Being one of the four largest banks in Australia, National Australia Bank (NAB) supports its customers with 35,000 employees across 714 branches. The bank primarily operates across Australia and New Zealand while possessing branches in China, Japan, Hong Kong, the United States, Singapore, and the United Kingdom.

Operational efficiency at NAB

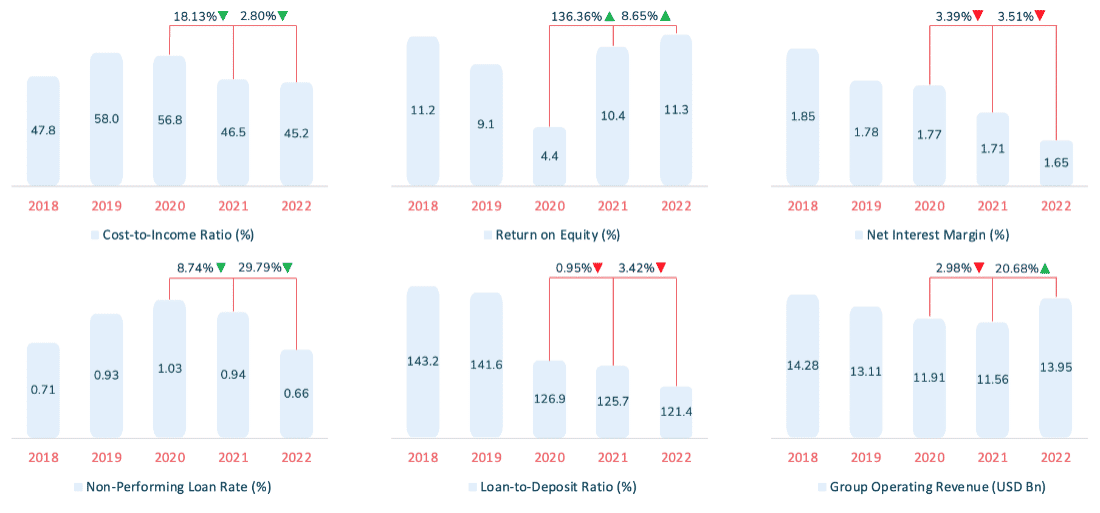

Operational efficiency has been on the mind of NAB, as reflected by its operating revenue and CIR (cost-to-income) ratio (Figure 1). The bank’s upward trend in ROE (return on equity) also reflects this, following its 2020 ROE of 4.4%.

On the other hand, higher interest rates in Australia have affected the NIM (Net Interest Margin), with NAB hitting a gradual low over the past five years. And despite the LDR (Loan-to-Deposit Ratio) being traditionally high, trends from FY2020 to FY2022 indicate that NAB is disbursing fewer loans than before.

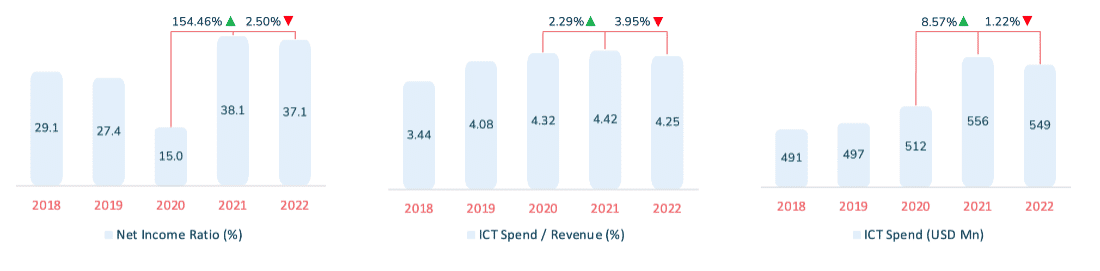

However, most importantly, the biggest strength from FY2018-FY2021 is the ICT spending, despite facing a slight decline in FY2022 (Figure 2). Regardless, the intent is clear – NAB is determined to enhance its technological capabilities.

NAB’s strategic focus areas

- #1 Simple and inclusive banking

With simplicity at the core of NAB, the bank has continuously worked to expand its self-serve features, such as making customer onboarding easier through enhanced electronic identification verification.

Inclusivity is also essential for a diverse customer base. With this in mind, NAB has worked on creating the following:

- ‘Language Loop’ – an interpreting service to support customers who are not native English speakers.

- ‘Walk Out Working’ – a session which ensures customers who visit a branch have a seamless first-time set-up while educating them on online banking security and fraud protection.

Furthermore, NAB has refreshed its Help Guides with step-by-step instructions and images. As a result, annual visits to these Guides have increased by 20% since the refresh.

