Telcos continue to make great headway in growing the non-connectivity business. It has grown from 13.4% of revenues in 2019 to 19.8% in H1 2022. Growing the ecosystem revenues to fight the ARPU decline in connectivity services is a top priority for every telco. The Asia Pacific region, with its diversity, offers a fascinating view of the varying strategies adopted by telcos to grow business beyond connectivity.

This research provides an insight into the operators’ progress in driving revenues from non-connectivity services and benchmarks the Top 10 telco’s to ace growth from this segment.

Assumptions and methodology

- We studied 40 telcos across 16 Asia Pacific countries that provide consistent, detailed updates on their business progress. 25 out of the 40 telcos had made progress in establishing and reporting their non-connectivity business revenues.

- Non-connectivity is defined as services excluding voice, fixed-line, broadband, and enterprise connectivity (IP-VPN, SD-WAN, etc.). It is broadly classified into four pillars — enterprise, content & media, e-commerce, and others.

- We identified the top 10 telcos to ace non-connectivity revenues in H1 2022 based on the twimbit growth index, viz., a combination of absolute revenue growth, % change in non-connectivity business.

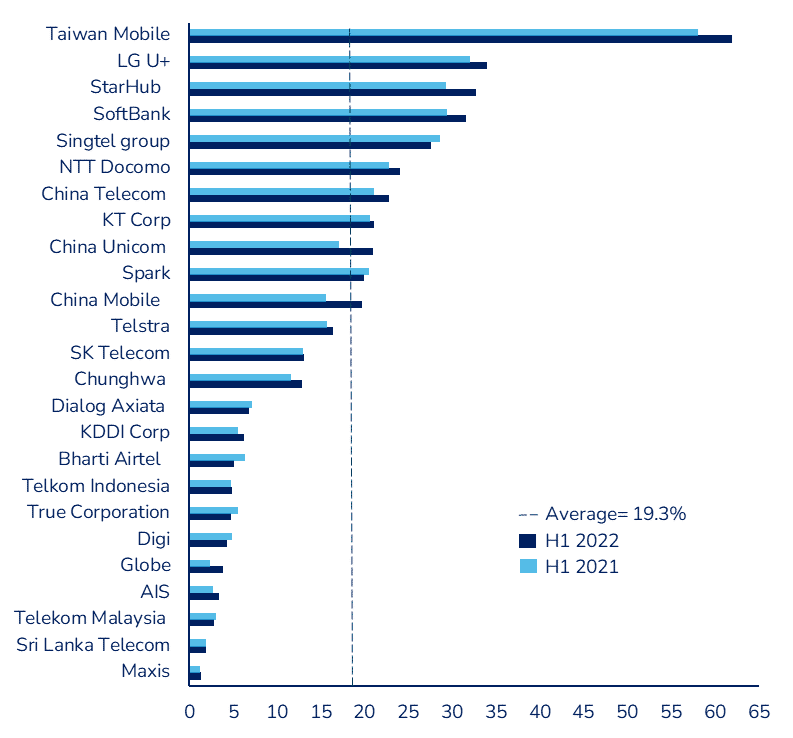

Exhibit 1

Percent of non-connectivity revenues to total revenue

twimbit’s 4 pillars of non-connectivity services

We classified non-connectivity services into 4 distinct categories, defining them as ‘twimbit’s 4 pillars of non-connectivity services’

- E-commerce

Being early to market is a prerequisite for success in this category. We have observed a tailwind in operators having their online portals to facilitate commerce. Many telcos are also using their stores to enhance the e-commerce trading volume.

- Enterprise non-connectivity

(Cloud, managed services, IoT, cyber security)

The Enterprise business represents the must-win segment for most service providers, especially with the advent of 5G. A detailed twimbit study on the enterprise segment is available on the platform (click here).

- Content and Media

(IPTV, pay TV, content leasing, OTT services)

Bundling content with broadband connectivity has helped telcos across the board. Many telcos have invested in developing and scaling localised content. Partnerships with Netflix, Amazon Prime and Disney has been extensively pursued across the region.

- Others

(Financial services, digital marketing, analytics, telehealth, education)

Payments represent a new ongoing opportunity. Whereas gaming, digital marketing, and other non-connectivity areas have seen some success in specific markets.

twimbit’s top 10 operators to ace non-connectivity revenues

To arrive at the top 10, we scored them on three parameters, giving each parameter equal weightage (33%).

- Absolute change in revenue from non-connectivity services between H1 2021 to H1 2022.

- Percentage change in non-connectivity revenues from H1 2021 to H1 2022.

- Revenue from non-connectivity services as a percentage of the total in H1 2022.

