Company Insights

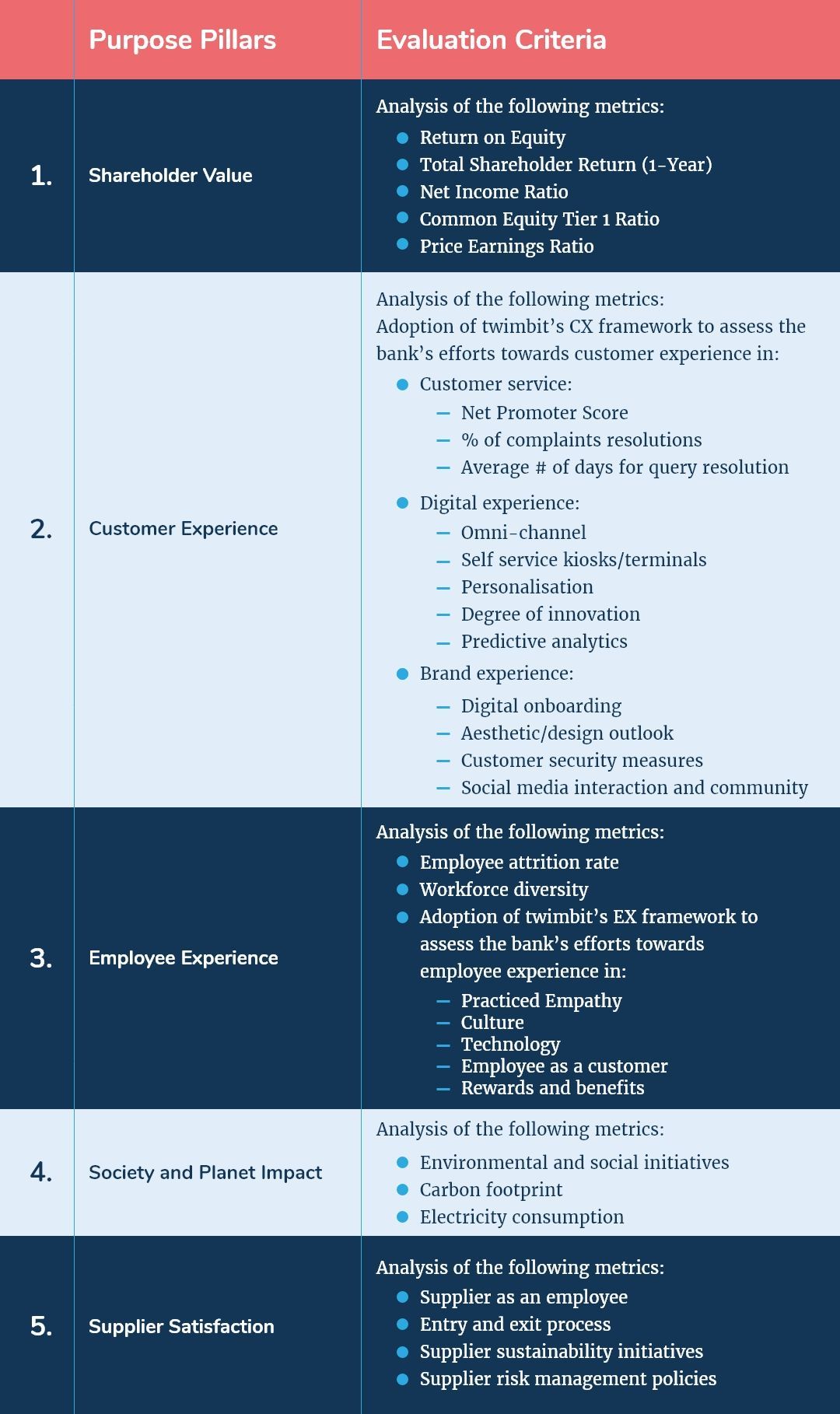

twimbit’s Purpose Index

Source: Refer to the methodology in Appendix A below

Housing Development Finance Corporation Limited Financials – An overview as of 31st March 2021

| Bank Name | Housing Development Finance Corporation Limited (HDFC) |

| Headquarters | Mumbai, India |

| Operating revenue | USD 12.31 billion |

| Group net profit | USD 4.25 billion |

| Total Assets | USD 238.62 billion |

| Employees | 120,093 |

| Countries in operation | 5 |

| Number of branches | 5,608 |

| Technology Investment | USD 380 million |

| Number of customers | 60 million |

| Market capitalisation | USD 123.55 billion |

| Operating Revenue CAGR growth (2016-2021) | 14.67% |

2. Conversion rate to USD as of 31st March 2021 – 0.01366 USD

Shareholder value

| Return on Equity (as of 31st March 2021) | 16.6% |

| Total Shareholder Return (1-Year) | 74.05% |

| Net Income Ratio | 34.54% |

| Common Equity Tier 1 Ratio | 7.58% |

| Price Earnings Ratio (as of 31st March 2021) | 26.40 |

Awards

| 2020 | The Banker: India’s Best Bank Finance Asia: Best Bank in India ET: Marketing and Brand Innovation of the Year Award |

| 2021 | Euromoney: Ranked No. 1 in the Mass Affluent category Asiamoney: India’s Best Bank for SMEs Finnoviti: Award for Warehouse Commodity Finance on Mobile |

