Introduction

The banking industry has attracted maximum interest from venture funding and start-ups worldwide, a catalyst accelerating growth. This catalyst has triggered existing banks to up the ante and quickly transform to ensure their competitiveness. As a result, banks have three key opportunities as they look to win the future.

1. Own customer journeys

Today, to win the customers’ business, it is not just about making a differentiated offer in terms of product and service features. Instead, the bank needs to be a part of the customers’ entire journey, and banking plays a role in the whole process.

In the past, the home loan market was about providing a competitive home loan to consumers. Success was about ensuring a good distribution channel and a well-oiled sales infrastructure. However, this is no longer sufficient.

Today’s leading banks want to be involved in the customer journey pre-purchase, during the purchase and support the lifetime ownership of the asset. Banks, see this as an opportunity. An opportunity to be part of a 20-year journey with the consumer, enhancing their ability to make the most of this asset, which involves re-financing and advice.

2. Invisible banking

Banking is needed, banks are not – Bill Gates, 1994.

Customers want consumer banking services quickly but without the hassle of wanting to deal with the bank. Ideally, as a consumer, you should be able to seamlessly consume it in your everyday life without needing any interaction with the bank. This level of seamlessness will truly drive financial inclusion, propelling growth for banks worldwide.

Being able to seamlessly enable consumers to improve their life outcomes by accessing a range of financial services without opening the banking app or calling your banker should be the desired end-state. For example, the ability to access credit finance on a third-party website can increase the reach and penetration of short-term loans.

3. Increase per capita consumption of services

Savings accounts, current accounts, credit cards, home loans, car loans, etc. – what do they have in common? A majority of the world’s banking customers today consume these limited services.

The average per capita consumption of financial services in developed markets would range between 4 to 6, while in developing markets, that number will be much lower at 1. Reach, the product’s complexity, and the high cost to serve – is a combination of factors that have been the limiting element for the banks.

However, fintechs popping up across the world open up a whole new world of opportunities, akin to consuming mobile applications on your phone in the pre-iPhone era, back when there was no touch screen interface, and a closed ecosystem limited your ability to consume applications.

Today, the average consumer uses at least 10 mobile apps a day and about 30 a month. The same is possible with financial services. Open banking sets to achieve new heights, driving exponential growth in the per capita consumption of financial services.

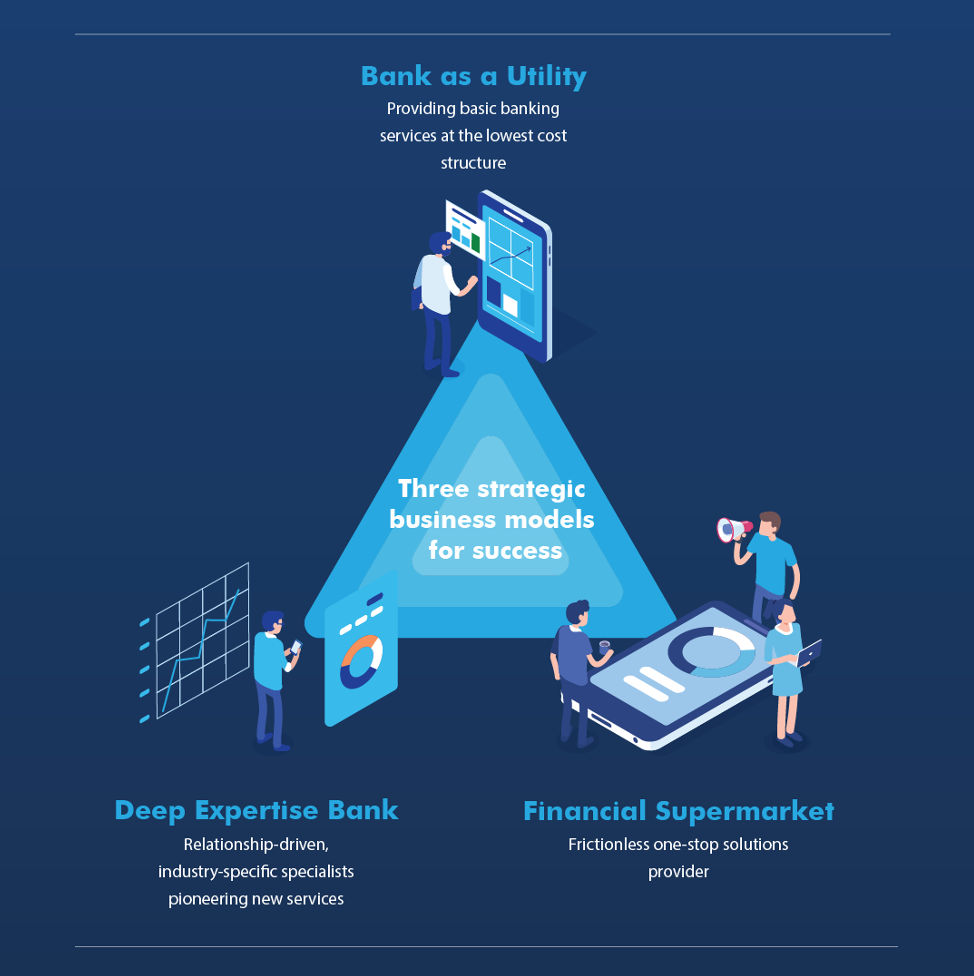

Business model options – the 3 strategies

The competition from a new breed of financial service providers, including neobanks, urge existing banks to transform rapidly and meet consumers’ new, unique needs. Because of this, we expect rapid growth in the financial services industry with innovation driven by new entrants and technology giants.