- #2 Resilient technology and operations

In the past 12 months, NAB has enhanced its cyber security maturity by aligning with the Cyber Security Framework (CSF) developed by the NIST (National Institute of Standards and Technologies).

The bank has also strengthened security by simplifying the technology stack through decommissioning legacy platforms and accelerating cloud migration. As of writing, 70% of the bank’s services have migrated to the cloud. NAB’s cloud migration rate is currently close to 3 applications to the cloud per week.

- #3 Helping communities prosper

A prosperous community is vital for a brighter future. NAB realises this, contributing AUD 45.7 million (USD 31 million) in community investments, which includes monetary contributions, time through employee volunteering, and foregone revenue. The bank also provides grants of up to AUD 10,000 (USD 6,777) to fund community-led projects with long-term social and environmental impact.

Other efforts include the following:

- NAB Foundation – a registered charity by NAB that aims to catalyse social and environmental progress in Australia by helping purpose-led organisations find new and innovative ways to solve social and environmental problems.

- ‘Bank in a Box’ – a portable bank by NAB for residents to access cash and banking access with full access to digital banking capabilities, which the bank used in the 2022 Lismore floods.

- #4 Supporting employees

Customers and employees are the bank’s twin peaks. – Ross McEwan, CEO of NAB.

As such, NAB proactively engages with its workforce via quarterly Heartbeat surveys. These surveys enable employees to share what works well, what should continue and what needs improvement. And the feedback from the Heartbeat surveys helps NAB’s leaders develop and communicate targeted actions to address the needs of their teams.

Beyond this, NAB offers well-being programs to assist its employees when needed. Employees and their families can access counselling services through the Employee Assistance Program. The bank also supports employees affected by natural disasters through counselling, flexible leave options, and emergency grants.

Chatbots for bank customers are commonplace, but NAB has taken a step further by investing in a dedicated chatbot (NAB Bot) for employees. Employees can now access NAB Bot using the Teams app on their computers or mobile phones. The encouraging uptake of NAB Bot has enabled the bank to save AUD 1.2 million (USD 812,000) in support team costs.

NAB further intends to expand the use of chatbots to other areas of the business, including human resources and legal. To achieve this, NAB is working closely with Microsoft to build low-code chatbots.

- #5 Championing climate action

Climate change poses a significant problem for society to address. Answering the call to this issue, NAB has stepped up, becoming a member of the UN’s Net Zero Banking Alliance in December 2021. The bank also published its inaugural Climate Report in FY2022, which includes decarbonisation targets for 4 emissions-intensive sectors:

- Power generation

- Oil and gas

- Thermal coal mining

- Cement production

NAB has done its part to reduce its operational emissions significantly in FY2022. The operational Scope 1 and Scope 2 GHG emissions by 74% against a 30 June 2015 baseline. NAB also sources 72% of its electricity consumption from renewable energy.

Additionally, NAB has committed AUD 70.8 billion (USD 8 billion) in environmental financing since 2015, which has exceeded the bank’s target of AUD 70 billion (USD 47.4 billion) by 2025.

NAB also supports sustainable agribusiness by:

- Supporting over 300 agribusiness colleagues with climate training.

- Participating in research and forming partnerships with Climate Works Australia, Commonwealth Scientific and Industrial Research Organisation, Australian National University, and WWF.

- Assisting in product development by supporting farmers with tailored products.

NAB’s digital strategy

HLB plans to deliver its digital strategy through the following (Figure 4).

