Telcos in the Asia Pacific have continued to build on the growth momentum from 2021. There is both increase in revenue and profitability. Tariff hikes have enabled Indian telcos in particular to register an impressive overall revenue growth story.

In this report, we evaluate and summarise the performance of 40 Asia Pacific telcos for Q2 2022 (Second quarter 2022, April- June). The analysis includes metrics such as revenue, EBITDA, mobile ARPU and CAPEX.

#1 Indian telcos set new benchmarks with growth of 22%

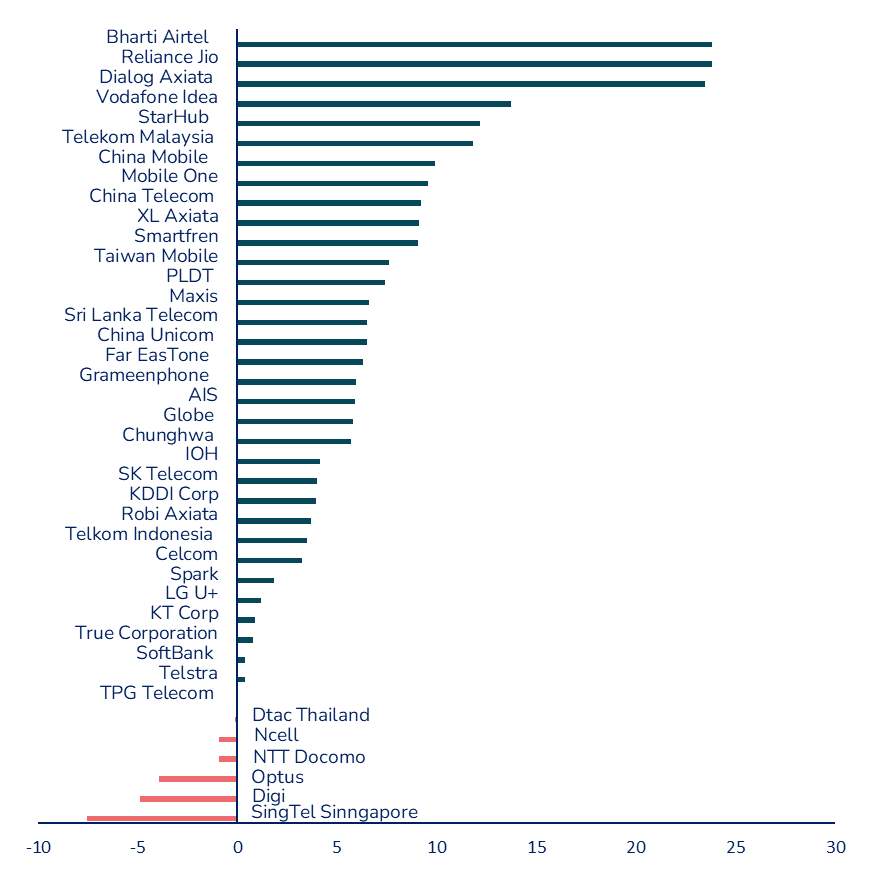

- 85% of telcos registered positive revenue growth in 2Q 2022 (figure 1). 40 telcos cumulatively added new revenues of US$ 8.67 billion.

The performance by the Indian telcos Bharti Airtel and Reliance Jio in the last two quarters is exemplary. No telco operating at such a large scale has recorded growth over 20% in recent times. These two Indian operators have performed well, and the trajectory is expected to continue.

Figure 1: Revenue % change for APAC telcos, Q2 2022

- The exceptional results are mainly attributed to tariff revision in the Indian market. This hike in mobile tariffs provided a cushion to the operators to rollout 5G and make other infrastructure related investments.

- Furthermore, tariff hikes has led to tremendous success in improving ARPU for the Indian operators (figure 2)

Figure 2: ARPU in Indian Rupees (US Dollar) Q2 2022 vs Q2 2021

| Telco | ARPU in Q2 2022 | ARPU in Q2 2021 | change (y-o-y) |

| Bharti Airtel | 183 ($2.3) | 146 ($1.84) | 25.3% |

| Reliance Jio | 176 ($2.22) | 138 ($1.74) | 27.5% |

| Vodafone Idea | 128 ($1.61) | 104 ($1.31) | 23.1% |

- The performance from StarHub in Singapore is also commendable. It focused its efforts on the enterprise business, and it is beginning to pay off as it recorded the 5th highest revenue change in the region. The enterprise segment contributed 37% of the total revenue in 1H 2022 (first 6 months of 2022). Additionally, the segment revenue grew 16.9% in 1H 2022.