HDFC Bank and its strategic focus areas:

- Business strategy

HDFC Bank (“HDFC”) is targeting a “One Bank” collaborative. Under this strategy, the bank aims to serve all business verticals through every possible delivery channel, driven by the diverse skills of its workforce and its multifunctional exposure. Ten growth engines drive the bank’s strategy for 2021, which also has the backing of HDFC’s traditional strengths in internal audit, underwriting, risk management, and governance.

- Reimagining the branch channel:

- Centred around holistic customer lifecycle management and the ability to understand customer insights and provide the right products

- Analytics-led customer conversations and a distribution planning tool allows the team to make data-driven decisions on key issues (like opening new branches)

- The digitisation of sales, service, and branch operations

- Customer service excellence at every touchpoint by simplifying and digitising the process

- People capability – Understanding the voice of the customer and using this understanding to create new propositions and an engaging customer experience

- Virtual Relationship Management (VRM):

- The bank has invested in a VRM channel to advance customer engagement and enhance the service experience

- VRM covers three pillars – virtual relationship, virtual sales, and virtual care

- It serves the customer lifecycle under five pillars – Save, Invest, Borrow, Transact, and Engage

- Semi-Urban & Rural (SURU) and Government & Institutional (GI):

- The bank uses CSC, a specific vehicle to offer digital facilities; CSC increases the distribution footprint in semi-urban and rural areas without the need for traditional branches

- Leader in the payments business:

- HDFC is a dominant player in the payment ecosystem in both the card-issuing and acquiring businesses

- The bank has the most extensive suite of payment form factors, including cards, POS terminals, payment gateways, UPI, and QR

- Every third Indian Rupee spent on cards in India happens via HDFC bank cards

- Technology and digital:

- Focusing on making banking easy for young, old, urban, and rural customers

- Creating secure APIs and microservices for information interchange

- Leveraging data analytics

- Commercial and rural:

- The strategy encompasses SMEs and MSMEs, emerging corporates, mid-market companies, commercial agriculture, and commercial transport companies

- Is the bank’s fastest-growing market group, which contributes significantly to India’s manufacturing output and employment

- Retail assets:

- Continued focus on the salaried segments with top-rated corporates and government institutions across geographies

- Corporate cluster:

- The focus is to deepen corporate relationships with more attention to their funding requirements

- Serves the entire ecosystem of large corporates

- Wealth:

- HDFC aims to cover a large geographical spread and provide differentiated wealth management solutions; the bank uses digital tools to increase its wealth management customer base

- Digital marketing:

- Create brand awareness and consideration about the financial solutions and develops customer brand loyalty

- Deliver business portfolio objectives using an omni-channel forte

- Contribute to direct business generation by targeting the right customer with the right product, at the right time, in their preferred channel of communication

- Customer experience

HDFC commits to keeping customers at the centre of everything it does. The bank’s value and recall reflect this commitment. The bank caters to a customer base that is diverse, ranging from individuals, farmers, startups and MSMEs to the government and large corporates. It does the following for its customers:

- Eliminating geo-dependencies:

- Customers can access HDFC services anywhere, regardless of where their account is from

- Customers can also access their accounts from their homes or while on the move through Net Banking and Mobile Banking

- Customer services and grievance redressal:

- HDFC plans to seek customer feedback and benchmark itself with best-in-class business entities

- The bank reviews its performance on customer service as well as customer grievance redressals

- Service monitoring and measurement mechanism:

- The bank has set up practices to monitor and measure the quality of services provided regularly, not only at various touch-points but also at product and process levels

HDFC has taken the following customer service initiatives:

- Mobile ATMs – The bank deployed 49 mobile ATMs across 47 cities in India to assist its customers during the lockdown. These ATMs eliminated the need to move out of localities to withdraw cash:

- The mobile ATMs could help customers with 15 varying transaction types

- ‘e-Kisaan Dhan’ App for farmers – The app provided farmers with access to agricultural and banking services from their mobile phones:

- Customers can access value-added services like “mandi” prices, farming news, information on seed varieties, Kisan TV, and more.

- Various banking services like procuring loans, opening a bank account, insurance facilities and more are also available on the app.

- HealthFirst initiative – HDFC launched a joint initiative with Apollo Hospitals to provide bank customers with exclusive access to quality healthcare through the hospital’s HealthLife program, along with an easy financing option.

