Top 8 key takeaways:

- The emerging markets in the region present a sizeable opportunity for neobanks due to three prime factors: large unbanked population (~50%), high mobile penetration (>73%) and growing middle class.

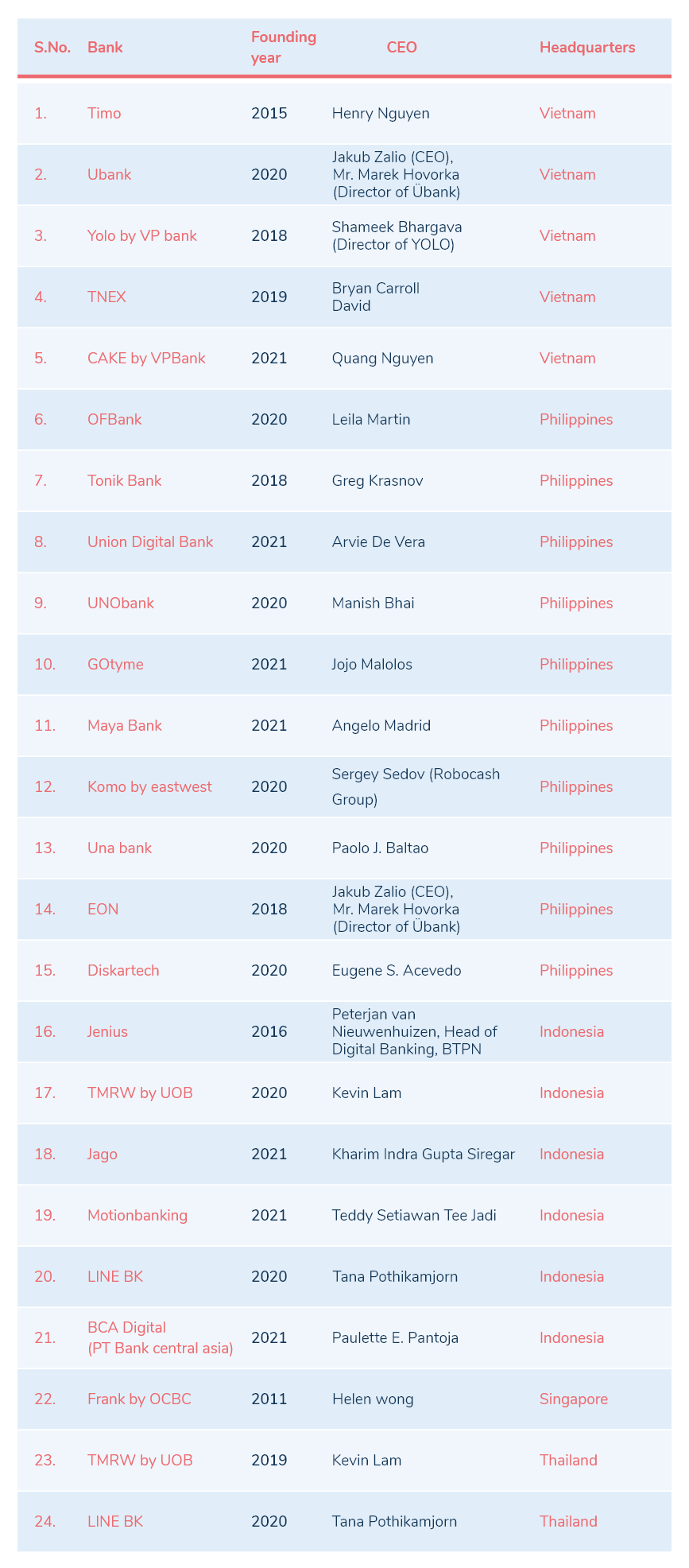

- Today, there are 24 active neobanks in ASEAN closing financial inclusion gap

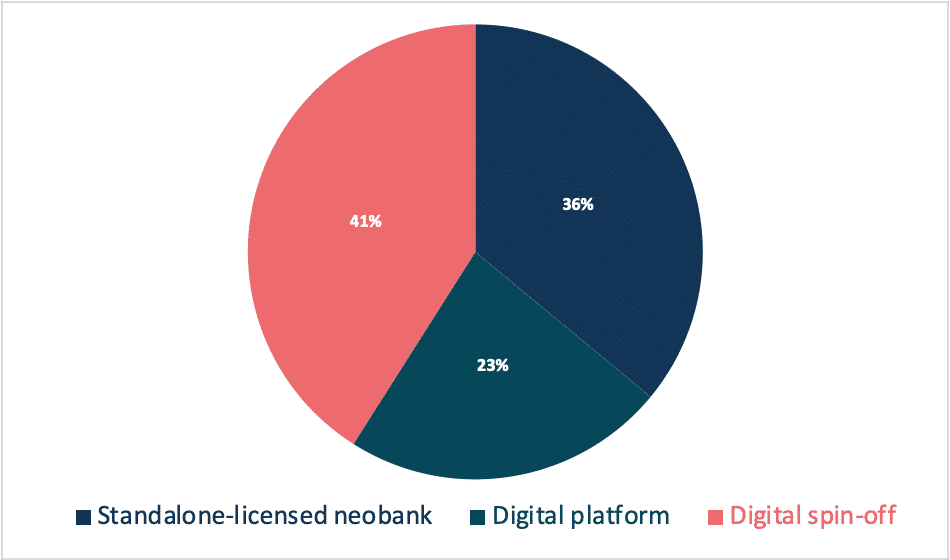

- In the region, digital spin-offs constitute approximately 41% of the total neobanks, whereas standalone-licensed neobanks rank 2nd at approximately 36%, with digital platforms at 23%.

- Malaysia has recently announced its five successful applicants for a digital banking licence.

- Countries like Singapore, Indonesia and the Philippines have established licensing regimes, while other countries are still in the discussion phase.

- The Philippines is ripe for neobanks, with an estimated 46% of people unbanked and 7 in 10 unbanked adults owning a mobile phone.

- Less than 60% of SMEs in the five countries (Singapore, Thailand, Vietnam, The Philippines and Indonesia) can access bank loans. Meanwhile, approximately 50% of the SMEs are unserved or underserved by financial institutions.

- Only 4 out of 22 neobanks cater to SMEs’ needs. Jago bank has a clear focus on SME financing and solutions. Other neobanks include TNEX, Maya bank and Diskartech have a diversified portfolio of retail and SME products.

ASEAN booming digital economy at a glance

In the last five years, neobanks have gained immense customer popularity, especially among the tech-savvy, young population, becoming a disruptive force in the banking system. Also, neobanks are vital in reaching the unbanked and underbanked population, enabling last-mile customers to access financial products and services.

