2021 was a strong comeback year for the telcos across the Asia Pacific, with the industry experiencing an all-time high growth in the last 5 years.

Most Asian telcos continued their growth story, reporting better connectivity and device revenues. Launch of 5G and a general decline in price competition positively impacted telco performance. In addition, we are noting a sense of urgency among telcos to establish growth from enterprise and other adjacencies.

This report dives deeper into the trends mentioned above. We also uncover critical innovation opportunities for telcos based on our research on industry best practices and leaders.

Our methodology

We closely followed 40 APAC service providers and captured their financial performance related to:

- Revenue,

- EBITDA (earnings before interest, tax, depreciation and amortisation),

- CAPEX (capital expenditure),

- ARPU (average revenue per user).

We then developed a perspective on industry trends through company reports such as annual reports, analyst presentations, press releases, blogs and our discussions with telco leaders.

Figure 1: State of APAC telcos 2021

Key highlights from 2021

#1. Industry revenue grew 6.4% YoY in 2021 compared to 1.7% the previous year

Telcos in the APAC region have seen slow growth in the last five years. Intense price competition, attractive pricing for data plans and the proliferation of unlimited data plans has resulted in declining per GB data yields, constantly pressurising operators to manage costs.

Overall, 2021 has served as a revival for many Asian telcos, with operators in key Southeast Asian geographies such as Indonesia, Thailand, and Singapore posting revenue growth.

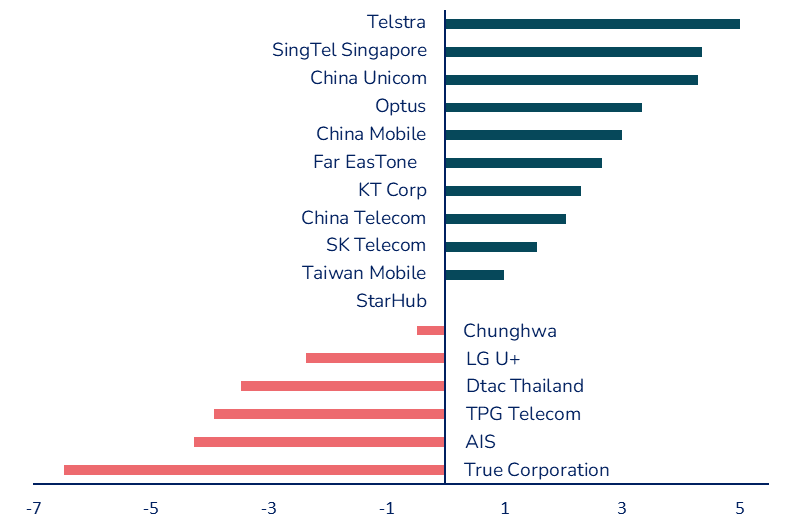

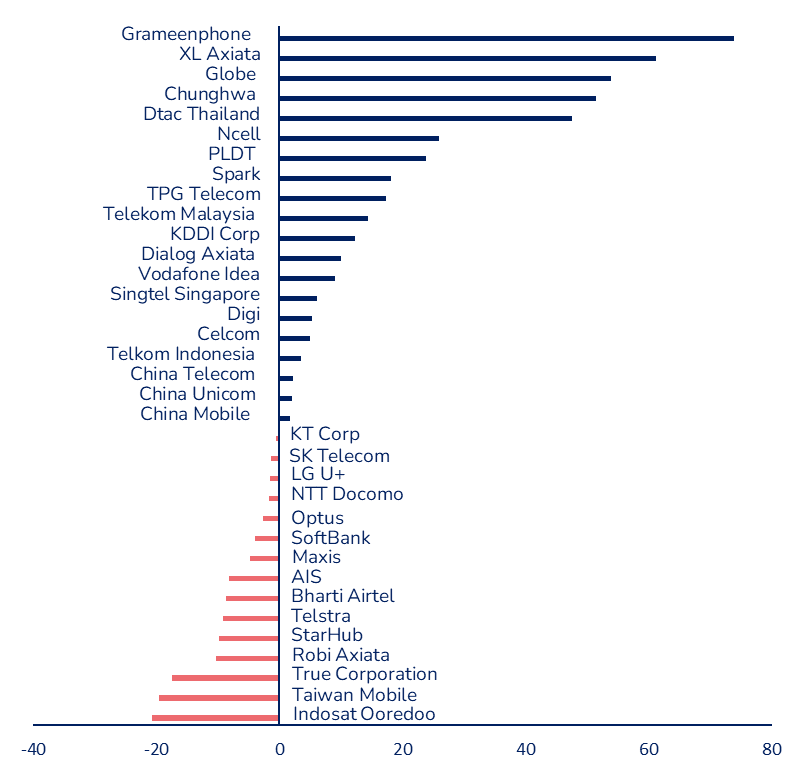

Figure 2: Mobile ARPU change (%) for APAC telco operators, 2021

Data pricing is improving in markets like India and Indonesia.

