measures such as the green transformation of office facilities, paperless office, precise control of room temperature, water and electricity conservation, and safe disposal of e-waste.

- Practised the concept of green procurement and implemented a strategy featuring low toxicity, environmental protection, energy savings, and emission reduction.

- Included environmental protection and energy savings indicators when evaluating supplier selection criteria and purchasing-related products.

Societal responsibility:

- The bank constructed the “Construction Bank of China Start-up Station.” This drive aimed to provide startups and innovative enterprises with services like equity investment, credit financing, and entrepreneurial growth, which are essential during the growth phase of such companies.

- The bank extended credit support for areas pertaining to rural revitalisation. It also focused on weaker areas in rural infrastructure and supported the construction of rural drinking water supply, village roads, information communications, and energy projects.

- The bank targeted poverty alleviation and created a comprehensive pattern driven by finance that featured e-commerce first, credit innovation, service network extension, and public welfare activities.

- The bank integrated the protection of customer rights and interests into its business development strategy and corporate venture development. The move was necessary to improve the management system and operation mechanism and promote the well-organised protection of consumer rights and interests.

Digital strategy

CCB aims to press ahead with digitalised operations steadily, sticking to the concept of New Finance of inclusiveness, openness and sharing. The bank took the lead in digital transformation, took digitalised operations as the breakthrough point to implement the Three Major Strategies. The bank also developed a set of effective digital transformation methods according to the basic logic of “building ecologies, setting up scenarios and expanding user base.” CCB was able to achieve this by:

- Forming a closed-loop agile iteration mechanism for digitalised operation, covering customer insights, product matching, channel access, evaluation, and monitoring

- Introducing an end-to-end digital operation closed loop which introduces the rights products and services to the right users in the suitable scenario, at the right time and in the right way

- Improving services to cover every personal customer and the efficiency of value conversion

- Exploring the building of ecological scenarios

- Initiating pilot programmes on building financial services for featured agricultural ecological scenarios

- Accelerating the capacity building in the middle platform of businesses

- Implementing enterprise-level user management systems and programmes to systematically and further create ecological value from scenarios

- Improving the ability to acquire customers via ecological scenarios

The bank has launched the following initiatives to improve its digitalised services:

- CCB Match Plus – An open podium leveraging FinTech to give corporate customers intelligent matchmaking services and a complete set of financial solutions in cross-border transaction frameworks.

- Cloud Workshop – A new digital service window that integrates online and offline services, as well as social and financial services, enabling professional account managers to provide online financial services to their customers.

- Long Pay – An internet-based enterprise-level mobile digital payment brand of CCB which includes a group of comprehensive, integrated payment and settlement products and services.

Security strategy

CCB took multiple measures to enhance customer information security management. The bank continues to develop and update relevant management rules and regulations based on its business needs. Steps taken include:

- Applied the principle of “minimum and necessity” in the customer information

- Explored the use of AI, big data, and other technologies in customer information risk prevention and carried out innovation in security certification products

- Carried out security inspection of customer information and standardised customer information protection

- Provided special training on “Holding the Bottom Line to Protect Consumer Information Security” to enhance the awareness and ability to protect customer information effectively

IT strategy

CCB has formulated an ongoing Information Development Plan with emphasis on six technological improvements. These technological improvements are platform-based, modularised, and cloud service-oriented and form a shared, agile, and collaborative enterprise-class digital technology foundation for the bank.

- Artificial Intelligence – The bank pressed ahead with its fintech strategy. It established the support capacity of AI technology with 424 AI scenarios, covering areas such as customer service, risk management, centralised operation, and smart government affairs service.

- BlockChain – The bank improved the blockchain layout and expanded the application and innovation of blockchain technology into areas such as international trade, smart government affairs, and supply chain service.

- Cloud Computing – The use of cloud computing was to build diversified application scenarios and share financial service experience. CCB launched CCB Cloud, a cloud service brand constructed and handled separately by the bank based on cloud computing, to develop multi-dimensional fintech products and an assortment of ecological services to all sorts of customers.