With millions still unbanked and underserved, ASEAN is fertile for neobanking. Almost 50% of the ASEAN population is unbanked, which means one in two people, with a further 24% estimated to be underbanked. More than 73% of people own a mobile phone than a bank account (50%) in Southeast Asia. Hence, ASEAN’s digital economy forecasts aim to exceed US$300 billion by 2025, with rising demand for online services and mobile alternatives.

Predominantly mobile-first, the region has over 90% of its internet users connected via smartphone and 915 million active mobile connections, nearly 1.5 times its population. Given the boom of the internet and smartphone adoption across ASEAN, neobanks are ideal for achieving financial inclusion in ASEAN. Also, the emerging markets in the region present a sizable opportunity for neobanks due to three prime factors:

- large unbanked population,

- high mobile penetration,

- and growing middle class.

New digital players shake up the market, transform banking for individuals and businesses, provide access to economic opportunities and increase liquidity for business owners.

We also view the interest of regulators with the introduction of licence policies and allocations. ASEAN has uniquely developed its policy frameworks to supplement a more interconnected and inclusive digital economy.

Table 1: The rise of neobanks in ASEAN

Note: Out of the 24 neobanks in ASEAN listed above, TMRW by UOB and LINE BK operates in two markets, Indonesia and Thailand. Most interestingly, however, is that only Frank by OCBC out of 24 neobanks runs a branch in Singapore.

Recently, the Monetary Authority of Singapore (MAS) awarded digital full bank licences to the Grab-Singtel consortium and tech giants, Sea and Ant group. These four neobanks can expect to start their business operations later in 2022. Similarly, Malaysia has announced five successful applicants for a digital banking licence, all in the queue to start their operations.

