The Commonwealth Bank of Australia (CBA) is headquartered at Sussex Street, Sydney, New South Wales and is among the ‘big four’ banks along with ANZ, NAB and Westpac in the Australian market. The primary markets for the banks are Australia and New Zealand, with a significant presence in the United States and the United Kingdom. CBA has a network of 807 branches operating across eight countries, providing banking services, funds management, superannuation, insurance, investment and broking services.

Financial highlights

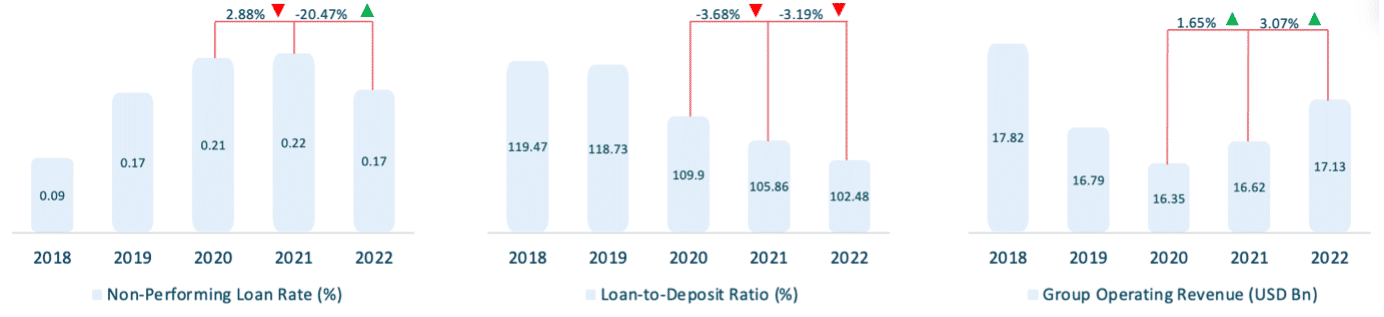

CBA’s asset quality improved post-pandemic, with its non-performing loan (NPL) rate witnessing a significant decrease of 20.47% between FY2021 and FY2022 (Figure 1). Although CBA’s loan-to-deposit ratio (LDR) has been historically high compared to banks in other regions (Figure 1), the LDR has constantly been declining for the past five years. It fell by 3.19% between FY2021 and FY2022.

An ideal LDR for any bank should be between 80% – 90%, and the decline might indicate CBA is trying to get the ratio within the ideal range. However, such a high LDR implies insufficient liquidity to cover potential and unforeseen fund requirements.

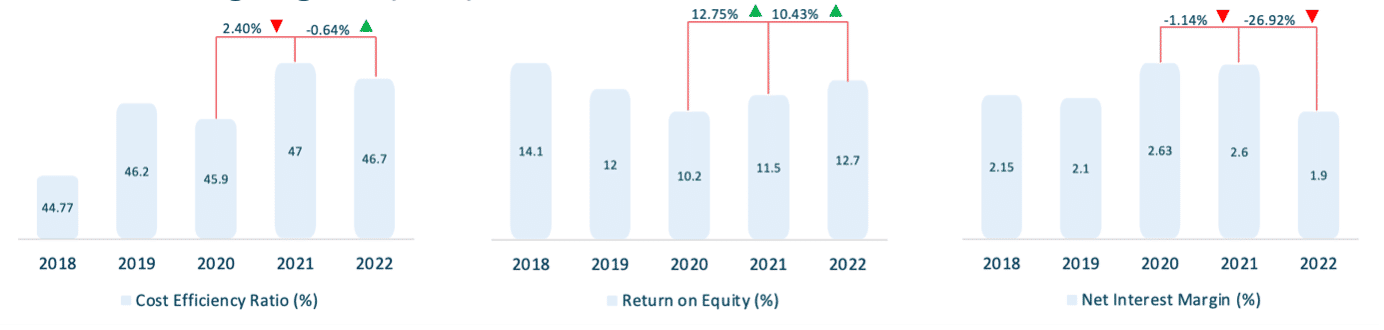

Generally, banks have a target cost-efficiency (CE) ratio of 50%. Yet, as reported, many banks are struggling to meet this threshold. A lower cost-efficiency ratio indicates the profitability of the bank. Therefore, the lower the number, the more profit the bank generates and vice-versa. Following this rule, CBA’s cost-efficiency ratio has increased in the past few years (Figure 2), with the bank now maintaining the ratio within the threshold, implying CBA’s efficient operations.

