Company Insights

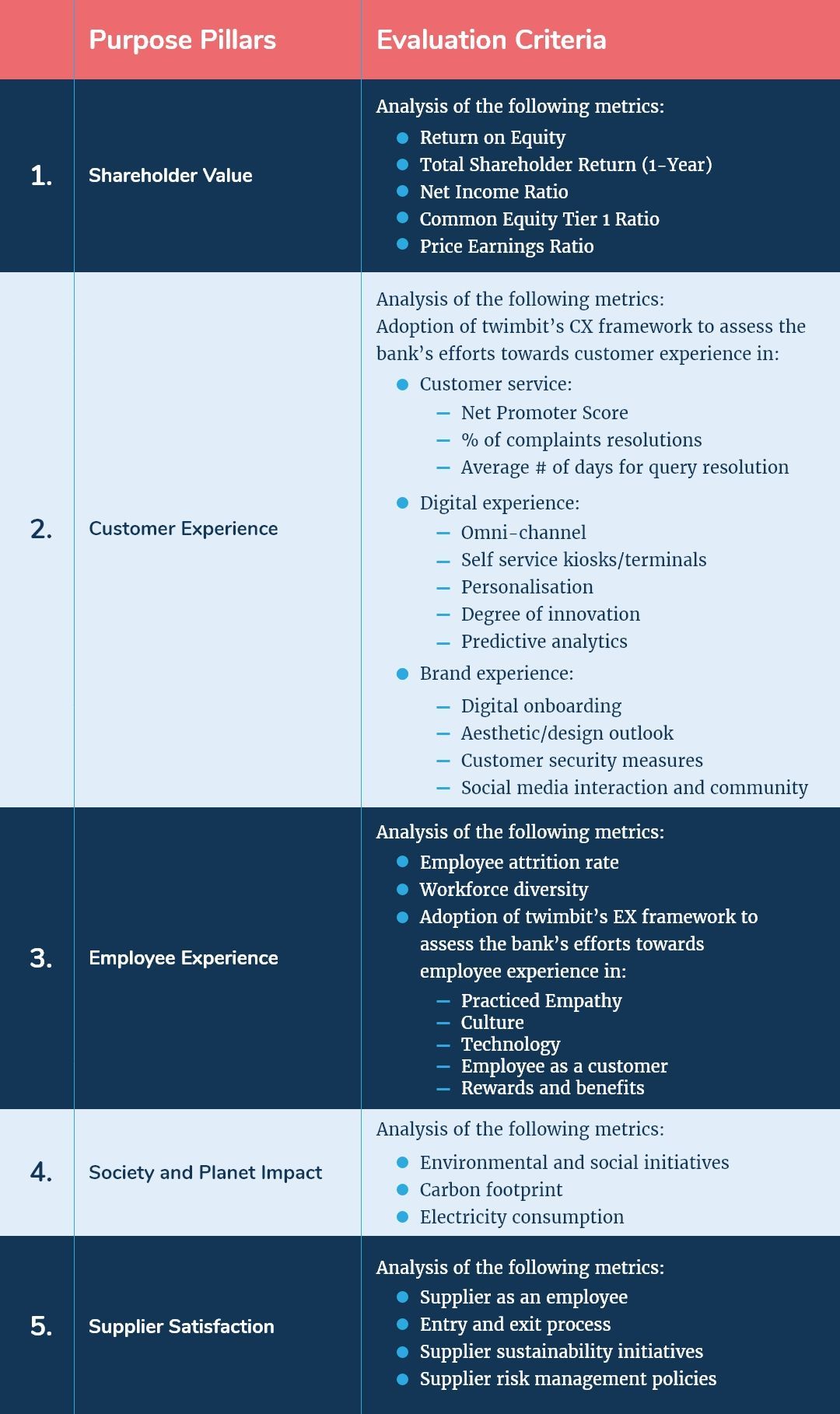

Twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Industrial Credit and Investment Corporation of India Financials – An overview as of 31st March 2021