- On the other hand, Trustwave, cybersecurity arm of SingTel, suffered heavily after the divestment of its payment card industry compliance business in October 2021. Market reports suggest that SingTel is looking to sell off this business. This led to a decline in revenue for the operator in this quarter.

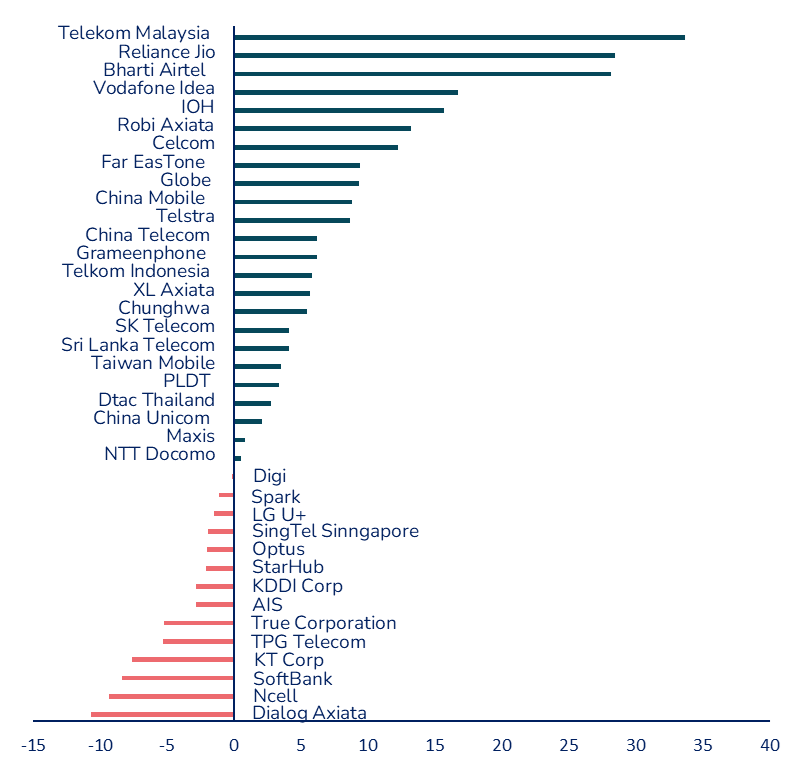

#2 EBITDA growth of 4.5% in Q2 2022

- Telcos are placing bets on digital and going beyond connectivity as they seek revenue growth. They continue to focus efforts on initiatives such as cloud-based virtualised infrastructure to drive cost efficiency. Close to 65% of operators enjoyed positive earnings change in Q2 2022 (figure 3).

- Telekom Malaysia’s performance is noteworthy as it leads the region in terms of positive EBITDA change. It accomplished favorable results in all the segments. The Malaysian operator is the leading convergence provider in country. It continued to expand the infrastructure capabilities and add subscribers along the way. It plans to expand its fibre network to 6 million premises by the end of 2022 and recorded a 14.1% increase in subscribers year on year (y-o-y).

- The % of total Cost (including depreciation & amortisation) to revenue decreased from 87.4% in 2Q 2021 to 77.6% in Q2 2022. Optimisation efforts enabled TM to record lower manpower and other OPEX costs.

Figure 3: EBITDA % change for APAC telcos, Q2 2022

- Dialog Axiata noted a decline in EBITDA despite good growth in revenue due to higher network costs and escalation in the cost base.

- In the case of SoftBank, all business segments showed growth except for the consumer business. This was down by 4%. The segment was impacted by the mobile business and the decline in sales of handsets.