- India: Bharti Airtel and Vodafone Idea increased tariffs for pre-paid plans by 20-25%.

- Indonesia: Top 3 telos withdrawn from supplying unlimited data plans.

We expect an upward revision of pricing for data plans. In China, ARPU continues moving upwards thanks to the uptake of 5G.

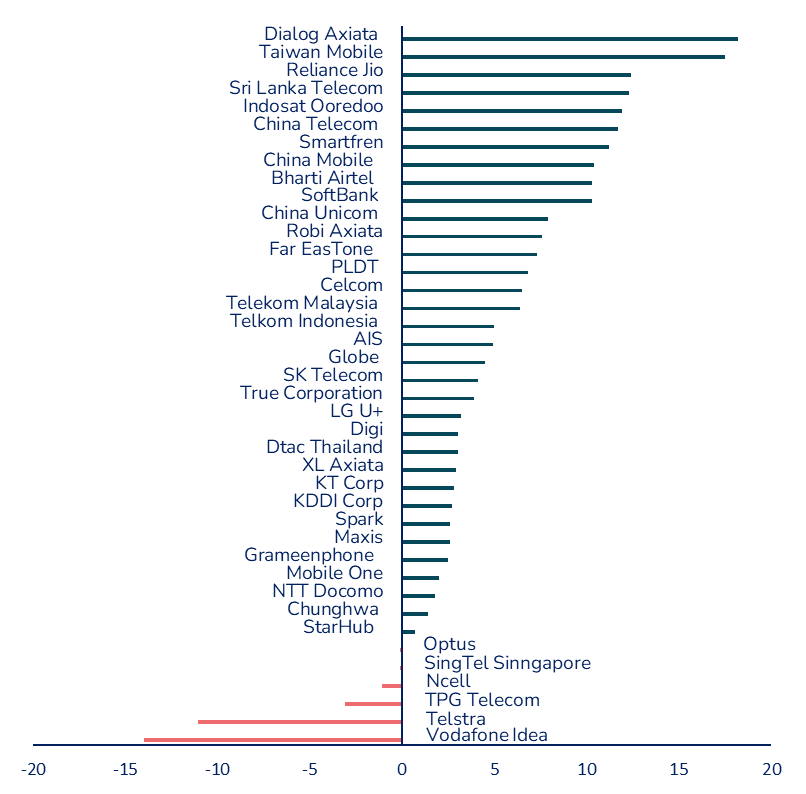

Figure 3: Revenue change (%) for APAC telcos, 2021

Telkom Indonesia: Based on 9 months of data

#2. Enterprise business and adjacencies drive new revenue growth

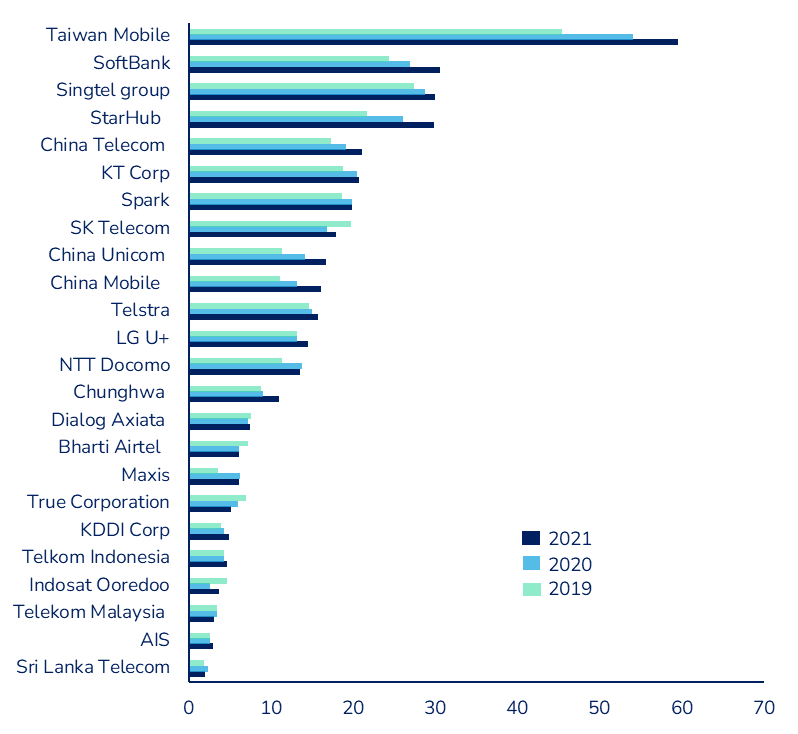

Compared to the total revenue growth, the non-connectivity segment shined with a YoY revenue change of 20.7% during 2021. Taiwan Mobile, Singtel, Starhub, SK Telecom, and China Telecom are operators recording strong growth in non-connectivity revenues.

Figure 4: Percentage of non-connectivity revenues to total revenues, 2019-2021

Telkom Indonesia: Based on 9 months of data

Singtel group: Based on 6 months of data

We recognise an urgency among telcos to shift focus towards faster-growing segments. Operators are taking multiple routes to address this:

Organising for successful digital business:

SK Telecom announced a new organisational structure separating its traditional and growth businesses, rebranding to call itself an “AI & Digital Infrastructure Service” company.

Co-building a digital ecosystem with partners:

Telkom Indonesia is accelerating its digital journey by investing and creating synergies with digital companies. An example is its investments in Gojek to integrate its digital services better.

- Integrating Telkomsel MyAds with GoBiz.

- Onboarding for Gojek MSME partners with Telkomsels DigiPOS Aja!

- Co-marketing for gaming services through Telkomsel’s Dunia Games and GoPay collaborating with Tencent.

In 2021, Telkom invested an additional USD 300 million in Gojek. Softbank and Alibaba are among the leading investors in Gojek. Following this, Gojek merged with Tokopedia to form GoTo.