- Big Data – The bank uses big data in its modern risk control system, which monitors early warnings, control, and resolution to assess customer risks accurately.

- Big data was also put to use in intensive capital management to save capital further and reduce ineffective and inefficient capital occupation.

- Internet of Things – The bank completed its pilot Internet of Things (IoT) specific network project, which connects to more than 200,000 IoT terminals and empowers 15 IoT applications, including the “Intelligent Security”, “5G+ Intelligent Banking” and “CCB Yunongtong”, featuring a preliminarily established IoT ecology.

- Quantum Information – CCB was the first to establish the Laboratory of Quantum Application in Finance to explore the applications of quantum security, quantum communication, and quantum computing in financial scenarios.

ICT contracts:

- Collaboration with Tencent to develop a financial technology joint innovation laboratory in Shenzhen

- Collaboration with the One Belt One Road Association Malaysia for small and medium-sized enterprises to participate in China’s 127th Import and Export Fair

- Partnership with BlackRock Inc. to expand its footprint in the country’s asset management market

- Agreement with China Chengtong to help optimise SOR’s capital structure and increase capital allocation efficiency

- Alliance with Cambodian Public Bank (Campu Bank) to jointly promote and develop business opportunities between both banks for their customers

8 Growth and Innovation Opportunities:

- #1 Transformation of the branch and its branch network

At the end of 2020, CCB has a total of 14,708 domestic entities, this includes the headquarters, 37 tier-one branches, 361 tier-two branches, 14,117 sub-branches, 191 outlets, a specialised credit card centre at the headquarters and 33 overseas entities.

The bank’s self-service channel has 79,144 ATMs, 25,529 self-service banks and 48,733 smart teller machines.

Towards the end of 2020, 96.57% of financial transactions with the bank were via its digital and electronic channels. The bank’s customers are migrating towards digital and electronic channels. As a result, the number of personal online banking customers rose by 8.93% compared to 2019. The number of corporate banking customers using online banking also increased by 13.23%.

The bank should reduce the number of physical branches as its customers prefer digital and electronic transaction modes. While the bank’s operating costs have seen a minimal increase over the previous year, it can vastly reduce the administrative, maintenance, and infrastructural expenses by reducing the overall branch network. Currently, the infrastructure and equipment cost of maintaining the branches is USD 5.34 billion.

CCB can also adopt the below measures to digitalise and consolidate its branch network further:

- Replace ATMs with Interactive teller machines (ITMs), which can provide the same set of services without human intervention.

- ITMs can help reduce the bank’s branch size, eliminate the personnel cost of running the branches, and bring down the infrastructure costs of maintaining branches

- The bank can conduct a branch review to identify low footfall, sales volume, and declining revenue branches to either consolidate with a corresponding sub-branch or shut down completely.

- #2 Customer experience

CCB should turn its customer experience from single-point interactions to a journey that a customer goes through when associating with it. Thereby, the bank will aptly connect a single bad interaction and the future behaviour of a customer. To improve the experience and efficiency, CCB needs to reset its customer experience priorities. This can be done by:

- Responding to each customer based on their specific complaints and feedback, rather than relying on a survey that few customers fill out

- Integrating chatbots to offer information about the various services offered by the bank

- Implementing virtual assistants in branches to handle customers, thereby reducing the ratio of employees per customer

- Improving the interface of the website and the mobile app to be more interactive and include detailed information on products and services rather than just basic details

- Offering personalised product stacks to cater to the financial needs and goals of customers

- Extending its “CCB Yunongtong” financial doorstep service to other areas other than the areas in the Guzhang county

- Educating customers who are not familiar with digital services by rerouting their calls to contact centres that teach them how to use digital channels

- Implementing an omni-channel experience for customers by consolidating its physical and digital domains for a seamless customer experience

- Integrate predictive analytic tools, such as budgetary tools for personal financial management

