This report outlines the financial performance of the leading network equipment providers (NEPs) globally. Here, we have evaluated and summarised the performance of 6 large NEPs for the year ending 2021:

- Nokia

- Ericsson

- Huawei

- ZTE

- Samsung

- Cisco

This analysis will help us to understand the impact of changing local and global dynamics, including COVID restrictions, supply chain disruptions, and geopolitical issues, on the performance of NEPs. We also try to focus on the future outlook of these companies as they tap into new opportunities and expand their R&D investments.

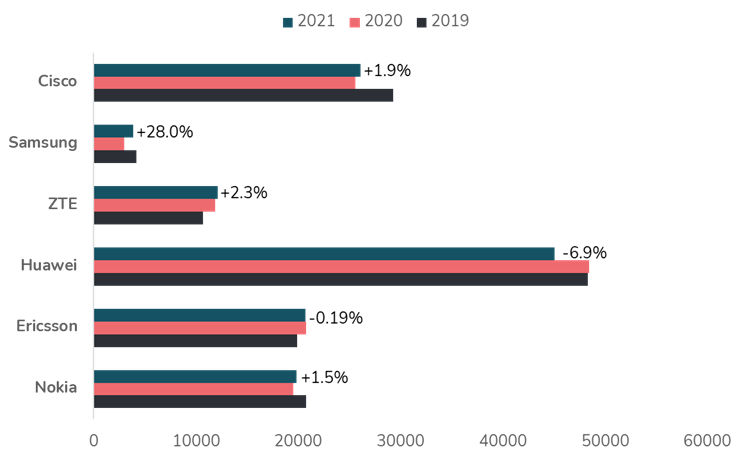

#1 Aggregate spending on networking equipment fell 1.2% YoY in 2021

hart 2: Increase in revenue in 2021 (YoY)

Globally, telecom operators and enterprises spent US$127.6 billion in 2021 on buying network equipment and related services from the six largest NEPs tracked in our report. However, their aggregate revenue for these NEPs fell by approx. 1.2% YoY in 2021, compared to a 2.9 % YoY decrease in the previous year. In addition, Huawei experienced a decline of US$2.4 billion in revenues that did not translate into others winning substantial business opportunities.

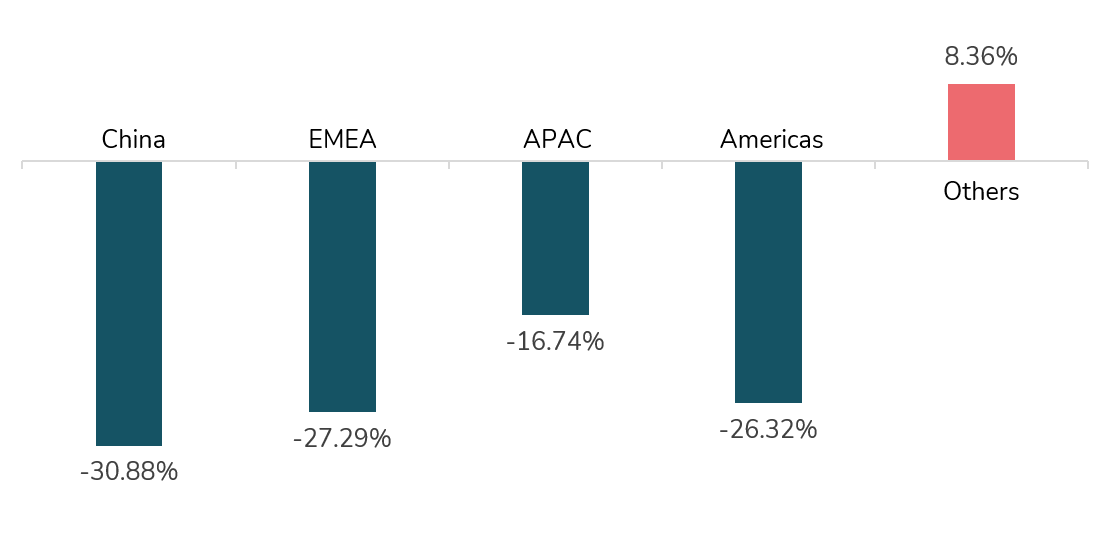

#2 5G rollout slowdown in China and geopolitical developments impacted revenue growth of vendors in China

- China Telecom plans to reduce the 5G investment by 10.5% as the operator intends to stabilise the CAPEX spend over the next few years.

- The budget for China Mobile on 5G networks decreased by 3.5% and is forecasted to reduce further in the coming years.

- Many Western countries and a few countries in Asia have left Huawei and ZTE out of the 5G infrastructure deals over security concerns.

Huawei experienced a decline across all its business segments in 2021. The single largest decline was in China. The total decline in revenues is US$40.7 billion. Network equipment in the same period declined by US$2.4 billion.

