Key Takeaways

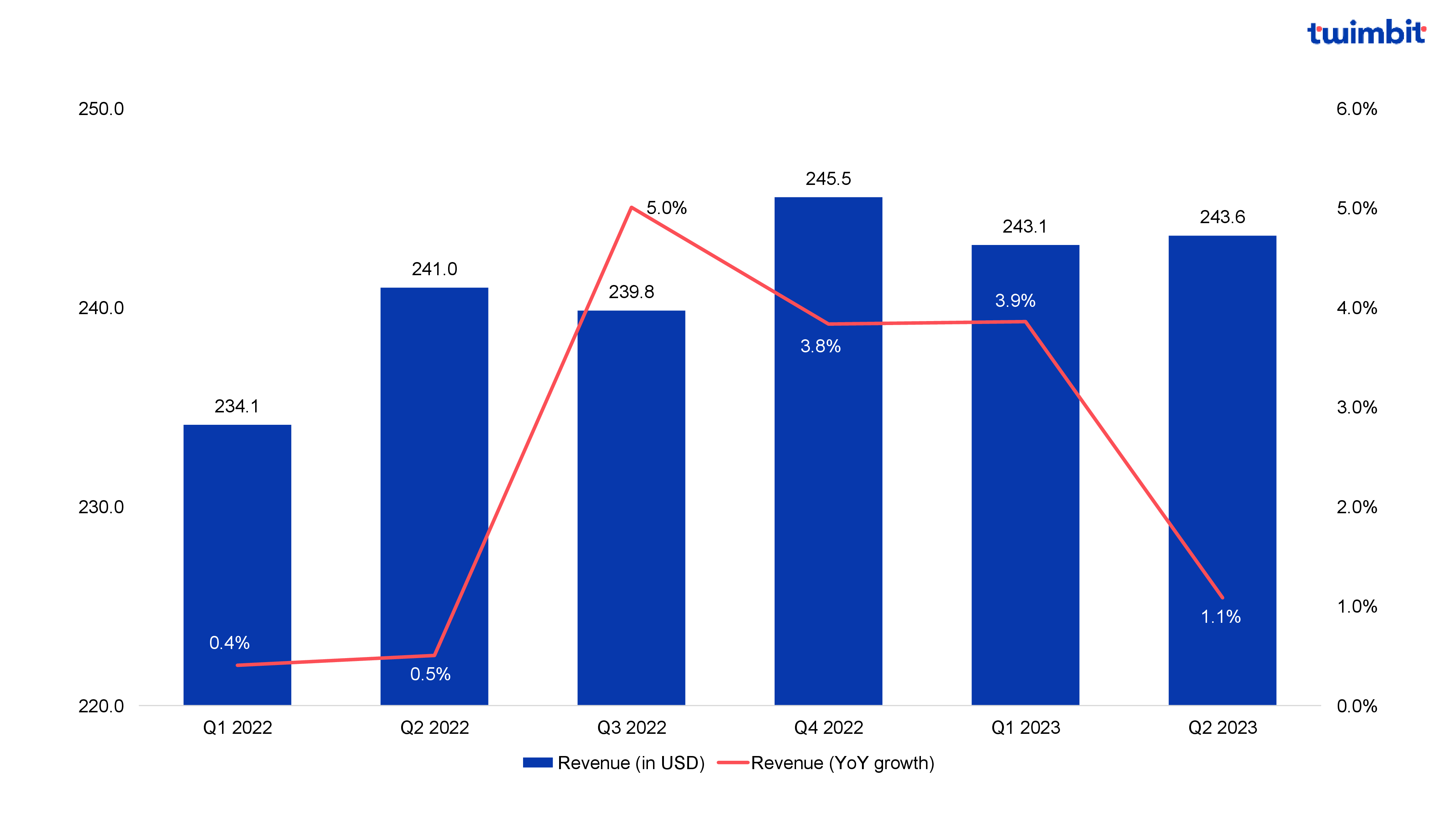

- In Q2 2023, the top 20 global telcos covered in this analysis witnessed a bit of sluggish growth. After three consecutive quarters of 3.8-5.0% YoY growth, they achieved a 1.1% YoY growth in constant currency, with around 70% reporting positive revenue growth.