- #3 Employee experience and productivity

The bank conducts a wide array of training programs for its employees to make them competitive and enhance their capabilities and competencies. The bank has also set up the CCB University, which focuses on the employees’ entire career path. However, CCB should focus on the well-being of its employees. This can be done by:

- Integrating a hybrid-work model in the business operations – employees get flexibility in their working hours and can opt to work from home or in-office

- Giving extended parental and maternal leaves to parents to bond with their new-borns

- Incorporating rewards and benefits, such as stock options for long-term employees

- Embracing mental health programs to cater for employees suffering from mental health issues

- Providing counselling to deal with grief and loss

- Detecting moments that matter for an employee outside the workplace, as they can have an impact on their job satisfaction

- Giving rewards and benefits that go beyond the remuneration provided

- Giving employees digital tools to access the bank’s servers and conduct digital account opening

- Setting up an organisational culture that pays emphasis on an employees’ journey from when they are hired to when they leave

- #4 Neobanking

CCB has innovatively launched version 5.0 of its personal mobile banking application. The app integrates edge computing, speech recognition and biometrics. This redesigned app version now has an in-built intelligent search system, an intelligent voice interaction feature and a new way of processing businesses, requiring voice input only.

CCB can use these innovative features to compete with other rising neobanks in China, like WeBank, MYBank and XW Bank. It can strengthen the position of its mobile banking application to become a digital bank of the future by:

- Offering personalised services like spending, budget, and investment analytics

- Focusing more on providing services to the impoverished small-medium enterprises (SMEs)

- Partnering with fintech firms that cater to specific needs of the millennials and Gen-Z market, such as gig workers, byte loans, small-ticket insurances, etc.

- #5 Artificial Intelligence (AI) in everything

CCB is investing in the technological know-how of AI as a critical aspect of the IT plan. The bank can increase the use cases of AI by:

- Implementing AI systems in the bank’s operations to evaluate the credit rating of a customer (based on their credit history) more accurately to avoid default in repayments

- Integrating AI in the bank’s mobile application to track financial transactions and analyse user data to check for abnormalities

- Using AI and ML at various customer touch-points for customer profiling and identifying potential customers for cross-selling and upselling products

- #6 Migration of workload to the cloud

CCB Cloud is the bank’s cloud service brand which operates independently and serves the bank based on cloud computing. It provides multi-level fintech products to all kinds of users. The bank should take further actions to improve its cloud capabilities. This will help CCB reduce its infrastructure footprint and lower ownership costs. CCB can do this by:

- Using cloud-native tools to generate insights from data about customer behaviours to identify areas that need improvement

- Enhancing operational security and efficiency by migrating routine, low-risk transactions to its virtual cloud environment

- #7 Security

A risk management committee oversees the bank’s risk management structure. The committee and the board of directors ensure that the bank’s risk management system protects CCB against market, credit, liquidity, operational, reputational, and strategic risk.

The bank improved its management efficiency and adopted digital tools for credit processing, improved the credit risk monitoring system, enhanced the credit customer selection, and improved collateral management. CCB should implement the use of technology in its traditional security practices by:

- Providing employees with training on cybersecurity

- Using multi-factor authentication feature to log into the website

- Integrating the use of biometrics in the mobile app

- Implementing the use of Know Your Customer (KYC) updates for customers

- Allowing access to the bank’s servers only through a VPN when using public WiFi

- Requiring frequent change of log-in and transaction passwords to safeguard the customer’s account

- #8 Society and planet contribution

CCB has taken initiatives to implement green strategies via green financing through green credit, which made investments in green projects that reduced the consumption of coal and water. The bank also implemented green methods in its day-to-day operations by making its office premises eco-friendly and implementing a procurement strategy featuring low emission and energy saving.

