Executive summary

Indian neobanks are growing at a CAGR of 43%, fastest in the Asia Pacific. Today, India has nearly 36 neobanks, including payment banks. Neobanks create a significant revenue growth opportunity for the banking and financial services (BFSI) industry, especially with the sponsored license partnership model between the incumbent and the neobank. It creates a clear shared responsibility between the two, the regulatory compliance responsibility is tied to the sponsored banking license partner and customer acquisition via product innovation is led by the neobank.

Product innovation for neobanks spearheaded from frictionless customer onboarding journeys. Today, it is no longer enough. Neobanks have to build experiences that stimulates the emotional being of the customer and establish an everyday relationship with them. It is vital to embed into customers’ everyday life to have a futuristic vision and empathy for their needs.

Our report outlines the best practices from the 6 top retail-focused neobanks in India that ace product innovation. We want to help and better guide Chief Executive Officers (CEO), Chief Product Officers (CPO), business unit leaders, and investors of existing and upcoming neobanks on the importance of product innovation in driving long-term growth.

Methodology

The objective is to benchmark and identify India’s top retail neobanks at the peak of building innovative products and services based on their customers’ journey.

After reviewing the product suite of over 88 neobanks across APAC (Product stack benchmark for APAC top 10 retail neobanks), we developed six product categories and customised them for the Indian context.

Each product category has a different weight on the overall analysis, which further segments into distinct sub-attributes.

*Sub-parameters have pre-defined scaling for better distinction between the neobank’s products and services.

Step 1: We shortlisted the 6 operational retail neobanks from the 36 neobanks in India (India, the new hub of neobanks 2.0).

One out of 6 retail neobanks in our study is a payment bank (Airtel Payments Bank). Other three payments banks – India Post Payments Bank Limited, Fino Payments Bank Limited, Paytm Payments Bank Limited have recently been granted license of Scheduled Commercial Bank (SCB’s). Hence we have not included above three mentioned neobanks in our study.

Step 2: We developed an informed perspective through the company websites, social and community channels, and published anecdotes.

Step 3: We evaluated our neobanks across 6 product categories and 30 sub-parameters on a scale of 1 to 5, measuring their product uniqueness and hyper-personalised approach to come up with our leaders. (Table 1)

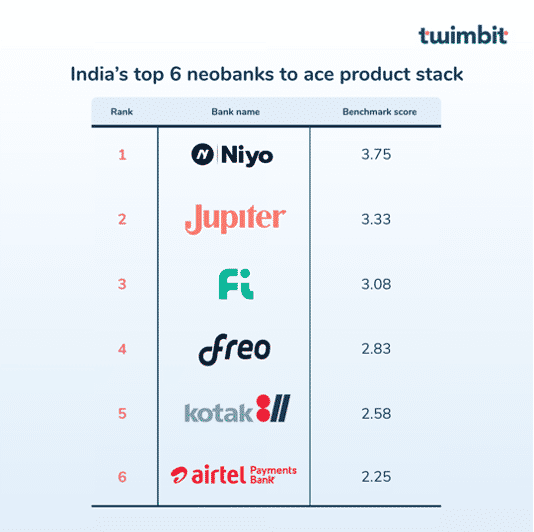

Step 4: We ranked the top 6 retail neobanks (Table 2) based on the above 6 product categories.

*Research Caveat: Limited to secondary sources and publicly declared information by the companies