- Business Banking Group (BBG) Workshops – HDFC conducted knowledge-sharing workshops, where it reached out to customers and informed them about the impact of COVID-19 on the Indian economy, forex, and markets; the bank also guides on how to navigate through the same.

- Banking beyond business: ‘Health Webinars’ – the bank conducted several webinars and other initiatives for its customers in preventive healthcare:

- HDFC conducted two awareness webinars (on World Senior Citizen’s Day and World Cancer Day)

HDFC has made the following improvements in its operations:

- Maintained a disability-friendly infrastructure to empower all customers

- In order to improve the bank for people who are physically challenged, HDFC has:

- Equipped all ATMs with a voice-guided system and a braille keypad for the visually challenged

- 718 ATMs with ramps to provide access to customers who use wheelchairs

- Providing an omni-channel experience by making all the bank’s products available at every customer touchpoint

- Employee experience

HDFC dedicates itself to promoting a culture of inclusion, diversity, growth and progression. It also cares for the wellbeing of its employees. The bank focuses on creating a valuable work environment that promotes active character and professional development, and the participation of its employees.

HDFC does this by concentrating on the following areas:

- Learning and development – The bank has a Leadership Competency Framework and a Functional Capability Framework in place, both of which help develop the core competencies required in an employee to achieve the bank’s strategic and operational objectives:

- An annual needs assessment exercise forms the basis of the training modules

- HDFC provides training through various modes — classroom sessions, e-learning certifications, guest lectures, and more

- Provided over 180,000 person-hours training on human rights and over 67,000 person-hours on anti-corruption and KYC (Know Your Customer)

- Diversity and inclusion – HDFC is committed to cultivating a culture of inclusion, diversity, growth and progression, and wellbeing. The bank is pivoting its attention towards women empowerment in the workplace and is doing so by:

- Providing equal and fair remuneration opportunities, irrespective of gender

- Adopting a gender diversity target to increase the representation of women in the workforce to 25% by FY2025

- Launching Careers 2.0, which helps skilled women professionals who opted to take a break due to family/personal reasons to transition back to work

- Prioritising female hiring by offering an additional referral bonus for women candidates

- Employee wellbeing – HDFC believes that an engaged workforce is key for creating ‘Happy Customers’. The bank constantly explores new possibilities and opportunities to provide for its employees and has done this by:

- Conducting regular medical check-ups and creating awareness on best health practices

- Providing counselling to help employees deal with mental health issues through a dedicated helpline

- Organising 15 health talk webinars on COVID-19-related topics to support and navigate employees through the pandemic

- Establishing a maternity care programme for female employees on the path to embracing motherhood

- Employee engagement – Apart from excelling in the professional space, the bank launched a series of initiatives to enable employees to nurture themselves holistically. It held several events covering sports, arts, music, culture, and nature. As many as 44,130 employees participated in the 16 initiatives organised. Some of these events are:

- Morning fitness sessions – These sessions included Zumba, yoga, meditation, aerobics, pilates and more. As many as 8,347 employees benefitted from these sessions.

- Art & Craft sessions for kids – These included hobby classes, DIY workshops and choreography sessions. A total of 11,745 employees participated with their children.

- AnalytIQ – An online brainteaser contest to challenge employees, it saw the participation of 3,500 employees.

- Zaika – A culinary skill contest organised in an online format and executed in 10 cities across India. HDFC calculated that 1,193 employees participated in the initiative.

For a detailed analysis on how HDFC is further enhancing its EX, check out https://twimbit.com/insights/hdfc-bank-2/.

- Society and planet impact

HDFC focuses on environmental, social and governance aspects while designing its products, processes, and policies. The bank targets to become carbon neutral by FY2032 and has the following initiatives to reduce its climate and environmental impact on the planet:

- Digital banking initiatives – The bank is reducing its paper usage and emissions footprint by:

- Implementing digital banking initiatives like mobile banking, net banking, and more

- Introducing digital products and services in rural and semi-urban areas

- Saving 1.5 million square feet of paper through the “Green Event” initiative

- Ambitious plantation target:

- Planted more than 600,000 trees during FY2021

- The bank targets to plant 2.5 million trees by FY2025

- Green buildings:

- Two large buildings have been Leadership in Energy and Environmental Design (LEED) certified, and two more are in the pipeline

- The Bangalore Data centre is a certified green data centre

- Use of renewable energy:

- Installed solar panels at large office locations in Bhubaneshwar, Chandigarh, Jaipur, Mumbai, Noida, and Pune with a cumulative solar capacity of 198.3 kWp

- Energy reduction initiatives:

- Implemented the energy management system across 600 branches

- Installed inverter ACs and used LED lights

- Keeping the branch temperature at optimal levels

Social responsibility:

HDFC launched the HDFC Bank Parivartan initiative to help develop the less-privileged sections of society. The initiative has five pillars, which are:

- Rural development – The bank has made interventions in soil, farm-based livelihoods, water conservation, on-ground training of farmers, creation of Farmer Producer Organisations, education, sanitation, and Natural Resource Management.