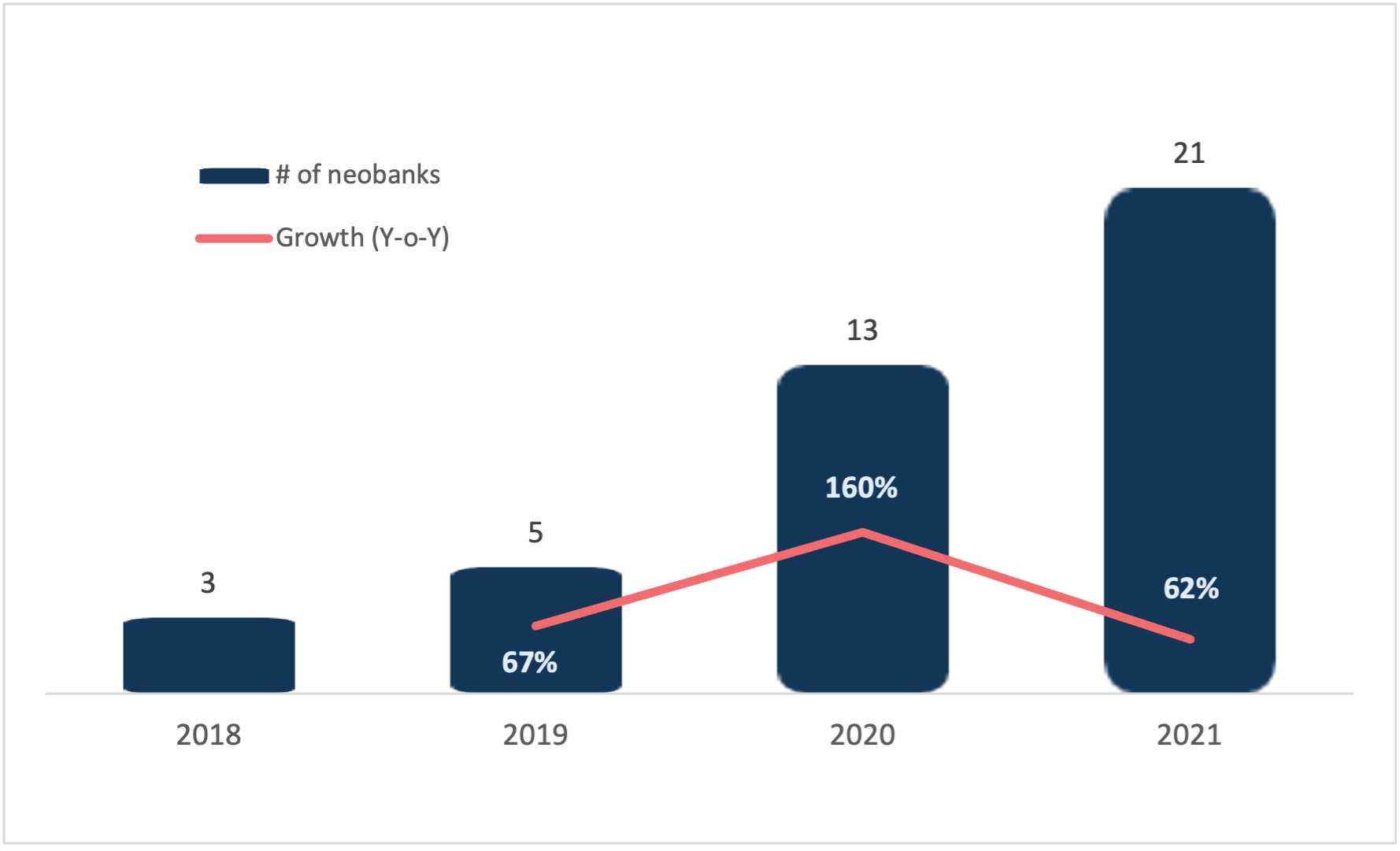

We charted an upwards slope for the growth of neobanks in the ASEAN region from 3 banks in 2018 to 20 banks in 2021 (Graph 1).

Graph 1: Growth of neobanks in ASEAN from 2018 to 2021

Note: twimbit analysis

In the ASEAN region, digital spin-offs constitute approximately 41% of the total neobanks, whereas standalone-licenced neobanks rank second at an estimated 36%, with digital platforms at 23%.