While CCB is taking the efforts mentioned above to help the society and planet, it should also take stringent steps to reduce its energy consumption and greenhouse gas emission, which is among the highest and currently stands at 551,005 Mwh and 351 (kt), respectively. CCB can do this by:

- Establishing solar panels and other sources of renewable sources of energy

- Positioning motion-sensing lights to reduce electricity consumption

- Making use of smart plugs and sockets

- Installing faucets with in-built timers to reduce the water consumption

- Shifting to using more energy-efficient lighting

- Encouraging employees to use bikes or electric vehicles instead of traditional vehicles

- Using a programable thermostat and keeping a check on the temperature

- Practising the 3R’s – Reduce, Reuse, Recycle

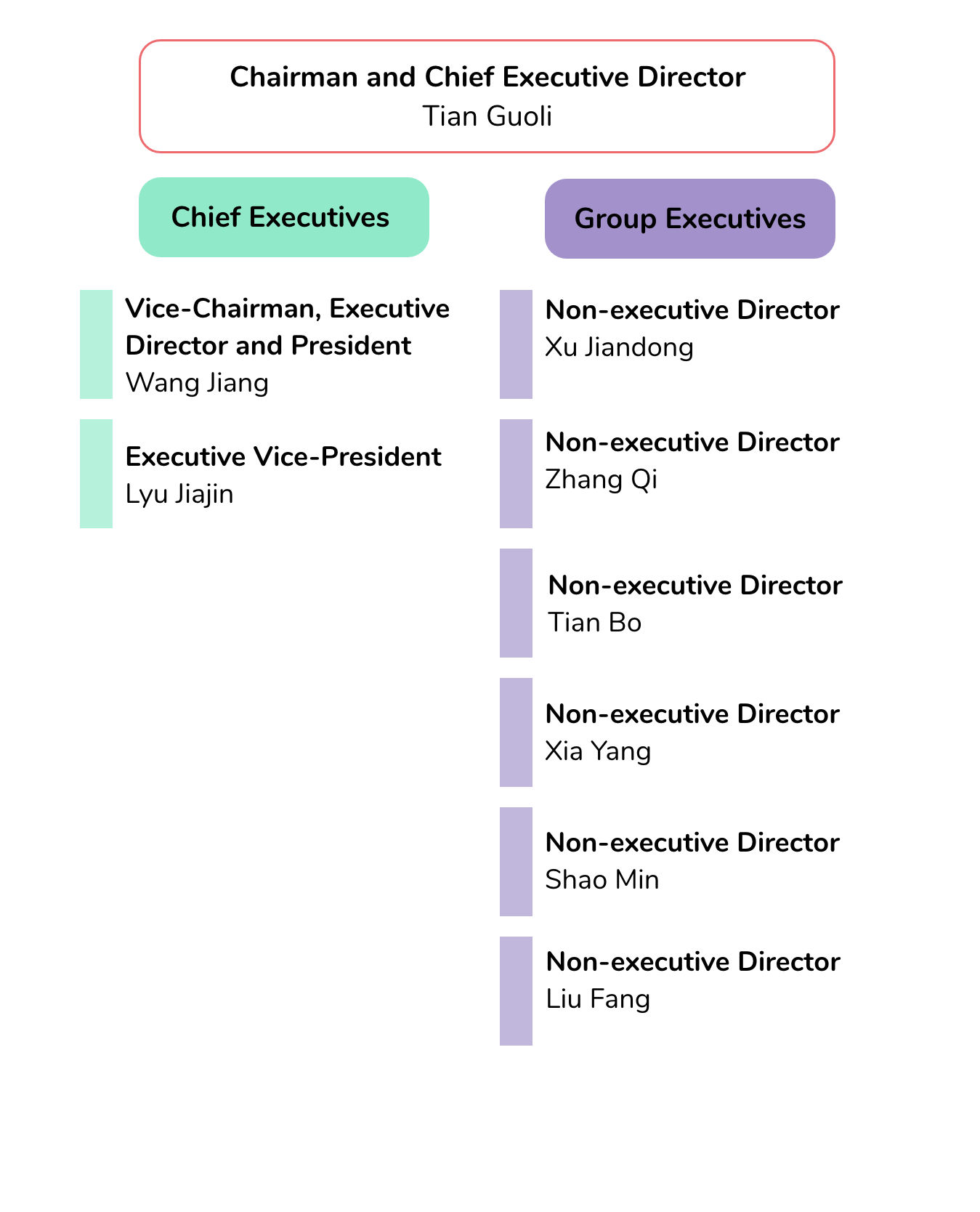

Organisation Structure

Executive profile:

Tian Guoli

Chairman, Executive Director

Tian Guoli served as chairman and executive director of CCB since October 2017, concurrently as the chairman for Sino-German Bausparkasse since March 2018. He is a senior economist and has received a bachelor’s degree in economics from Hubei Institute of Finance and Economics in 1983.

Wang Jiang

Vice-Chairman, Executive Director, President

Wang Jiang has served as vice-chairman and executive director of the bank since March 2021, concurrently as president of the bank since February 2021. He has received a PhD degree in economics from Xiamen University in 1999.

Quote

- Business Strategy, Annual Report 2020

We will achieve remarkable results in implementing the concept of New Finance by making solid progress in house rental business, inclusive finance and FinTech.

Lyu Jiajin

Executive Director, Executive Vice President

Lyu Jiajin has served as an executive director of the bank since December 2020, concurrently as executive vice president of the bank from July 2020. He is. Senior economist and has obtained a PhD degree in economics from Southwestern University of Finance and Economics in June 2014.

Xu Jiandong

Non-Executive Director

Xu Jiandong has served as a non-executive director of the bank since June 2020. He has obtained a bachelor’s degree in finance from the Central University of Finance and Economics in 1986.

Zhang Qi

Non-Executive Director

Zhang Qi has served as director of the bank since July 2017. He studied at the Dongbei University of Finance & Economics and obtained his Bachelor’s, Master’s and PhD degrees in 1995, 1998 and 2001, respectively. He is currently a PhD supervisor at Dongbei University of Finance & Economics.

Tian Bo

Non-Executive Director

Tian Bo has served as a director of the bank since August 2019. He graduated from Beijing College of Finance and Trade in 1994 with a Bachelor’s degree in finance. He obtained a Master’s degree in management in 2004 from the Capital University of Economics and Business.

Xia Yang

Non-Executive Director

Xia Yang has served as director of the bank since August 2019. In addition, he is a senior economist and accountant. Xia Yang graduated from Nanjing University with a bachelor’s degree specialising in human and animal physiology in 1988. He graduated from Nanjing University with a PhD degree in management sciences and engineering in 2018.

Shao Min

Non-Executive Director

Shao Min has served as director of the bank since January 2021. She graduated from the School of Accounting of Dongbei University of Finance & Economics with a bachelor’s degree in economics in 1987.

Liu Fang

Non-Executive Director

Liu Fang has served as director of the bank since January 2021. She obtained a master’s degree in world economics from the School of International Economics of the Renmin University of China in 1999.