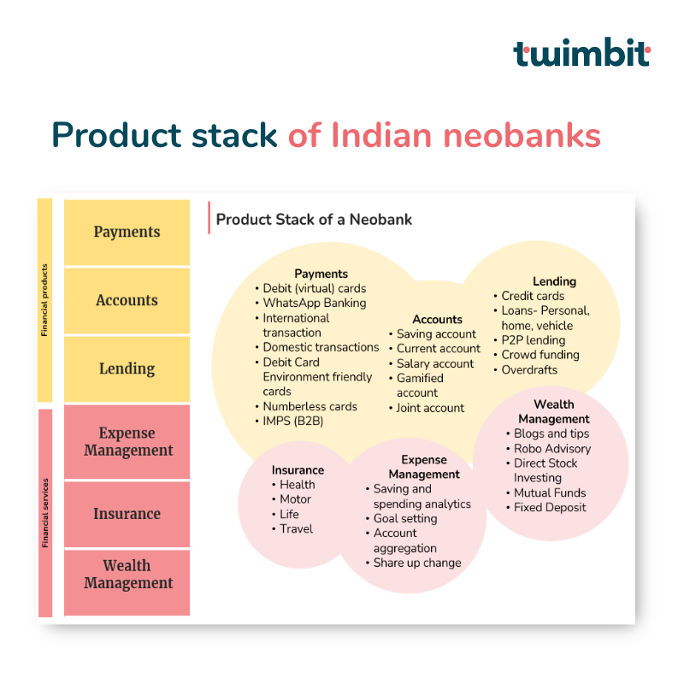

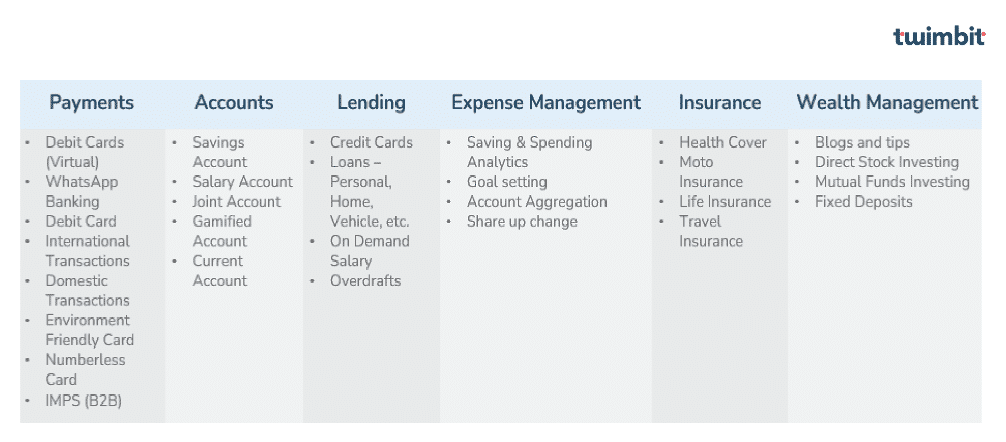

Best practice analysis for each product category

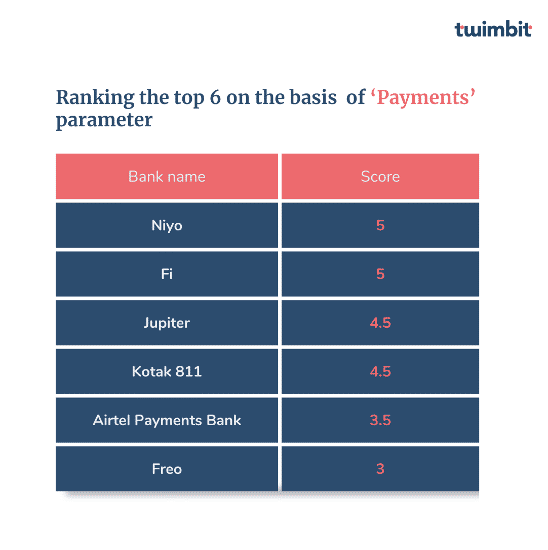

#1 Payments

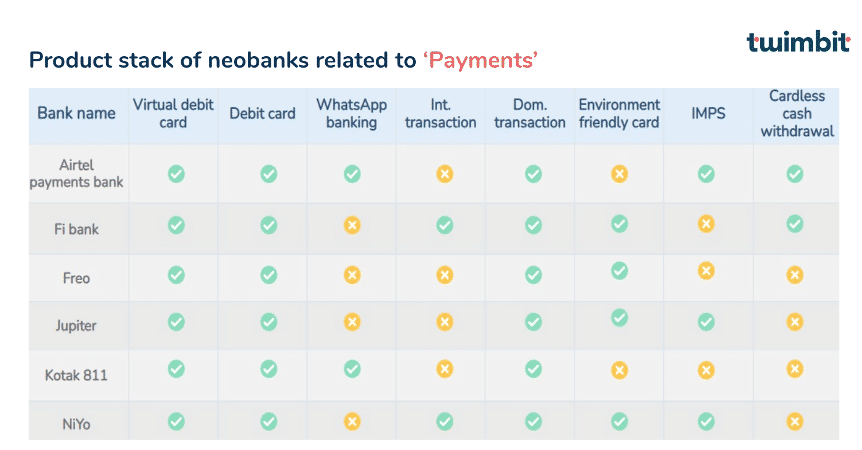

We analysed ‘Payments’ based on 9 sub-parameters, including the availability of virtual debit cards, WhatsApp banking, and international transactions (See Table 3). While analysing the table below, we observed the following key insights:

Key insights:

- All neobanks provide a virtual and a physical debit card.

