Digitalisation in banking is unlocking multi-fold opportunities, enabling banks to identify new ways to generate value and better serve their customers. They are adopting a transformative approach from product centricity to customer-centric journeys. Revenue streams go beyond the traditional product mix and come from attached value-added services that support end-to-end customer lifecycle.

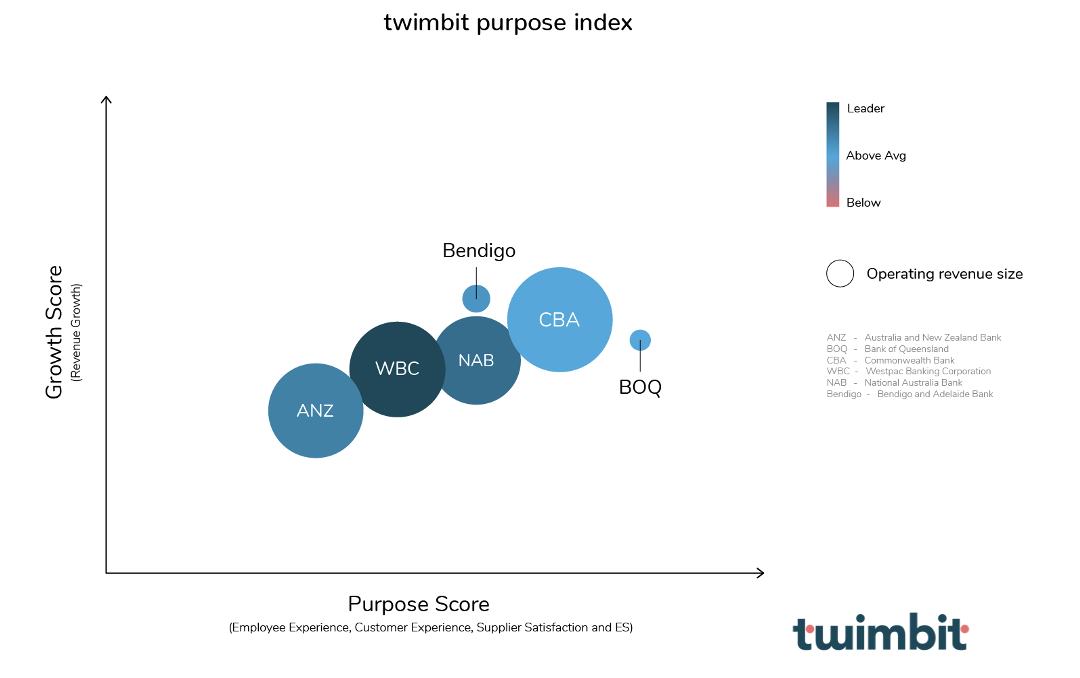

We analysed the top 6 Australian banks on the twimbit Purpose Index (Figure 1). For this report, we deep-dived into the big 4 Australian banks. Our analysis includes growth opportunities across five key areas that the banks need to focus on for future success.

- Redefining home lending experiences

- Reimagining business lending processes

- Winning the market with a digital-first propositions

- Reducing the IT complexity

- Maximizing value with data analytics

twimbit Purpose Index: Key takeaways

- Australian banks generally operate at a high-cost efficiency ratio when compared to banks in other APAC regions.

- The banks have been plagued by remediation expenses which contribute towards their high operational efficiencies.

- Banks are reducing their branch network and aim to reduce their cost base below USD 5.7 billion.

- Investments have shifted from infrastructure to growth and simplification for an enhanced customer experience.

