Smart branches redefine customer engagement value

Banking giants are reducing their physical footprint and growing their presence on digital channels, however this does not eradicate brick-and-mortar branches in the foreseeable future. The banks of tomorrow need two faces – physical and digital. Heavy investments into digital banking solutions, combined with the human touch, creates a potent phygital business model. Phygital model gives a competitive advantage to incumbents, as they can leverage the physical network to build trust and empathy with customers at the same time bring the convenience and speed to service customer needs. This creates an edge over new-age digital-only banks, bringing stiff competition and consolidation in the financial industry.

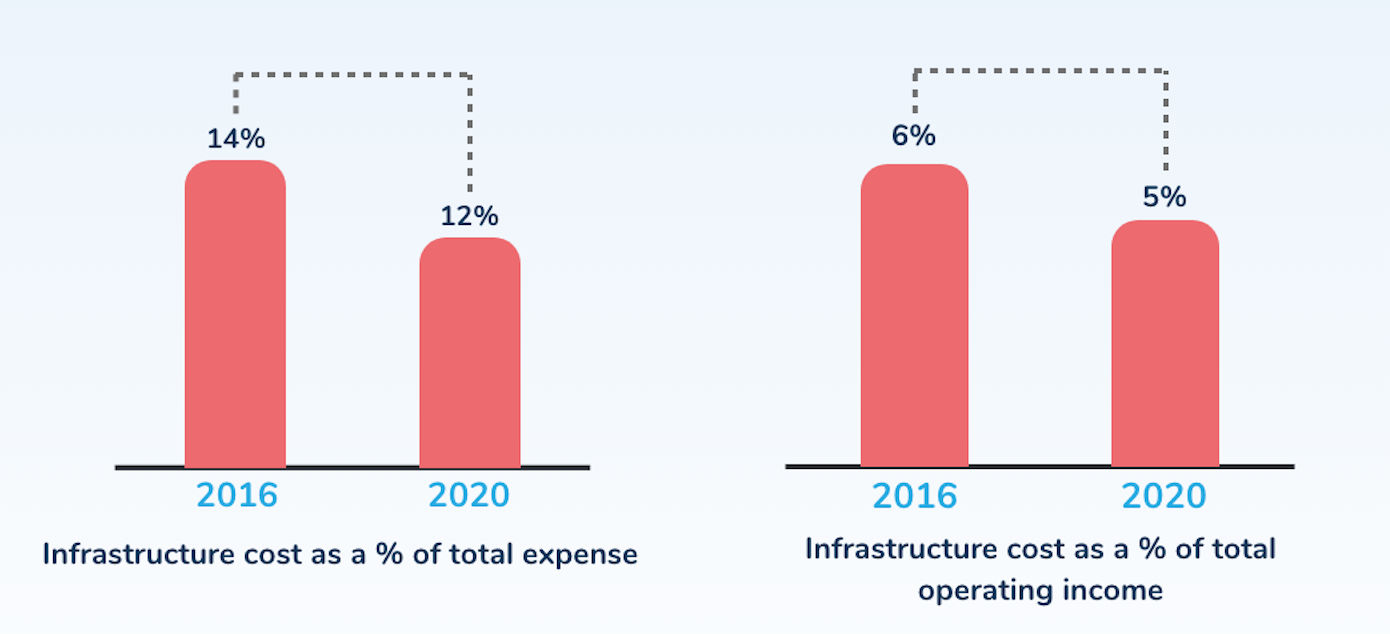

Figure 1: Infrastructure cost decline of top banks in APAC

twimbit analysed the infrastructure cost of banks (infrastructure cost includes rent, electricity and maintenance, and lease payments in the overall operating expense for the bank) and found that the percentage of infrastructure cost-to-total expense saw a considerable decline between FY16 and FY20 (Figure 1). Whereas, the infrastructure cost-to-total operating income also declined during the same period. The primary reason for the declining expenses is due to the decrease in the number of bank branches over time. However, branch facilities are still an important channel of business, especially for Asia-Pacific countries such as India, Japan, Australia, and Taiwan.

Markets like Japan are an indicator of the slow digitisation in bank branches

Japan has way too many bank branches for a relatively small country. There is a bank branch on every corner, which makes going to the bank to carry out daily transactions convenient. Since most users prefer to bank traditionally, Japanese banks are reluctant to change their operations for fear of losing their customers to “un-digital” competitors.