| Bank Name | Industrial Credit and Investment Corporation of India [ICICI] |

| Headquarters | Vadodara, Gujarat |

| Operating revenue | USD 4.282 billion |

| Group net profit | USD 2.22 billion |

| Total Assets | USD 215 billion |

| Employees | 98,750 |

| Countries in operation | 14 |

| Number of branches | 5,266 |

| ICT spend | NA |

| Number of customers | 21.2 million |

| Market capitalisation | USD 74.50 billion |

| Operating Revenue CAGR growth (2016-2021) | 18% |

2. Conversion rate to USD as of 31st March 2021 – 0.01366 USD

3. As per the management discussion analysis – 32.3% year-on-year increase in technology-related expenses

Shareholder Value

| Return on Equity (as of 31st March 2021) | 12.21% |

| Total Shareholder Return (1-Year) | 65.60% |

| Net Income Ratio | 20.46% |

| Common Equity Tier 1 Ratio | 16.80% |

| Price Earnings Ratio (as of 31st March 2021) | 21.35 |

Awards

| 2021 | The Asian Banker: Best Retail Bank in India FE Best Banks Awards: Best Private Sector Bank Business Today: Bank of the Year |

ICICI Bank and its strategic focus areas:

- Business strategy

ICICI bank is determined to grow its core operating profits within the boundaries of risk and compliance. The bank uses the rapid adoption of technology as its growth opportunity. It aims to leverage its technological capabilities to create value for the customers while offering them comprehensive financial products and services. The bank provides more than 340 services and has more than 150 partners, including 21 unicorns.

For 2021, the bank plans to move forwards with the idea of ‘One Bank, One ROE’ while adopting a customer-centric approach, calibrating risk growth in operating profits and continuous investments in technology inside its key business segments.

- Retail and Rural Banking – The retail business is a key driver of growth for the bank. The focus in the retail business is to fulfil customer needs through personalised banking. The bank is pursuing this strategy by building a diversified and granular loan portfolio to suit its customers’ individual needs.

- Small & Medium Enterprises and Business Banking – Programme-based lending offers SMEs and business banking customers a wide solution range to address their evolving business needs.

- Wholesale Banking – ICICI is building relationships with large companies, MNCs, financial institutions, and government entities by moving from mere credit providers to partners with these clients. Moving forwards, the bank has changed its strategy from a product-centric to a client-centric model. The client-centric model heavily prioritises the client at the centre, and all the groups across the bank align around the client, providing them with the entire offerings from the bank.

- International Business – The bank has its presence in various countries across the globe. The franchisee of the bank focuses on four strategic pillars:

- The NRI ecosystem – Deposits, remittances, investments, and asset products

- The MNC ecosystem – Foreign MNCs investments in India and Indian MNCs investments in foreign countries

- Trade ecosystem – Incorporating India-linked trade transactions

- Funds ecosystem – Capturing fund flows into India through FDI and FPI

- Customer experience

ICICI is on a journey where differentiated customer experience and operational excellence are the core of its business activities. Along the way, the bank aims to continually create value across the customer’s entire lifecycle through easy delivery, low-touch operations, and enhanced customer engagement. Additionally, ICICI has built upon the transition from customer satisfaction to customer delight in banking with the concept ‘Fair to Customer, Fair to Bank’. Furthermore, ICICI launched several customer-centric initiatives during the year:

- Customer 360° – When a customer opens another relationship with the bank, the existing customer data and Know Your Customer (KYC) documents are reconsidered for the purpose

- Insta loan disbursement – The customer would get a link to initiate the loan disbursement

- Online Dispute Resolution – The bank propels an industry-first initiative that enables real-time decision making on reversal of charges by using data science and zero human interaction

- AI-powered bot – With AI implementation in phone banking, the bank can handle 90,000 calls every day

- EazySign – A web platform for SME customers to efficiently execute e-signing of documents and online payments of stamp duty

- All-new bank website – Personalised search and hyper-personalised communication helps with an enhanced customer experience

- Partnerships across ecosystems, co-branded credit cards and e-commerce – The bank partners with these clients to provide differentiated offerings for its consumers and create opportunities for growth

- Employee experience

The bank has adopted a strategy of backward integration to create an industry-ready workforce. This strategy focuses on hiring employees based on their social skills and attitude rather than their English-speaking capabilities. The bank also continually boosts its employees’ morale by continuous engagement across employee segments, periodic communication meetings anchored by senior leaders, and the iCare online portal to raise queries.

ICICI is taking the following initiative for its employees:

- Organising culture, ecosystem, and STACK sessions to enable reiteration help to reinforce its culture among the employees.

