The economic growth of Singapore is expected to slow in 2023, despite a projected increase of GDP between 0.5% and 2.5%, compared to a higher growth rate of 3.6% in 2022. The banking sector currently contributes to 20% of the country’s GDP, despite declining non-interest income and slower earnings growth.

While banks in Singapore excel in technological innovations, blockchain, artificial intelligence, distributed ledger technology (DLT), and big data analytics, it is anticipated that the profitability will be influenced by the upsurge in net interest margins.

Moreover, the evolving behaviour of affluent clients, whether their inclination to spend or invest through private advisors, contributes to a decline in income derived from wealth management and investment banking fees. Despite these challenges, there is a prevailing sense of optimism that inflation will gradually alleviate in the latter half of 2023, averaging between 3.5% to 4.5%. This change will help offer some relief to Singapore’s economic outlook.

Market highlights

- Anticipated earnings for Singapore banks project to grow at a slower trajectory due to the attainment of peak NIM (net interest margins) in October 2022.

- The widening asset spread has driven the peak of NIM in the past decade, resulting in the banks’ record-high net profits.

- The fall in wealth management and investment banking fees resulted in a decrease in non-interest income.

- The affluent clientele of Singapore banks actively spend their wealth or invest it through personal private investment advisors.

- The average decline in income from wealth management stood at 29.12% compared to 2021.

- DBS recorded a 45% decline in its fee income from investment banking, whereas UOB recorded an increase of 6%.

- OCBC did not witness any notable change in its fee income from investment banking.

Priorities for Singapore Banks

- Purpose Bound Money (PBM) – DBS collaborated with Open Government Products (OGP) to launch a live pilot that enables real-world transactions through OGP’s voucher platform using tokenised SGD-based vouchers.

- PBM is a digital currency that operates under logical rules and can be transferred once specific programmable conditions are satisfied.

- The tokenised cash is limited to designated purposes, encompassing a specific period and designated recipients.

- Technology and innovation centre – UOB is investing USD 375.3 million (SGD 500 million) to build an innovation centre in Singapore’s first upcoming smart business district, Punggol.

- The innovation centre will be crucial in developing new features for UOB’s digital mobile banking app, TMRW.

- A regional hub for piloting and launching new digital products.

- UOB’s innovation accelerator, FinLab, will also be located at Punggol Digital District, offering assistance to tech firms, small businesses and startups to grow their digital initiatives.

- Open source – The imperative for flexibility and fostering innovation drives the decision of OCBC to embrace open source.

- The OpenShift platform helps OCBC modernise applications, decrease dependence on proprietary software, strengthen resilience, and introduce new business capabilities.

- OCBC utilises the platform to enhance its enterprise data science capabilities, scale AI deployment, and drive the scalability of AI technology.