Exhibit 1: Revenue performance YoY basis, Q1 2022 – Q2 2023

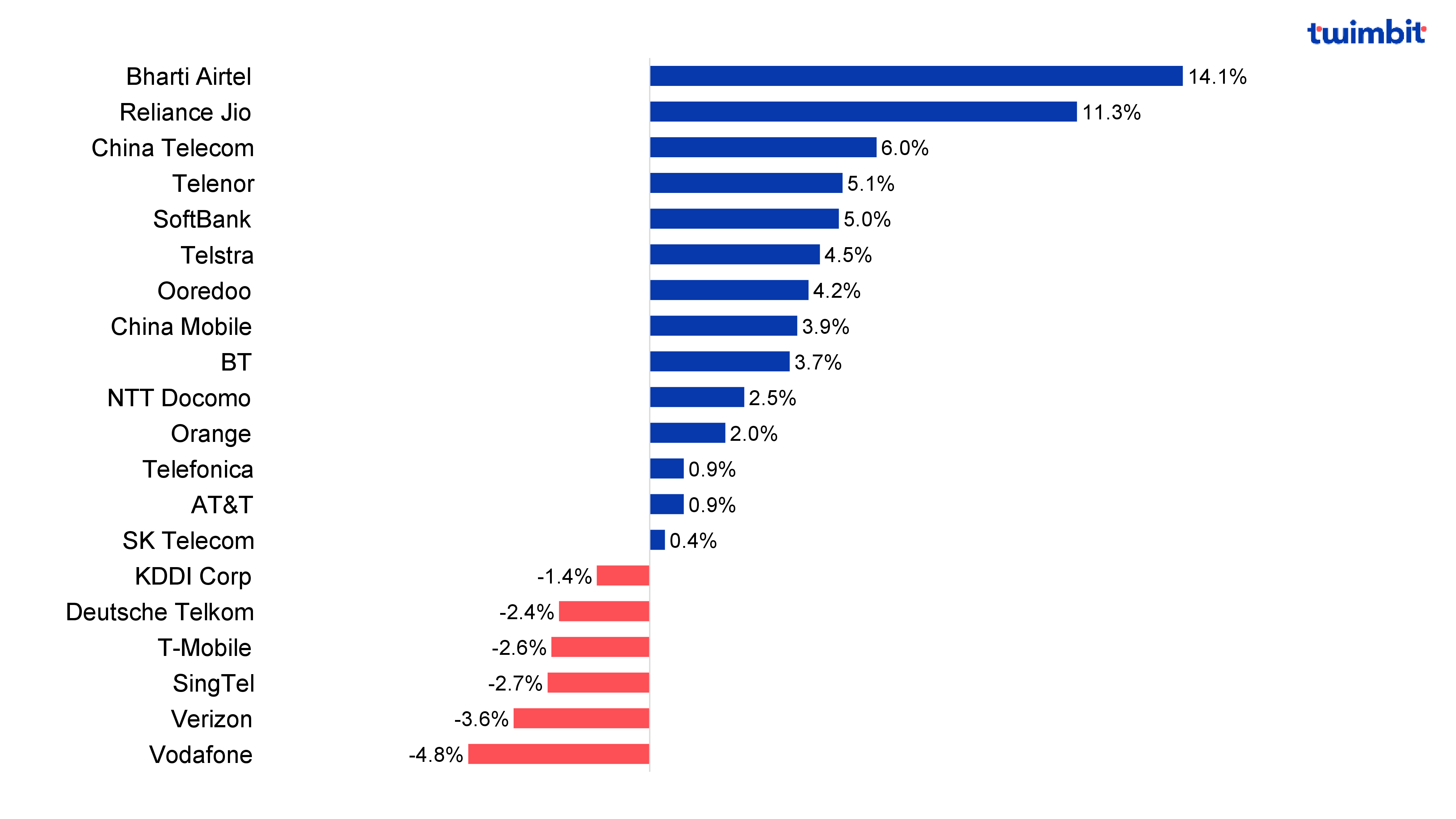

- India’s leading telcos, Bharti Airtel and Reliance Jio, sustained growth momentum with a double-digit revenue growth rate. However, the growth rates were slightly lower compared to previous quarters.

- Telenor revenue grew by 5.1%, driven by mobile service revenues and price adjustments across various markets, while China Telecom and SoftBank achieved revenue growth rates exceeding 5%, driven by their ICT business offerings for enterprise customers.

