Indian banks have been on the road to recovery with healthy financial results, strong loan growths and improving asset quality. This trend continued in Q2 2023 with a substantial loan growth of 10.5% YoY (year-on-year), which helped banks boost their interest incomes. Indian banks achieved a profitable quarter with declining NPAs and improved cost efficiency.

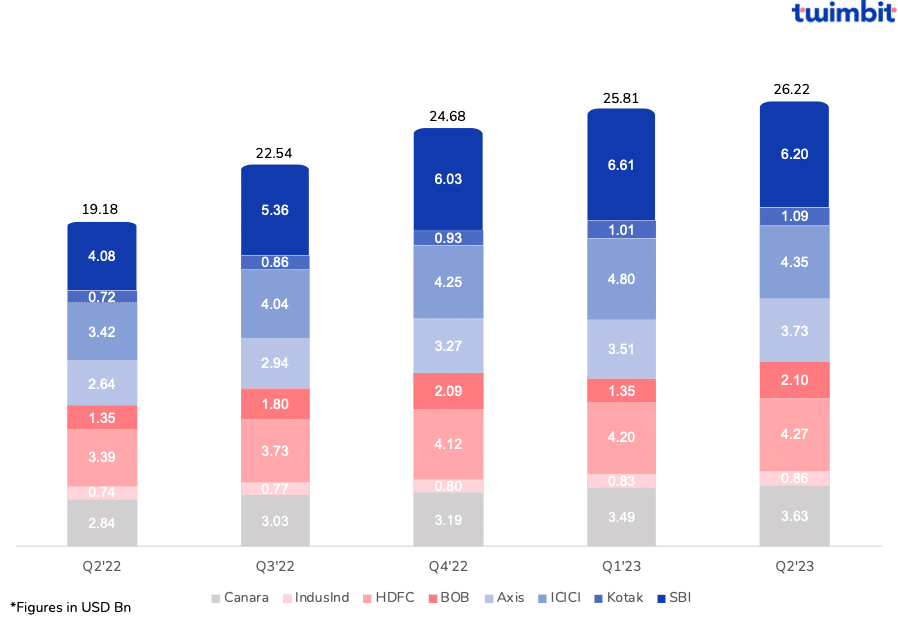

The top 8 banks in India generate USD 26 billion in net revenues

Net revenue grew by 36.74% YoY (USD 26.22 billion) in Q2 2023 (Figure 1). This was driven by a 16.4% increase in interest income and a 12.8% increase in non-interest income.

Based on our findings, we recorded the Bank of Baroda to chart the highest YoY growth at 55.74%, from USD 1.35 billion in Q2 2022 to USD 2.1 billion in Q2 2023 Similarly, the 34% increase in net interest income and 37% increase in non-interest income played significant impact to the bank’s overall growth.

Conversely, despite witnessing growth, IndusInd Bank charted the lowest among the top 8 at just 16.84%, increasing from USD 0.74 billion to USD 0.86 billion.

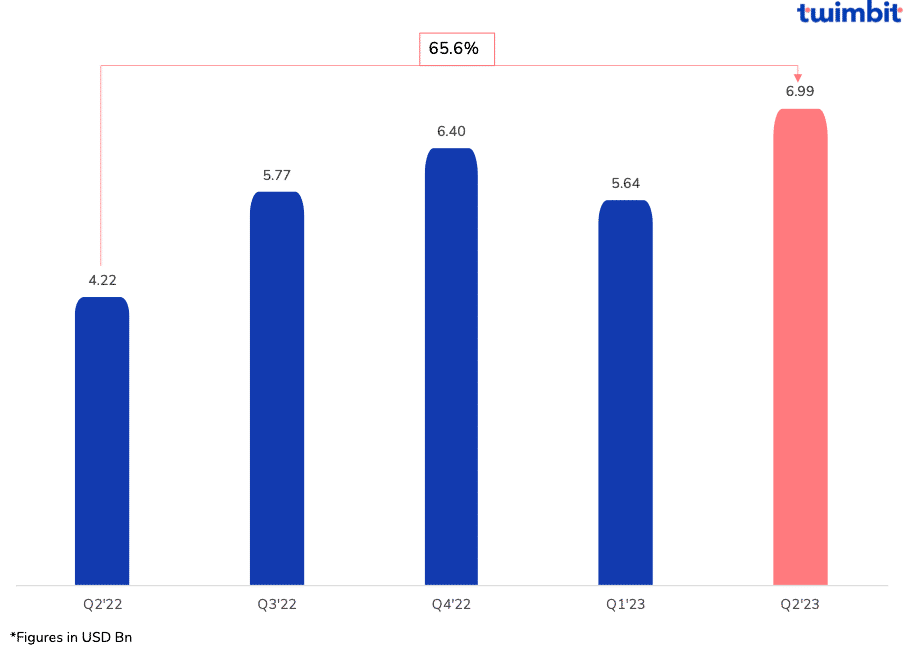

Net profit grew by 66% YoY to USD 7 billion

Between Q2 2022 and Q2 2023, public sector banks across India dominated, recording exponential growth rates. On average, the three public sector banks stood at 113.60%, with SBI leading at 178.25% and recording its highest-ever net profit, USD 2.05 billion.