- The Holistic Rural Development Programme (HRDP) is active in 1970 villages across 21 states

- The initiative led to the construction of 8,800 water conservation structures

- It has trained more than 100,000 farmers

- Promotion of education – Parivartan is being executed in partnership with several leading non-governmental organisations (NGOs). The program encompasses teacher training, scholarships, career guidance, and infrastructure support:

- ‘Teaching the Teacher’ (3T) programme seeks to transform education in government schools by improving the skills of teachers

- More than 1.9 million teachers trained across 28 states/union territories are under the 3T programme

- It introduced 980 digital classrooms in state-run schools across eight states

- Skill training and livelihood enhancement – Under this programme, the bank targets the people in rural India. It imparts income-generating skills, primarily in agriculture and allied areas (such as dairy and poultry). The programme also provides career counselling to school students:

- The programme has benefitted more than 170,000 people

- The Sustainable Livelihood Initiative (SLI) is the flagship programme under Skill Training and Livelihood Enhancement:

- The programme aims to create sustainable communities by empowering women

- The programme has trained more than 780,000 women

- Healthcare and hygiene – The sanitation projects focus on infrastructure creation and behavioural changes. The core of the programme is community-led sanitation campaigns that promote hygienic conditions in rural areas through appropriate waste disposal:

- The programme has helped with the construction of more than 23,500 toilets in households

- Health camps organised not only offer diagnostic services but also assist the communities on other sanitation and hygiene aspects

- Financial literacy and inclusion – HDFC conducts financial literacy camps at its banking outlets and financial literacy centres across the country through NGO partners. The camps enrich communities with knowledge about savings, investments, and organised finance:

- The flagship programme under this initiative, Digidhan, moves across the country on wheels, explaining the benefits of digital banking through an audio-visual mode:

- More than 1.8 million financial literacy camps organised

- As many as 14.2 million beneficiaries reached

- The flagship programme under this initiative, Digidhan, moves across the country on wheels, explaining the benefits of digital banking through an audio-visual mode:

Digital strategy

HDFC considers digitisation as an important enabler for the bank’s vision to offer a distinctive customer experience. The bank’s digital strategy follows a philosophy that stems from empathy for its customers and its employees.

HDFC has a two-pronged approach to digitisation — digitising its current banking facilities and building for the future. The bank designs its products to make digital banking simple, easy, contextual, and highly secure.

HDFC intends to transform its branches into ‘phygital’ financial marketplaces through catchment scoping and mining with institutionalised consistency. Additionally, customers need centric conversations enabled through artificial intelligence-led predictive analytics.

Following are the key digital initiatives taken by the bank:

- Rural digital initiatives – The bank’s initiatives align with the Government of India’s, which in turn has helped HDFC penetrate semi-urban and rural markets:

- The bank has been able to extend its services at the Gram-Panchayat level

- Video KYC – The V-CIP service for video KYC aims to offer an enhanced customer onboarding experience for new customers:

- This has helped reduce account opening Turnaround Time (TAT) with higher conversions

- It is easy to open an account from the comfort of one’s home or office

- Opened a total of 236,861 accounts using V-CIP

- Customer Experience Hub (CXH) – A platform that will provide an omni-channel banking experience for customers. It enables banking transactions on more than ten self-assisted and agent-assisted channels:

- The platform provides customers with personalised digital banking experiences while also raising their engagement levels and encouraging them to adopt digital self-service workflows

- Digital journeys – The initiative replicates existing features, products or services available on other platforms to streamline all online forms and provide a consistent customer experience:

- The personal loan digital journey has helped the bank digitise the lending process to easily onboard customers and achieve efficiencies through faster credit decisions and reduced costs

- Extending APIs for partners – The initiative has helped HDFC extend APIs to internal and external platforms and achieve a more extensive distribution network for banking products and services. This allows the bank to present on the customer’s platform of choice.

Security strategy

HDFC is continuously improving its technology protection systems for cybersecurity and enhancing protection capabilities. The bank is doing this by:

- Strengthening firewalls to scan for potential security breaches and issues

- Preventing cybersecurity threats by implementing two-factor authentication, strengthening anti-virus features for in-home devices and prohibiting any download on local storage devices

- Sustaining operational effectiveness and efficiency through a secure work-from-home environment

- Adapting and updating its cyber-defence framework to counter new-age threats

- Continuous information security awareness for employees and customers

IT strategy

HDFC is focusing on the adoption of data analytics and emergent technologies such as Artificial Intelligence (AI) and Machine Learning (ML) to achieve operational efficiencies by:

- Digital factory – The project focuses on small-ticket credit, ranging from credit cards to personal loans by:

- Building secure and scalable platforms

- Using new-age, cloud-native open-source technologies, micro-services enablers

- Enterprise factory – The bank is building a new data centre and moving towards cloud-based systems by:

- Building enterprise tech capabilities to support its digital factory

- Decoupling the core systems into that of micro-services based business logic, so an outage in one system does not affect the working capabilities of others

- Moving from Monolith to ‘loosely coupled systems’, micro-services architecture

- Enterprise IT:

- Enhancing the core to sustain growth

- Ensuring that the core technologies are ‘always ON’ for building resiliency in the stack

- Upgrading legacy platforms

- Enhanced APIs for integrated end-to-end solutions by:

- Connecting various ecosystems with a variety of financial services

- Leveraging competency in data and analytics by:

- Underwriting capabilities through AI and ML

- Transforming the bank branches into ‘phygital’ financial marketplaces through AI-led predictive analytics

The bank has taken the following initiative to strengthen its technology infrastructure:

- Increasing the capacity to handle UPI:

- The bank successfully managed more than 230,000 UPI transactions in an hour

- Ranked among the top in UPI performance metrics

- Technical declines while accessing the bank’s servers have reduced:

- The average uptime for customers was at 99.91% during the FY2021

- Net banking and mobile banking capacity doubled:

- The infrastructure can now support 90,000 users concurrently

- Migrated core data centres to state-of-the-art facilities

- Completed disaster recovery drills for critical payments systems:

- A switchover takes less than 45 minutes when needed

- Significant upgrades in network and security infrastructure to support the exponential growth in digital transactions

ICT contracts

- Partnership with Paytm to deliver financial solutions to consumers and merchants

- Collaboration with Adobe to enhance personalised customer experience with a focus on a zero-touch digital interface to enable account openings, loans, and investments

- Alliance with Zeta to implement the ‘Digital Factory’ initiative

- Association with Creditas to provide solutions for loans and credit card customers

9 Growth and innovation strategies:

- #1 Cost to serve

The operating expenses for HDFC have been increasing steadily over the years. In FY2021, HDFC’s operation expenses grew by 6.2%, from USD 4.19 billion to USD 4.47 billion.

Under the operation expenses, the following segments saw increases from FY2020 to FY2021:

- Personnel costs from USD 1.30 billion to USD 1.415 billion (8.8%)

- Impairment losses from USD 1.24 billion to USD 1.56 billion (25.8%)

- General administrative expenses from USD 2.89 billion to USD 3.05 billion (5.54%)

One reason for the growth in personnel cost is the high attrition rate, 15.28% — it is expensive to search, hire, and train a newly hired employee.

The credit market has become saturated as every bank is offering the same service to customers. Due to the nature of the market, banks have to become increasingly competitive. In order to stay ahead of the competition, they are reducing their profit margins and, in some cases, taking a risk by extending credit to customers with a low credit score resulting in default in repayments.

On the other hand, the operating revenues have been increasing exponentially. In FY2021 alone, there was an increase of 13.39%, from USD 10.85 billion to USD 12.30 billion for HDFC. The primary contributor to the operating revenue growth is interest income.

Non-interest income indicated a marginal increase. We note that although the bank’s non-interest income saw an increase of 21.5% Y-o-Y in Q2 2021, it contributed only 21% to HDFC’s revenue.

HDFC should focus on the following key areas to optimise its cost structure:

- Pay more emphasis on non-interest income and look for other revenue sources

- Conduct more stringent checks on credit scores before dispersing loans to avoid defaults in repayments to reduce the high loan impairment losses

- Concentrate on areas to lessen its high attrition rate, which will, in turn, reduce the turnover costs linked to hiring and training new employees

- By automating general administrative tasks, the bank will be able to lower the administrative costs associated with repetitive processes

- Reducing the paper used in welcome kits will help in scaling down administrative costs

- #2 Transformation of the branch and its branch networks

At the end of FY2021, HDFC had a physical network of 21,364 banking outlets. This consisted of 5,604 domestic branches, four overseas branches and 15,756 business correspondents. During the year, the bank made additions worth USD 23.84million to its infrastructure cost. The repair and maintenance costs increased from USD 173.20million to USD 220.78million in FY2021, an increase of 27.47%. As much as 95.7% of all retail transactions went through electronic and digital channels.

HDFC is still adamant in pursuing the expansion of its physical branch network. It has previously opened 283 branches in FY2019 and 354 branches in FY2020. The bank has also broadened its ATM network in FY2021 and added 1,186 machines.