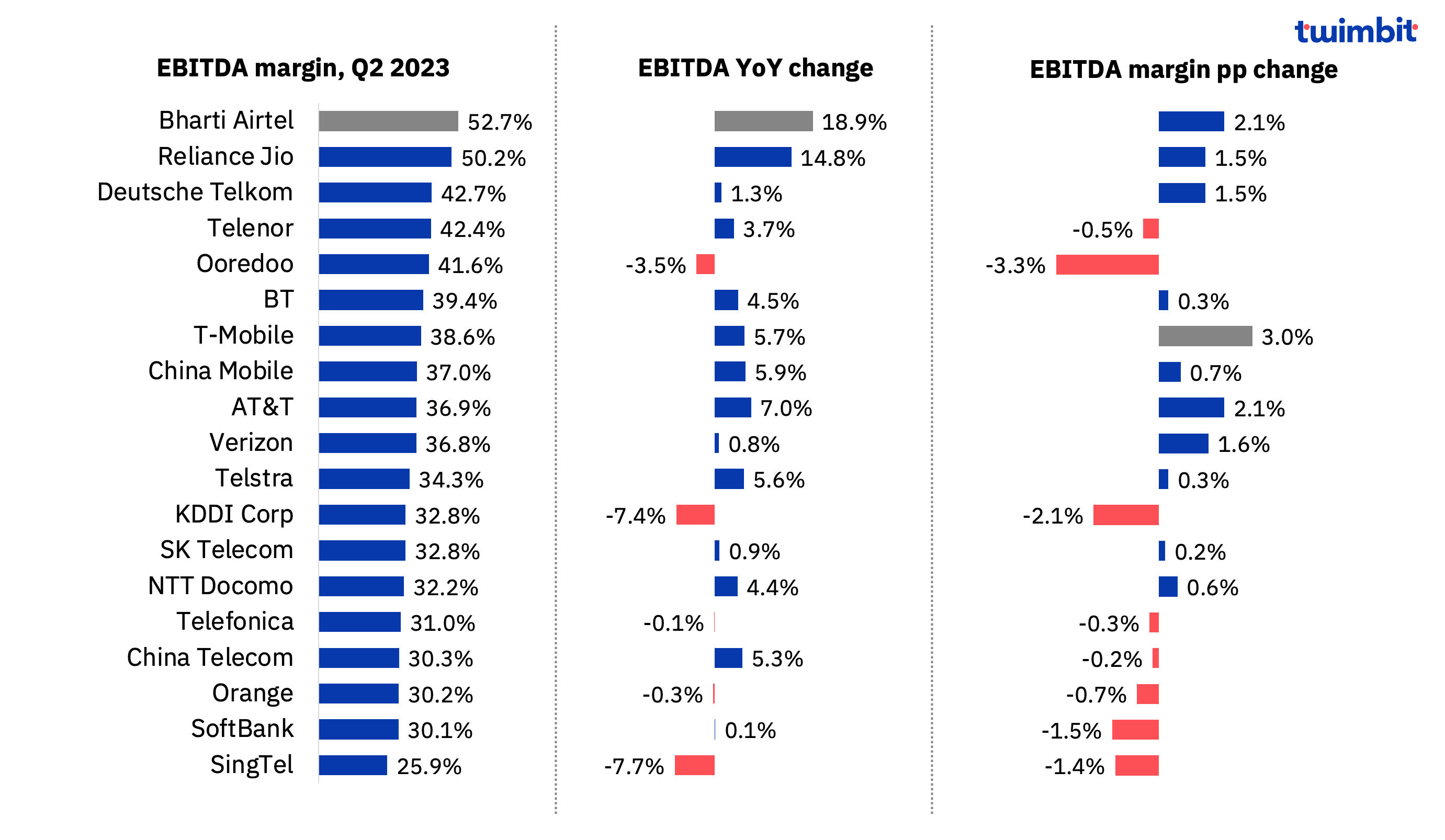

- The top 20 global collectively increased their EBITDA margin by 86 basis points YoY to reach 36.4% in Q2 2023, with Bharti Airtel and Reliance Jio maintaining robust EBITDA margins of more than 50%.