There were several factors to the bank’s success, specifically strong loan growth, where the loan book grew by 10.3% in Q2 2023, the highest for the bank in over 2 years. Its net interest income also rose by 24.7%, driven by loan growth and higher interest rates.

In contrast, private banks recorded an average increase of 39.61%.

Despite the US banking crisis, Indian banks outperformed with sustained bank credit growth and liquidity buffers. The Reserve Bank of India (RBI) attributed the surge in credit to various factors, including significant growth in the retail loan book.

The corporate sector also showed a significant rebound in lending activity as the recovery continued.

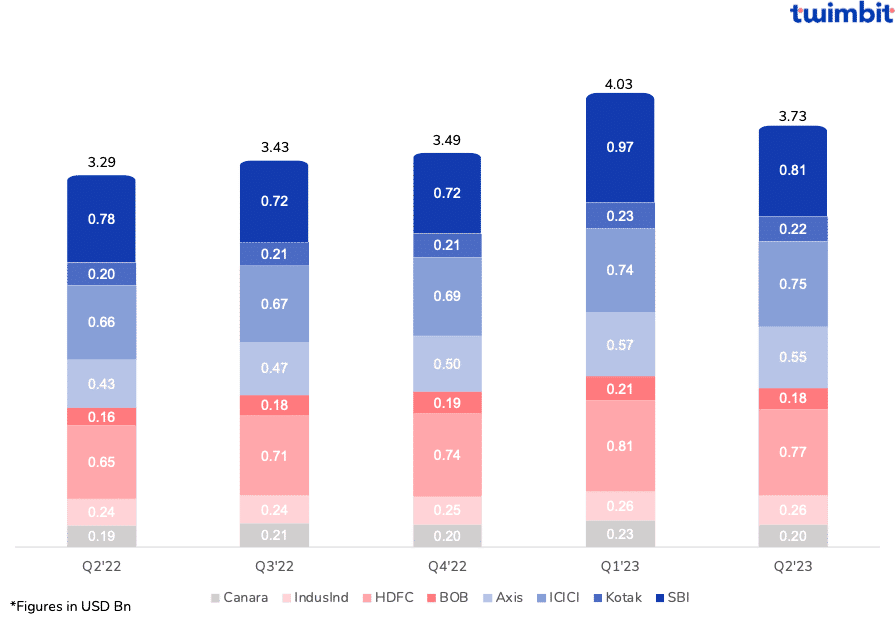

Growing trends in fee income

The demand for more digital banking transactions and other fee-based services such as wealth management and insurance have significantly increased banks’ fee income.

Banks’ fee income grew by 13.34% YoY, from USD 3.29 billion in Q2 2022 to USD 3.73 billion (Figure 3) in Q2 2023.

Banks look to further diversify and develop their fee income through 3 key areas:

- #1 Digital banking

By simplifying customer execution, banks can generate heightened fee revenue from offerings like online bill settlement, fund transfers, and account initiation.

- #2 Wealth management

Banks aim to fulfil the heightened demand for wealth management solutions such as asset management, portfolio guidance, and related offerings that yield fees.

- #3 Expansion of bancassurance

This business model in which banks sell insurance products to their customers has led to increased fee income from commissions on insurance sales.