The bank has made headway in its digital journey through all customer touch-points (like sales, service, and operations). HDFC uses the mobile-first approach and a customer analytics and distribution planning tool to enclose ‘Need-Based Selling’. This will provide customers with products that are for their needs. While the bank is taking steps to digitalise itself, it can accelerate the process by:

- Replacing ATMs with Interactive teller machines (ITMs) that are capable of providing the same services without in-person tellers

- ITMs can further contribute to reducing the branch size and lowering the infrastructure cost

- Eliminating the branches with low footfall or consolidating branches with low sales volume into one specialised branch

- #3 Customer experience

HDFC keeps its customers at the centre of its operations and provides services that deliver an enjoyable customer experience (CX). The bank also launched various initiatives during the COVID-induced lockdown to continue providing great customer service and initiatives for the rural customers to make banking easier for them.

To improve CX, the bank can implement the following in its operations:

- Omni-channel experience – One of the long-term objectives of the bank is to provide an omni-channel experience to its customers by making all products available at every customer touchpoint. The bank already has a multichannel presence from the traditional touch-points (like branches and phone banking) to more modern touch-points (like net banking, mobile banking, and EVA, the chatbot). Therefore, HDFC can develop an omni-channel experience across all these physical and digital touch-points for a smoother customer experience.

- Self-service kiosks – These customer touch-points will help customers perform basic tasks like cash and cheque deposits, passbook updating and statement printing without human interaction. This will also help the band reduce its personnel cost in the process.

- Personalised products – HDFC should focus on providing customers with products that cater to their specific needs and requirements, like micro-loans, etc. This will further increase customer loyalty and retention.

- Budgetary tools – The bank can integrate a spending and budgeting tool in its mobile app to help customers track their spending and get a predicted bill to assess their monthly targeted expenditure, learning from its peers like CBA (Commonwealth Bank of Australia). To take this further, HDFC can provide an investment analytics tools to help customers with investment recommendations and keep track of their investments.

- #4 Employee experience and productivity

HDFC has various training and development programs to enhance the productivity and wellbeing of its employees. The bank can implement technology to enhance employee experience by:

- Implementing Artificial Intelligence (AI) and data analytics into the training and development delivery channels to get personalised insights about each employee’s learning capabilities

The bank can incorporate rewards and benefits that go beyond stock options, insurance, and accommodation benefits by:

- Giving employees the option to work on cross-department projects for lateral career advancements

- Providing counselling to employees dealing with grief and loss

- Extending pre-natal and child-bonding leaves with childcare assistance

- #5 Migration of workload to the cloud

HDFC has invested heavily in scaling up its infrastructure to handle any potential load for the next three to five years. The bank is currently accelerating its cloud strategy to be cutting-edge, leveraging best-in-class cloud service providers. Investments in advanced analytical tools on the cloud will also ensure a deep understanding of customer behaviour and their preferences to provide customers with personalised products.

HDFC can amplify its cloud capability by:

- Using cloud-based platforms for management and HR-related tasks to streamline operations and lower costs simultaneously

- Provide end-to-end protection of confidential data stored in the cloud; this will help the bank maintain its customers’ trust

- #6 Artificial Intelligence in everything

The bank has already deployed AI-led predictive analytics to increase its operational efficiencies. It also uses AI and Machine Learning (ML) to offer personalised services, credit underwriting and risk control. In addition, HDFC introduced EVA, the chatbot, to provide customer service and became the first bank in India to introduce a humanoid for customer service.

To broaden the application of AI, HDFC can do the following:

- Use AI to process data for improved fraud detection and regulatory compliance

- Use AI-based systems to assess a customer with limited credit history (based on their overall banking behaviour and patterns) to make improved loan and credit decisions

- The bank is making significant investments in areas where it can improve its operations (like analytical tools for the cloud, MarTech solutions for digital journeys, technology upgrades, and the automation of internal processes). It can make use of AI-powered smart systems to help make investment decisions by researching the market for potential untapped investment opportunities, learning from its peers such as ING (International Netherlands Group) and DBS (Development Bank of Singapore)

- #7 Neo banking

HDFC’s mobile banking app has seen the addition of significant features which make it more convenient for its customers. The new app is easy to navigate, uses simpler terms and provides personalised notifications based on a customer’s usage and needs.

The bank should improve on the app by upgrading its user interface (UI) further to enhance the user experience (UX) of its current and potential customers. Some of the changes could include bold design changes, integrating gamified dashboards, and incorporating third party vendor integration within the app. As HDFC is already making strides in digital transformation, implementing these changes will help the bank position itself better among millennials and Gen-Zs.

HDFC should also implement the following:

- Provide personalised products to address the needs of millennials

- Partner with fintech firms to position itself strategically in the market

- Strengthen the capability of the existing EVA humanoid

- Introduce micro-loans and investment options to give flexibility to the target customer segment

- Introduce rewards based on the intensity of use of the bank’s products

- #8 Cybersecurity

The bank has an Information Security Policy and a Cyber Security Policy laid by an independent assurance team with internal audit to protect against attacks such as hacking, phishing, ransomware, and other means. Every threat assessment is based on the framework “Identify, Prevent/Protect, Detect, Respond and Recover”. Controls such as firewalls, anti-malware, red teaming, intrusion detection and many more have been implemented.