- Only Airtel Payments Bank & Kotak 811 provide an option for WhatsApp banking.

- FI and NiYo provide an option for international transactions where NiYo offers a zero-forex markup card.

- All neobanks provide an option to make P2P payments.

- NiYo leads in security by providing numberless cards.

- 4/6 neobanks offer environment-friendly cards.

- 3/6 neobanks offer IMPS services.

- NiYo and Fi Bank are top scorers in payments, with a benchmark score of 5/5 (see table 4).

Analyst tip:

Neobanks can ramp up their capabilities to enable payments through voice, touch, and gestures using multi-experience platforms that securely operate multiple modalities.

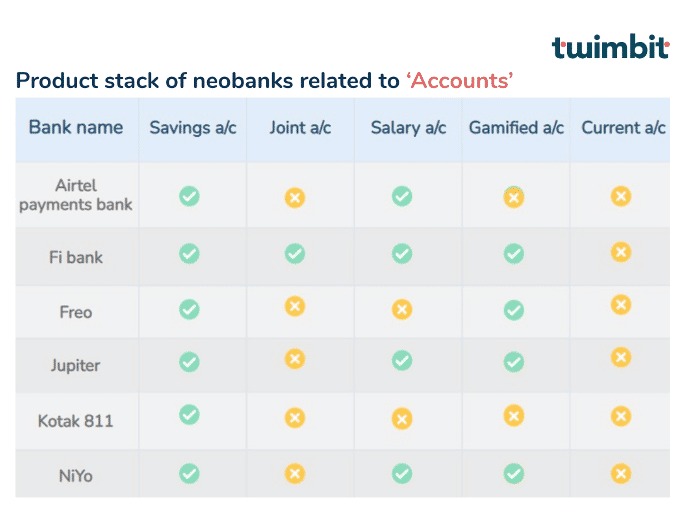

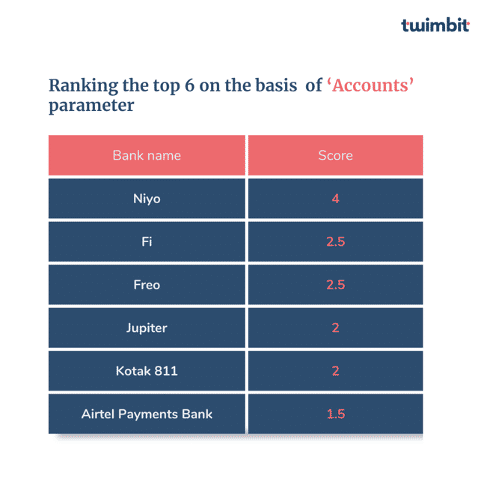

#2 Accounts

We analysed ‘Accounts’ based on level of differentiation in the types of a/c (refer to table 5).

Key insights:

- All the neobanks offer a savings account as a product.

- Only Fi bank offers joint a/c.

- 4/6 neobanks provide a salary account.

- 4/6 neobanks provide a gamified experience while using account-related services.

- NiYo aces ‘Accounts’ parameter with a score of 4 with its hyper-personalised and unique product offerings related to accounts whereas Fi leads in offering maximum number of different types of accounts. (refer table 6)

Analyst tip:

Neobanks must diversify their product stack in terms of offering different types of accounts to serve better as a one-stop solution. For instance, recreating the concept of joint bank account, by allowing couples to share their finances, set up budget goals, create milestones, track the progress of financial targets and pool their money together intelligently.