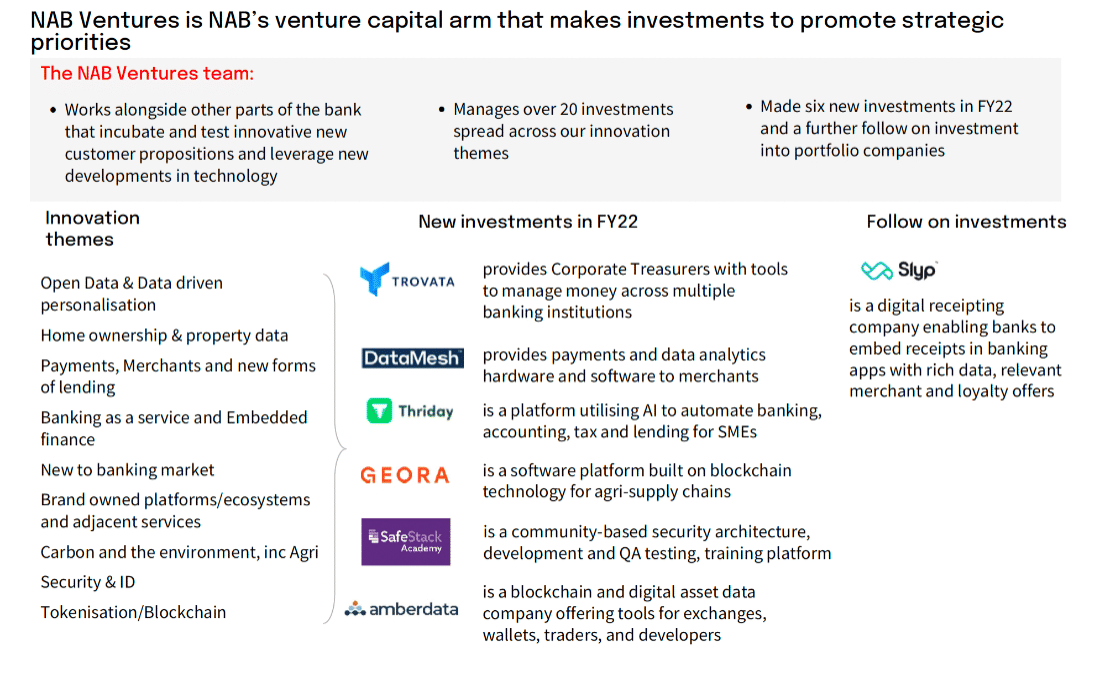

- #1 NAB Ventures

NAB Ventures is the bank’s in-house venture capital fund that supports entrepreneurs in and outside of Australia in their mission to build leading technology companies. It currently manages over 20 investments spread across the bank’s innovation themes. In FY2022, NAB Ventures made 6 new investments (Figure 5).

- #2 Optimising the digital experience

NAB experienced significant digital trends between FY2020-FY2022, most notably:

- >32% decline in over-the-counter transactions

- 23% decline in inbound calls

- 163% increase in chatbot interactions

Additionally, transaction accounts opened digitally increased from 33% in FY2021 to 40% in FY2022, while the use of cheques fell by 24%.

This change indicates the customers’ preference for going more digital. Hence, NAB is keeping up by enhancing digital self-service capabilities, such as:

- NAB Messaging – offers more personalised, continuous thread conversations to solve customer queries on the app and website.

- NAB app – allows customers to securely call the bank with integrated pre-authentication.

Customers can now lodge disputes regarding their card transactions online or on the NAB app at any time. Since its launch, customers have launched 74% of their disputes online.

- #3 NAB Hive

NAB Hive is a cloud-based digital merchant portal launched by NAB in 2022 in partnership with Pollinate, a UK-based Fintech.

The portal:

- Aims to offer a simpler, more flexible way for merchant customers to manage their business and payment needs via a single, easy-to-use portal

- Focuses on a digital end-to-end experience to provide more tailored human advice to small businesses on structuring loans or obtaining merchant payments or e-commerce facilities

- Allows retailers to see transactions in real-time and generate data on aspects such as the relative performance of stores and products and sales intensity based on the time of day

NAB’s technology innovation

- #1 NAB Easy Tap

NAB Easy Tap is an innovative app that turns a merchant’s Android phone into a terminal to accept contactless card payments (i.e., EFTPOS – electronic funds transfer at point of sale).

There are no set-up fees or terminal fees for this app. NAB Easy Tap also enables same-day settlement for NAB business accounts while ensuring the onboarding process is quick and easy. On average, the application is approved in minutes, and merchants are onboarded in 2 business days.

Another key feature of NAB Easy Tap is that it provides insights and analytics for merchants to better understand sales trends and the percentage of return customers based on real-time transaction and settlement data.

- #2 API ecosystem

NAB launched its API developer portal in 2016, and in the 6 years since, the bank has built an extensive portfolio of over 3,900 APIs spanning multiple categories:

- Foreign exchange

- ATM and branch locations

- Authentication

- Accounts

The bank encourages users to request access to its API database. Users can build, test, and learn with the bank’s APIs and test data upon approval.

- #3 NAB Now Pay Later

NAB Now Pay Later, a BNPL (Buy Now Pay Later) service offering from NAB, enables customers to split payments of up to AUD 1,000 into 4 fortnightly payments.

Key features of NAB Now Pay Later are:

- No late fees

- No interest

- No account fees

- No minimum purchase amount

- Virtual card with a revolving security number (CVV)

Customers can activate NAB Now Pay Later through the NAB App, after which the bank performs a credit check to assess the customer’s eligibility.