Brand refresh to capture new growth areas

An example here is Singtel’s NCS business. Most incumbent telcos with a more defined B2Bbusiness need to align their go-to-market messaging to capture new growth areas. The brand refresh campaign should address two key challenges:

- New growth opportunities emerging with enterprise digital transformation,

- Initiatives to expand customer segments and geographic presence.

For NCS, this transformation meant co-developing 5G enabled solutions for enterprises in collaboration with Singtel. It is also expected to facilitate NCS’ expansion outside the home market.

#3. Collaboration efforts helped drive profitable growth

Collaboration in CAPEX spending:

Malaysia’s decision to opt for a single wholesale network provider aims to lower the cost of 5G rollouts. All significant operators can lease wholesale infrastructure from DNB (Digital Nasional Berhad), aspiring to lower 5G costs by at least 50%

Another example is the South Korean operators; SK Telecom, LG U+, and KT collaborating to rollout 5G services in rural areas of the country.

Improving costs through scale:

APAC is a tough market for operators despite the growth trends noted across key geographies. 2021 noted some major consolidations through mergers and acquisitions. For example, Indosat Ooredoo and 3 Indonesia merged to become Indosat Ooredoo Hutchison, the second-largest telco in Indonesia. The key highlights from the merger are:

- OPEX savings: Utilising complementary networks by decommissioning duplicate sites and optimising other duplicated infrastructure.

- CAPEX savings: More efficient use of combined spectrum resources and increased scale to enhance CAPEX savings.

- Non-network savings: Increasing efficiency in sales, marketing & distribution. Creating opportunities for additional savings in spending related to providers & partners