Despite having such a high LDR, the net interest margin (NIM) declined between FY202 and FY2022. This decline can be due to less interest received on loans or more interest being paid out on deposits. The former could be true since banks have provided relief aid during the COVID-19 pandemic to customers through lower interest rates on their existing loans.

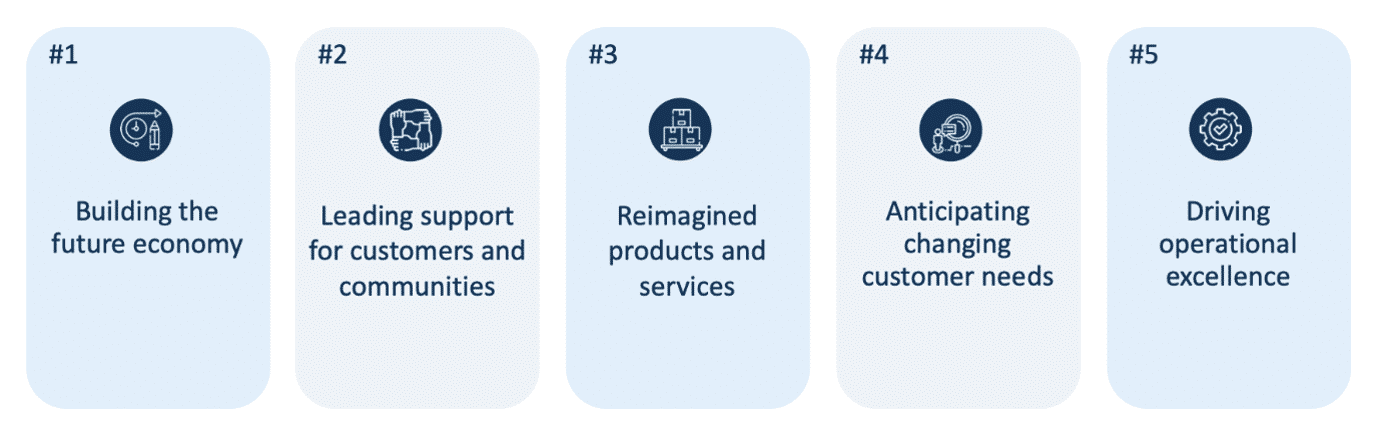

Strategic focus areas

- #1 Building the future economy

CBA helps its customers transition to a more modern, resilient, and sustainable economy while striving to reduce carbon emissions. Thus, the bank is working hard on new ways, linking them with green financing to reduce the overall carbon footprint.

- Offering institutional customers sustainability-linked loans and facilitating Environmental, Social and Governance (ESG) bonds.

- Developing new products and services that support retail customers to reduce and offset their carbon emissions while saving costs on renewable energy.

- #2 Leading support for customers and communities

CBA ensures all individuals and businesses have access to financial products and services that meet their needs to help them make better financial decisions.

- Developed an artificial intelligence (AI) powered tool called the customer engagement engine, which uses data analytics to proactively identify and offer financial assistance to customers in need. Since its inception, the bank has helped more than 1.6 million flood-affected customers in Queensland and New South Wales.

- Developed a benefits finder tool within its app to help customers find unclaimed benefits and rebates. Since its launch, the tool has initiated over two million claims and alerted 4.7 million customers about government benefits and rebates during FY2021 alone.

- #3 Reimagined products and services

CBA creates a more differentiated proposition for retail and business customers by driving product innovation and building new ventures and partnerships.

- CommSec Pocket – Helped customers invest more than 1.3 billion dollars. The app enables customers to start with as little as USD 50, gradually building their portfolio over time to achieve their larger financial goals.

- CommBank Smart Health – Allows medical practitioners to save time and administration while improving the customer payment experience. The service can be availed through the bank’s smart EFTPOS terminals and used for payments and claims processing.

- Unloan – The mobile-first digital home loan platform provides customers with low-rate and no-fee loans, processed in as little as ten minutes, by reducing complexities associated with traditional lending options.

- #4 Anticipating changing customer needs

CBA leverages data analytics and AI to gain a comprehensive understanding of how to better anticipate customer needs now and into the future.

- CommBank Yello rewards existing customers with personalised benefits and offers, which include discounts and cashback based on their tenure with the bank and the products and services they use.

- Money Plan helps customers manage their finances, from planning categorical budgets to managing their bill payments and setting savings goals.