Financial highlights

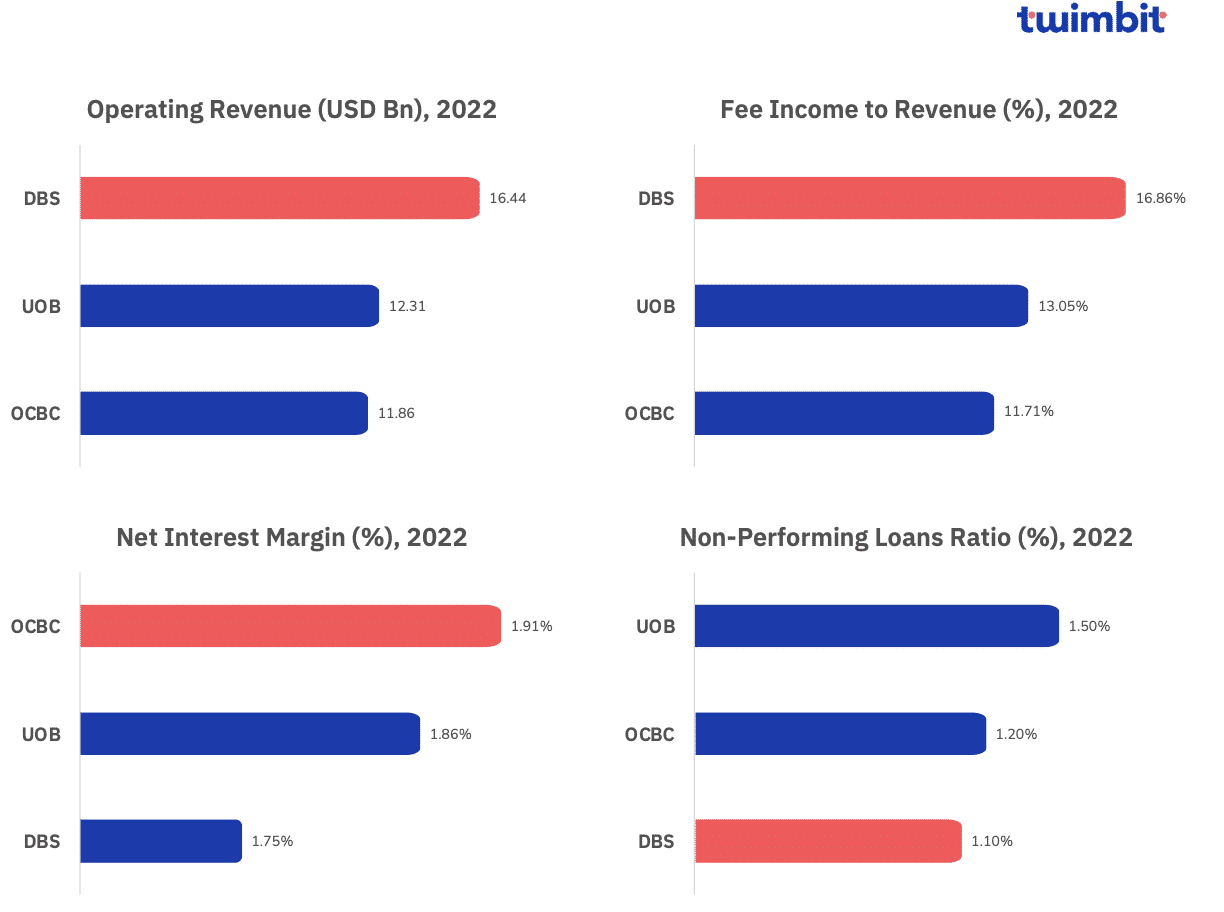

Singapore banks generate below-average revenues compared to their counterparts in the Asia Pacific. However, it is worth noting that these banks rank among the top banks. They have the highest fee income to revenue contribution at an average contribution of 13.87% of total revenue. Specifically, DBS has generated the highest fee income at 17% of its total revenue.

The NIM did not increase, despite Singapore’s series of interest rate hikes. Instead, it peaked as the policy tightening in Singapore reached its conclusion. Furthermore, these banks have declined fee income, primarily due to decreased wealth management and investment banking fees. The decline in fee income compounds the challenges posed by low NIM.

Singapore banks maintain a strong loan book with some of the APAC region’s lowest NPL (Non-Performing Loans). With an average of 1.27%, Singapore ranks second only to Australian banks in NPL.

Why does DBS have the best-in-class ICT spend ratio?

- DBS has an ICT spend-to-revenue ratio of 9.3% with a cost efficiency of 43%, resulting in an optimum mix with the investment outlay.

- The ICT spending in DBS, including its sizeable in-house team (not captured in the 9.3% ratio), projects its ICT spending to be as high as 16% of revenues.

- BOQ and BPI incur higher ICT spend-to-revenue ratios, spending 10.9% and 13%, respectively, which results in a higher cost to serve (50%).

- DBS has 12,000 technologists (2X the number of bankers) focused on data and AI, with an additional 1,000 members from the employee team.

- DBS’ ICT budget has led to an effective cloud-first strategy, with 99% of its applications being migrated from physical service to the cloud in the last three years.

Top initiatives by Singapore banks

- #1 DBS continues to be the CX banking leader across all customer touchpoints

DBS RAPID

- A digital solution that harnesses DBS’s API (application programming interface).

- DBS offers 180 APIs, enabling seamless business transactions within an ecosystem.

- These APIs integrate real-time processing of payments, receivables and information enquiries into various business workflows.

DBS BetterWorld

- Interactive metaverse experience in partnership with Sandbox.

- DBS aims to utilise it as an additional innovative engagement tool to spread awareness on important ESG issues.

DBS PayLah!

- A lifestyle app for customers to conduct everyday transactions (separate from the Digibank app).

- Use the app to book tickets and rides, pay expenses, access rewards, order meals and scan to pay at more than 180,000 points.

- Earn and manage card reward points seamlessly and collect stamp cards within the app for cashback rewards on rides.

- #2 UOB reimagines digital customer journeys to create more invisible experiences

UOB Branches adopt different branch styles for various customer segments:

- Lifestyle Branches for young professionals and young families

- Wealth Centres for the merging affluent and the affluent

- Business Centres for Entrepreneurs and Small Businesses

UOB Rewards+ is Singapore’s most extensive rewards program, offering customers access to over 1,000 deals, cashback and rewards. Available at more than 20,000 merchant locations, the program encourages customers to use UOB cards for daily necessities.