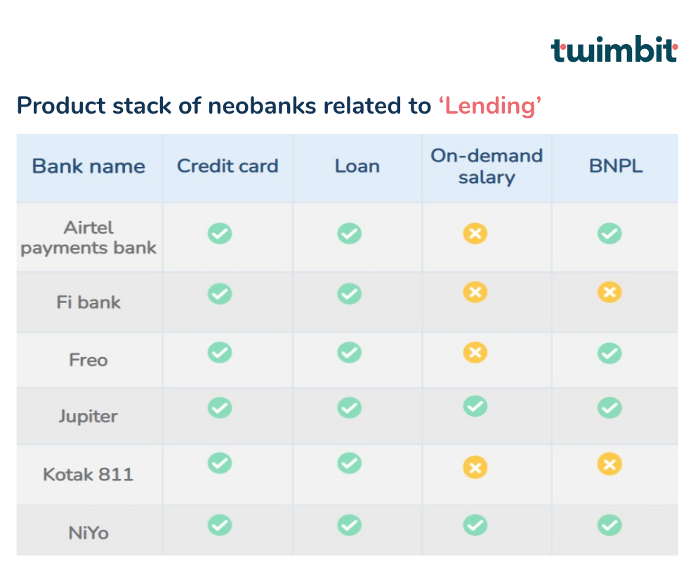

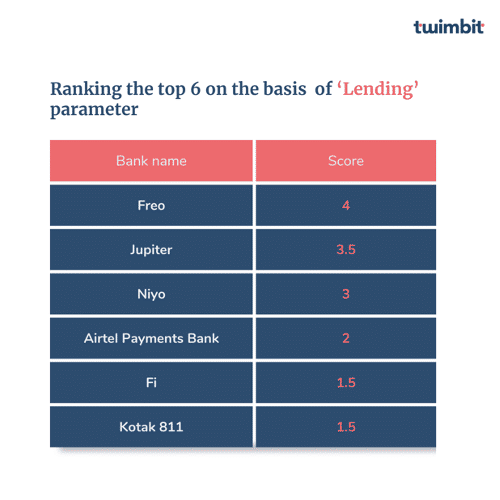

#3 Lending

We analysed the ‘Lending’ parameter based on four sub-parameters – the availability of credit cards, loans, on-demand salary and BNPL (see Table 7).

Key insights:

- All neobanks offer a credit card.

- All neobanks provide at least one type of loan (home loan, car loan, personal loan) to their customers.

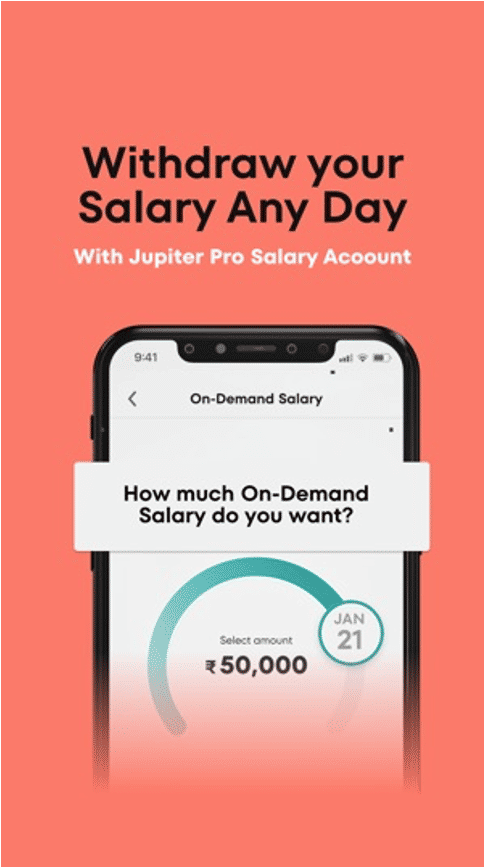

- Jupiter and Niyo are the only neobanks offering the ‘On Demand Salary’ option.

- 4/6 neobanks offer BNPL services.

- Freo leads ‘Lending’ with a score of 4 (refer to table 8).

Analyst tip:

With only a few neobanks offering lending products, neobanks have a vast untapped market and a pool of opportunities to stand out and lead from the front.