Graph 2: Classification of neobanks in ASEAN

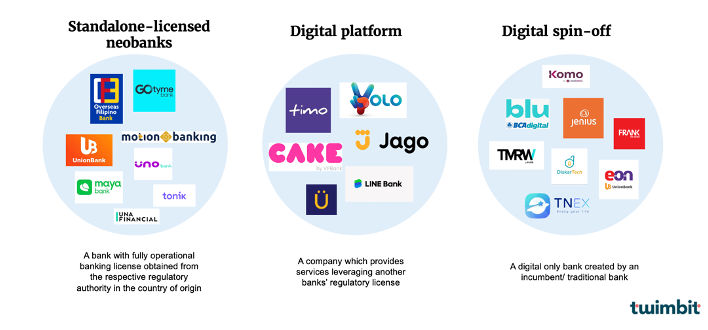

Figure 1: Examples of neobanks in each category

Neobank market landscape in ASEAN

Today, digital consumption in Southeast Asians is a way of life. The extraordinary shift in consumer behaviour allowed digital merchants to soar, creating;

- Native digital SMEs

- Early adopters who have embraced end-to-end digital services

With e-commerce platform companies like Shopee, Lazada, Grab etc., the younger population (around 61%) are driven toward fast and efficient digital propositions, unlike traditional banks. Hence, neobanks appeal to the younger audience, accommodating those who do not want to go to a branch or cannot do so. Also, at a time when citizens avoid public spaces, remote banking acts as an ideal solution.

For example, countries like Indonesia and the Philippines have thousands of islands, where most people stay in remote areas without much access to financial services. Notably, these countries are becoming well suited for banking with a mobile phone instead of in brick-and-mortar branches.

Therefore, to realise a better future for them and the full potential of the region’s demographic dividend, policymakers must understand the perspectives, priorities, and concerns of ASEAN’s millennials and SMEs.