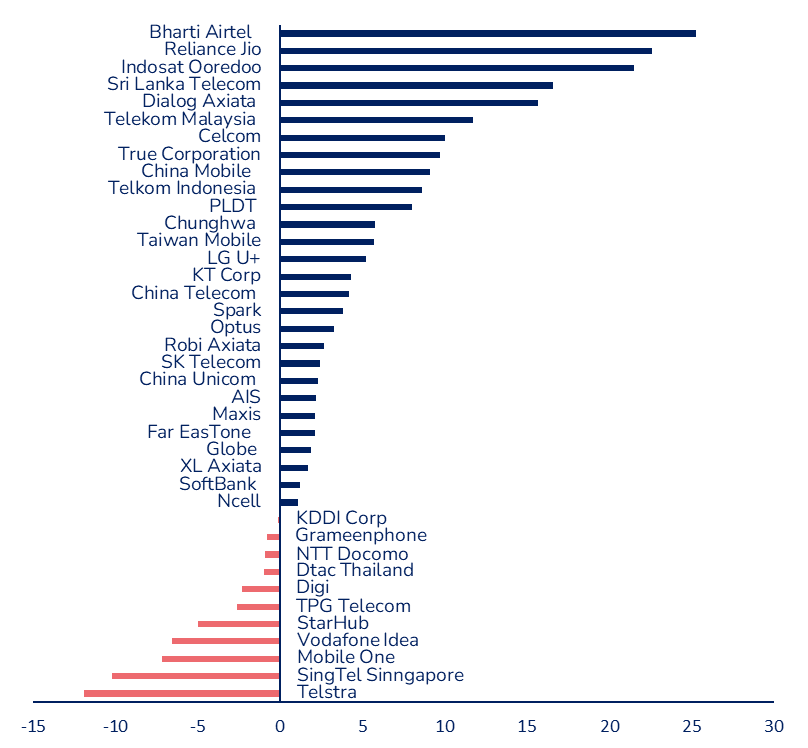

Figure 5: CAPEX change (%) for APAC telcos, 2021

Singtel Singapore and Optus: Based on 9 months of data

Innovation opportunities for Asian telcos in 2022

#1 Leapfrog with customer experience

Delivering exceptional customer experience has remained a challenge for telecom operators. Today’s customers are digitally savvy and more open to technology. Also, the high service expectations set by digital natives such as Netflix, Spotify, Uber, and Amazon, are adding to telco woes. Industry leaders recognise the urgency in investing and transforming customer experiences. twimbit’s recently concluded study, Telco CX Leaders 2022, emphasises an industry-wide shift towards orchestrating customer experience rather than delivering standard products. Some leading telcos are demonstrating excellent progress in 4 ways of producing and differentiating customer experience;

- Digital experience

- Service experience

- Employee experience

- Brand experience.

