Due to a significant increase in inflation during the last quarter of 2022 which reached 7%, the Australian banking sector is expected to encounter ongoing difficulties in 2023. They will be particularly concerned about the decline in mortgage demand and higher interest rates. This is worrisome because inflation can restrict the borrowers’ capacity to repay loans, leading to increased NPLs (non-performing loans). Moreover, the inflationary rise and a slight uptick in GDP have added pressure on the operating revenues of banks. These factors have sparked a shift in Australia, with banks beginning to shift their perspective from household lending to institutional banking.

Market highlights

- Rising inflation will force the Reserve Bank of Australia to increase interest rates, leading to a fall in bank lending and the NIM (Net Interest Margin)

- Banks are likely to save on operating costs to offset the impact of declining NIMs on net profits, evident by branch closure and staff reduction

- High-interest rates and stricter regulations ensure BNPL firms must first hold credit licenses.

- A lack of funding and the challenging landscape led to major neobanks like Volt closing their operations.

- Banks are shifting from home lending to institutional banking and are diversifying beyond residential mortgages as the market is gripped by intense competition.

- Banks are simplifying their operations by eliminating redundant products and closing non-core businesses.

Key challenges faced by Australian banks

- High Loan-to-Deposit Ratio

- LDR is at 106.16%

- Strong credit demand for housing loans

- Low-interest rates led to borrowing surges and deposit reductions

- High LDRs pressure banks to maintain sufficient reserves and cover unexpected cash runouts

- Low Net Interest Margins

- NIM declined from 2.13% in 2018 to 1.77% in 2022

- NIM is below the APAC average of 3.04%

- The primary drivers for the decline are:

- Lower home loan margins

- Continued pricing pressure on mortgages

- Change in customer preferences from fixed-rate to floating-rate loans

- Higher balance of lower-yielding liquid assets

Financial highlights

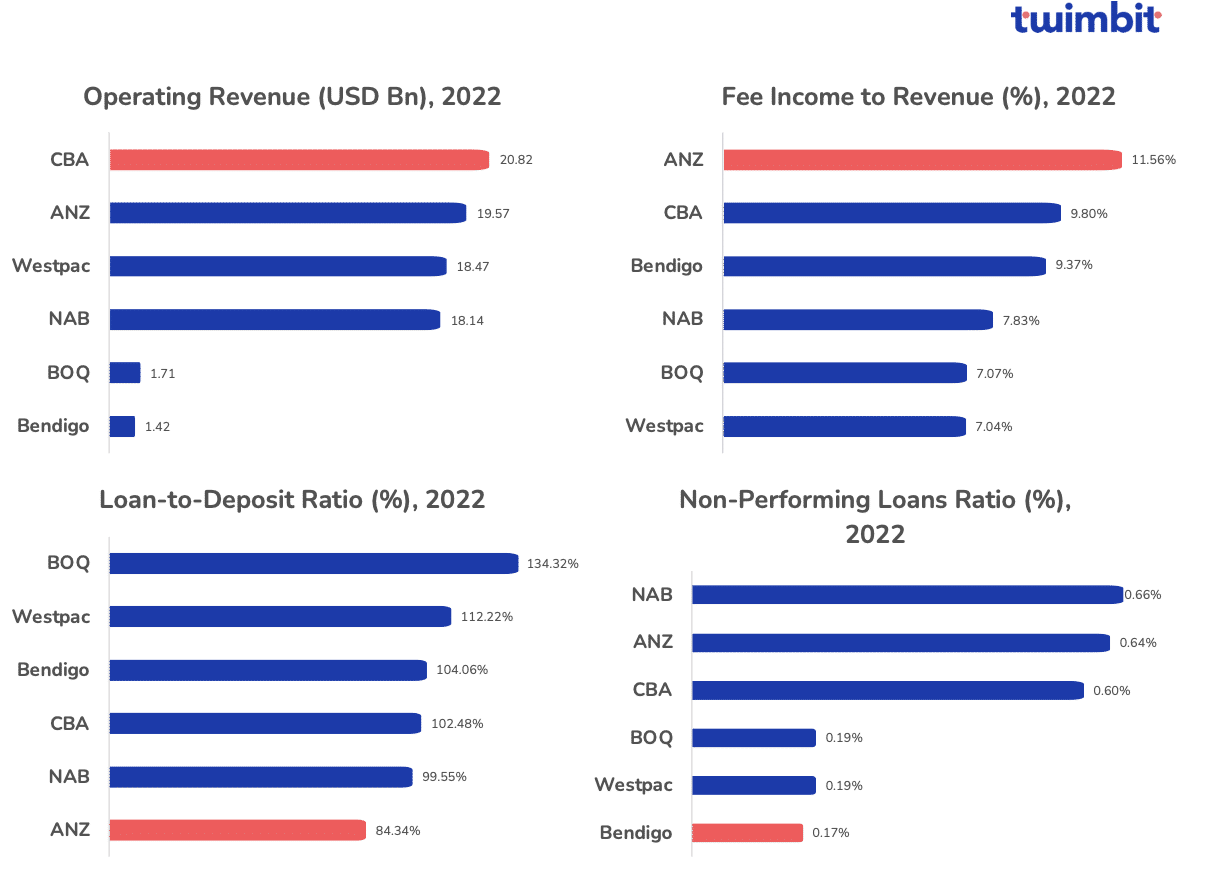

None of the Big 4 banks have revenues above the APAC average of USD 27.17 billion, with CBA having the highest revenue of USD 20.82 billion. However, BOQ and Bendigo are very small compared to other banks due to lower revenues than the Big Four.

The average fee income to revenue for Australian banks is 9%, the lowest in APAC. Currently, none of the Australian banks’ fee income to revenue is above or at par with the APAC average.

Australian banks have historically had high LDR (loan-to-deposit ratios), with an average of 106.16% in 2022. This is due to the industry’s reliance on home lending as its primary form of business. Despite such high LDR, the non-performing loans in Australia are among the lowest in APAC at just 0.41% in 2022.

The top initiatives by Australian banks

- #1 ANZ unlocks growth through sustainable phygital experiences

1835i – ANZ’s external innovation and venture capital partner

ANZ Plus

Today, more than 45% of active ANZ Plus customers have created savings goals, a significant increase compared to less than 5% on the traditional platform.

- Simplify money management with smart tools and a branchless digital proposition

- Save for multiple goals and eliminate the need for new accounts.

Breathe branches

ANZ collaborates with Breathe Architecture Studio for a sustainable new branch design.

- The design is flexible and cost-effective for remodelling and scaling based on changing needs.

- ANZ partnered with Anixter and 2by2 for a new solution allowing branch technology infrastructure to be disassembled, relocated, and reused.

- ANZ Plus stores and pop-up outlets also use the same sustainable design principles.

- #2 NAB makes payments and banking easier for SMEs

The digital-first strategy of NAB is to digitize simple tasks and reduce the need for human intervention. Here, NAB makes the most of its human agents, only utilising them for relationship-led customer support. To achieve this objective, the bank has launched the following for its SME business:

NAB Easy Tap is a digital proposition that allows the merchant to turn their Android phone into an EFTPOS reader to receive contactless card payments.

- The service comes with no set-up fees or terminal fees

- Allows for same-day settlement for NAB business accounts

- Obtain approval within a few minutes and start accepting payments two days after onboarding

Merchants can also access the NAB Hive portal for real-time customer and settlement data, insights, and analytics to better manage their business.

- #3 CommBank harnesses the power of AI to build hyper-personalised tools and deliver the best integrated digital experiences

Bill Sense is a feature built within the Commbank mobile app to help customers predict upcoming payments.

- Allows customers to track monthly payments

- Predict bills up to 12 months in advance

- Protect customers from getting overwhelmed with compiling payments

- Predict bills based on customers’ spending behaviour and past transactions

Step Pay is CBA’s first Buy Now Pay Later (BNPL) service which is available to more than 4 million customers of the bank

- The service is accepted anywhere where the bank’s cards (Mastercard) are accepted

- The initial approval limit offered is up to AUD 1000

- Repayments can be made over 4 fortnights

Unloan is a mobile-first digital home loan platform in Australia.

- Offer simple low-rate and no-fee home loans

- Grow loyalty bonus by 0.01% per annum per year

- Take as little as 10 minutes to apply

CommSec Pocket has facilitated more than AUD 1.3 billion in customer investments.

- Investment starts at AUD 50

- Customers can gradually build their portfolio and reach their financial goals

CBA Kit is the bank’s financial literacy program for kids.

- Includes a virtual account and prepaid card to teach kids about managing money

- In-app characters provide educational content to promote positive financial habits.

- #4 Up is Bendigo’s digital bank

Established in 2022 due to the partnership between Bendigo and Ferocia, a fintech company, Up has a customer base of over 600,000 users and holds more than AUD 1 billion in deposits.

The bank offers features, such as Maybuy and 2Up, which cater more towards the millennials and Gen-Z.

Maybuy

Maybuy is a form of Save Now, Buy Later (SNBL) model that encourages smart customer practices, such as saving, thereby eliminating impulsive purchases.