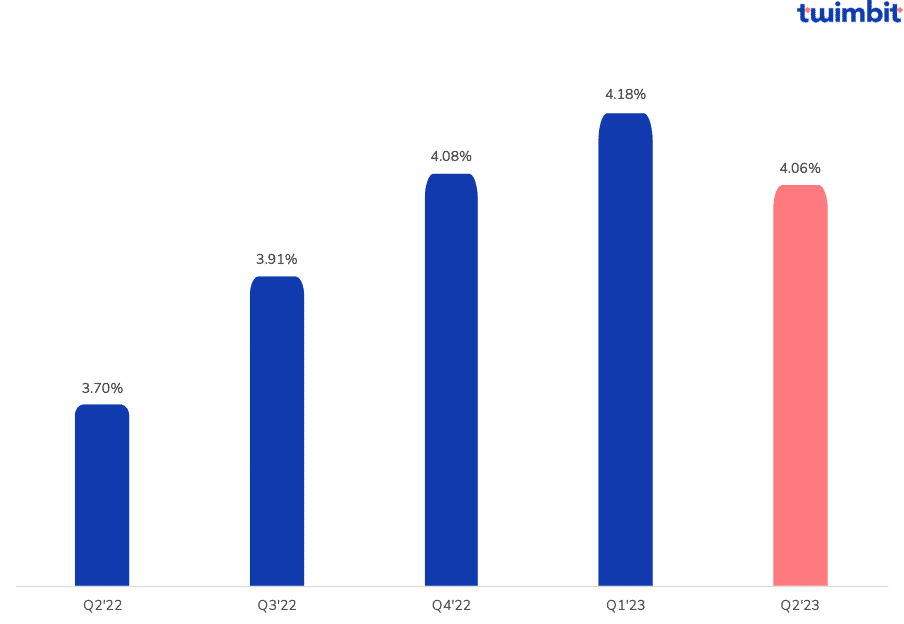

Net interest margins take a dip in Q2 2023

Enhancing the quality of assets resulted in a 36 basis point (Figure 4) increase in the net interest margins (NIM), reaching 4.06% between Q2 2022 and Q2 2023. However, NIMs decreased over the previous three quarters. 6 of 8 banks declined in NIMs from Q1 to Q2 2023, with IndusInd marking a 1 basis point increase and HDFC Bank maintaining stability.

Irrespective, Indian banks still have a higher NIM than banks in other countries in APAC. These high NIMs are due to a credit surge, higher lending rates by the RBI, and the low cost of holding deposits.

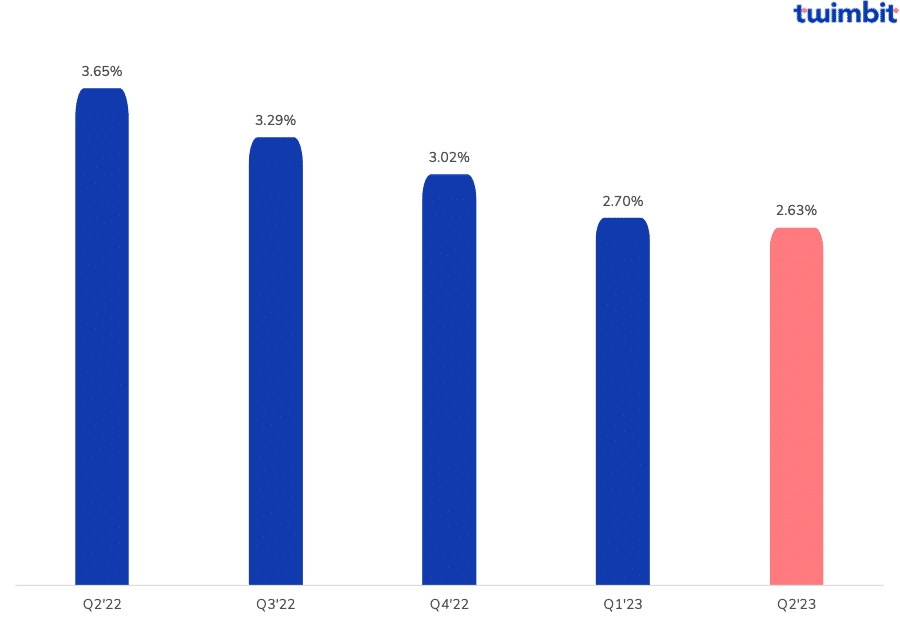

NPAs fall by 102 bps, the lowest in a decade

The average non-performing assets (NPAs) of the top eight banks witnessed a 102 basis point decline. The current NPA stands at 2.63% (Figure 5).

Of the 8, 3 are public sector banks. These banks generally operate with a higher NPA ratio. However, at the same time, these banks have recorded the highest decline in their NPAs by an average of 33.19% compared to the decline witnessed by private banks at an average of 19%.

Indian banks have been able to control their NPAs due to the following:

- Improved credit appraisal and monitoring to identify potential NPLs early and apply corrective measures

- Stringent credit checks to assess applicants’ creditworthiness and risk of default

These initiatives help India avoid disbursing loans to applicants below the acceptable credit risk level.