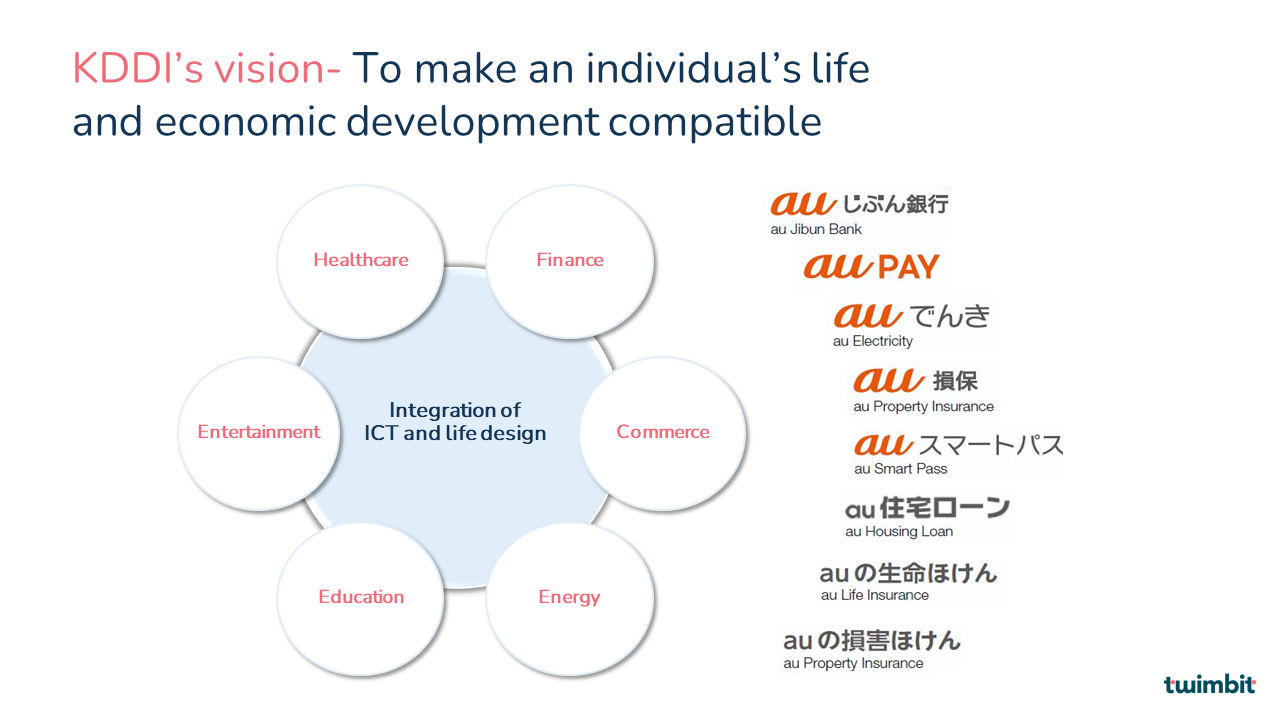

KDDI’s au life design is an excellent example of integrating big tech to deliver a personalised digital experience to customers.

au strengthens its point of contact with customers by using big data to find entry points into the lifestyle needs of users.

By integrating services such as hailing taxis and making restaurant reservations, ‘au PAY’ is the super-app that will be the launchpad for the daily life activities of customers.

#2 Participate and capture growth from applications & ecosystems

Fundamentally telco business is encapsulated into 4 layers. Their core business consists of:

- Infrastructure and connectivity,

- Application and solutions,

- Services.

The core business is evolving fast with new opportunities in mobile edge computing, SD-WAN, private networks, etc. However, applications and solutions hold a larger share of the pie.

Our study shows operators in the Asia Pacific generate an average 17% of revenues from non-connectivity businesses in 2021. However, there are few exceptions, notably from Japan, South Korea, and Taiwan, where operators have built significant revenues from adjacencies.

Ecosystems are an important part of telcos beyond connectivity strategies. Their approach is two-pronged as they build their ecosystems and partnerships in other ecosystems.

SoftBank seeks to expand business fields outside telecommunication with its’ Beyond Carrier’ strategy

Its decision to merge Yahoo Japan and Line is a good example. Blending e-commerce, communication and financial services ensure an all-in-one experience.

- SoftBank has created an ecosystem where a user does not feel the need to switch to any other platform.

- PayPay, SoftBank’s financial services platform, enables smooth transactions for users. Additionally, it has the highest share in Japan’s QR and barcode payment market

#3 Reduce operating expenses and cost to serve with automation

Most of the APAC region telcos reported strong EBITDA improvements during 2021. While we believe revenue was the top driver, operators need to focus on operating expenses to improve margins further since this aspect is vital with 5G. Operators are adopting for multiple strategies to rationalise 5G CAPEX spending. However, they will soon have to extend their efforts to improve operating expenses. New digital technologies and automation are helping operators at managing costs better.

Spark New Zealand has retained its focus on costs to strengthen its overall performance. In fiscal year (FY) 2017, Spark New Zealand set an objective to become the country’s most cost-efficient operator by FY 2020. Its journey highlighted three critical areas for cost transformations:

- Automation: achieved efficiency gains through lower administration;

- Higher sales productivity through better tools,

- and improved provisioning times through automated processes.

- Simplification: reduced service plans and portfolio;

- Converted 270 mobile products to 20 and 500 managed data variants to less than 200.

- Adopted a tiered service model to align costs more closely with the price.

- Limiting duplication: identified overlap between market-facing & operational teams;

- Reduced copper costs as 20%-25% of consumers of copper broadband shifted to wireless broadband.

- Adopted the most cost-effective technologies to deliver connectivity.

Spark executed its strategies and became the lowest cost operator. From FY 2017-20, Spark achieved a USD 228 million gross cost reduction.

Figure 6: EBITDA change (%) for APAC telcos, 2021

Telkom Indonesia: Based on 9 months of data

#4 Drive high-speed broadband access beyond urban centres

High-speed broadband availability is still limited in Asia. According to industry estimates, fixed broadband penetration across Southeast Asia is as low as 35%. This leaves significant headroom for telcos to grow connectivity business. The accelerated demand for fixed broadband technologies during covid serves as a proof point. Addressing the widening digital divide is the number one priority for many governments. However, these initiatives will have to be carefully crafted to address pricing challenges.