The key question is – are banks the biggest beneficiaries of this growth, or will they lose out to the competitive new entrants or the established technology giants such as Google, Apple, Facebook and Amazon. In the case of the telecoms industry, the telecom service providers lost out on the new growth avenues to a new breed of market participants, such as WhatsApp, Zoom, and Netflix, to name a few. Will the banking industry fare any better?

We believe banks have positioned much better to compete effectively. But they need to make decisions on their strategic choices moving forward. They need to choose between one of three options;

- bank as a utility,

- deep expertise bank,

- and financial supermarket.

While the banks may adopt one of the three options as their priority, it does not necessarily require them to abandon their existing portfolio of services. They can continue their existing services, but the core competence and future innovation development should prioritise their choice of strategy.

1. Bank as a utility – Provide banking services at the lowest cost structure

Many banks realise that they cannot keep pace with all the innovation happening in the industry. Banks cannot develop propositions in an agile manner and support the rapidly changing consumer demand. Therefore, banks may opt to become “Bank as a Service” provider to providers. It focuses on developing highly cost-effective infrastructure and operational processes to support up and coming financial service providers.

Banking as a service focuses on enabling the success of third-party providers. This model becomes more like infrastructure owners by bundling their offerings into APIs, white labelling them and facilitating third-party providers to build their products over them. The banks will charge a fee for their infrastructure use or have revenue-share arrangements with the fintechs.

In this model, the traditional bank acts as a provider of its banking license and key products, including deposits, loans, and repayments. The fintech, on the other hand, manages account opening, movement of money and issuance of cards through its platform and UI.

Federal Bank Ltd. of India – Innovating and Growing through Partnerships

Federal Bank has bundled its 300+ APIs into 13 categories and has partnered with more than 50 fintechs, providing a full-stack for Jupiter and Fi, the two leading neobanks. In less than three minutes, Jupiter and Fi can offer up a savings account, complete with a debit card.

More than 450,000 accounts are being opened every month with these two partnering neobanks. The growth in accounts opened has been nine-fold, and in CASA balance, the growth has been seven-fold in the past six months. Neobanks partner with traditional banks, i.e., Federal Bank of India, which provides the platform for customer management, holds the customer funds and provides interbank payments and settlements. The neobank takes the front seat and is responsible for product distribution and customer journey. Along with neobanks, the Federal Bank of India has partnered with service providers, Flexmoney for debit card EMIs and Rupeek for gold loans.

2. Deep expertise bank – Relationship-driven, industry-specific specialists pioneering new services

Deep expertise banks are also known as specialised banks due to their offerings and speciality in a specific industry. A deep expertise bank can focus on serving only a particular industry or a division or segment of a much larger bank which serves a specific industry. Innovation is the key player here in this model. Banks will need to continuously innovate to support the diverse and ever-evolving requirements of their industry.

Banks are being challenged with shrinking revenues from their existing product portfolios. The current operating model must change. Banks should focus on one product line or category and develop expertise in delivering that product.

There are unlimited opportunities for banks to develop deep expertise. Below, we discuss four possible examples of how banks can build their deep expertise to help understand their innovative options.

- A) Financial inclusion

India Post Payments Bank (IPPB) is a division of India Post, established in 2018. Aiming to bank the unbanked population of India by utilising the >155,000 post offices and >300,000 mail carriers, IPPB acts as the financial services advisor to provide doorstep banking services to the last mile customers using the India Post network.

What does IPPB offer? Well, it offers all the basic banking functions, from:

- deposits,

- money transfers,

- bill & utility payments,

- and merchant payments.

IPPB also provides the educational importance of savings and insurance for customers. The bank earned more than 50 million customers as of January 2022.

- B) Agriculture

Westpac Agribusiness – Agribusiness is separate from the bank’s personal and business banking divisions. The division oversees the farmers’ farming and agricultural needs by working alongside local specialists familiar with the local area inside out. Offering a varied range of services from livestock leasing to seasonal funding needs, the bank helps farmers and the like to achieve their long-term growth objectives.

Instead of making the customers come to the bank branch, the bank follows the mantra of ‘Your paddocks are our offices’ where the representative goes to the customer’s farm to better understand and assist them with their specific needs. Westpac was awarded CANSTAR’s Bank of the Year for Agribusiness in 2021.

- C) Banking the High-Net-Worth Individuals

Japan houses more than 50% of all high net-worth individuals within the APAC region, possessing trillions of dollars in personal assets currently deposited in low-yield deposits. Individuals are looking to invest their assets out of these low-yield deposits, causing local and international players to fight to acquire these new customers.