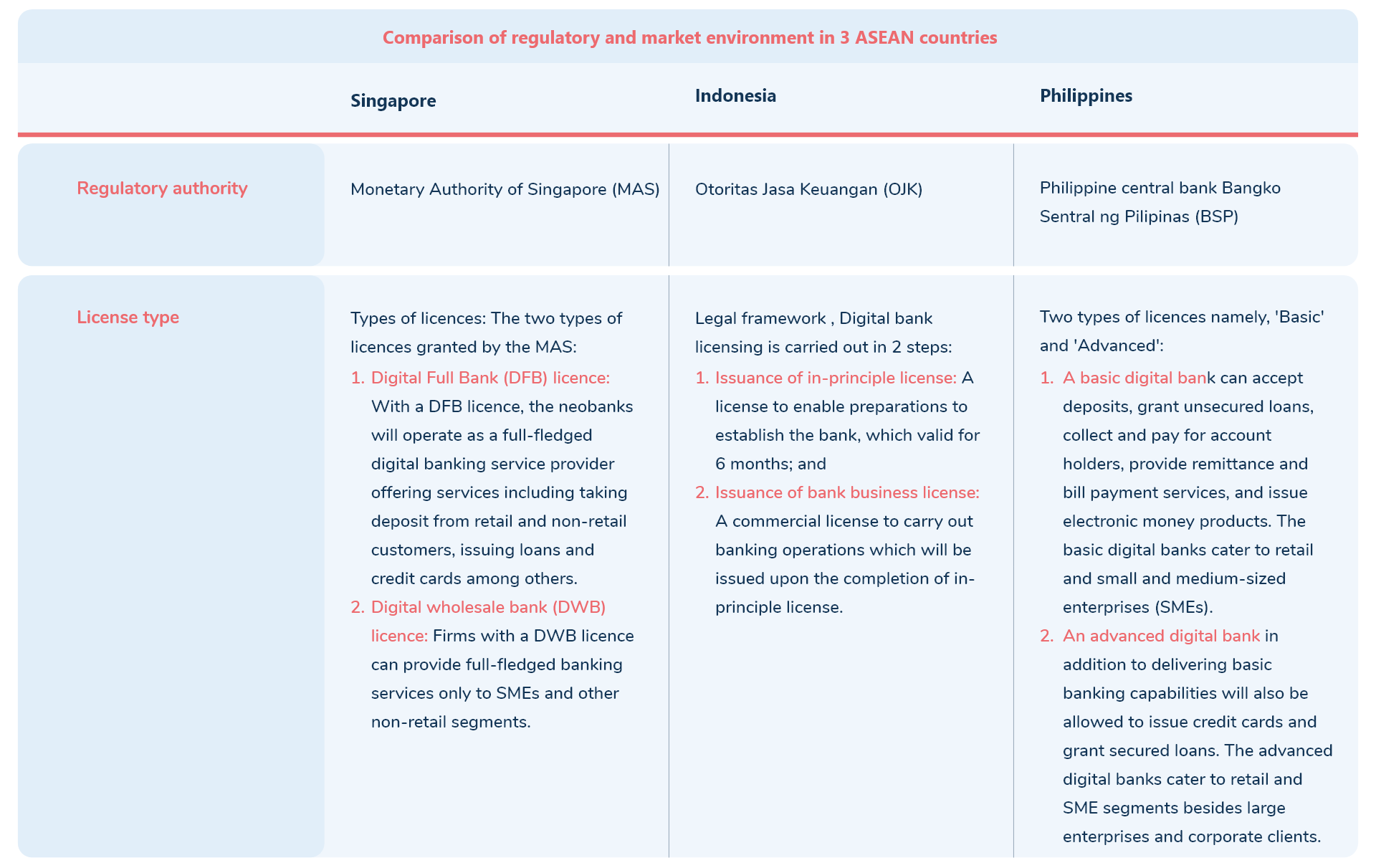

Regulators across the ASEAN countries have displayed a surge in interest when encouraging the growth of neobanks. Countries like Singapore, Indonesia and the Philippines have already prepared their respective licensing regimes, while other countries are still in the discussion phase.

For example, regulatory sandboxes exist in Singapore to handhold and support fintech startups. At the same time, it allows policymakers to be proficient and implement laws to regulate these enterprises. However, regulatory capacities vary greatly among ASEAN member countries on how to deal with fintechs.

Table 2: A comparison of the regulatory environment in 3 ASEAN countries

ASEAN’s country-specific neobank analysis

The Philippines

The Philippines is ripe for neobanks, with an estimated 46% of the population unbanked and 7 in 10 unbanked adults owning a mobile phone, representing an untapped opportunity. By leveraging the growing use of internet technology and mobile phones, most neobanks in the Philippines primarily focus on serving the millennial generation and the unbanked population.

Although most Filipinos are still learning about digital banking, around 60% of bankable customers are willing to shift to more digital banking players. As a result, the unbanked and underbanked proportion will be cut to approximately half to 20% of the country’s bankable population. This rapid uptake of users indicates Filipinos are hungry for a financial development that makes banking simple, digitally-driven, and one that genuinely helps them grow their money.

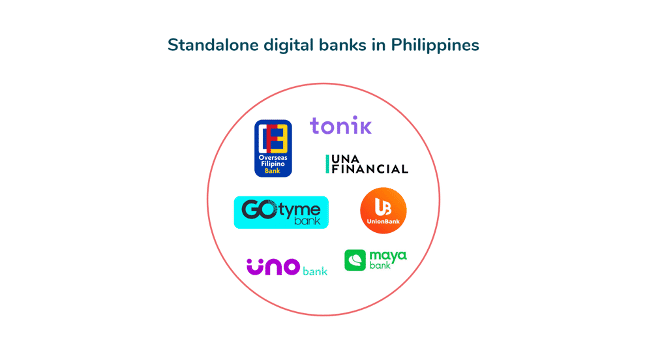

Furthermore, the Bangko Sentral ng Pilipinas (BSP) recently approved the digital bank licencing frameworks for up to seven firms (Figure 2). These include:

- Overseas Filipino Bank,

- Tonik Bank,

- UNO bank,

- GoTyme,

- Union Digital Bank,

- and Maya Bank.

BSP also approved two Singapore-headquartered fintech companies to operate their neobanks in the country. BSP as its regulator, is progressive and collaborative, working hard to realise the vision of a digital banking ecosystem to serve its population.