Appendix A

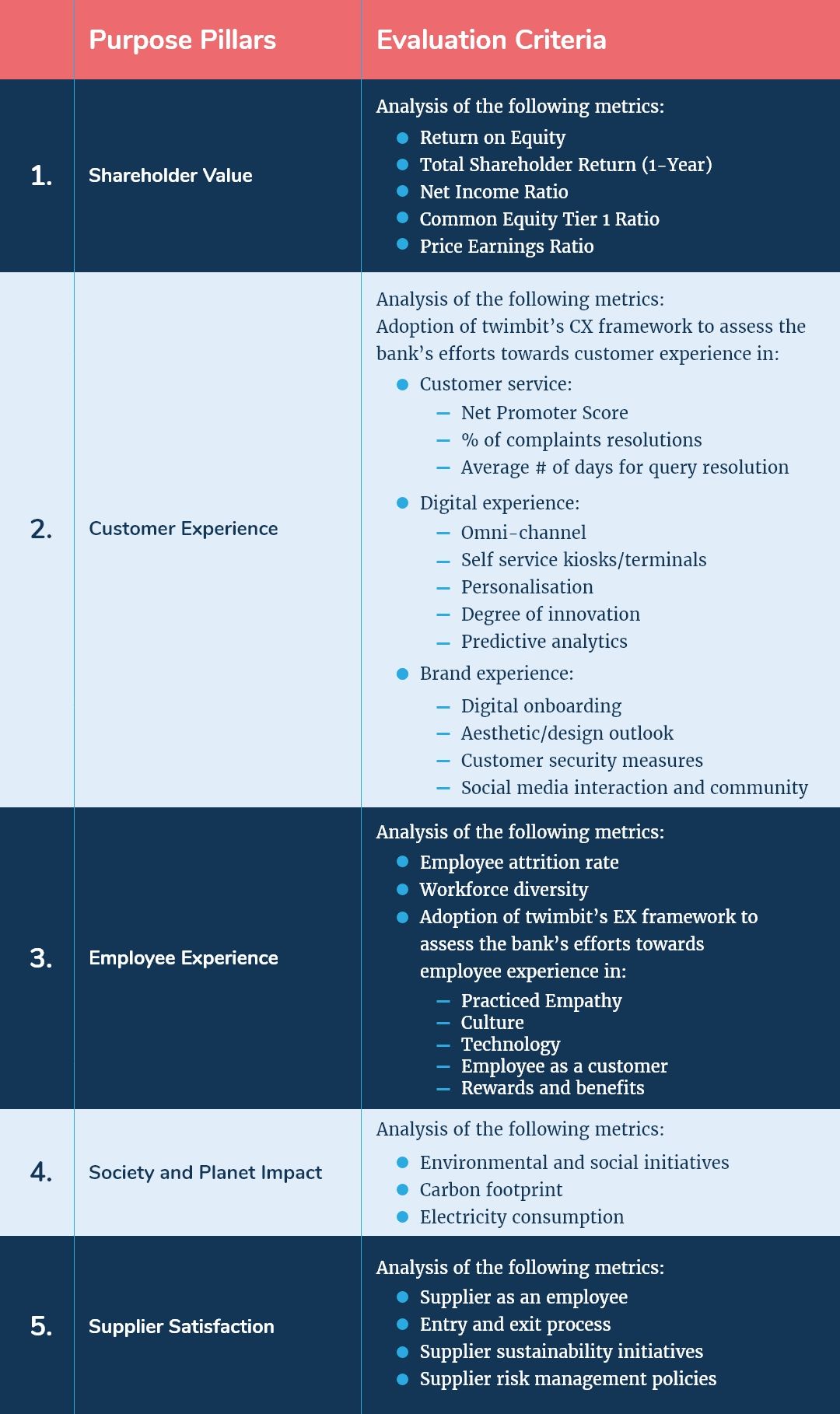

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Borneo Post. Company News. Retrieved October 1, 2021, from

https://www.theborneopost.com/2019/11/01/campu-bank-to-collaborate-with-china-construction-bank/

CCTGroup. Company News. Retrieved October 1, 2021, from

http://www.cctgroup.com.cn/cctgroupen/media%20centre/headlines/642458/index.html

China Construction Bank Corporation, (2020, December 31). Annual Report 2020.

http://www.ccb.com/en/newinvestor/upload/20210428_1619614419/20210428205022826915.pdf

China Construction Bank Corporation, (2020, December 31). Corporate Social Responsibility Report 2020.

http://www.ccb.com/en/newinvestor/upload/20210327_1616775640/20210327001724508034.pdf

Finews. Company News. Retrieved October 1, 2021, from

https://www.finews.asia/finance/28590-tencent-partnerships-china-construction-bank-gansu-bank

Nikkei. Company News. Retrieved October 1, 2021, from

Reuters. Company News. Retrieved October 1, 2021, from

Simply Wall Street. Company Financials. Retrieved October 1, 2021, from

https://simplywall.st/stocks/hk/banks/hkg-939/china-construction-bank-shares#valuation

Xinhuanet. Company News. Retrieved October 1, 2021, from