Digitisation of banking in Japan has been slow due to a number of reasons:

- Continued widespread use of cash (for as much as 80% of all transactions),

- Less than 20% of people using digital banking services to date, and

- Many shops in Japan not offering any other means of payment.

Instead of reducing the branch footprint, traditional banks are improving their branches to make them enticing with personalised help, alluring lobbies, and chic furniture to provide a better customer experience. There are, though, banks like Jibun bank, which targets Millennials. Jibun has no physical branches and is the first mobile-centric bank in Japan.

Pre-requisites for branch transformation initiatives

A branch transformation exercise has implications on people, processes and technology. The study revealed several initiatives that the banks adopted prior to their comprehensive branch transformation program. These include:

Up-skill branch talent to handle complex customer enquiries

Staff development is an important aspect of a bank’s digital transformation journey. As basic banking services are accessible digitally, banks should ensure that the personnel at the physical branches are prepared to provide support for more complex products and services. Frontline staff must also learn about empathetic human interaction, as this is now crucial for building customer loyalty.

HSBC continues to invest in their staff with the right training and tools to support customers wherever they choose to bank, whether in-person or online. The bank expanded its development programme for customer-facing employees, giving them coaching to develop the skills and confidence to resolve complex customer queries at the first point of contact, whenever possible. HSBC has now trained approximately 6,000 employees in seven markets—the UK, Hong Kong, Mexico, the US, Singapore, Indonesia, and Canada — in these new roles.

Training as digital ambassadors

To assist customers with the new digital channels and services, OCBC transformed many bank tellers into digital ambassadors. The bank continues to train its staff in new disciplines, such as design thinking, digital technology, data analytics, and artificial intelligence. All product managers are conversant with API management and customer experiential design. OCBC formed agile squads, comprising staff with a mix of expertise and domain knowledge, to onboard new products to the market in a limited time window.

Top 6 future branch models for success

- #1 Revamp bank branches into community hubs

Banks can retain the loyalty of customers by providing an exceptional customer experience. There is a need to adopt a more attractive branch model. Branch visits should go beyond processing transactions and clarifying queries to become a community hub where people can socialise, relax, and bank, all at the same time. The examples below show how banks can transform their branch experience to make branch visits appealing to their customers.

Virgin Money – Situated at a short distance from Piccadilly Circus is one of Virgin Money’s eight lounges, the Haymarket branch. The lounge leaves no doubt that it is a place for socialising. Its customers have access to the lounge, where they can watch TV while enjoying coffee. They could deposit or withdraw cash or access the full banking facilities available at this level. Descending to the lower ground floor, customers get to dive into Virgin’s aviation history. The level mimics an aircraft, complete with aircraft seats, overhead lockers, and floor lights. Customers can either position these seats towards a large screen or swivel them to face one another for informal meetings.

The area extends to a children’s playroom, equipped with interactive games to keep them entertained while parents bank. On top of this, the lounge is also available to the local communities for organising events, holding charity meetings, and conducting fundraising activities. Virgin Money lounges attract 68,000 people per month and have also helped the bank achieve a net promoter score of 85%.

While Virgin Money has kept its community hub separate from its bank branch, many banks are now converting their main branches into similar hubs.

Another example is Capital One, which opened new cafe branches that customers could use to connect with branch representatives or “cafe coaches” and get financial advice over a latte, aside from the general cafe experience.

Bendigo bank – The bank established four branches by transforming them from traditional branches to a community-centre-like environment. There is a wide range of features for customers, such as a free Retail Pop-Up Space, an indoor community space equipped with technology for community or business meetings, workshops or small events, and free WiFi.

DBS – Café + branch – DBS has built a lifestyle branch with an open layout for Millennials and Gen-Zs to bring them back into the bank branch. Novel 24/7 “café and branch” is situated at Plaza Singapura. The branch comes with many technological innovations to appease the tech-savvy generations, ranging from a ‘VR corner’ which gives customers a virtual experience towards their retirement plan to ‘Pepper’, the bank’s humanoid robot that gives customers on-the-spot guidance through the branch. Apart from this, the branch also features best-in-class ATMs. The customer experience starts with the aroma of freshly brewed coffee, right at the entrance.