SkyArtverse by UOB is the first Asian bank property to create a decentralised virtual art gallery in Decentraland, a popular Metaverse platform.

- The virtual gallery exhibits 37 winning artworks from the 2022 UOB Painting of the Year competition.

UOB Mobile apps have specialised applications for different customer segments.

- UOB TMRW for consumers

- UOB SME for SMEs

- UOB Infinity for corporate clients

UOB TMRW is the current flagship digital banking platform for UOB.

- Utilises AI-driven insights to deliver personalised customer benefits and perks through Rewards+

- Made investing simple through SimpleInvest.

- Manage accounts, credit cards, investments, and transactions on the go.

- Allows access to bill payment, Buy Now Pay Later (BNPL) and various instant payment facilities locally and in Thailand.

- Features smart money management capabilities that provide:

- Consolidated financial view across banks and

government agencies - Investment recommendations from SimpleInvest and SimpleInsure

- Consolidated financial view across banks and

- #3 OCBC provides innovative product propositions to support customer journeys.

OCBC STACK is a digital platform that enables customers to maximise the potential of reward points.

- Access all reward points on one platform

- Track and combine rewards points across various rewards programs

- Use the points to redeem instant vouchers

OCBC RoboInvest is a hassle-free robo-advisory platform that uses tested algorithms to provide intelligent investment plans.

- No human intervention or constant portfolio monitoring

- Customers can invest in 38 portfolios starting from USD 100

- No lock-in period

- Smart portfolio rebalancing

OCBCx65Chulia is a virtual bank branch on the Metaverse platform, Decentraland.

- Customers gain an additional access point that represents a new way to engage.

- The next phase of OCBCx65Chulia will include gamification to enhance the customer experience further.

Problems Faced by the Singapore banking industry

As banks in Singapore attract unprecedented wealth, the diminishing risk appetite among Asian millionaires presents several challenges for the Singapore banking industry. A key challenge Singapore currently faces is that they are witnessing a decline in wealth management and investment banking fees for the banks.

Specifically, the wealth management fees for the three biggest banks in Singapore declined by an average of 29% between 2021 and 2022:

- DBS – declined by 26% from USD 1340 million to USD 998 million

- UOB – declined by 30% from USD 576 million to USD 402 million

- OCBC – declined by 32% from USD 866 million to USD 592 million

Growth opportunities for Singapore banks

- #1 Build up wealth management offerings to improve fee income

The net interest margins (NIM) for Singapore banks have peaked and are likely to plateau, resulting in slow bank interest income growth. Stagnant interest income growth also indicates a decline in fee incomes between 2021 and 2022.

The fee incomes for DBS, OCBC and xUOB declined by 9%, 18% and 9%, respectively. The primary driver for the declining fee incomes is the decline in wealth management income.

Banks should enact the following initiatives to increase their wealth management fees.

- Enhance the range of services offered to include estate planning, tax optimisation and philanthropic advisory.

- Introduce performance-based fee structures where fees are linked to investment performance and returns generated for clients.

Another initiative banks can work on is to provide comprehensive and specialised services to family offices.

- Cater to families and affluent individuals with the option to hire investment advisors.

- Encourage strong business conduct with the bank through dedicated experts to best address complex needs.

- #2 Expanding into new revenue streams

Singapore banks are witnessing a decline in their non-interest income due to a decline in wealth management fees. Therefore, banks should explore new realms of non-interest fees to offset the decline in wealth management fees.

For starters, there are several best practices that banks across Singapore can adopt from other banks worldwide and within its region to enhance their sustainability and growth further.

The acquisition of Lakshmi Vilas Bank Ltd. by DBS in 2020:

- This acquisition enabled several lending opportunities for DBS to expand its presence in the Indian SME sector.

- SMEs, which typically have difficulty obtaining traditional loans, could now obtain private credit through DBS.

The introduction of Eco-Care loans by OCBC in March 2021:

- Reduce customers’ long-term energy consumption with affordable eco loans that offer lower interest rates and rebates on electricity plans.

- OCBC extended USD 2.62 billion in Eco-Care loans, accounting for 1 in 5 home, renovation and car loans.

The decision of DBS to expand its geographical presence to Dubai:

- The Emirates and its direct connectivity with Asia, Africa, the Middle East, and Europe markets make it a strategic hubspot for financial institutions.

- The ease of trade and capital flows further enhances its appeal as a desirable location for financial institutions.