- #5 Driving operational excellence

Auto-decisioning in the home loan process has significantly reduced friction, creating a seamless customer experience. This is because it auto-decisions 60% of the proprietary home loan application.

CBA is also disinvesting in projects which no longer align with the bank’s organisational strategy and has started a disciplined capital management plan. Since the beginning of the plan in 2018, the bank has generated 11 billion dollars in capital from disinvestment.

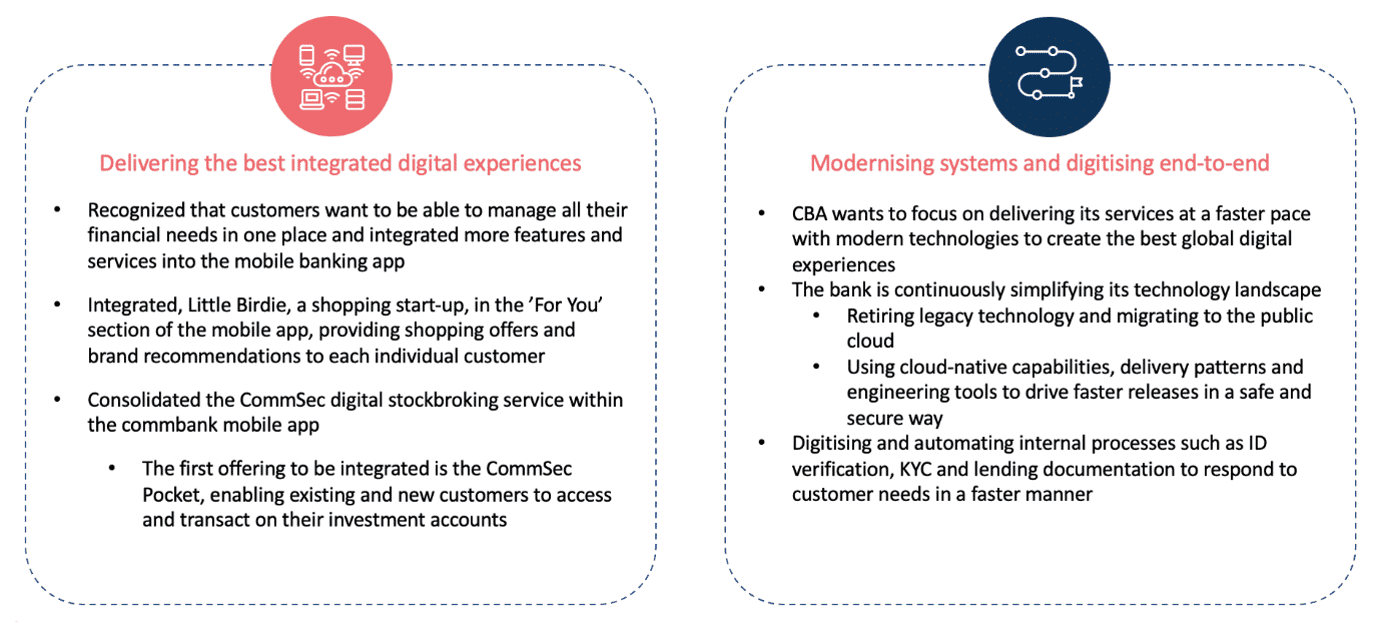

CBA’s digital strategy

CBA plans to deliver its digital strategy through the following (Figure 4).

CBA’s technology innovations

CBA is always trying to develop new offerings that can enhance the customer experience through all the banking touchpoints, helping customers in their day-to-day transactions (Figure 5).

- #1 Bill Sense

Establishing budgets for the upcoming month can get stressful at times. This is why ‘Bill Sense’ is here, alleviating the customers’ stress and helping them to predict their upcoming payments. The tools in the mobile app can predict upcoming payments up to twelve months in advance using spending behaviours and past transactions of the customer.

- #2 StepPay

Buy Now Pay Later (BNPL) is all the rage today, and CBA is the first major Australian bank to get on top of this trend, creating StepPay, its BNPL service. To date, it is currently available to more than four million customers. Customers can use this facility with an initially approved limit of AUD 1000 (USD 667) anywhere the bank’s card is accepted and can make repayments in four equal instalments at intervals of four fortnights.

- #3 Smart EFTPOS terminals

Payment terminals are nothing new and have been in use for a long time. However, CBA has equipped their terminals with enhanced connectivity options, from dual SIM functionality to Wi-Fi and broadband connectivity. In addition, the device has inbuilt features like split payments, adding surcharging, tipping, and emailing receipts. This makes CBA’s smart EFTPOS terminals new, more advanced and future-ready.