The requirements have changed. No longer are individuals merely seeking financial advice about investment options. On the one hand, customers are interested in niche advisory on how to send their children to foreign schools and universities, a field in which foreign banks have an edge. On the other hand, Japanese banks have an edge due to their extensive distribution network and simpler product offerings, winning the customers over. Moreover, the customers prefer the simpler products over the sophisticated products offered by foreign banks after the global financial crisis.

Japanese banks like Mizuho Financial Group and Sumitomo Mitsui Financial Group provide services to such individuals by preparing tailored proposals regarding asset succession and wealth transfer between generations. Another speciality of these domestic banks is assistance in buying property and selling business of the wealthy.

- D) SME banking

MYbank – MYbank is China’s first digital bank established to provide financing to MSMEs, a vital growth engine for the Chinese economy. Since its inception in 2015, the bank has provided loans to more than 20 million MSMEs in China. The bank operates on a 3-1-0 lending model, where the online loan application takes just three minutes, the loan approval one second and the whole process requires zero human intervention.

MYbank does not approve decisions based on a person’s credit history or available collateral for an offer. Instead, this is where Big Data comes to play. Big Data from its parent company, Alibaba financial services, boast a customer base of more than 900 million to assess the monthly sales of small businesses and their repayment patterns.

3. Financial supermarket – Frictionless one-stop solutions provider

Each customer approaches things differently, having different financial needs for which they have to approach different service providers. Enter financial supermarkets – an answer to all customer needs.

Financial supermarkets can be driven by financial institutions that build an ecosystem, offering various financial and lifestyle services. They commoditise each customer journey and can become a standard solution across customer segments. Therefore, banks, fintechs, and neobanks can serve a large gamut of customers and increase their capita consumption of services, creating an opportunity for banks to cater to the entire customer lifecycle and embed it in their daily lives.

Banks can choose to become orchestrators by enabling third-party services on their platform or partner to drive marketplaces for a niche customer solution. The industry is also witnessing a new wave of banking SUPER APPS that focuses on customer acquisition and retention through various unrelated services. However, the success of the ecosystem orchestrators, marketplaces, and super apps lies in how they can remove any friction in the system that degrades the customer experience on the platform.

The benefits are as clear as day for banks that intend to become financial supermarkets. These benefits include banks being able to generate increased fee revenues based on the services they offer to customers. Also, customer loyalty and retention will increase as it will become difficult for customers to switch to another competitor.

Case study – DBS Bank

DBS Marketplace – DBS launched its consumer needs-driven marketplace in 2017 with DBS Car Marketplace, followed by Electricity Marketplace, Property Marketplace, and Travel Marketplace in 2019.

The DBS Property and Car Marketplaces generated more than USD 730 million (SGD 1 billion) in loans across Singapore, Taiwan, and Hong Kong markets in FY2020. DBS Marketplace is an example of an orchestrator providing customers with loans required to purchase properties or cars listed on the platform.

DBS Car Marketplace – A one-stop solution portal for all car buying and selling needs, presenting customers with all the information required to purchase and sell a car. Also, the bank has partnered with sgCarMart and Carro and is currently the largest seller-to-buyer car marketplace in Singapore.

DBS Electricity Marketplace – This allows customers to compare different electricity pricing plans for a seamless transition between electricity providers. Currently, customers on the platform can pick and choose from 15 fixed price plans and 2 Non-Standard Price Plans provided by four electricity providers, namely, Geneco, Keppel Electric, PacificLight and Tuas Power.

DBS Travel Marketplace (in partnership with Singapore Airlines, Expedia and Chubb Insurance Singapore) – Allows customers to book flights and hotels and provides them with travel insurance all in one place. In addition, the portal tries to enhance the customer experience by reducing the time and effort taken on multiple platforms to plan a vacation.

The services offered on DBS Marketplace have expanded, and the portal now offers services about education, home renovation and health along with the ones stated earlier.

References

Accenture. News. Retrieved April 11, 2022, from

https://www.accenture.com/us-en/insights/banking/top-10-trends-banking

American Banker. Industry Analysis. Retrieved May 19, 2022, from

https://www.americanbanker.com/news/the-rise-of-the-invisible-bank

Asia Development Bank. Report. Retrieved April 16, 2022, from

BCG. Business Article. Retrieved April 8, 2022, from

https://www.bcg.com/publications/2018/four-ways-banks-can-radically-reduce-costs

Deloitte. Capital Markets Outlook. Retrieved April 14, 2022, from

Deloitte. Banking Report. Retrieved April 8, 2022, from

Deloitte. Banking as a Service, Explained. Retrieved May 19, 2022, from

International Finance Corporation. Case Study. Retrieved April 18, 2022, from

McKinsey & Company. Article. Retrieved April 19, 2022, from

McKinsey & Company. Industry News. Retrieved May 9, 2022, from

Reuters. News. Retrieved April 13, 2022, from

https://www.reuters.com/article/us-wealth-japan-analysis-idUSTRE58G14320090917

Wisegeek. Article. Retrieved April 27, 2022, from