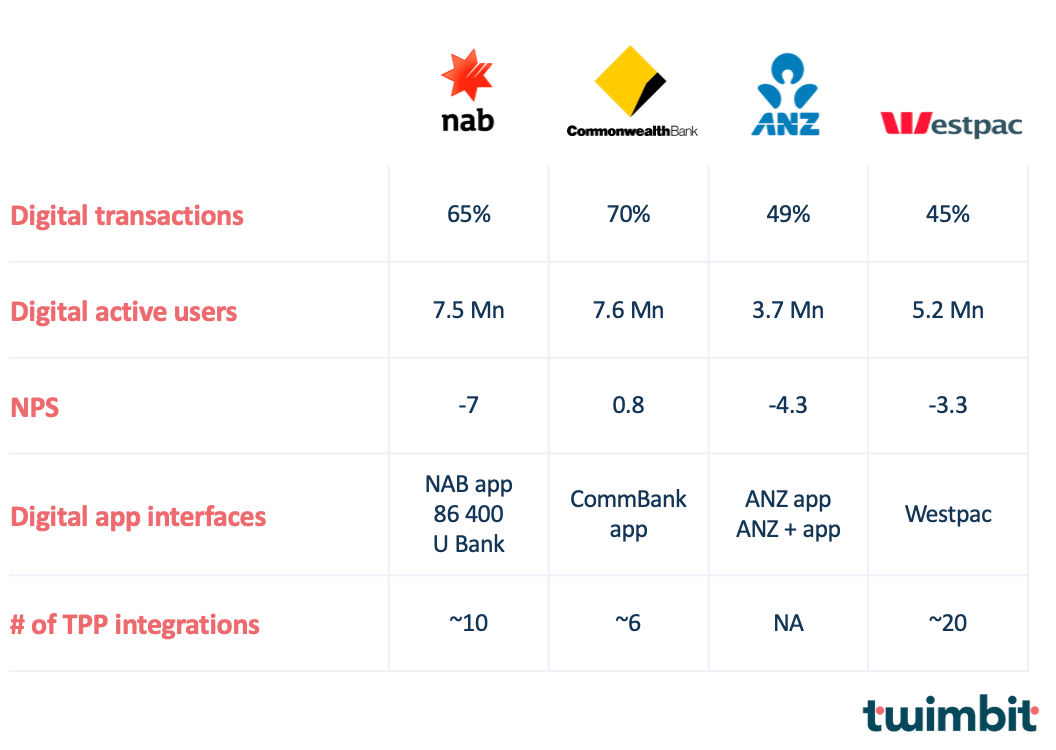

- CBA and NAB are leaders in digital transactions, whereas ANZ and Westpac are still far behind with low digital transaction proportions and a much lower active digital customer base.

5 growth opportunities for the big 4 Australian banks

After conducting our analysis of the Big Four Australian banks, we were able to come up with the following five growth opportunities:

- #1 – Redefining home lending experiences

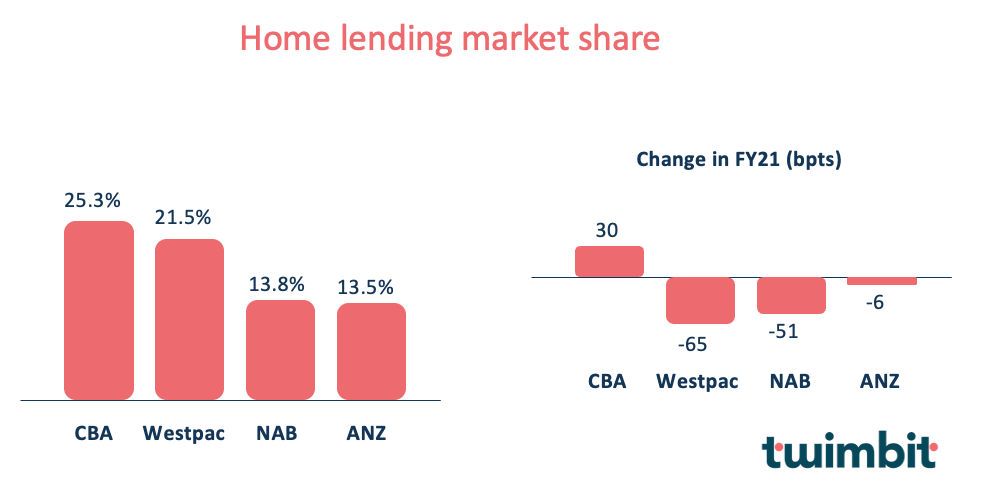

Home lending is one of the biggest revenue generating segments for Australian banks. CBA has the highest market share in home lending, closely followed by Westpac (Figure 2). All banks except CBA occurred a loss in their market share compared to FY20, with Westpac taking the biggest hit (Figure 2). The Australian banks are facing challenges in the form of low-interest rates and tightening lending requirements. The net interest margins are constantly declining and have reduced at an average of 1.56% between FY17 and FY21 and are likely to remain under pressure due to the central bank holding its cash rate at 0.1%.