- #4 Cheddar

Cheddar is a brand and deals discovery app launched by the bank’s venture scaling arm, x15ventures. The platform was built with Gen Z and millennials in mind. Currently, the platform has over 600 merchants listed. It uses artificial intelligence and data analytics to offer customers personalised brands, authentic content and deals and reward them for their purchases in the form of cashback.

CBA’s digital partnerships

4 growth opportunities for CBA

- #1 Enhancement of the branch network

People in flood-affected areas, Lismore in New South Wales and Gympie in Queensland, have always struggled to access their financial services without interruptions.

Pop-up branches fix the issue, with CBA even instating technology hubs in partnership with universities across Adelaide and Melbourne. And on top of that, the bank plans to expand further, developing more tech hubs across Australia to support career development and innovation. At the same time, the bank should also care about the little guys, offering personalised support to customers and small business owners with their individual needs.

Further, the bank should consolidate low-footfall branches into CX labs to help with customer journeys by delivering an omnichannel experience and holding sessions to educate customers on how to use the bank’s digital services.

- #2 Cost to serve

As CBA began to optimise its branch and ATM networks, many expected a drop, particularly in its occupancy expenses. However, not many would have expected a significant drop of 16% between FY2021 and FY2022, with CBA cutting off 68 branches and 395 ATMs. Although this led to optimisation, wage inflation increased staff expenses by 9% during this period, with a 6.2% increase in staff.

Meanwhile, low-yielding liquid assets and lower home loan margins create investment inefficiencies, severely deteriorating the bank’s net interest margins, and reducing them by 8.65% between FY2021 and FY2022.

Improvements in the NIM can be achieved by increasing fee and commission income which currently stands at just 9.27% of the total operating income.

And despite an LDR of over 100%, it appears that CBA cannot seem to catch a break regarding its NIM, as it is still decreasing. The increase in deposits at the bank stood at 11.90%, whereas the loans only increased by 8.32%. Therefore, the next step for the bank is to disburse more loans to offset the higher increase in the deposits and increase their LDR, thereby improving the NIM.

- #3 Partnership Ecosystem

CBA has partnered with various organisations to offer more incorporated services to its customer. These include partnering with;

- More to offer a National Broadband Network (NBN) plan for three years to customers eligible for pre-approved home loans

- CoGo helps customers understand their emissions and offset their previous month’s transactions by purchasing carbon credits

- CSIRO (Commonwealth Scientific and Industrial Research Organisation) limiting global warming to 1.5 degrees Celsius

The next step for CBA is to support end-to-end customer journeys through partnerships with third-party providers. The bank can do this by:

- Helping pre-approved home loan applicants find potential properties they can purchase

- Suggesting products and services to customers as and when they require them based on information accumulated using machine learning, AI and spending behaviours and patterns

- Partnering with marketplaces to supplement its core value propositions by offering products and services which are sourced from financial and non-financial third-party providers

- #4 Blockchain

CBA forged a partnership with the largest regulated crypto exchange in the world, Gemini, and the leading blockchain analysis firm, Chainalysis, to breach the crypto market. Integrating the service into its existing mobile banking app, the bank excites its customer base of more than eight million app users to buy, sell and trade in ten selected crypto assets, including Bitcoin, Ethereum and more.

The World Bank was also offered a helping hand, with CBA activating its first blockchain-operated debt instrument, ‘bond-i’. The bank built and developed the platform through its Blockchain Centre of Excellence over the Ethereum network. CBA is the sole arranger for the bond helping World Bank raise USD 81 million.

Finally, CBA established a blockchain market in partnership with BioDiversity Solutions Australia to offer digital tokens. This partnership will also help facilitate the trading of biodiversity credits for the New South Wales Government’s Offset Scheme, which requires developers to obtain credits to offset the impact of their development.

Moving forward, CBA should aim to establish its blockchain and explore ways Distributed Ledger Technology (DLT) can help the bank accelerate the rate at which it transacts business. Focusing on these steps can help the bank efficiently facilitate cross-border payments and transactions, leading to a smooth and seamless customer experience.

Conclusion

CBA is doing a lot in areas that can improve the customer experience and provide customers with a seamless experience across all banking touchpoints. The bank is also enhancing its work ethic to make it an enjoyable place for its employees. The bank is also exploring new opportunities like BNPL to serve its customers more flexibly. Cost and branch optimisation are some areas where the bank can improve to provide a much better experience to its customers and employees.