Figure 2: Seven standalone digital banks in the Philippines with a license from BSP

Indonesia

Indonesia has a high population of young people with a median age of under 30, and two-thirds of the country’s unbanked individuals own a cell phone. As a result, Indonesia’s unbanked population, estimated to be 83 million people, is larger than many countries’ populations.

Around 24.9% of adult Indonesians have a digital bank account. The country is also home to over 60 million micro, small, and medium enterprises (MSMEs), but nearly 70% do not have credit. Hence, neobanks intend to provide a new option for the underbanked and MSMEs to access their financial services.

Even though the country has three digital spin-off neobanks and one standalone licensed neobank, Indonesia is not considered sceptic owing to the low percentage increase in the number of neobanks. Therefore, there is a significant opportunity to serve most of the unbanked and underbanked population. Following this, BCA Digital, UOB Bank, and Bank Tabungan Pensiunan Nasional (BTPN) bank have launched their digital spin-offs (Blu, TMRW, and Jenius), respectively (Figure 3).

Figure 3: Three digital spin-offs in Indonesia catering to GenZ and millennial needs

Singapore

In Singapore, most adults’ financial needs are well-met. However, Singapore’s stronghold on traditional banks may make it difficult for neobanks to survive, as approximately 98% of Singaporeans have a bank account. Furthermore, a considerable demographic shift has occurred, highlighting an ageing population and a stifling dichotomy.

On the one hand, customers are clinging to their old “safety net” of brick-and-mortar institutions, while others have begun adopting new habits more aligned with digital banking. Frank by OCBC is the only neobank in Singapore landing on our list.

The entrance of new digital banking players in Singapore will further fragment the market. Moreover, given the pedigree of traditional banks that operate like technology companies, the most prominent way in which Singapore can establish a common ground for neobanks to grow and develop is by:

- Defining a niche customer segment/persona

- Owning specific customer journeys

- Product innovation

- Customer experience

Vietnam and Thailand

Vietnam and Thailand are preparing their ecosystems to give fully digital bank licences. They already have several domestic and foreign commercial banks working in the digital domain through partnerships or fully acquired fintech enterprises.

- Vietnam

There are many favourable conditions for Vietnam neobanks to develop and scale up to serve 40% (approx. 100 million) of the unbanked population, who possess a very high smartphone and internet adoption. In fact, most traditional banks that seek to enter the neobanking space provide innovative banking solutions through digital platforms. Also, non-cash regulations have increased the number of intermediary e-banking services such as e-wallet services and online payment gateways in the country.

Two key trends to observe in the banking industry along with providing seamless and embedded lifestyle

1. An obsession with rethinking the customer experience, and

2. Personalisation in terms of data, giving the right product at the right time, the right message at the right location, and for the right person.

David Jimenez Maireles, Chief Experience Officer, Deputy CEO, TNEX Bank

The State Bank of Vietnam is still formulating policies on digital banking. An unprepared regulatory framework is one of the significant reasons limiting local fintech growth.

Currently, Vietnam is home to four digital platforms (Figure 4) and one digital spin-off.

Figure 4: Four digital platforms in Vietnam

- Thailand

Banks in Thailand possess a conservative and traditional attitude toward digitalisation. This is because a large chunk of Thailand is unbanked (18%) and underbanked population (45%). However, many fintech firms are utilising the 72% mobile penetration rate to offer digital banking services such as e-wallets and payments.

Moreover, the Bank of Thailand has announced its intention to research the various licences it could issue to serve its primarily underbanked and unbanked populations. This move will encourage competition in the country’s banking industry, drive financial inclusion and grant Thailand access to an enriched and personalised banking experience. In addition, the success of industry disruptors in other sectors is driving banks and non-banking businesses to offer customised and customer-centric digital banking services.

Malaysia

Bank Negara Malaysia (BNM) and the Minister of Finance Malaysia are looking forward to announcing the five successful applicants deserving of digital bank licences

A. The following applicants will be licensed under the Financial Services Act (FSA) 2013:

- a consortium of RHB Bank Berhad and Boost Holdings Sdn. Bhd.,

- a consortium led by Kuok Brothers Sdn. Bhd. and GXS Bank Pte. Ltd.,

- and a consortium led by YTL Digital Capital Sdn Bhd. and Sea Limited.