- Skilling sessions on ICICI STACK deliver 1.4 million learning hours to employees across business groups. These sessions acquaint employees with its way of selling and to onboard the employees on its digital product suite.

- In partnership with Coursera, ICICI provides training on data science, behavioural finance and model thinking. In addition, ICICI and Coursera offer certificate programmes under this initiative from universities like Johns Hopkins and Duke University.

- Curated video modules on emerging technologies by leading organisations allow the employees to understand various technologies like Blockchain, AI & ML, Cloud, API Ecosystems, etc.

- The Employee App – The ICICI bank UOYM app integrates several functions, including engagement, learning and business applications. The app helps employees keep track of their upcoming meetings, records leaves and attendance and creates business leads.

- Initiatives for woman employees:

- The bank has curated a liberal leave policy for female employees

- Fertility leaves for employees seeking to undergo treatment

- Childcare and adoption leave

- The bank bears travel and accommodation costs for the child (up to 3 years) and the accompanying caregiver or the family member, which allows the female employee to focus on her work

- The bank has curated a liberal leave policy for female employees

- Society and planet impact:

ICICI bank continuously manages its environmental footprint, incorporating several changes in its operations in this endeavour. The bank believes that preserving the environment in its business model can result in a positive impact. The green initiatives are:

- Energy management and conservation – The strategy to manage the environmental footprint is based on effective energy utilisation, focusing on governing and saving it.

- The energy conservation strategy focuses on three areas to achieve the bank’s energy goals:

- Improving existing energy efficiencies

- Investing in superior design and technology

- Adopting renewable energy

- The bank implemented energy-saving measures in 1,100 branches with high energy consumption, which helped save 6.53 million kWh (Kilowatts) of energy

- Replaced diesel generators with lithium-ion batteries to help avoid the pollution caused by the generators

- Replaced old air-conditioning systems with new inverter-based 5-star rated systems; this led to savings of more than 25% of the energy previously used

- The energy conservation strategy focuses on three areas to achieve the bank’s energy goals:

- Water-saving – The bank ensures that the water consumption is lower than the benchmark at its large offices. The water is recycled and reused at three large offices, along with rainwater harvesting at these three large offices.

- All new offices opened during the year were fitted with water-efficient plumbing fixtures

- Waste management – Continuous aim to minimise the waste generated by the bank’s operations. The strategy is in line with the philosophy of ‘Reduce, Reuse and Recycle’. The bank manages and handles the waste generated within the bank accordingly:

- Wet waste – The organic waste is recycled by composting and using it as fertilisers in the gardens at the bank’s large office premises.

- E-waste – The waste is safely disposed of and recycled by certified recyclers.

- Dry waste – The majority of dry waste is the result of using paper. The bank is reducing its paper usage and shifting towards using an environment-friendly form made from wheat straw, residual material from agriculture.

Social responsibility

The bank has taken the following initiatives:

- Boost the aspirations of rural communities – The strategy revolves around serving rural value chains by leveraging opportunities in different ecosystems within the rural market. This strategy’s core compromises six ecosystems – agriculture, dealers, self-employed, corporates, institutions, and micro-entrepreneurs. Adhering to the needs of these ecosystems, the bank has made up products and services to meet the needs of these groups.

- Promoting financial inclusion – The bank undertakes various drives to reach out to customers in rural areas. It has opened 21 million Basic Savings Bank Deposit Accounts (BSBDA), the biggest amount by any private sector bank in India.

- ICICI has a Financial Literacy Plan in place to educate rural customers about financial savings.

- Micro-Lending – The bank aims to assist people employed at the grassroots level in the rural economy, which require a more supportive and sensitive response to their financial requirements. There are specific programmes by the bank to address necessary concerns:

- Self-Help Group-Bank Linkage Programme (SBLP) – Groups made by less than 20 women engaged in livelihood activities. The bank inspires the concept of entrepreneurship among the deprived rural women and motivates them to earn sustainable livelihoods

- Joint Liability Groups (JLGs) – These are semi-formal groups belonging to weaker sections of society. The bank lends to these groups to supplement its direct efforts of micro-lending.