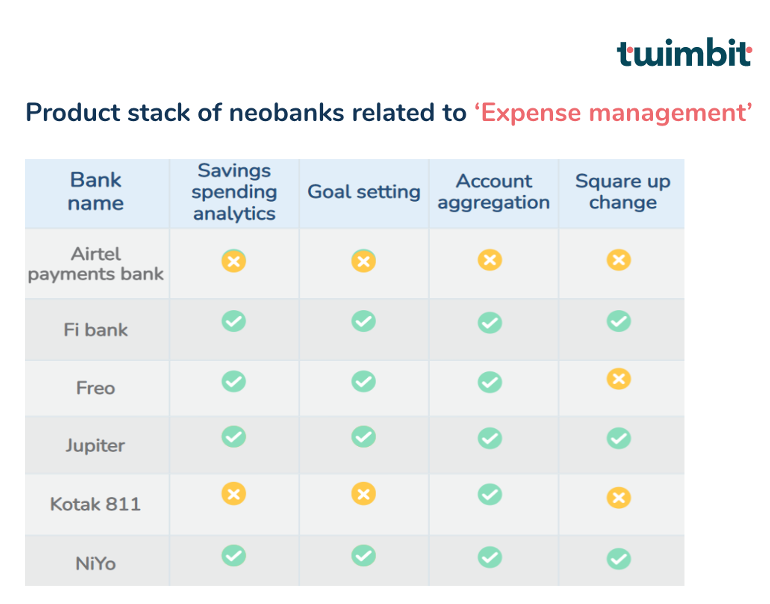

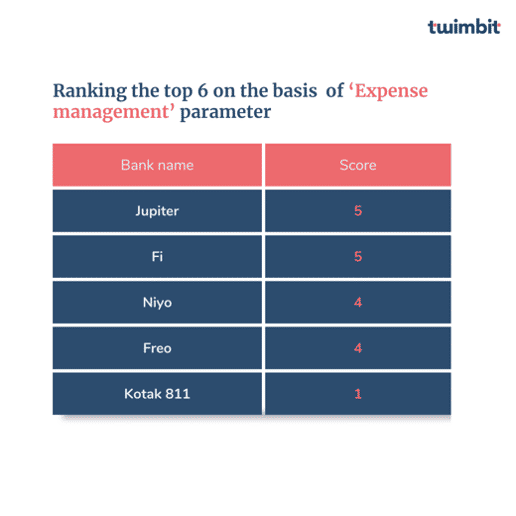

#4 Expense Management

We analysed the ‘Expense Management’ parameter based on four sub-parameters – the availability of saving spending analytics, goal setting, account aggregation, and share-up change.

Key insights:

- Airtel Payments Bank does not provide any expense management-related products.

- 3/6 neobanks provide “share-up change” as a product.

- Account Aggregation is an option made available by all the neobanks except Airtel payments bank.

- 4/6 neobanks allow their customers to access saving and spending-related analytics and provide an option for goal setting.

- Jupiter and Fi Bank ace the “expense management” parameter with a score of 5/5.

Analyst tip:

- Fi and Jupiter’s account aggregation feature allow users to sync multiple bank accounts.

- Providing ‘saving and spending’ analytics is a common product. Gamifying the experience with rewards, challenges, and community activities elevates the customer experience.

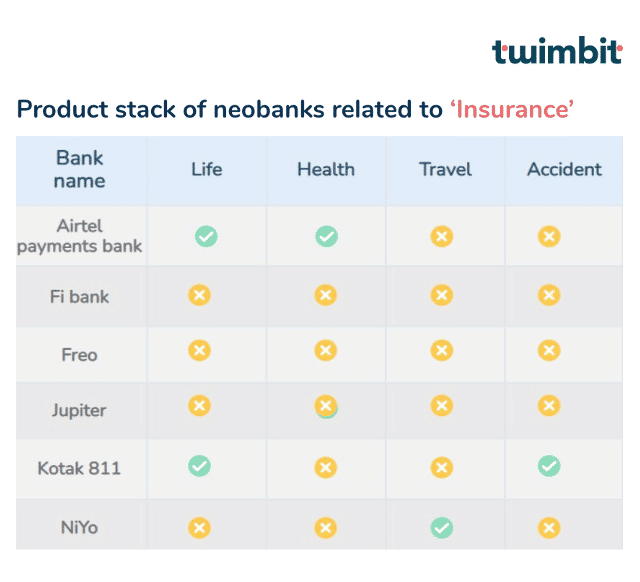

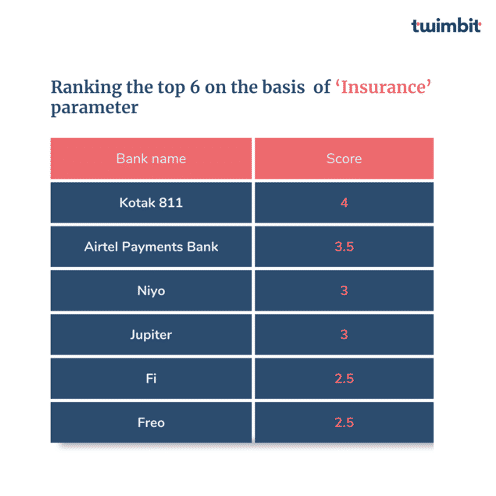

#5 Insurance

We analysed the ‘Insurance’ parameter based on various sub-parameters, including the availability of a type of insurance plan.