B. The following applicants will be licensed under the Islamic Financial Services Act (IFSA) 2013:

- a consortium of AEON Credit Service (M) Berhad, AEON Financial Service Co., Ltd., and MoneyLion Inc.;

- and a consortium run by KAF Investment Bank Sdn.Bhd.

Malaysians own the majority of three out of the five consortiums, which include;

- Boost Holdings and RHB Bank Berhad,

- Sea Limited and YTL Digital Capital Sdn. Bhd.,

- and KAF Investment Bank Sd Bhd.

The role of SMEs in ASEAN and challenges faced in accessing finance

The benefits of going digital in ASEAN are not being experienced equally by all sectors of the economy. Even with a rise in consumer fintech and e-commerce innovation, the SME sector remains stuck with traditional banking and business. As a result, millions of ASEAN’s SMEs face issues when accessing and using digital technologies, preventing them from reaping the full benefits of participating in the digital economy and realising their full potential.

SMEs are essential in the economies of member states within ASEAN. Across the five countries discussed above, SMEs contribute between 30% and 60% of the country’s GDP. However, while SMEs are vital, most have limited access to financing. Less than 60% of SMEs in these five countries can access bank loans. Meanwhile, approximately 50% of SMEs are unserved or underserved by financial institutions.

Although SMEs are vital in the Philippines, comprising 99.5% of all businesses, they only employ 63% of the workforce. Hence, they underperform, accounting for 36% of value-added to the economy. Many barriers prevent the Philippine SMEs from reaching their full potential. The most obvious ones are poor internet infrastructure and digital skills.

This problem becomes even more acute for the 80% of SMEs in rural areas where business owners have limited digital and financial literacy, with little or no access to reliable mobile or broadband internet. The most intriguing, however, is one related to a lack of innovative digital financial products that address the specific needs of SMEs.

Poor financial infrastructure with low SME coverage by credit bureaus and inadequate distribution channels prevent banks from reaching out and servicing SMEs either physically or digitally. These are one of many key factors restricting SMEs lending and resulting in the poor financial inclusion of SMEs.

The arduous and time-consuming paperwork combined with the slim prospects of getting financial aid is limiting the growth of this market. Banks have always perceived lending to SMEs as high risk. Credit scoring for SMEs is a challenging task. Banks do not have digital avenues to access information about SMEs and use only their financial statements.

Neobanks are at the cusp of unlocking a massive SME growth opportunity

Banks and financial institutions must assess an SME’s creditworthiness accurately. Traditional norms plague the credit risk assessment, acting as a challenge when evaluating the company’s financials. However, neobanks bypass this by creating an intelligent loan application process that captures customer data beyond the financial statements. This data includes;

- customer reviews,

- repeat purchases,

- delivery cycles,

- pricing mechanisms,

- and customer interactions on social channels.

Neobanks aim to become a one-stop-shop for all SME needs. In Vietnam, the role of SMEs is crucial to the national economy. Yet, the SME sector still faces many difficulties and obstacles in accessing funding and financial services.

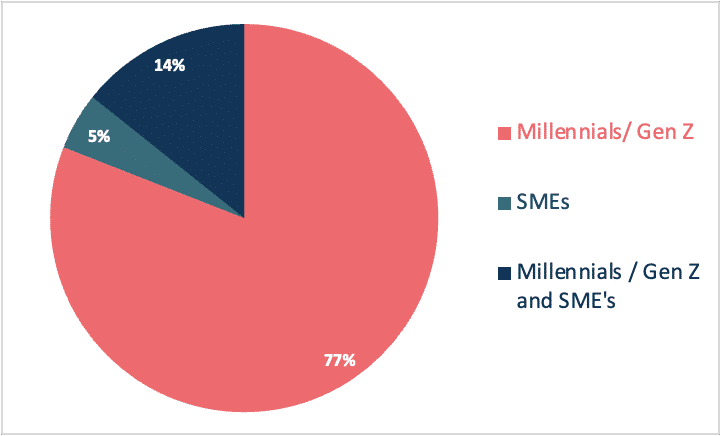

Graph 3: ASEAN neobanks segmentation with respect to customer type (twimbit analysis)

In the ASEAN region, only 4 out of 22 neobanks cater to SMEs’ needs. Among all the neobanks, only Jago bank is explicitly catering to the needs of SMEs. Other neobanks include TNEX, Maya bank and Diskartech.