Digital strategy

Making digital advancements is the top priority for ICICI. The bank wants to be at the forefront to accelerate digitisation, leveraging digital technology across all its business segments with the ICICI STACK. The prime focus of the ICICI is on enhancing and improving the customer experience. The ICICI STACK consists of:

- Digital First – Advanced analytics in the area of payments and products to satisfy the customer needs

- Future Ready – Providing reliable, seamless, and robust platforms for superior customer experiences

- Ecosystem Banking – Use of cutting-edge technology in partnerships with merchants and API banking to provide an open architecture platform

The bank takes digital initiatives:

- Video KYC – The bank launching the service has allowed customers to complete the KYC process through video interaction without having to visit a bank branch. Being the first in the industry, ICICI offers this service for opening salary accounts, availing of personal loans and credit cards.

- In December 2020, 41% of salary account customers and 46% of credit card customers were onboard using the service

- Digital onboarding is much higher than traditional channels when compared to 2019 and previous years

- iMobile Pay – ICICI allowed individuals who were not bank customers to connect their bank accounts with the mobile app to make payments and conduct business transactions. The app also gave them access to the entire range of services offered by the bank. In addition, the bank launched version 3.0 of the app in December 2020.

- The app saw an activation by 0.5 million non-ICICI bank customers in the initial two months of its launch, and more than three million non-ICICI users currently use the app.

- InstaBIZ – A new digital platform for SMEs and the self-employed segment of the economy. The platform offers more than 200 products and services over mobile and internet banking platforms.

- The platform currently has more than one million active customers and recorded 2.4x year-on-year growth in financial transactions when compared to the previous year

- Whatsapp Banking – The initiative provides uninterrupted customer service during the COVID-19 pandemic and allows retail customers to conduct many banking requirements from their homes during the lockdown.

- CorpConnect – The platform enabled corporate customers to integrate their Enterprise Resource Planning (ERP) system Application Programme Interfaces and host-to-host protocols.

- DigitalLite – The platform allowed for seamless and quick onboarding of customers. DigitalLite and CorpConnect allow corporate customers to manage their supply chain financing, payments, collections and reconciliation requirements of dealers and vendors.

- AI – Approximately 1,500 robotic automation processes were put in place to handle 700 workforce activities to enhance operational efficiency and improve the response time

- Ecosystem banking – The bank has a robust API ecosystem that integrates over 340 services within payments, collections, lending, cards, and connected banking.

- Includes over 150 fintech partners constituting 21 unicorns

- Supports over 40 different banking use cases

- Enables plug and play API ecosystem for merchant banking

During the FY2021, the bank also did the following:

- Issued 75% of all credit cards digitally to customers

- Focused on data analytics-led underwriting

- Digitised the mortgage and loan business

ICICI STACK

The initiative launched in March 2020 enabled banking on a digital platform for all types of customers, including governments bodies, institutions, district administrations, local bodies, and associated stakeholders. The platform is a significant enabler of digital adoption by customers. STACK is solution, persona and personalisation based.

As per the acronym, STACK comprises five layers, with each layer providing a different set of solutions to the customer.

STACK for retail customers:

- Start relationship instantly – This is the ‘account’ layer that consists of the bank’s iMobile App, Net banking, InstaSave, FDXtra and iWish Flexible platforms

- Transact digitally – ‘Payment layer’: IMPS, NEFT, RTGS, bill, payments, wallets

- Avail Insta Loans – ‘Loan layer’: credit cards, loans and PayLater

- Care for self and business – ‘Care layer’, various types of insurances offered by the bank, i.e., life insurance, health insurance, home insurance, motor insurance and more

- Keep growing – ‘Growth layer’: Operates in Systematic Investment Plans, Public Provident Fund, Fixed Deposit, Mutual Funds, and online trading

STACK for business banking customers:

- Start relationship instantly – Digital current account activation

- Transact digitally – Bulk payment through ‘eazypay’, API banking

- Avail Insta Loans – supply chain financing, purpose-based loans

- Care for self and business – Group health and GPA, employer-employee insurance

- Keep growing – Business networking alliances

Security strategy

The Board of the bank focuses on cyber security and data privacy as well as the scalability and resilience of its technology architecture. The bank believes that cyber security is not an IT security issue but a business issue. Therefore, ICICI follows a multi-dimensional approach to cyber security.

The CIA trio of ‘Confidentiality, Integrity and Availability’ is at the core of the information security framework implemented at ICICI. The bank follows a ‘defence in depth’ approach, enabling them to protect customer data using a multi-layered defence mechanism and a set of tools and techniques which complement each other. ICICI is the pioneer in allowing its customers to configure control parameters such as card withdrawal limits and international card access.