- #2 Migrate over-the-counter services to digital self-service kiosks

Over-the-counter services is the primary reason for high cost and low efficiency for bank branches, as they involve manpower and customers standing in long queues. Banks can migrate services provided on the counter to digital service kiosks which lessens the need for human tellers to staff bank branches. Moreover, smart branch technologies allow for a personalised approach to sales along with 24/7 access to the bank branch. They also create an omni-channel user experience; customers get a seamless experience whether they are online, on an app, or at the branch.

The smart self-service kiosks should have the following technologies:

- Fully automated cash and coin handling,

- Non-cash transactions and sales through digital capabilities,

- Improved branch formats and design, and

- A digitally enabled customer ecosystem.

Next-generation ATMs

OCBC rolled out next-generation ATMs to 23 branches in 2019. These ATMs allow cash withdrawals of up to S$200,000 (USD 147,908), the selection of note denominations, and simultaneous note and coins deposits. By doing so, OCBC migrated 31% of over-the-counter services to the new ATMs. Other digital service kiosks help branch staff conduct high-demand services efficiently, such as overseas card activation and the updating of personal and account details.

Robot assistant

HSBC introduced ‘Pepper’, a robot in its flagship branch in Manhattan. The robot answers basic customer questions and guides them to the respective advisor. Therefore, it makes the branch visit seamless for the customer while not eradicating the need for human intervention.

In-Branch tablets

HLB introduced in-branch tablets throughout its branch network for improved customer efficiency. The tablet performs functions such as new account opening, product application, account management and data-enabled personalised offers. It also allows the customers to enjoy a no-queue experience and has reduced time spent by branch staff on operational duties. As of August 2020, HLB had deployed the tablets to over 150 branches.

Uniqlo – Harajuku store

Banks can learn from big retail giants which have completely transformed the retail experience for their customers. Take an example of the Uniqlo Harajuku speciality store, which incorporates the brand’s Style Hint outfit recommendation app into 240 touchscreens spread across the store. These displays allow customers to view and customise various outfits and locate these outfits in store. Banks can adopt a similar branch model by incorporating several touchscreens for various banking services and connecting the customer with a specialist if needed. A division of each banking service in a specified area, featuring touchscreens addressing that particular service. Customers can use these touchscreens to conduct their business and call up a specialist if they need further help. By dividing the services into a specified area and assigning specialists to deal with that service, banks can reduce the waiting time for customers and address their queries swiftly.

- #3 Establish a centre for digital banking education and financial advisory

Banks aim to shift most daily banking activities to digital channels. To facilitate this goal, banks should use their physical branches for educating customers on how to use these digital services conveniently and effectively.

For instance, UOB Singapore has deployed a team of 30 Digital Advocates at some of its branches to train customers on how to use the self-service kiosks at a bank branch along with its mobile app, UOB Mighty. This makes the digital process convenient and smoother for customers who may not be familiar with the technology. The bank has also deployed 14 Senior Digital Advocates to branches to teach senior citizens how to use other touch-points for their daily banking needs. These initiatives facilitated an increase in digital transactions, of which 96% of all transactions in Singapore are on digital platforms. Moreover, one in three bank accounts in Singapore is opened digitally, and two out of five customers prefer to use multiple banking touch-points.

As daily banking gets transferred to digital channels and self-service kiosks, banks can focus on utilising their branches for wealth management advisory. Banks can deploy artificial intelligence (AI) and advanced data analytics to provide the most suitable investment solutions.

UOB – The bank has gone through branch transformations in Thailand and Singapore. In the former, two-thirds of the branch space is for financial advisory, while the rest remains for over-the-counter services. In Singapore, UOB converted some of its high street branches into wealth-management advisory centres. These branches integrate digital and in-person financial advisory services to assist emerging affluent customers in making investment decisions confidently.

- #4 Expand physical footprint with smaller, fully self-serviced ‘robotic-branches’

While staffed flagship branches are necessary for high-traffic, high-visibility urban locations, banks can build fully self-serviced branches for greater physical footprint penetration at reduced costs. These branches have full banking services available via video conferencing. Banks can also eliminate branches with low footfall and consolidate them into one specialised branch serving a wider geographic region.