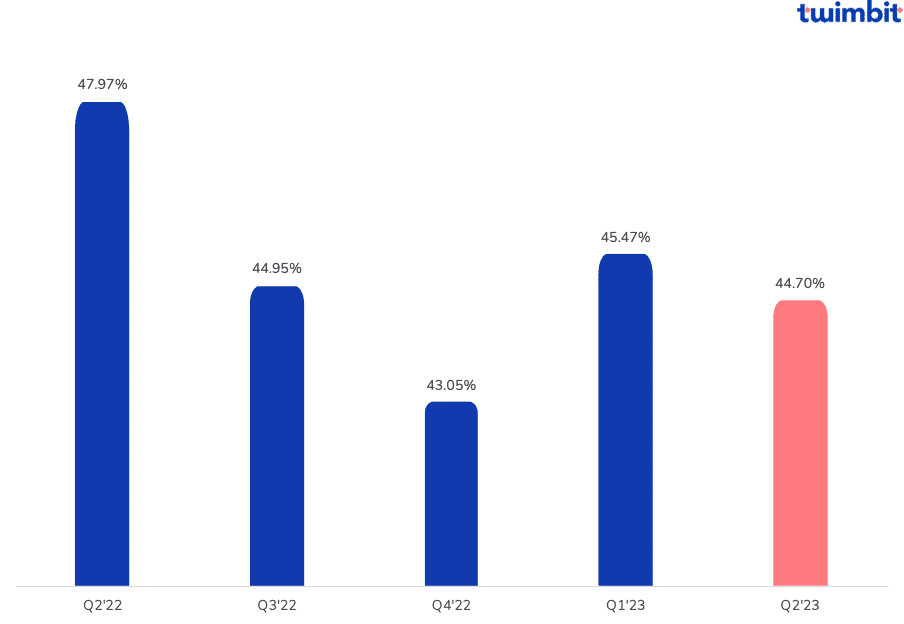

Cost efficiency for Indian banks dropped by 3.27% between Q2 2022 and Q2 2023

Indian banks have been more efficient in their operations than peers in other regions. Their average cost efficiency stood at 44.7% in Q2 2023, down from 47.97% in Q2 2022 (Figure 6).

Of all the banks analysed, only SBI has its cost efficiency above the threshold value of 50%. However, the bank has vastly improved its efficiency, reducing it from 61.94% in Q2 2022 to 50.37% in Q2 2023. The bank achieved this due to an exponential increase of 32% in interest income and 74% in non-interest income.

Top Initiatives by Indian Banks

- #1 ICICI Bank

ICICI Bank has numerous initiatives for all its customer bases, with over 600 APIs for retail banking and over 85 for corporate banking.

- iMobile Pay – A SuperApp for retail customers with more than 400 services

- ICICI STACK – A merchant account with zero balance and swipe-based benefit

- Embedded banking for MSMEs – One-to-one client ERP integration using APIs

- #2 Kotak Mahindra Bank

The bank established a digital acquisition and fulfilment engine in Kotak 811. This has transformed the bank into a semi-autonomous digital-only bank focusing on mobilising engagement and cross-selling products.

- Kotak 811 acquired a 12.3 million customer base (71% of the total) in March 2022

- The app has more than 6.2 million monthly active users

- #3 HDFC

HDFC Bank launched its SmartBuy e-commerce platform that offers various products and services, including groceries, electronics, fashion, and travel. To use the service, one has to have an HDFC bank account and a valid credit or debit card.

Some of the benefits of HDFC SmartBuy:

- Earn reward points on their purchases and redeem them as cashback, gift vouchers and other benefits

- Obtain discounts on various products and services

- Gain access to a wide variety of national and international brands

- #4 Axis Bank

The bank opened 3 DBUs (Digital Business Units) as part of the Government of India’s initiative – to launch 75 DBUs in 75 nationwide districts. This initiative aims to take banking services to the rural and semi-urban parts of the country.

The Axis Bank DBUs are equipped with;

- Digital user interactive devices

- Self-service infrastructure

- Internet banking kiosks

- Passbook printing kiosks

- Account opening kiosks

It also offers digital applications for Government-sponsored schemes on the National Portal.

In conclusion, the performance of Indian banks in Q2 2023 was strong, indicating a positive sign for the banking sector. The strong economic growth, the decline in NPAs, and the improvement in profitability are all positive factors that are likely to continue to benefit the banking sector in the coming quarters. However, it is important to note that the global economic environment remains uncertain, and some risks could impact the profitability of Indian banks.

To learn more about how Malaysian Banks performed in Q2 2023, click here.

To learn more about how Indonesian Banks performed in Q2 2023, click here.

To learn more about how Filipino Banks performed in Q2 2023, click here.

To learn more about how APAC Banks performed in Q2 2023, click here.