The bank adopted other measures to enhance its cyber security further:

- Every new application of infrastructure undergoes rigorous security testing

- Continuous scanning of IT infrastructure and application landscape helps identify potential issues

- Conducts cyber security drills and tabletop exercises to fine-tune the response mechanism

IT strategy

ICICI is continuously investing in building digital and technological competencies to deliver enhanced customer service and increase the productivity of the bank, all while optimising costs. In addition, the bank monitors and improves its technical capabilities and infrastructure to reduce disruptions in customer services.

The plan for 2021 and ahead is to be future-ready and work on the 2025 technology strategy. Under this strategy, ICICI creates an enterprise architecture framework across digital platforms, data and analytics, microservices-based architecture, cloud computing, and cognitive intelligence.

The three pillars of the architecture framework are:

- A resilient and flexible backbone – New-age, agile and flexible

- Deep understanding of customers – Customer profiling, understanding customer life cycle and ecosystems

- Delivering delightful customer experiences – Customised, digitised, and simplified products result in digital native engagement with customers

The 2025 technology strategy subsists of:

- Data platforms and analytics – Master data management system, enterprise data warehouse in cloud

- Engineering – Digital decoupling of core platforms

- Competency and skilling – Using AI, ML, data sciences, cloud, design thinking and agile methodology to upskill and improve the employees’ core competencies, all while improving their well-being

- Technology foundation – Automated processes along with service-mesh and event-based architecture

- Customer engagement – Reimagining the marketing technology platform, consolidation of loan origination systems, digital engagement hub and One Bank One CRM

- Productivity – Knowledge management and productivity and collaboration tools

ICT contracts

- Partnership with Visa for the ‘Visa in a Box’ programme to accelerate fintech innovations across digital issuance, prepaid use cases and lending

- Partnership with three FinTechs to launch co-branded prepaid cards – each in banking, business expense management and neo-bank

- Alliance with Greater Chennai Corporation (GCC) and Chennai Smart City (CSC) Limited to launch ‘Namma Chennai Smart Card’, a contactless prepaid card to facilitate tax, utility, retail, and e-commerce payments

8 Growth and innovation strategies

- #1 Cost to serve

The operating expenses for ICICI have marginally decreased by 0.2% from USD 2.952 billion in FY2020 to USD 2.945 billion in FY2021.

Under the operating expenses, the following segments experienced the following changes from FY2020 to FY2021:

- Personnel costs from USD 1.129 billion to USD 1.105 billion (2.2% decrease)

- Depreciation of property from USD 129.36 million to USD 146.43 million (13.2% increase)

- Administrative expenses remained constant at USD 1.69 billion

- Provision for non-performing assets from USD 1.2 billion to USD 1.47 billion (21.9% increase)

On the other hand, the operating profit for the bank witnessed a notable increase of 29.43% from USD 3.84 billion in FY2020 to USD 4.97 billion in FY2021. Income from the treasury business of the bank recorded an exponential growth of 290.3%, from USD 176.62 million in FY2020 to USD 689.28 million in FY2021. The contribution of net interest income to net income was USD 5.33 billion, whereas the contribution of non-interest income was USD 1.90 billion.

The bank is in a healthy position with constant operating expenses and increasing operating profits. The cost to income ratio witnessed a 14.5% decline, from 43.50% in FY2020 to 37.20% in FY2021. However, there are certain areas where the bank can focus on to reduce its operating expenses further and increase its operating revenue, thereby increasing its cost efficiency:

- The bank should focus on areas to generate complementary revenue streams through non-interest earnings. Currently, the interest earnings of the bank are 2.81 times the non-interest earnings.

- Reducing the provision for non-performing assets will further drive down the operating costs of the bank. Moreover, ICICI should have a more stringent credit profiling of its customers before extending loans to avoid default in repayments.

- The bank should replace repetitive person-hours with cognitive process automation at the administrative level to reduce the personnel cost associated with these tasks.

- ICICI should digitise more functions and processes requiring intense human intervention, such as cashiers and customer grievance redressals.

- #2 Transformation of the branch and its branch network

Towards the end of FY2021, ICICI physical network consisted of 5,266 branches, 14,136 ATMs, 2,713 cash deposit machines and 1,786 instant banking kiosks. Of the 5,266 branches, 51% are in rural and semi-rural areas, with 649 branches in previously unbanked villages. During the year, the bank added 922 cash deposit machines and 148 instant banking kiosks.