Apart from external attacks and threats on the bank, HDFC should also improve its operational capabilities to avoid technical glitches in its IT infrastructure. The bank was recently under scrutiny by the Reserve Bank of India (RBI) due to a series of technical problems in its digital channel over the past two years. These technical glitches, which resulted in RBI banning HDFC from issuing new credit cards, led to a loss of business for the bank. HDFC’s stock fell by 4% after the glitch affected customers services.

HDFC facilitates growth via secure digital initiatives, such as adapting and updating its cyber defence framework to counter new-age threats. The bank can, however, focus on the following areas to improve security:

- HDFC could develop new risk capabilities to account for non-financial risks

- Incorporating Cognitive process automation (CPA) to develop and test new security strategies

- Using predictive analytics in the cybersecurity strategy to identify risk trends

- Performing cyber risk assessments to help identify and manage vulnerabilities

- Use AI and ML to identify data manipulation attacks that are becoming more popular and can often go unnoticed

- Improve the mobile app to avoid technical glitches which prevent customers from using the app

- #9 Society and planet impact

HDFC has a comprehensive strategy to reduce its electricity consumption and reduce its carbon footprint via its eco-friendly green building and use of renewable energy. The bank can also lower its energy consumption by:

- Extending the installation of solar panels to its other office premises (currently only for large offices)

- Eliminating the use of single-use plastic

- Practising the 3Rs – Reduce, Reuse, Recycle

- Making use of smart plugs and sockets and shift to using more energy-efficient lighting