Exhibit 2

Top 10 operators to ace non-connectivity revenues (NCR) in H1 2022

| Rank | Telco | NCR H1 2022 (US$ million) | NCR H1 2021 (US$ million) | Absolute change (US$ million) | % change y-o-y | % of NCR of total revenue |

| 1 | Taiwan Mobile | 1,809.4 | 1,543.3 | 266.0 | 17.2 | 61.9 |

| 2 | China Mobile | 14,698.2 | 10,393.1 | 4,305.2 | 41.4 | 19.7 |

| 3 | China Unicom | 5,540.7 | 4,204.5 | 1,336.2 | 31.8 | 21.0 |

| 4 | China Telecom | 8,279.3 | 6,939.3 | 1,340.0 | 19.3 | 22.8 |

| 5 | StarHub | 256.0 | 211.3 | 44.7 | 21.1 | 32.7 |

| 6 | SoftBank | 7,924.8 | 7,058.3 | 866.5 | 12.3 | 31.6 |

| 7 | LG U+ | 871.9 | 808.1 | 63.8 | 7.9 | 34.0 |

| 8 | Chunghwa | 477.7 | 415.7 | 62.1 | 14.9 | 12.8 |

| 9 | KDDI Corp | 1,495.0 | 1,307.2 | 187.9 | 14.4 | 6.2 |

| 10 | Telstra | 1,329.7 | 1,265.0 | 64.7 | 5.1 | 16.4 |

| Top 10 total | 42,682.7 | 34,145.7 | 8,537.0 | 25.0 | 20.8 | |

| All APAC total | 47,923.5 | 39,411.0 | 8,512.4 | 21.6 | 19.3 |

- Percentage of non-connectivity to total was 20.8% for the top 10 telcos compared and the segment grew at 25%

Key Insights

#1 Non-connectivity will grow to 28.5% of total revenues for telcos in Asia-Pacific by 2025

Exhibit 3

Average % of non-connectivity revenue to total revenue 2019-2025

- The non-connectivity revenues have demonstrated impressive growth in the past 4 years.

- Non-connectivity revenue grew 21.5% in H1 2022 (YOY) compared to 7.5% overall revenue growth (Analysis of 25 telcos)

- 8 telcos have non-connectivity accounting for more than 20% of the total business. These telcos belong to China, South Korea, Singapore & Taiwan.

- Taiwan Mobile yet again achieved the highest contribution of non-connectivity revenues to the total business.

#2 South Korean operators ace the content and media segment

- The media business accounts for an average of 10.5% of total revenue for the top 3 South Korean telcos (refer to figure 4).

Exhibit 3

Percent of media revenue to total for South Korean operators

| Telco | Content & media revenue (KRW billion) | Total revenue (KRW billion) | % of content & media to total revenues |

| KT Corp | 966 | 9,126 | 10.6 |

| SK Telecom | 938 | 8,567 | 10.9 |

| LG U+ | 660 | 6,762 | 9.8 |

| Total | 2,564 | 24,455 | 10.5 |

- IPTV is the key driver for growth in the media segment.

- The upgraded broadband infrastructure in the market has fuelled the adoption of multiplay packages inclusive of IPTV. This helped improve the ARPU for the telcos.

- KT Corp’s lead in the media and content business is attributed to its monopoly in the DTH segment and strong position in the IPTV segment

- twimbit recognised SK Telecom as the Best telco to ace “Content & Media”. Read this article here

#3 China Mobile noted the highest improvement in % of non-connectivity revenue to total in H1 2022

- The non-connectivity revenues for China Mobile accounted for 15.6% of total in H1 2021. It has now grown to 19.7% of total in H1 2022, a 4.1% jump, the highest in the region.

- It also added the highest new non-connectivity revenue of US$ 4.3 billion. Today, it also has one of the largest enterprise business in terms of revenue in the Asia Pacific region.

- The success in enterprise is attributed largely to the 93.9% growth in Industry cloud revenues reaching US$ 2.8 billion. The operator has a rich portfolio of offerings in this segment that include

- 210+ types of self-developed IAAS, PAAS & SAAS products

- 2300+ types of SAAS products from partners

- China Mobile has cumulatively signed 11,000+ agreements related to 5G industry commercial projects to date.

- twimbit recently recognised China Mobile as the best telco to ace “Enterprise Business”.

#4 Taiwan Mobile reach a new high of 61.9% revenue coming from non-connectivity services

- This high percentage of revenues from non-connectivity services is unmatched in the region. The contribution to overall revenue from its e-commerce segment, momo, continued to increase and reached at 59.2% in H1 2022, while the segment grew by 18.3%. The remaining 2.7% of non-connectivity portion comes from media business (Pay TV & channel leasing)

- momo invested in logistics and 20% of deliveries were done by in-house fleet. It expanded the total warehouse space by 25% in Q2 2022

twimbit takeaways

- The telcos have enjoyed the most success from media and content business. This is the closest adjacency for the service providers. A strong market for local language content, supported by investment from telcos to produce local content has been a key driver for success.

- Telcos are strengthening their enterprise propositions for vertical industries via 5G. It is a must-win segment for monetizing 5G, and the Chinese telcos have showcased tremendous progress in this area.

- Only a handful of telcos have been successful in winning business in the e-commerce segment. Taiwan Mobile, SK Telecom (spun off to form a separate subsidiary) and SoftBank are the three major telcos in the region who succeeded in establishing the e-commerce business.

- Telcos are beginning to make inroads into financial services, gaming and OTT services as they expand their portfolio of non-connectivity services.