#3 Vendors have focused on strengthening solutions for enterprises with vertical industry propositions

- ZTE government and corporate business grew 16% y-o-y, compared to 2% growth in the carriers segment. Energy, transport, government, finance, the Internet, and major corporation sectors were the key drivers of growth. ZTE government and corporate business segment saw growth for their servers and storage products across all the leading sectors.

- The acquisition of Cradlepoint at the end of 2020 helped Ericsson improve its financials in 2021. Investment is key to Ericsson’s ongoing strategy of capturing market share in the rapidly expanding 5G enterprise space.

- Cisco acquired Replex GmbH, a privately held enterprise software company based in Germany, in 2021. This acquisition would help Cisco expand product capabilities to provide an enterprise-scale, cloud-native solution.

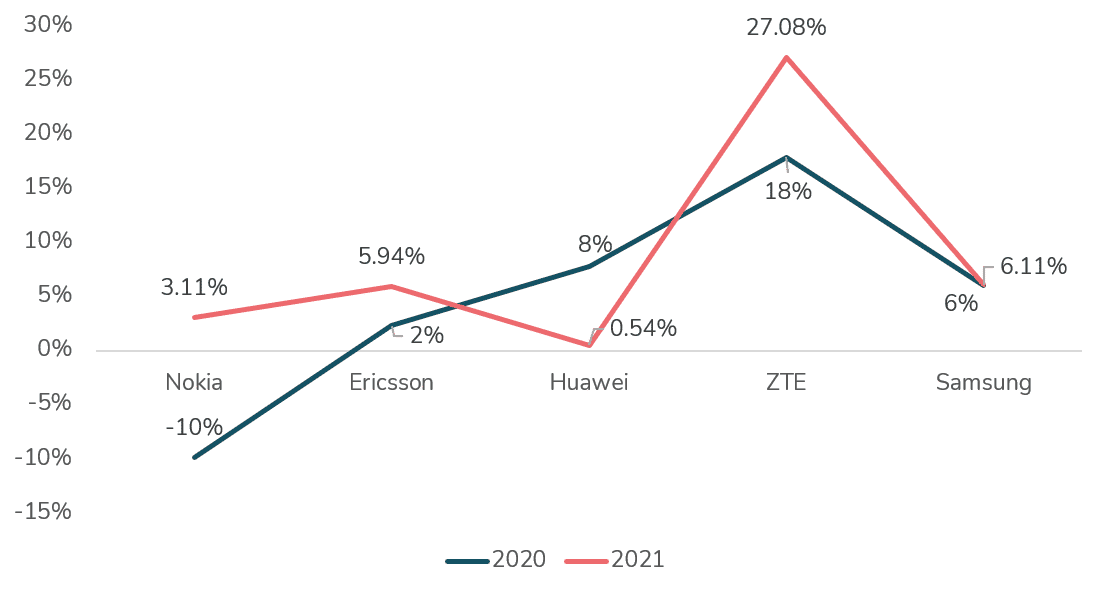

#4 R&D spend accelerated for 5G product roadmaps

Chart 2: Increase in R&D (YoY)

- Mobile networks research and development expenses for Nokia increased by 10% y-o-y, reflecting higher investments in 5G R&D to accelerate product roadmaps and cost competitiveness.

- In 2021, Nokia launched a new 5G portfolio powered by the latest ReefShark system-on-chip technology.

- Ericsson R&D expenses increased in networks and digital services due to increased investments in the segments’ 5G portfolios.

- Samsung has constantly been increasing its investment in R&D to gain a competitive edge. The R&D investments in 2021 helped them in:

- Developing MMU Beam Forming SoC (Feb 2021) – System on Chip (SoC) is 30% more power-efficient than the previous model.

- Developing 5 types of ORAN* RU for the US (Sep 2021), two types of 700/850 4T4R 40W, two types of 320W, C-band 8T8R 320W.

#5 NEPs to continue their focus on strengthening in-house capabilities and expansion of the enterprise segment in 2022

- Samsung is strengthening its technological competitiveness, including its core 5G chip.

- ZTE is increasing investment in core technologies (chips, its algorithm, and the network architecture.) and accelerating digital transformation across various industries to develop new opportunities in the government and corporate market.

- Nokia is capitalising on its renewed mobile network portfolio to gain RAN market share.

- Ericsson is leveraging the acquisition of Vonage to further expand its presence in the enterprise segment.

- Cisco is acquiring Opsani to strengthen and expand its capabilities to serve enterprises and cloud-native environments.