Key insights:

- Fi Bank and Freo don’t provide any insurance except for deposit insurance.

- Only Kotak 811 provides accident insurance.

- NiYo is the only neobank that includes travel insurance.

- Only Kotak 811 takes the initiative to educate its customers about insurance and provide insurance, i.e., health coverage.

- Kotak 811 ace the ‘Insurance’ parameter by scoring 4/5.

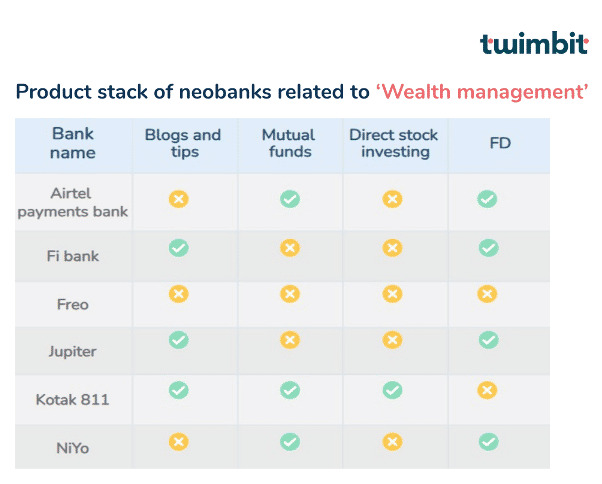

#6 Wealth Management

We analysed the ‘Wealth management’ parameter based on four sub-parameters, including the availability of blogs and tips and investment management.

Blogs and Tips: Financially educate consumers on investment-related products and wealth management via social media.

Investment Management: Providing the customers with a platform to make investment(s)* and managing them across assets.

*Investing in assets other than Fixed Deposit (already covered under expense management) – Mutual Funds, Direct Equity, Gold, Real Estate, ETFs, etc.

Key insights:

- Freo does not offer products under the wealth management parameter.

- 3/6 neobanks work towards the financial education of their customers via blogs and other platforms.

- Kotak 811 is the only neobank providing an option to invest directly in individual stocks.

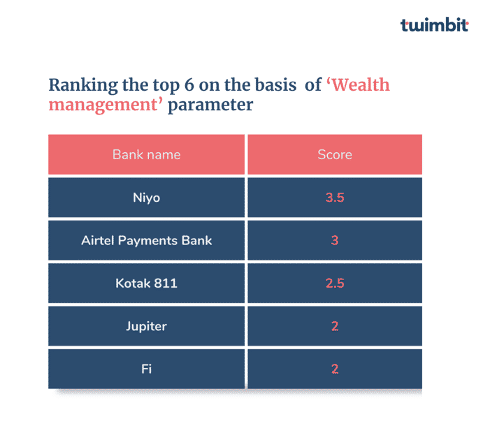

- NiYo leads the ‘wealth management’ parameter with a score of 3.5 (refer to table 14).

Analyst tip:

Currently, very few neobanks offer ‘Wealth Management’ related products. Adopting a key product, such as the Robo-Advisory, is extremely slow in the Indian neobanking. Neobanks need to focus on helping customers automate their investment and advisory process. The tool can be used to create micro-investing opportunities by integrating third-party products.

Way Forward:

3 life-centric strategies to drive growth

- Gain a profound understanding of customers

A serious shift from seeing people as “buyers” with static personas to seeing people as multi-dimensional by using dynamic data to personalize connections and monitoring life forces that affects them.