- #3 Making financial services accessible for the underbanked population

The partnership between UOB and NAC (National Arts Council)

UOB signed a 3-year MOU (Memorandum of Understanding) with NAC to foster a vibrant arts scene in Singapore, which included collaborating and developing the financial and business competencies of the local arts community.

The MOU aims to deliver maximum impact for Singapore by focusing on these three key areas:

- Empower local artists by enhancing their financial and business capabilities.

- Promote community wellness with collaborative art activities and initiatives.

- Facilitate network expansion to help promising artists to reach new audiences.

The launch of the Adopt-A-Hawker Centre program by DBS

The program aims to support and safeguard the livelihoods of hawkers affected by the pandemic through these initiatives:

- Bolster earnings by purchasing meals from them and distributing meal packs to front liners, families in need, and other beneficiaries.

- Help hawkers improve their online presence and explore digital tools to digitise their businesses.

- Include group buys and better online discoverability of hawkers to increase their monthly earnings by at least 10%.

- #4 Cybersecurity risks arising from the adoption of 3rd-party services

DBS experienced disruptions in its online banking service on two occasions where customers could not use the banking services for ten hours. Such disruptions prove that banks need to do more regarding their system availability and IT system resilience.

Therefore, banks should take the following actions to strengthen their risk management systems with third-party service providers:

- Conduct comprehensive evaluations of their cybersecurity, procedures, infrastructure, and incident response capabilities.

- Implement a vendor risk management program to assess, monitor, and manage cybersecurity risks related to third-party services.

- Regularly monitor security controls and practices, utilising network, system, and data handling tools.

- Collaborate to establish incident response protocols, roles, and communication channels and conduct drills to test response effectiveness.

- Enforce data protection and privacy standards, including handling requirements, encryption standards, access controls, and breach notification procedures in contracts.

- #5 Generate fee income through UPI and PayNow integration

The integration of UPI and PayNow can help Singapore banks generate fee income through the following:

- Transaction fees – Banks can charge a nominal fee for processing UPI transactions. This amount can be a portion of the transaction or a fixed amount.

- Merchant Discount Rate (MDR) – This is a fee which banks charge to the merchant for accepting the UPI payments. This fee is usually shared between the acquiring and the issuing banks.

- Interchange fees – This is the fee banks charge for processing the transaction between different banks. The acquiring bank pays this fee to the issuing bank to settle the transaction.

- Cross-selling financial products – UPI transactions offer valuable customer spending data. Banks can utilise this data to gain insights into customer behaviour and provide personalised products and services.

- #6 Rising competition from digital-only banks

Trust Bank:

- It is among the newest online retail banks attracting customers by providing reduced fees, enticing incentives, and waivers on minimum account balances.

- The bank offers a basic interest rate of 1.5%, providing the opportunity to earn a maximum of 2.5% on deposits up to USD 56,250.

- New credit card customers are given vouchers valued at USD 25 to use at FairPrice supermarkets.

GXS Bank:

- The digital-only bank is a joint venture between Southeast Asian super app Grab Holdings and Singaporean telecoms giant Singtel.

- The bank offers a daily accrued interest rate of 0.08% p.a.

- Customers can create up to eight ‘savings pockets’ with a goal and earn a daily interest rate of 3.48% p.a.

- The maximum deposit limit is up to USD 3750.

Learnings for traditional banks:

- No minimum balance requirement – Customers are not required to maintain a monthly average balance.

- Interest rates – Digital banks offer higher interest rates as an incentive to open a virtual savings and deposit account. In comparison, traditional banks offer lower interest rates due to the cost of maintenance.

- Microloans – GXS launched flexible loans that let customers borrow as little as USD 150. The payback tenure starts at two months, while customers can pay off early without fees.

What is the future of Singapore’s banks?

As 2023 approaches the mid-way mark, the banking industry in Singapore is projected to experience slower growth in 2023, influenced by various factors. Declining earnings for Singapore banks can be attributed to peak NIM, signalling a profitability slowdown.

However, Singapore banks remain at the forefront of technological innovation, actively exploring advancements like blockchain, artificial intelligence, and big data analytics. The decline in non-interest income, mainly from wealth management and investment banking fees, indicates a behaviour shift among wealthy clients seeking alternative investment strategies.

The expected slowdown in inflation during the second half of 2023 may provide some relief to the overall economic landscape in Singapore.

To know about the State of Australian Banks in 2023, click here.

To know about the State of Indian Banks in 2023, click here.

To know about the State of Malaysian Banks in 2023, click here.

To know about the State of Vietnamese Banks in 2023, click here.

To know about the State of APAC Banks in 2023, click here.