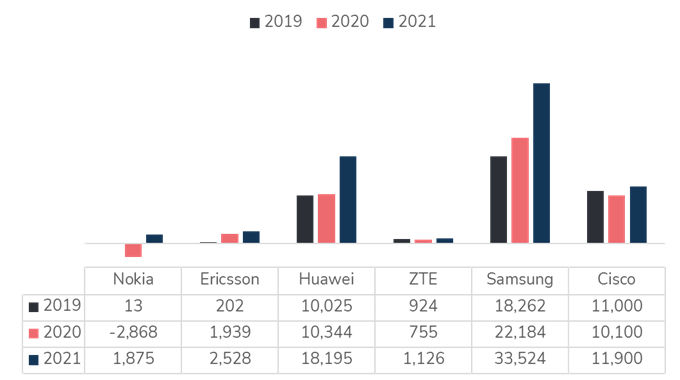

#6 Profitability for the vendors improved in 2021

Ericsson:

Ericsson’s profits have been steadily growing in the last few years, as the Swedish equipment maker improves its presence in the 5G rollout across North America as well as Europe and Latin America.

The growth in profit in 2021 has slowed down to 30% as compared to an increase in profit of more than 800% in 2020, as the company took a major hit in the Chinese market.

Ericsson’s future outlook to expand its presence in the wireless enterprise segment and broaden its global offerings has led to the largest acquisition in Ericsson’s recent history. The company announced the acquisition of US-based Vonage, a specialist in cloud-based communications solutions in November 2021 for $6.2 billion.

Nokia:

The company saw an impact of more than $4 billion in its bottom line in the year 2021. This was primarily due to lower income tax expenses and increasing operating margin. The operating margin was at 9.7% as compared to 4% in 2020.

This was a transformational year for Nokia after it completed the company-wide restructuring and investments in R&D to have more competitive products.

Huawei:

Despite substantial revenue decreases across its company, Huawei Technologies Co.’s net profit increased by 76 percent in 2021, showing efforts to cut costs and rely on local components to survive the blow from American sanctions.

ZTE

ZTE profits increased by 49% in 2021, despite the challenges faced by the Chinese equipment maker in the global market. The growth in profits was attributed to its growth in revenues across all business segments (carrier network, consumer business govt and corporate business). ZTE was heavily involved in the construction of 5G networks in China and continued to optimise its products and market structure in other countries in order to maintain strong growth in its operator business.

Samsung:

Samsung increased its profits by more than 50% in 2021, owing to the increase in operating profits from its chips business (which contributed 64% to the overall operating profit for the company) and the mobile business (despite the chip shortage). Samsung Network’s business revenue grew both in the domestic and international markets, and the company plans to expand its presence in Europe and other global markets while focussing on the 5G network expansion in South Korea.

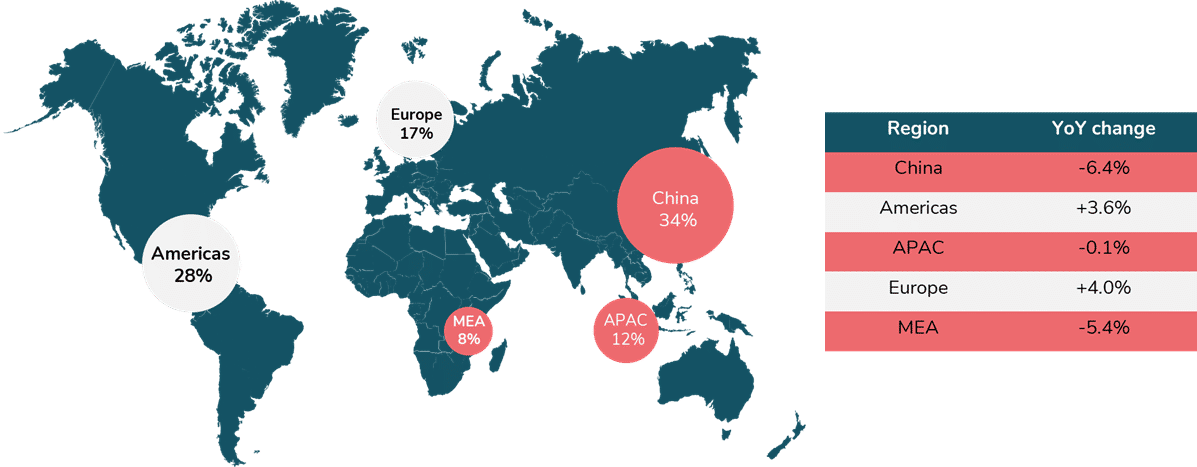

#7 Regional analysis

- Investments in 5G reached their peak in 2021, as operators co-developed the 5G network rollouts in China to lower the cost. Huawei and ZTE benefited from this as the other top equipment manufacturers took a major hit in the Chinese market.

- Nokia, Ericsson, and Cisco focused on expansion in the Americas, as the sanctions against the Chinese vendors gave them new opportunities.

- Nokia, saw maximum growth of 14% in Latin America in 2021, as sales of IP networks and Optical networks improved.

- Ericsson saw growth of 5% in the North American market and 19% in Latin America. Sales in both Networks and Digital Services continued to grow as a result of market share gains.

- Europe becomes a competitive region as the vendors improve their product capabilities and want to expand their presence.