The Reserve Bank of Australia is on its way to implement more stringent capital adequacy requirements from 2023 and will increase the cash rate for the first time in more than ten years. CBA and ANZ predict that this change will lead to a 10% fall in property prices by 2023 which will have a significant impact on the housing lending market.

Therefore, it becomes extremely critical for the banks to create opportunities by orchestrating home lending experiences. The banks need to customize the product suite per the customer needs and segments. They can focus on the following opportunities to scale their business:

- Journey led mapping for specific customer segments

- Professionals

- Farmers

- Young executives

- Home-makers

- HNI

- Integrations with real-estate marketplaces

- Personalised insights on loan modifications, price readjustments, and benefits management

- Carbon footprint measurement tools for retail customers

- #2 – Reimagining business lending processes

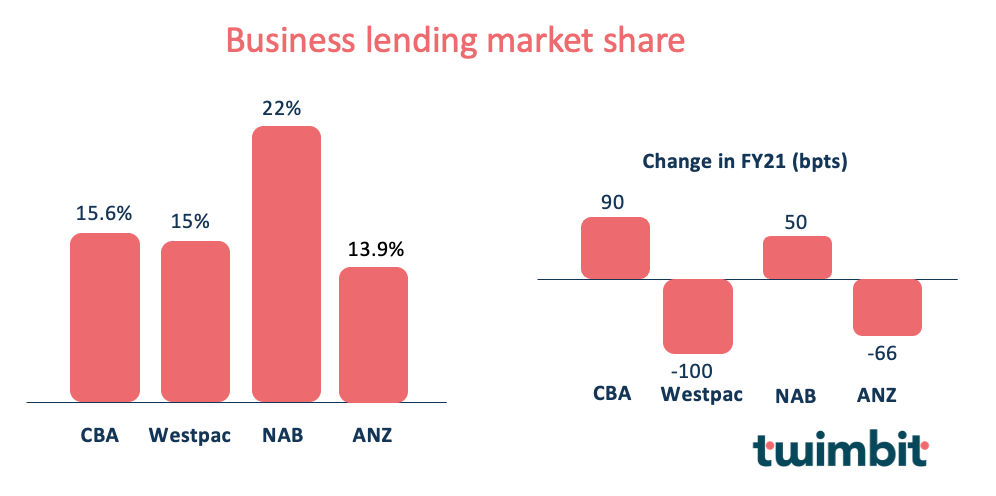

Business lending has seen the introduction of fast-track loan approvals by all four banks with new credit decisioning digital tools. These services allow for loan disbursement in under 20 minutes to small businesses. NAB leads the pack with the highest market share in the segment at 22% (Figure 3), as it:

- Provides customers with the option to meet with the banker in farm over their farm or property

- Enables quick digital loan disbursement through the introduction of its QuickBiz platform in 2017

- Personalises business owner-banker relationship to drive customer engagement

- Simplifies and fast-tracks small business lending through digital customer credit assessment

To expand all four bank’s business lending shares in the market, they should focus on:

- Augmenting supply chain financing

- Factoring

- Supplier finance

- Receivables finance

- Buyer-led programmes

- Disbursing specialised loan structuring and execution

- Creating dedicated branches and specialised staff to support regional economies

- Strengthening SME portfolio

- Enhancing existing sustainability risk management frameworks through analytics to improve credit portfolios

- Diversifying into:

- Carbon-credit markets

- Sustainability linked loans

- #3 – Winning the market with digital-first proposition

All the banks are revamping their mobile apps to provide more useful features to the customers and encouraging them to conduct more transactions digitally (Figure 4). These features include:

- Rental management

- Bill prediction analytics

- Family finance management

- Integrated customer authentication systems

- Real-time dashboards

- #4 – Reducing IT complexity

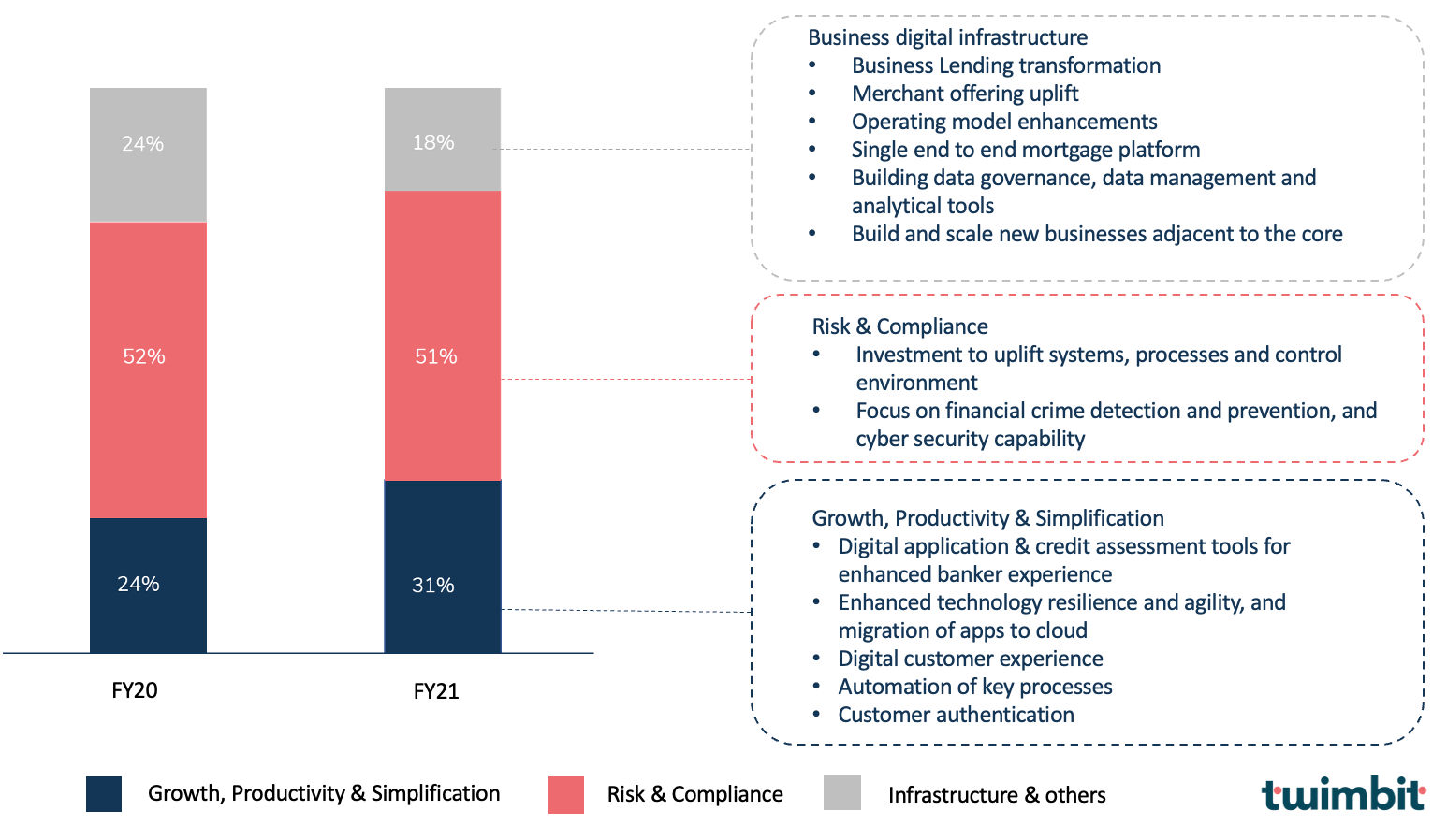

Banks are continously increasing their investments in digital applications and assessment tools for internal employees and customers. They have heavily invested in automation of processes and migration of apps to the cloud. This has resulted in reallocation of investment from infrastructure towards growth, productivity, and simplification (Figure 5).