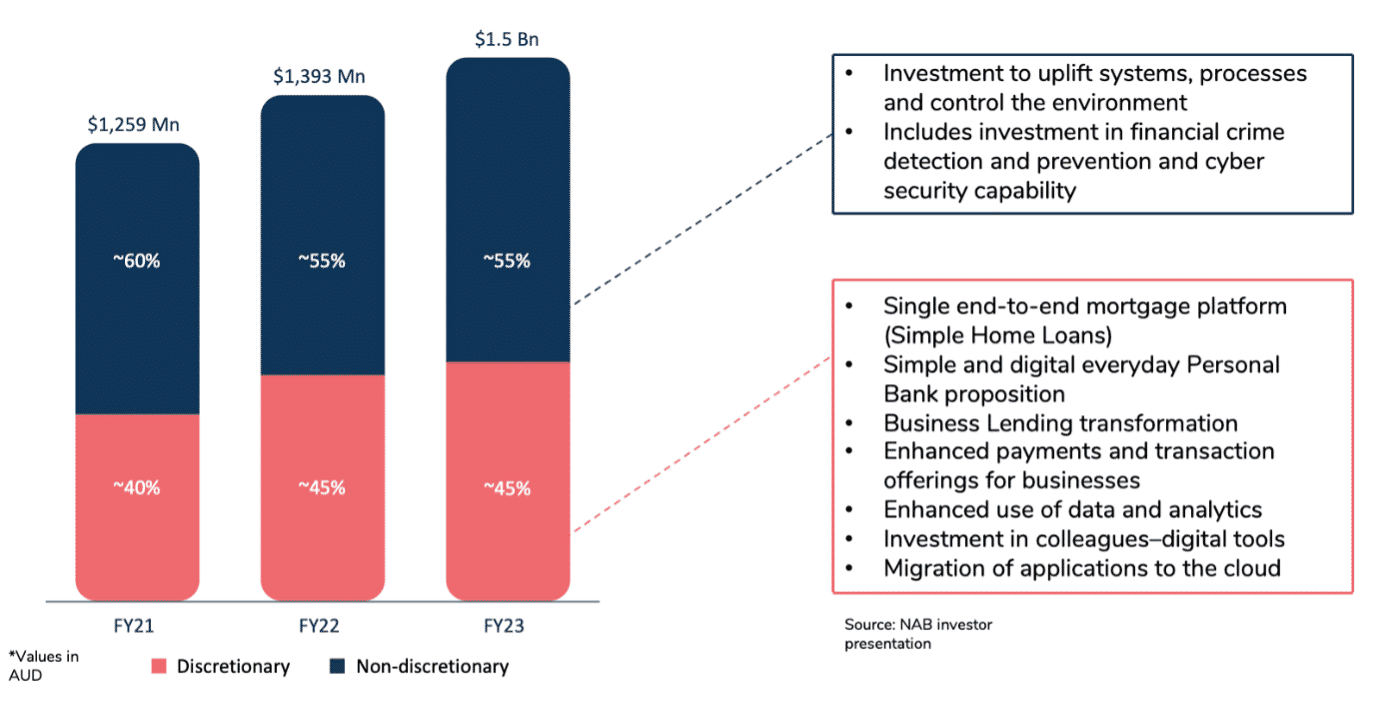

NAB investment outlook FY2023

Expert predictions also see NAB investing an additional USD 71.17 Mn (AUD 100 Mn) in FY2023. This additional spending will be on systems to help keep customers and the bank safe while maintaining spending on discretionary projects which support long-term growth.

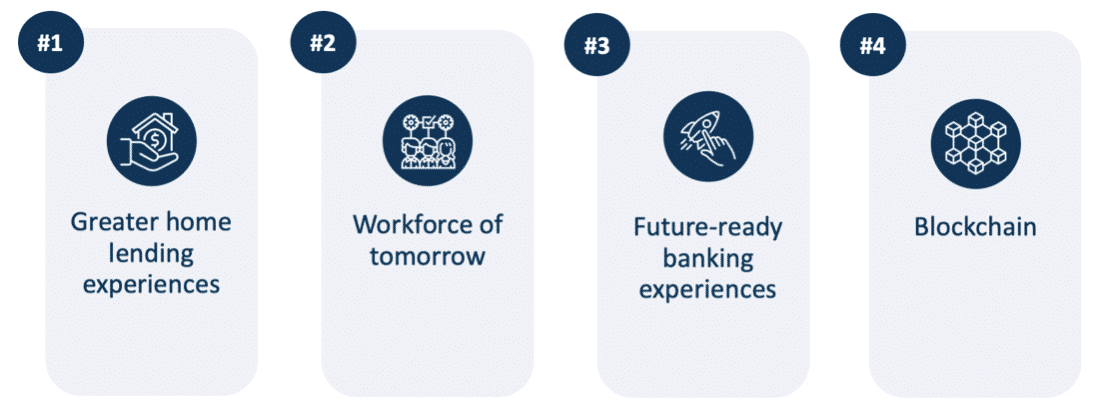

Growth opportunities

- #1 Greater home lending experiences

NAB also made changes to its home lending experience in FY2022 to further simplify its processes and enhance self-service capabilities:

- Over 85% of digital-enabled loan modifications are now processed via self-service features in the NAB app.