The bank also made additions worth USD 22.63 million to its infrastructure cost in FY2021. The repair and maintenance cost increased by USD 24.92 million, from USD 241.55 million in FY2020 to USD 266.47 million in FY2021, representing an increase of 10.32%. More than 90% of the bank’s transactions, consisting of financial and non-financial transactions, were conducted through digital channels.

Digital initiatives play an important role in driving growth and efficiency for the bank in the retail business, made apparent by its investment in technologies such as API banking portals and self-service kiosks. Due to these initiatives, the bank can service more customers through its existing branches and has enabled employees to offer more value-added services. ICICI can further improve its branch network by doing the following:

- Eliminating the branches with low footfall and replacing such branches with Interactive Teller Machines (ITMs) will help reduce the branch size and invest the freed-up capital in connecting villages that are currently unbanked

- Replace cash-deposit machines with ITMs to conduct more transactions than just cash deposits

- Install more self-service kiosks to reduce human interaction to conduct simple business transactions, and this will also help reduce the personnel cost for the bank

- The bank can consolidate branches in neighbouring areas which see low footfall into a specialised branch serving these regions

- #3 Customer experience

- Omnichannel experience – ICICI aims to improve its physical and digital touchpoints in the form of bank branches, ATMs, self-service kiosks and mobile and net banking, respectively, for a smooth and seamless customer experience proving the omnichannel experience beneficial for the bank.

- Personalised insights and recommendations – The bank should focus on understanding the behaviour patterns, needs, requirements and spending patterns of the customer to provide them with personalised products based on their specific needs and requirements.

- Customer analytics – Using Artificial Intelligence (AI) and Machine Learning (ML), the bank can give customers insight into their savings and spending patterns and provide recommendations to meet their individual financial goals.

- AI bot phone banking – The 90,000 calls the AI handles with customers can be used to analyse customer conversations to generate insight into the customers’ overall banking behaviour.

- Ecosystem change – Change the look and feel of its orange theme that has proven unappealing to current or potential customers.

- #4 Employee experience and productivity

- Along with multiple video and course modules, the bank has deployed several training and development programs to increase employee productivity and well-being. However, the bank should also focus on using technology to enhance the employee experience by focusing on:

- Building hybrid work models that encourage work from home and in-office flexibility, including onboarding and training

- Integrating ML and data analytics to augment and deliver relevant recommendations to employees for their career advancements

- Designing personalised employee programs to help each employee adopt and learn skills based on their specific roles

- Assisting employees with a clear career development path

- Incorporating rewards and benefits for employees that go beyond insurance, stock options, accommodation support and leases. Ideas include:

- Cross-departmental project work for lateral career advancements

- Pre-natal and child-bonding leave extensions with childcare assistance

- Employee counselling regarding grief and loss

- Periodical career breaks

- #5 Migration of workload to the cloud

ICICI bank is making investments in fast emerging technology such as cloud computing and data sciences coupled with customer preferences and are dynamically redefining risks and opportunities. The bank has launched CP Online, a first-of-its-kind cloud-based platform that integrates various stakeholders for the issuance of commercial paper. By automating and digitising the process, the program reduces the client’s workload by more than 80% and turnaround time is reduced from four days to less than a day. To improve its cloud capabilities, here are the potential steps:

- Apply advanced analytics, AI, and ML on customer data sets to create meaningful insights to identify various customer pain points

- Provide end-to-end protection for all the confidential data stored in the cloud, which will help the bank maintain customer trust and confidence

- Utilise cloud-based platforms for management and HR related tasks to increase operational efficiencies

- #6 Artificial Intelligence (AI) in everything

When hiring, the AI-based testing and selection platform adopted by ICICI helps determine the potential employee’s cognition, language ability, personality and emotional awareness. The platform is configured to administer adaptive testing with advanced features such as image recognition, text analytics, language checks, emotions and tone analytics, and security check systems. In addition, the bank can further integrate AI in its operations by:

- Implement AI to process data for fraud detection

- Utilise AI-based systems to conduct and manage daily tasks using virtual assistants and chatbots, which humans currently manage

- Use voice and facial recognition for identification purposes as a quick and secure means of security mechanism

- #7 Neo banking

ICICI is partnering with neobanks and has taken the lead in the segment by partnering with Instant Pay, which offers full-stack banking services to individuals and businesses of all sizes. It has also partnered with Open, a neobank offering service to SMEs and start-ups. Furthermore, the bank should continue extending its license and partnership with niche neobanks that serve gig-workers, daily farmers, villagers, street vendors, female workers and more.