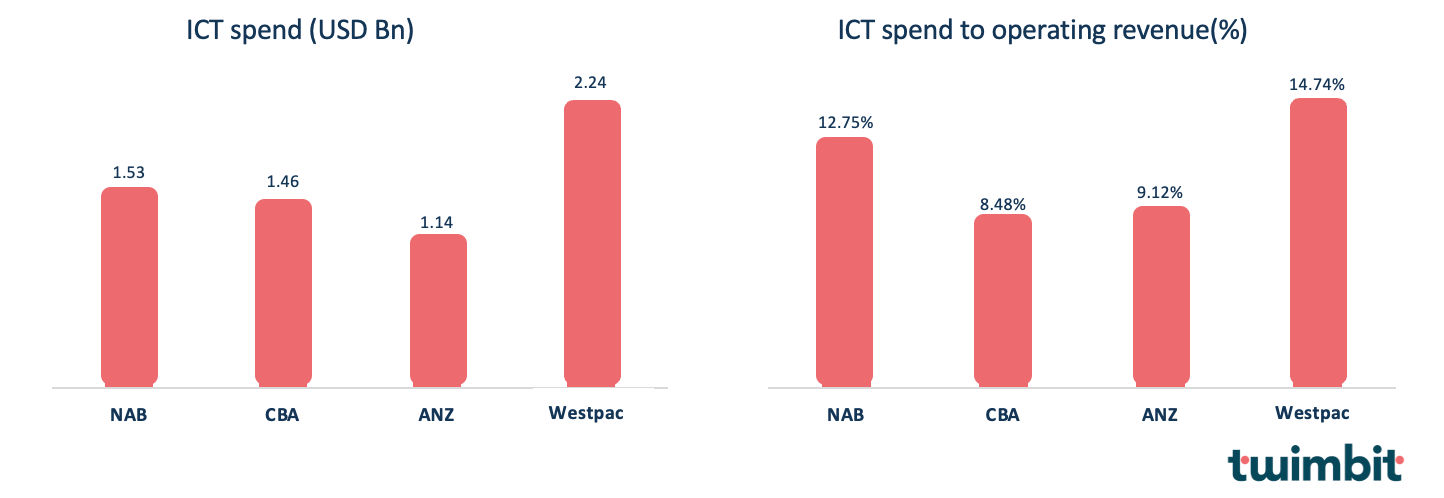

Westpac has the highest ICT spend among the big four banks, both in terms of dollar value and as a percentage of operating revenue (Figure 6).

Banks are faced with the dilemma of whether they should outsource their IT infrastructure or build them in-house. They need to focus on the following while making these decisions:

- In-house enterprise IT

- Platform customer migrations

- High-speed application delivery

- Security

- #5 – Maximizing value with data analytics

Data is valuable when it is analyzed and utilized efficiently. Banks are custodians of massive volumes of data. These volumes of data can be leveraged to cut costs and create personalised experiences for customers.

ANZ uses data to identify trends and patterns in travel behavior of its customers which is then used to fuel their communication strategies. This is done by studying the customer behavior during the time between when customers buy an airline ticket and when they travel, or during their travel or return after a trip.

They then use data on the products they have, as well as behavioural and socioeconomic insights on their customers, and overlay this with transactional intelligence to create a profile of different customer segments and decide communication strategies.

For example, a customer using their ANZ credit card for the first time on a trip to Singapore might receive a mobile message reminding them of the card’s capabilities within the airport, followed by a notification in Singapore informing them that ANZ will waive the transaction fee on their first 10 international transactions.

Similarly, all the other Australian banks are viewing data analytics as one of their top priorities to manage customer journeys and improve internal processes. Here are some other initiatives taken by the big four banks to leverage the power of data:

- Data driven approaches to provide personalized recommendation to customers based on their spending habits

- People analytics to deliver required training to employees and identify potential skill shortages

- AI led customer conversations based on personalized information

- Behavioral biometrics to manage identification and fraud detection

Conclusion

Australian banks are competing well with the Asia Pacific banking market with its digital transformation initiatives. However, the banks operational efficiency and revenue growth have seen downward trend. They must reflect and think about the answers to these fundamental questions to be future ready:

- How can they reduce dependencies on the home lending market and increase their revenue streams?

- How can they transform their business lending processes to scale up in the market?

- Which ecosystem strategies to embrace to be at the forefront of digital transformation in the long run?

- Buying vs. building to reduce the IT complexity?

- How to leverage the power of data to create holistic experiences for the stakeholders?

For detailed insights, download our State of Australia banks 2022 report.

Endnotes

S&P Global. Industry News. Retrieved May 6, 2022, from