- Over a third of simple home loans were processed and achieved ‘time to yes’ in under an hour.

- NAB launched the Tailored Home Loan – a simpler home lending proposition with more transparent rates and no application fees.

- NAB also made calculators and tools available on its website to estimate home loan repayments, equity and borrowing power.

Another area that NAB can seek to expand is strengthening its home loan portfolio. This is where the bank should aim to take a few lessons from ANZ’s playbook, particularly the ‘First Home Coach’. In essence, it is a free service for potential home buyers, complete with a bank representative who will walk them through the entire home-buying journey.

NAB should also consider journey-led mapping for specific customer segments, including professionals, inhabitants of rural areas, and young executives. Lastly, the bank should seize the opportunity to partner with real estate marketplaces for greater outreach.

- #2 Workforce of tomorrow

NAB is committed to nurturing professionals who will shape the future of banking. The bank accomplishes this by encouraging its staff to be lifelong learners. This is evident with 8,000 employees completing the Career Qualified in Banking program.

NAB has also:

- Trained employees in the Melbourne Business School’s climate program

- Developed leaders through the Distinctive Leadership program

- Provided training to over 4,800 employees through the NAB Cloud Guild

Nevertheless, NAB can still take other avenues to upskill its workforce. These include increasing efforts in online learning by preparing e-learning modules such as UOB’s Better U Program and Maybank’s MyCampus platform.

To boost digital enablement among employees, NAB should also introduce an internal incubation program to encourage, challenge, and reward employees to accelerate innovation and develop next-generation ideas (e.g., RHB).

- #3 Future-ready banking experiences

Climate change has exacerbated seasonal natural disasters that affect communities worldwide. Because of this, banks have had to adapt and embrace climate resiliency in their action plans to brace for the future ahead.

NAB is no different, as its branches are in areas prone to seasonal weather events such as fires and floods. Additionally, earthquakes and aftershocks are natural disasters that risk damaging its branches across New Zealand. Hence, ‘Bank in a Box’ was established by the bank to circumvent this issue, providing customers access to full digital banking services.

The next step for NAB is to explore ways to circumvent infrastructural damage from natural disasters that will inevitably occur. The bank can do this by:

- Ensuring that its digital capabilities can provide the same services as physical branches to offer uninterrupted services to customers in times of any future natural disasters

- Including an option for customers to make video calls to the bank within the NAB app may be particularly helpful for senior customers or those who require in-depth assistance

- Consider opening unmanned, tablet-based smart branches to minimise infrastructural damage during natural disasters

- Consider closing branches with low footfall and consolidating these branches into larger community hubs to provide an omnichannel experience and educate customers on the use of digital services

- #4 Blockchain

Through its in-house venture capital fund, NAB Ventures, the bank was able to invest in Geora, a fintech that uses blockchain for agriculture technology. The platform is the first SaaS blockchain platform in agriculture to link traceability data with financing solutions using simple, no-code digital tools. In addition, the system captures crop data that could allow lenders to create tailored financial products for farmers.

The bank has also begun the development of its stablecoin to help settle trades on its carbon credit platform. In collaboration with other banks, NAB developed a Distributed Ledger Technology (DLT) based marketplace, better known as Carbonplace, where organisations can exchange their carbon offsets.

The next step for NAB includes:

- Implementing blockchain technology to make bank-to-bank and international transfers at significantly lower costs

- Increasing transparency in the transactions as all the movements are reflected and identifying the source and destination of any transfer is straightforward

NAB should also implement blockchain in its client identification system based on a Distributed Ledger Technology (DLT) to help the bank perform KYC verification on customers when processing credit or loan applications. This move will enable the bank to identify users on a single instance and store the information with access granted to other banks in the system.

Conclusion

As one of the big four in banking, NAB has a lot to fill, especially with its recent ICT spending increase in FY2022. However, one thing is clear; NAB is set on the right track, prioritising simplicity and inclusivity in their banking. And with resilient technology and the right frameworks, the bank is most definitely working towards the future of tomorrow.

Check out our previous report on NAB, here.