- #8 Society and planet impact

The bank is fervent in reducing its carbon footprint, incorporating renewable energy and water management usage in its premises wherever feasible. To achieve its objective, the bank should focus on the following:

- Installing roof-top solar panels on office buildings wherever possible

- Using green products such as virtual cards, eco ink and pulper cards to reduce the direct impact on their operations on the environment

- Installing water-efficient faucets to reduce water consumption

- Making use of smart plugs and sockets to conserve energy

- Using more energy-efficient lighting solutions

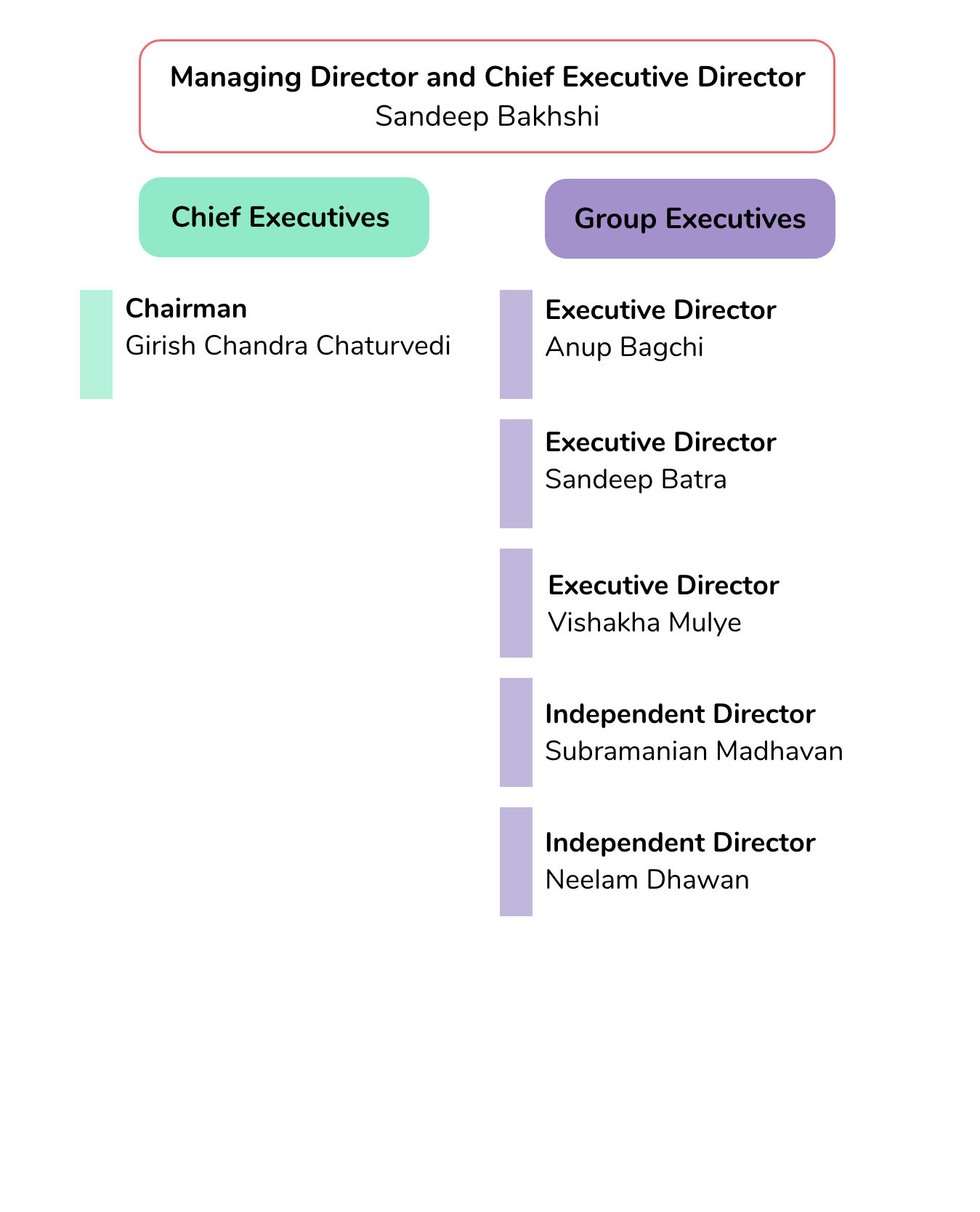

Organisation structure

Executive profile

Girish Chandra Chaturvedi

Chairman

Girish Chandra Chaturvedi is the Non-Executive (Part-time) Chairman of the bank. He is a retired IAS Officer from the 1977 batch from Uttar Pradesh. Concurrently, he is the Chairman of the National Stock Exchange (NSE). He completed his Master’s in Social Policy in Developing Countries from London School of Economics and Master’s in Physics from The University of Allahabad.

Quote

- Digital adoption, Annual Report 2021

Our continuing efforts to promote a cashless ecosystem and enable digital access to financial services proved invaluable. Our customer centric approach enabled us to respond to the needs of customers and launch digital alternatives for them to meet their financial needs.

Sandeep Bakhshi

Managing Director & CEO

Since October 15, 2018, Sandeep Bakhshi has been the Managing Director (MD) and Chief Executive Officer (CEO) of ICICI Bank. He previously served as a Wholetime Director and Chief Operating Officer (COO) of the bank. He completed his management studies from XLRI in Jamshedpur.

Anup Bagchi

Executive Director

Since February 1, 2017, Anup Bagchi has been an Executive Director on the Board of ICICI Bank, formerly holding the place of Managing Director and CEO of ICICI Securities Limited. He has a management degree from IIM, Bangalore, and an engineering degree from IIT, Kanpur. He holds the responsibility of Retail Banking at the bank.

Sandeep Batra

Executive Director

Sandeep Batra has been an Executive Director on the Board of ICICI since December 23, 2020. He serves as a Chartered Accountant (CA) and Company Secretary and is also responsible for the Corporate Centre at the bank. He previously held the position of Group Alliance Officer for ICICI.