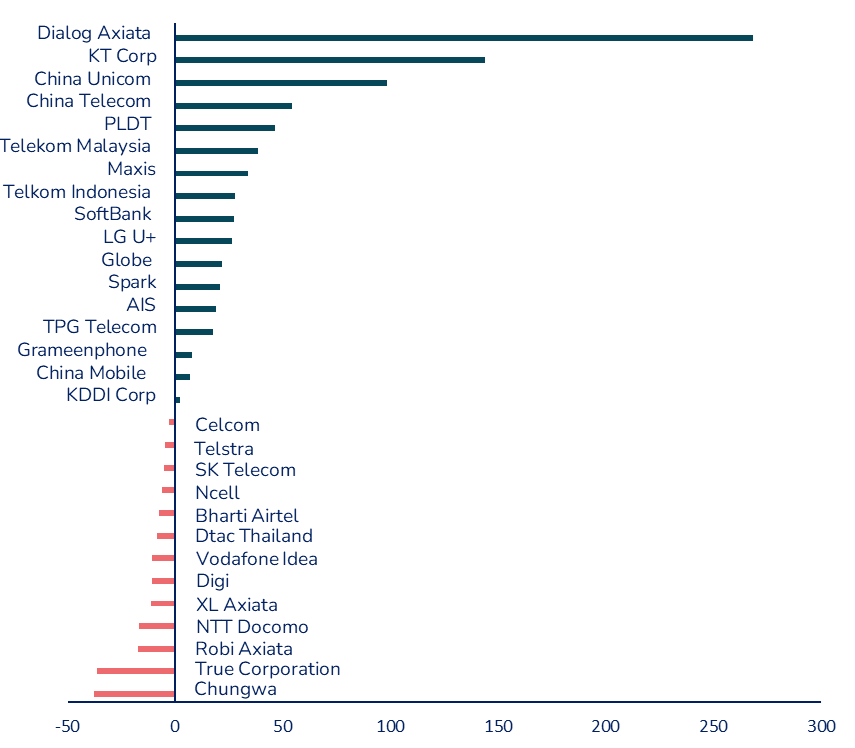

#3 Trend for lower CAPEX spending continued in Q2 2022

- 45% of the telcos charted a negative change in their CAPEX in Q2 2022. This is consistent with what we observed in Q1 2022. This trend is expected to continue through 2022.

- The peak investment phase has passed for most of the operators as they rolled out 5G in 2020 & 2021. Furthermore, the trend for CAPEX savings through co-building has continued in the region.

- For the operators beginning/yet to launch 5G, the CAPEX is anticipated to evidently rise from 2023.

- Dialog Axiata’s CAPEX spending has been on the rise in Q1 2022 and also in Q2 2022. The company noted the highest change in CAPEX of 209% in Q1 2022 (first quarter of 2022) a change of 268% in Q2 2022. The spending includes:

- investing in the broadband infrastructure to strengthen its leadership in the Sri Lankan broadband market,

- fuelling the core and transport networks, including fibre and 4G capacity upgrades.

- It was interesting to note that two of the Chinese telcos are amongst those who have led in CAPEX investments in this quarter. China Unicom made significant enhancements in network capabilities. China Telecom intensified its cloud network integration capabilities. The investments included-

- 81K servers to computing power, 19K cabinets in the IDC segment, established two-tier security core platform across 32 data centres, etc.

Figure 4: CAPEX % change for APAC telcos, Q2 2022

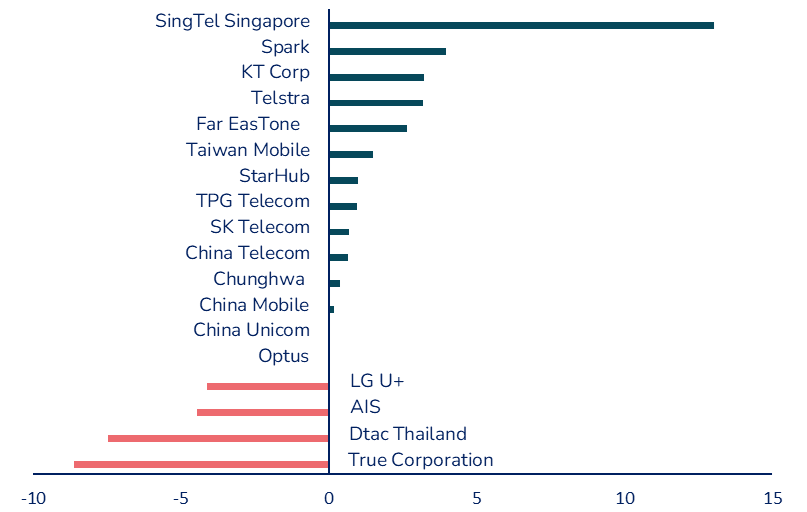

#4 Trends in ARPU

- The easing of border controls has contributed to the increase in ARPU for SingTel driving growth in roaming revenues.

- Spark outperformed the New Zealand market with a mobile service revenue growth of 5.5%. Its data-driven marketing strategies paid off and it registered a 13% growth in number of subscribers signing up for various subscription plans.

- In 2021, the launch of 5G helped stabilize the declining ARPU trend. China and South Korea, the early adopters benefitted from this in 2021. However, this initial benefit on arresting the ARPU decline has now diminished.