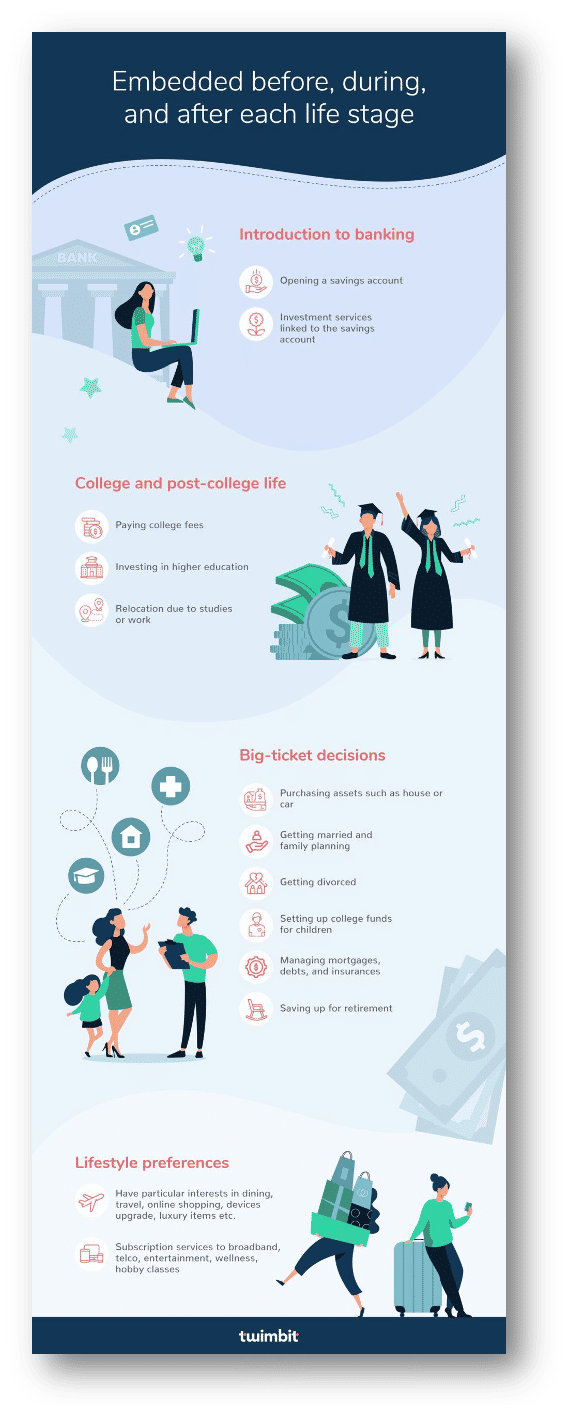

Neobanks can unlock a human insight advantage for better understanding of users’ needs across products and services and having a more meaningful role in customers’ lives, now and in the future. The neobanks have to embed themselves in their customers’ lives by identifying their demands and needs at every stage of their life. (Figure 2). Defining the customer journey help neobanks to gain insights into the customers’ usage, spending patterns, and major pain points to deliver an engaging banking experience.

embed themselves

- Broaden your canvas for value creation

A shift from partnership with third party related fintech services to marketplace banking model with ecosystem of aggregated products and services addressing specific customer needs in mind. Hyper-personalisation plays a significant role in driving customer acquisition and engagement.

For eg., Jupiter can collabarote with ACKO insurance or Zerodha insurance to offer different insurance services or it can also partner with for eg. Makemytrip to create a one-stop travel marketplace.

Marketplace banking are fast becoming an invaluable business model. DBS marketplace is a great example of integrating third-party solutions. It has launched six consumer needs-driven banking marketplaces DBS travel, DBS car, DBS health, DBS property, DBS home & living etc.

Neobanks must play to their strengths and orchestrate an all-in-one platform that embeds financial, lifestyle, travel, education, and healthcare solutions to be profitable and sustainable. These value-added services will help them expand their portfolio and acquire more customers, ultimately generating more income.

- Design a delightful experience continuum

A shift from overcomplicated, underperforming experiences that fail to satisfy customers to thoughtful and easier connected solutions for a simpler and engaging experience. This can be done by eliminating frictions from the mobile application, evaluating customer experience across journeys like customer onboarding. Moreover, neobanks needs to maintain a continuing experience advantage by unifying a person’s entire banking activity into a single, delightful platform with synchronicity across media.

With incumbents stepping up to the plate, the pressure is red hot for neobanks to constantly innovate to survive in the market. Neobanks must continuously leverage data to deliver hyper-personalised lifestyle-based solutions for the millennials and Gen-Z, the majority of their customer base.