Vishakha Mulye

Executive Director

Vishakha Mulye has been an Executive Director of ICICI Bank since January of 2016. She is a Chartered Accountant and is accountable for domestic and foreign Wholesale Banking Group, Markets Group, Proprietary Trading Group and Transaction Banking Group at the bank. She also chairs the Board of ICICI Bank Canada.

Subramanian Madhavan

Independent Director

Subramanian Madhavan is an Independent Director at ICICI Bank, a member of the Institute of Chartered Accountants of India, and possesses a Post Graduate Diploma in Business Management from IIM, Ahmedabad. Furthermore, he is a member of the Institute of Directors, the All-India Management Association and the Delhi Management Association.

Neelam Dhawan

Independent Director

Neelam Dhawan is an Independent Director at ICICI Bank. She is an Economics Graduate from St. Stephen’s College and has an MBA degree from the Faculty of Management Studies, University of Delhi.

Appendix A

twimbit purpose index

We, twimbit, evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In assessing the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Business Insider. Company News. Retrieved November 19, 2021, from

Entrepreneur India. Company News. Retrieved November 24, 2021, from

https://www.entrepreneur.com/article/332315

ICICI Bank, (2021, March 31). Annual Report 2020-21.

ICICI Bank, (2021, March 31). Environmental, Social and Governance Report 2020-21.

Livemint. Company News. Retrieved November 19, 2021, from

Moneycontrol. Company Financials. Retrieved November 12, 2021, from

https://www.moneycontrol.com/financials/icicibank/profit-lossVI/ICI02/1#ICI02

Moneycontrol. Company Overview. Retrieved November 12, 2021, from

https://www.moneycontrol.com/india/stockpricequote/banks-private-sector/icicibank/ICI02

Techcircle. Company News. Retrieved November 19, 2021, from

The Hindu Business Lines. Company News. Retrieved November 24, 2021, from

The Paypers. Company News. Retrieved November 19, 2021, from

https://thepaypers.com/online-mobile-banking/icici-bank-partners-busy-for-banking-solutions–1250417

Varindia. Company News. Retrieved November 19, 2021, from

https://www.varindia.com/news/icici-bank-partners-with-phonepe-to-issue-fastag