Trader Joe’s – Trader Joe’s is well-known for being small, organised, and friendly. The brand’s stores are so tiny that two stores could easily fit within a regular grocery store’s space. The objective is to give customers a feel of their neighbourhood shops. Banks can adopt this model and reduce the size of their branches in areas with less footfall, while also reducing operational costs.

Drivers of change in this area are:

Bank of America – The bank introduced three fully automated branches to reduce costs while providing customers with simple and intuitive technology. While customers can perform everyday banking tasks on their own, they can make a video call to an advisory to seek support for more complex tasks. These branches allow customers to have one-on-one conversations to get a mortgage, plan for retirement, open a small business, or get a car loan.

DBS Bank plans to transform one-third of its branches into self-service spaces by 2022. This is because data released by the bank suggests that digital customers generate twice as much revenue as traditional customers. Moreover, the bank’s cost-to-income ratio for the digital segment was 33% in FY2019, 20 percentage points lower compared to the traditional segment’s cost-to-income ratio of 53%.

- #5 Bank while travelling

It is sometimes difficult for customers to visit their bank branches to conduct banking activities due to lack of time. To overcome this obstacle, banks can bring their branches to the customer, allowing them to conduct their banking activities on the move – while going to work or coming back home, and not take time out of their busy calendars to visit the branch.

Poland’s Idea Bank established their first bank branch on rail tracks along three routes of PKP Intercity trains. Trains running along these routes have a special carriage attached to them. These carriages are for office work and have all the essentials required, including tables, chairs, and a presentation screen. Travellers also have access to printers and scanners. The facility is available for all passengers boarding the train, but priority is for Idea Bank customers. Passengers can also enjoy a cup of coffee while reading the newspaper delivered to the coaches. The idea behind the creation of banks on rail tracks is to support small businesses by providing them with a space to work while they commute.

- #6 Transform heritage branches into museums

SBI – Chandni Chowk Branch – Begum Samru’s kothi

The Chandni Chowk branch is the oldest branch of The State Bank of India. Set up in 1806, it was declared a heritage building in 2002. The building has European architectural features, including arched doorways, spiral iron staircases, and vintage English lifts. The building is home to a mini-museum in the reception area, which highlights significant and unknown facts about the building. Other banks with heritage or significant branches can also take this approach of converting part of their historic branch into a museum, showcasing the history of the area while also conducting day-to-day banking activities.

Conclusion

While the traditional branches may become irrelevant, the need for a physical banking infrastructure prevails. The goal of futuristic bank branches should be to match the preferences of the local markets served with the right mix of digital and personal interactions. Branches can emulate similar experiences that mobile and web apps give to the customers and translate them into an omni-channel banking platform.

Branches of tomorrow can:

- Migrate services to digital channels as more and more people are using digital channels

- Provide self-service kiosks and touch-points as many customers are open to self-service for resolving issues, etc.

- Ramp up the digital sales and marketing network to avoid the defection of customers to competitors for other banking products

- Restructure the bank branches to have dedicated areas for customer advisory, self-servicing, and community

- Raise employee skills to elevate them from mere position holders to broad relationship coaches

Endnotes:

Bain & Company. News. Retrieved October 30, 2021, from

https://www.bain.com/insights/reimagining-the-digital-branch-of-the-future-lets-get-practical/

CookingLight. News. Retrieved February 17, 2022, from

https://www.cookinglight.com/news/trader-joes-stores-size

Finextra. News. Retrieved October 27, 2021, from

McKinsey & Company. News. Retrieved October 29, 2021, from

Mormedi. News. Retrieved November 3, 2021, from

https://www.mormedi.com/en/banking-digitalisation-in-japan-the-time-is-now/

Navrang India. News. Retrieved February 17, 2022, from

https://navrangindia.blogspot.com/2019/10/begum-sambrus-kothi-state-bank-of-india.html

SPGlobal. Company News. Retrieved February 24, 2022, from

Strands Blog. News. Retrieved October 27, 2021, from

https://blog.strands.com/digital-banking-in-japan

World Bank. Bank data. Retrieved November 3, 2021, from

https://data.worldbank.org/indicator/FB.CBK.BRCH.P5?end=2020&start=2016