Figure 5: Mobile ARPU % change for APAC telcos, Q2 2022

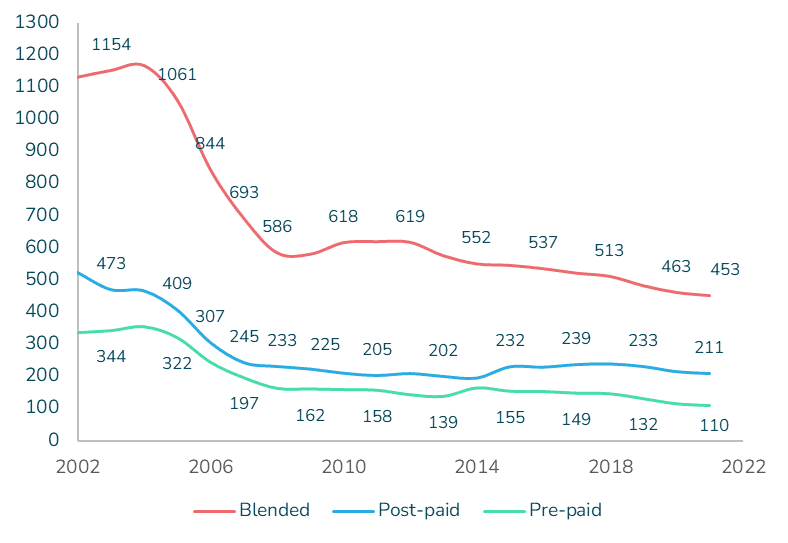

- In Thailand, consumers have shown a preference to migrate to lower-tier data plans, particularly in the pre-paid segment. This has resulted in decline in mobile APRU over time (figure 6). Intense price competition has contributed to this trend.

- Inflationary pressures and surge in Omicron cases have also contributed to the decline in ARPU.

- The Thai telcos are positioning 5G as a premium offering and expect this to help uplift ARPU by 10 to 12%.

Figure 6: Mobile ARPU in Thailand 2002-2022 (Thai Baht)

#5 Indian and Chinese telcos ace the twimbit’s growth index in Q2 2022

- twimbit’s Growth Index recognise the leaders based on two parameters with an equal weightage to:

- Absolute change in revenue

- Percentage change in revenue

Figure 7: Net addition and % revenue change for top 5 telcos, Q2 2022

| Telco | Country | Change (US$ million) | % change (Y-o-Y) |

| Bharti Airtel | India | 584 | 23.85 |

| Reliance Jio | India | 587 | 23.82 |

| China Mobile | China | 3,658 | 9.94 |

| China Telecom | China | 1,549 | 9.19 |

| Vodafone Idea | India | 164 | 13.74 |

| Top 5 | – | 6,541.1 | 9.87 |

| All APAC | – | 8,670.8 | 6.1 |

- The top 5 telcos have all registered growth in excess of 10% as compared to the overall industry growth of 6% in Q2 2022.

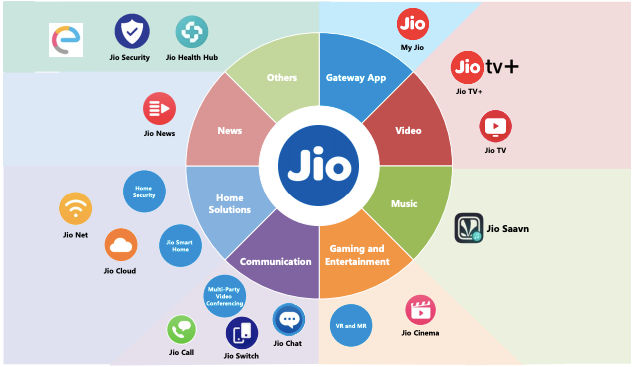

Indian telcos, Jio and Airtel have created a product/service ecosystem. The telcos place their diverse products strategically into the life journeys of consumers. This makes it difficult for any user to switch brands. The mobile apps for these operators are not less than a super app. Here is a glimpse of the ecosystem that Jio has created over time (figure 8).

Figure 8: Product/service portfolio of Reliance Jio

Vodafone Idea (Vi) has an intriguing comeback story. The operator struggled in 2021 with a negative change in revenue and EBITDA. The setback was because of AGR (Adjusted Gross Revenue) dues to an extent of US$ 8.1 billion which increased the telco’s liability heavily. In recent times, the relief measures by the telecom department in India eased pressure on Vi. In addition to this, the tariff hike gave the operator an opportunity to make a perfect comeback.

Throughout 2021 China Mobile aced the twimbit’s growth index. Even though it operates at such a massive scale, it consistently delivers an above-market performance. Similarly, China Telecom makes it amongst the top 5 telcos to ace the growth index for several quarters. These two telcos enjoy success from the rapid progress made in the enterprise/B2B segment. Both operators have been delivering enterprise projects at scale.

It is a delight to read through their Investor/analyst presentation. The consistency in reporting and segmentation of business units is remarkable. It works out as a best practice/learning for other operators in the region. Please find below the link to the presentation by China Mobile.

Telcos achieved commendable growth in Q1 2022 and the story continued in Q2 2022. Stay tuned for our next quarterly report (Q3 2022) and updated version of the following reports-

- Asia Pacific telcos to ace non-connectivity revenues in 2021

- 2021 Asia Pacific telecom enterprise