Maybank, the leading bank in Malaysia, operates more than 2000 branches worldwide, with services available for customers in 18 countries. The bank’s presence spans 10 ASEAN countries, with Malaysia, Singapore and Indonesia being the home markets and is also present in London, New York, Hong Kong, and Dubai.

Operational efficiency at Maybank

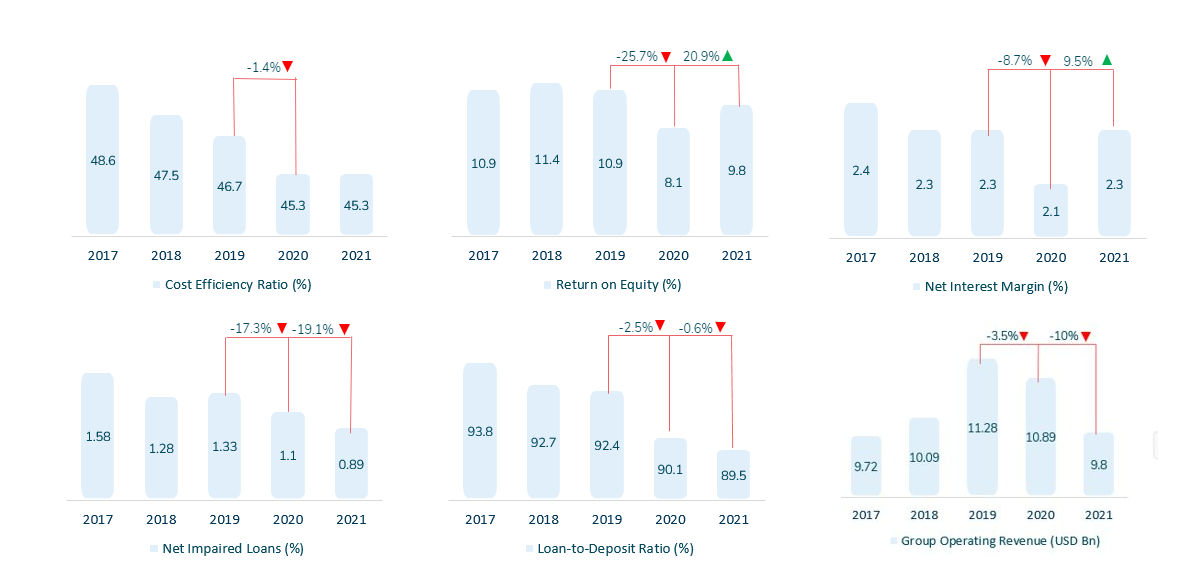

The improvement of Maybank and its asset quality marked the reduction of the Non-Performing Loan (NPL) rate by 33% from FY17 to FY21 (Figure 1). At the same time, the Loan-to-Deposit (LDR) ratio also declined by 3.13% during the same period. Ideally, the LDR ratio should be between 80% – 90%, and Maybank is on the upper end of the threshold. This threshold is maintained with the bank’s consistent Net Interest Margin (NIM). (Figure 1).

The bank has a strong focus toward reducing its cost-efficiency ratios and could attain a ratio of 46.7% in 2019 (Figure 1). Achieving a further decline, the cost-efficiency ratio is maintained at 45.3% for the past two years.

Strategic focus areas for Maybank

- #1 Customer experience

Maybank is delivering an exceptional customer experience in line with their M25 aspirations. The bank has deployed seamless payment solutions, implemented chatbots and Robo Advisors and upscaled business capabilities to provide a holistic customer journey.

- #2 Employee experience

From customised mental well-being outreach sessions to flexible working environments, Maybank has acted on various initiatives to enhance its employee experience. The bank launched top initiatives: MaybankCares Sustainability Platform and #LearningNeverStops.

- #3 New value drivers

The bank aspires to create new growth opportunities in the areas of Digital, SME, and Wealth, to build long-term competitive advantages. The bank introduced apps such as Maybank2uBiz and Tap2Phone to achieve this goal.

- #4 Sustainability

Maybank plans to mobilise RM 50 billion(USD 12.1 billion) in sustainable finance by 2025. Initiatives include

- Cashville Kidz – Financial literacy program targeted at school children ages 9 – 12

- R.I.S.E. – Coaching and mentoring programme to foster economic empowerment for disadvantaged communities

- Maybank Women Eco-weavers – Training on capacity-building and microfinancing for women weavers from marginalised communities

Digital strategy at Maybank

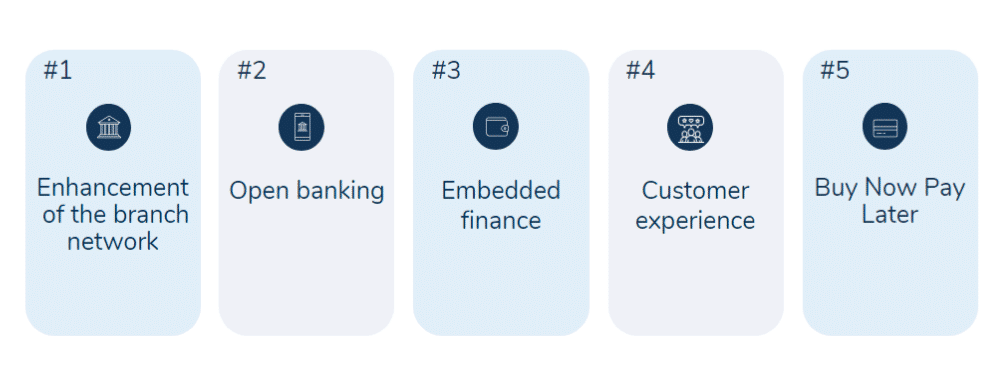

Maybank plans to deliver its digital strategy through the following (Figure 3).