- Customers can add a product to the bank’s app and start saving by selecting a savings schedule

- Allow customers to purchase their desired products

2Up

2Up is an initiative that helps two individuals come together to share expenses, track spending and save towards a common financial goal.

- Allow 2 people to share their finances as one, separate from their personal accounts

- Obtain a shared debit card, set up joint savers and get instant digital cards

- #5 NAB’s integration of 86 400 with ubank

86 400 was established in 2019 and was overtaken by NAB in 2021 and merged into its Ubank subsidiary.

High-interest savings account

- No monthly fees on any ‘Save’ accounts

- Customers can open up to 10 Save accounts for different savings goals

- The bank offers an interest rate of up to 4.75% made up of the base rate of 0.10% and a bonus interest rate of up to 4.65%

- Customers need to deposit AUD 200 every month in the Save account to earn the bonus interest rate

Shared account

- Customers can set up a shared savings or expense account to track their shared saving goals and expenses

- Each individual associated with the sharing account gets a purple debit card separate from their regular debit card

- #6 Westpac aims to elevate the digital banking experience for its customers by launching the following initiatives.

Growth opportunities for Australian banks

Upon closely analysing the top 5 Australian banks, we uncovered 3 growth opportunities to help them grow and overcome the challenges that the banks currently face.

- #1 Buy Now Pay Later (BNPL)

Customers demand different forms of payment from their banks. As a result, BNPL is one of the most popular forms of payment in Australia and the APAC region. In Australia, BNPL payments expect to grow at an annual rate of 21% and reach USD 14.2 billion by the end of 2023.

However, only NAB and CommBank currently offer a BNPL service to their customers, with Westpac’s BNPL service, PartPay, on the way. On the other hand, ANZ, Bendigo and BOQ do not have any BNPL offerings.

Therefore, a competitive BNPL offering will help Australian Banks:

- Increase customer engagement, wallet share and customer loyalty

- Create additional revenue streams through transactions, merchant fees and interest on unpaid balances

- Attract new customers to the convenience of BNPL

- Access customer data generated through BNPL usage for better personalised experiences

- #2 Open banking

Open banking is becoming essential due to changing consumer behaviour and increased competition. Consumers are increasingly looking for digital solutions that offer personalised experiences.

Currently, all six banks are data holders and data recipients, wherein they can share the Customer Data Right (CDR) data with an accredited organization when authorised to do so from the bank’s mobile app or website. In combination, these banks have 27 data holder brands and accounted for more than 193 million API usage calls in 2023.

Therefore, open banking is necessary as it can help Australian banks:

- Lower transaction fees – The reduction in bank-to-bank settlements will help in up to 90% cost savings as there will be fewer intermediaries

- Expand service offerings – Connecting APIs with NBFCs and fintechs will allow banks to offer a wider range of products and services

- Data analytics – Open banking can generate an abundance of customer data, create new products and services and improve risk management

- Fee-based income – Banks can generate fee income by collaborating with third-party service providers and offering them their tools and services

- #3 Cost to Serve

The average cost efficiency of the top six Australian banks is 52.33%, above the threshold of 50% and way above the APAC average of 45%. Despite having an average LDR of 106%, the average NIM is still at 1.77%, almost half the APAC average of 3.08%.

A decline in the NIM is due to lower home loan margins, continued pricing pressure or mortgages, changing customer preferences for fixed-rate loans over floating-rate loans and a higher balance of lower-yielding liquid assets.

Thus, there are several ways Australian banks can aim to improve their cost to serve:

- Maximise digital technologies to automate and streamline business processes

- Replace legacy systems with cloud-first computing to reduce infrastructure costs

- Remove redundant products and services from the portfolio

- Reduce reliance on interest incomes and find new revenue streams from non-interest incomes

- Expand product portfolio and put less pressure on mortgage lending

- Leverage open banking APIs to generate fee-based income from third-party financial service providers

The future for Australian banks

In conclusion, Australia is navigating through a challenging landscape. Despite the Big 4 benefiting from previous interest rate hikes, rising inflation and the need for higher rates pose concerns for bank lending and NIMs. In response, the industry has begun closing branches and reducing staff to offset further declining profits. Additionally, the regulation of BNPL and the gradual decline of neobanks highlight Australia’s evolving nature in the financial sector. As the industry adapts to these changes, it will be crucial for banks to navigate the economic landscape effectively and ensure their long-term sustainability.

To know about how Australian banks have changed from 2022, read our report on the State of Australia banks, 2022.

To know about the State of Indian Banks in 2023, click here.

To know about the State of Malaysian Banks in 2023, click here.

To know about the State of Vietnamese Banks in 2023, click here.

To know about the State of APAC Banks in 2023, click here.