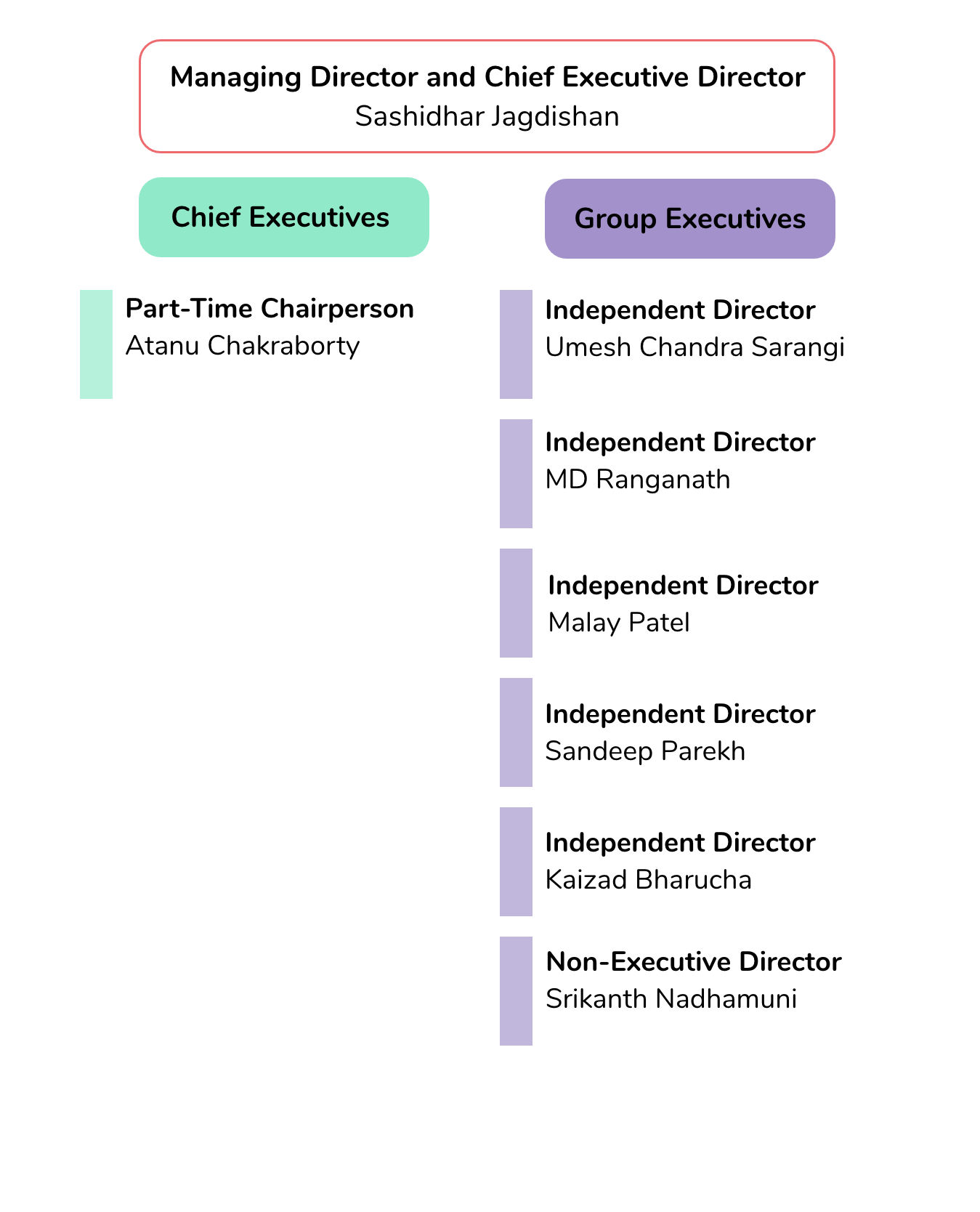

Organisation structure

Executive profile

Sashidhar Jagdishan

Managing Director, Chief Executive Officer

Sashidhar Jagdishan has been the Chief Executive Officer of HDFC bank since August 2020. He joined the bank in 1996 as a Finance Manager and later got promoted to Business Head of the finance department in 1999. Jagdishan was the Chief Financial Officer of the bank will 2019. He is a science graduate and has a Master’s degree in Economics.

Quote

- Business Strategy, Annual Report 2021

Our strategy of expanding our distribution footprint will enable us to capture the growth potential across different consumer segments like the tech-savvy and millennial going forward.

Atanu Chakraborty

Part-Time Non-Executive Chairperson and Additional Independent Director

Atanu Chakroborty has been appointed as the part-time Chairman of the bank by RBI for a period of three years starting May 2021. Chakraborty is an IAS officer and retired as Secretary of the Department of Economic Affairs in April 2020. He previously was the Secretary of the Department of Investment and Public Asset Management. He attained his Bachelor’s degree in Engineering from NIT, Kurukshetra, a Diploma in Business Finance from ICFAI, Hyderabad and a Master’s degree in Business Administration from the University of Hull, UK.

Umesh Chandra Sarangi

Independent Director

Umesh Chandra Sarangi has been serving as an Independent Director for the bank since July 2016. He was the Chairman of the National Bank of Agricultural and Rural Development (NABARD). He holds a Master’s degree in Science (Botany) from Utkal University and has 35 years of experience in Indian Administrative Services.

MD Ranganath

Independent Director

MD Ranganath has been serving as an Independent Director of the bank since January 2019. He previously held the position of Chief Financial Officer of Infosys till November 2018. Ranganath has experience in the Global IT services and financial services industry for over 26 years. He holds a Master’s degree in technology from IIT, Madras and a Bachelor’s degree in engineering from the University of Mysore. He also holds a PhD in Management from IIM, Ahmedabad and is a member of CPA, Australia.

Malay Patel

Independent Director

Malay Patel has been serving as an Independent Director of the bank since 2015. He concurrently serves as a Director on the Board of Eewa Engineering Company Pvt. Ltd. He is a Major in mechanical engineering from Rutgers University, USA and an A.A.B.A. in business from Bergen County College, USA.

Sandeep Parekh

Independent Director

Sandeep Parekh has been serving as an Independent Director of the bank since January 2019. He concurrently serves as the managing partner of Finsec Law Advisors. He holds an LL.M. degree in securities and financial regulations from Georgetown University and an LL.B. degree from Delhi University. The World Economic Forum recognised Parekh as a “Young Global Leader” in 2008.

Kaizad Bharucha

Executive Director

Kaizad Bharucha is the Executive Director of the bank (since 2013) and is responsible for Wholesale Banking. He was previously the Group Head – Credit & Market Risk. He holds a Bachelor’s degree in Commerce from the University of Mumbai.

Srikanth Nadhamuni

Non-Executive Director

Srikanth Nadhamuni is a Non-Executive Director on the Board of the Bank. He previously held the position of Chief Technology Officer of Aadhaar and is currently the Chairman of Novopay Solutions, and is the CEO of Khosla Labs. He holds a Bachelor’s degree in Electronics and Communications from the National Institute of Engineering and a Master’s in Electrical Engineering that he obtained from the Louisiana State University, USA.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

HDFC Bank, (2021, March 31). Integrated Annual Report 2020-21.

HDFC Bank, (2021, March 31). Business Responsibility Report 2020-21.

Bloomberg Quint. Company News. Retrieved October 18, 2021, from

https://www.bloombergquint.com/business/inside-hdfc-banks-plans-to-spruce-up-its-digital-offerings

Business Standard. Company Financials. Retrieved October 12, 2021, from

https://www.business-standard.com/company/hdfc-bank-4987.html

Business Today. Company News. Retrieved November 10, 2021, from

Livemint. Company News. Retrieved October 25, 2021, from

Livemint. Company News. Retrieved October 22, 2021, from

Moneycontrol. Company News. Retrieved November 3, 2021, from

Moneycontrol. Company News. Retrieved November 5, 2021, from

The Economic Times. Company News. Retrieved October 16, 2021, from

The Economic Times. Company News. Retrieved October 29, 2021, from