Top 5 growth opportunities at Maybank

- #1 Enhancement of the branch network

Maybank spends USD 30 million in a year on branch operation and maintenance costs to manage 2617 branches. Simultaneously, the bank has executed these key initiatives:

- Redesigned self-service branches and kiosks to leverage solar power.

- Enhanced CX for business customers with 20 Business-Friendly branches (BFB). It also released Universal Banker (UB) program to train personnel to enhance the in-branch experience for them.

- Launched cardless ATM withdrawal using a QR code to reduce physical contact.

The bank can further focus on transforming branches into community hubs to boost social engagement and make the branches elderly-friendly for senior citizens unfamiliar with digital tools. It can also introduce tablet-based smart branches, to provide customers with a personalised “one-to-one” service experience.

- #2 Open banking

The bank launched “Maybank Sandbox” in 2017. The online portal consists of the following:

- 20 APIs (Application Programming Interfaces) for developers to browse and integrate APIs into their applications.

- A dashboard to provide users with an avenue to contribute ideas on potential new APIs to be added or identify bugs that need fixing.

As of date, Maybank has enabled 85 operations, making the bank Malaysia’s front-runner in open banking. Moving forward, the bank can further partner with third-party providers to enable them to embed banking products directly into their own offerings and establish itself as a BaaS provider. The bank can also partner with overseas players like WeChat and Naver Pay and can enable payment solutions for inbound tourists like LINE Pay in Japan

- #3 Embedded finance

Maybank has created a zero-commission online marketplace, “Sama-Sama Lokal”, that is integrated with the Maybank2u app, consisting of over 18,000 listed merchants.

- Supports local businesses by helping them establish their online presence.

- Provides automated delivery for orders and payments and a tracking function with real-time updates to customers.

As of date, Sama-Sama Lokal has generated approximately USD 4.5 million in order value. The bank can further focus on expanding into other marketplaces, such as home and property, considering the new Home2u digital home financing solution. It can also expand into the car and the travel marketplace based on the bank’s offerings in both the markets.

- #4 Customer experience

The bank has embraced digitalisation to enhance customer experience, introducing Maybank2u, Maybank wealth app, Maybank2e, and MAE lifestyle app by Maybank2u. However, while these apps are easily accessible, customers need to have a Maybank account to register for them. To help further ease the process, Maybank has executed these implementations as of date:

- Rolled out biometric technology to onboard new customers through the Maybank2u app

- Enabled cross-border CASA STP, which allows existing Maybank customers from Malaysia to open savings accounts digitally in Singapore

- Improved customer accessibility by introducing digital account opening through Maybank2u for Mudarabah Investment Account Zest-I

Currently, opening a Maybank account is a simple, digital process enabled by an e-KYC solution. Yet, activating accounts can take up to 45 mins compared to CIMB’s 17 mins account activation. This delay can be a hassle for customers. The best in class account opening account opening process is completed in <2 minutes by DBS in APAC. Banks like Bendigo and ICICI also take 3-5 minutes for the process. Therefore, the bank should focus on making the onboarding process easier and move towards creating a super-integrated application with all the features from these different applications, thus simplifying customer journeys and increasing the customer base in the process.

- #5 Buy Now Pay Later

“EzyPay” is the bank’s most recent BNPL (Buy Now Pay Later) offering in the market that allows most Maybank and Maybank Islamic credit card holders to split payments of more than USD 241 into interest-free loans for up to 12 months. Maybank introduced the BNPL offering because it aims to;

- Ease the burden of purchasing big ticket items with instalments as low as USD 20.

- Allow customers to apply for an EzyPay loan online via Maybank2u or the Maybank app.

Moving forward, Maybank should focus on using AI (Artificial Intelligence) technology to identify suitable customers and preemptively provide them with BNPL offerings to increase the attachment rates. In addition, the bank should also provide active lucrative offers from their merchants to retain existing customers. It can also tap into the Gen Z market with targeted BNPL offerings to encourage them to become Maybank customers in the long run.

Conclusion

Digital advancements, converging industries, fusing technologies and the increase in linked ecosystems mark the banking industry redefining itself in the modern digital transformation era. While this change enables them to identify new ways to generate value for their stakeholders, the top priority for Maybank is to always focus on making the digital experience seamless. And according to our analysis, Maybank is heading towards a secure digital future that supports end-to-end customer journeys with its digital roadmap.