Neobanking models strive to overcome the key factors limiting SMEs from lending and addressing their varied financial and non-financial needs. They plan to achieve this by financing SMEs and offering a comprehensive suite of products and services. In addition, neobanks harness the power of data, technology and partnership to create a pure-play customised digital offering for SMEs.

Considering how important SMEs are to ASEAN’s national economies based on their contribution to employment and GDP, ASEAN financial institutions must rethink the role banks want to play in the SME banking services area.

Neobanks can build capabilities organically and establish ecosystems by forming strategic partnerships with incumbents, fintechs and e-commerce providers. Most importantly, they will gain SME market leadership in the industry.

Neobanks must consider what innovation business models work best and which partners will help them achieve the right solutions to cater to this unserved and underserved market.

Governments, policymakers and regulators need to synchronise to encourage an innovation-friendly business climate which encourages collaboration. If captured effectively and responsibly, the benefits to banks, SMEs, the national economy and society will be immense.

Table 3: Neobanks catering to the needs of different customer segments

Future growth opportunities for ASEAN’s neobanking industry

Consumer banking behaviour has been effectively curtailed by the new normal, and the future aims to remain digital. However, customers will continue to look for and choose banks that encourage a more human relationship built on mutual trust, speed, and convenience, rather than the often tedious and frustrating transactional interactions. This can be seen unfolding with key developments in industry regulations and customer expectations.

With a strong digital infrastructure backing the region, consumers are digital-ready. Also, the strong digital infrastructure supports the commercial launch of 5G and high smartphone penetration.

By collaborating with incumbents, fintech companies and other non-bank players, including telecom and technology giants, neobanks can;

- create powerful digital propositions for niche customer segments,

- co-create features customised to every customer’s need,

- and enable smoother neobanking functions.

Furthermore, developing neobanking regulatory frameworks will enable operational banks to be established by non-banking players in the foreseeable future.

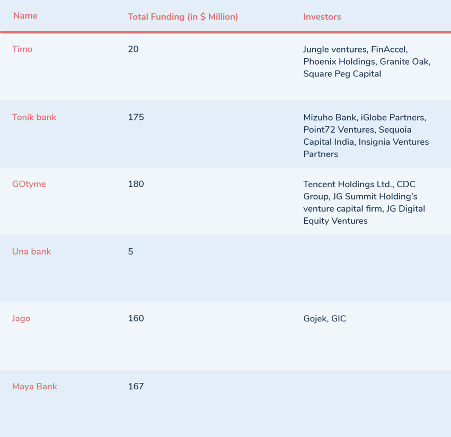

With growing buzz around the neobanking sector in ASEAN, funding and investors are plunging into the market. As a result, the ASEAN region is becoming a new investor and innovation hotspot. On top of this, digital financial services have remained centre stage and are likely to continue attracting more investments.

Table 4: Total funding amount, including all rounds

Figure 5: Investors in the race of neobanking market in ASEAN

References:

https://www.usasean.org/sites/default/files/uploads/ewc-5-asean-2021-final.pdf

https://www.weforum.org/agenda/2022/01/south-east-asia-sme-digitization-financial-services/

https://vietnamnews.vn/economy/1165050/two-thirds-of-smes-in-asean-unable-to-secure-funding.html

https://jakartaglobe.id/opinion/ai-will-power-the-future-of-banking-experience-in-indonesia

https://twimbit.com/insights/the-philippines-catching-up-with-the-neo-banking-world

https://www.prove.com/blog/digital-banking-innovations-in-vietnam

https://www.bnm.gov.my/-/digital-bank-5-licences

https://www3.weforum.org/docs/WEF_ASEAN_Youth_Survey_2019_Report.pdf

https://www.iseas.edu.sg/wp-content/uploads/2021/05/ISEAS_Perspective_2021_75.pdf

https://www.weforum.org/agenda/2020/05/fintech-can-help-smes-recover-covid-19

https://twimbit.com/insights/the-philippines-catching-up-with-the-neo-banking-world

https://media-publications.bcg.com/The-Rise-of-Digital-Banking-in-Southeast-Asia.pdf