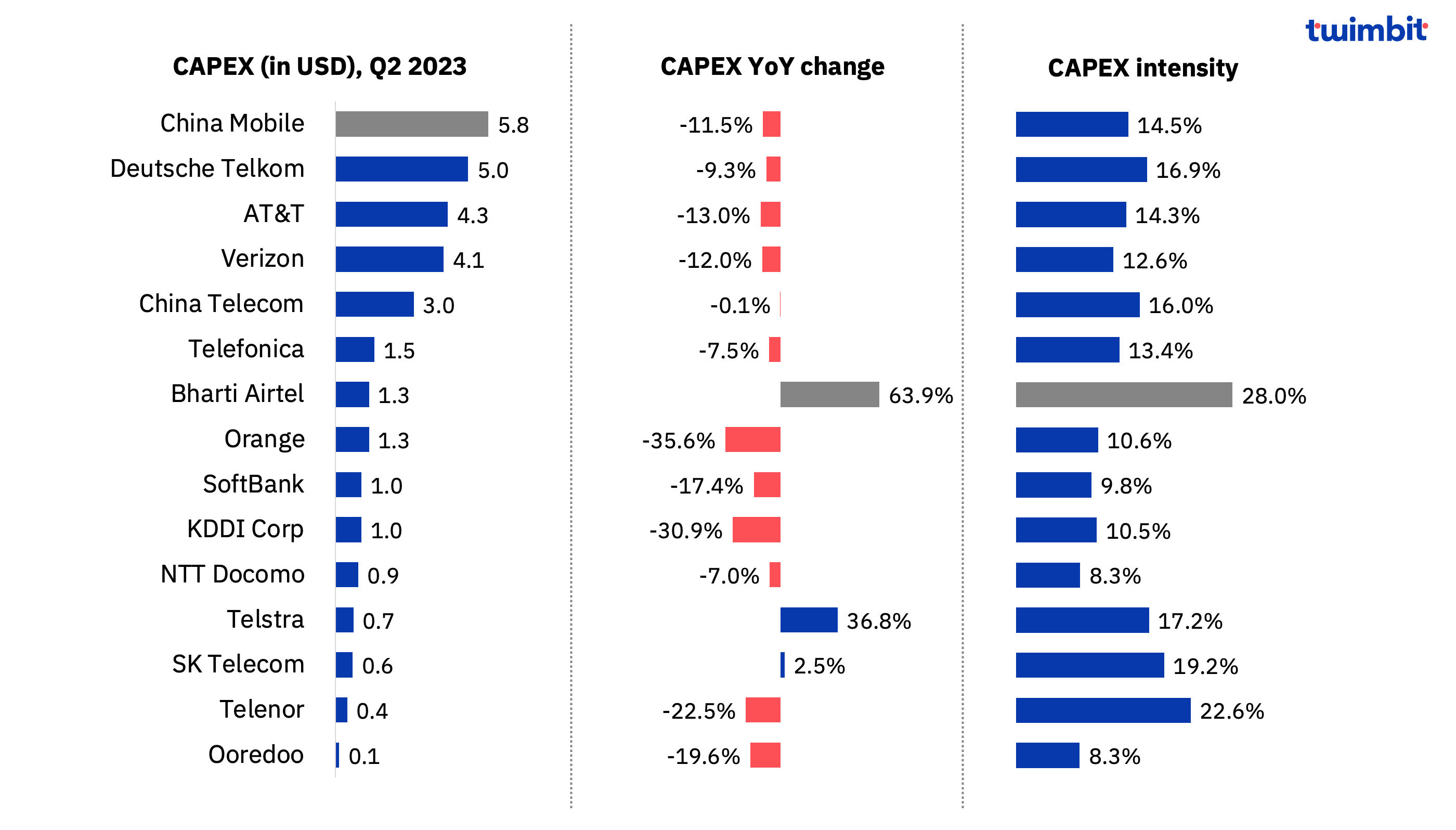

- With 5G deployments peaking in most regions, telcos collectively saw a 180-basis points reduction on a YoY basis in CAPEX spending in Q2 2023, with a few like Bharti Airtel, Telstra and SK Telecom witnessing an increase in CAPEX.

- Most telcos experienced low single-digit ARPU growth, but Bharti Airtel stood out with a significant 9% increase, on account of a favourable subscriber mix and tariff adjustments made between November 2022 and March 2023.

- Telcos formed strategic partnerships with leading vendors like Cisco and NVIDIA in Q2 2023 to drive enterprise solution innovations, IoT connectivity enhancements, and network optimization.

- In June 2023, Vodafone Group Plc and CK Hutchison Group Telecom Holdings Limited (a wholly owned subsidiary of CK Hutchison Holdings Limited) announced the merger of their UK telecommunication businesses. Vodafone will hold a 51% stake in the combined entity, while CK Hutchison will have 49% ownership. The new merged company will intensify competition for the UK’s top two converged operators while simultaneously expanding options for wholesale partnerships.

Financial Performance

India telcos continue to outperform their global peers

In Q2 2023, the top 20 global telcos lost the growth momentum and recorded a low single-digit average revenue growth rate of 1.1% YoY. Notably, ~70% of these telcos showcased an encouraging upward trend, underscoring their resilience and positive outlook. It is worth highlighting that Indian telco achieved impressive double-digit growth, while China Telecom, Telenor, and Softbank reported growth rates exceeding 5% during Q2 2023. However, Vodafone, Singtel, Verizon, T-Mobile, Deutsche Telkom, and KDDI Corp reported a decline in their revenue.

- Indian telcos Bharti Airtel and Reliance Jio, continued growth momentum but at a more modest pace compared to previous quarters.

- In Q2 2023, Bharti Airtel group achieved the highest revenue growth of 14.1% YoY, reaching INR 374 billion (~USD 4.6 billion) backed by strong and consistent performance delivery across the portfolio.

- Its India operations revenues grew 13.1% YoY led by growth of 15.8% YoY in the business segment, fuelled by robust demand for data and connectivity-related solutions.

- Bharti Airtel homes business segment also continued its growth impetus, up by 25.4% YoY, which was led by new customer acquisitions.

- Additionally, it also witnessed substantial growth in mobile services revenues, which increased 12.4% YoY, on account of strong 4G customer additions and an increase in ARPU also boosted overall revenue.

- Reliance Jio achieved 11.3% YoY revenue growth in Q2 2023 to reach INR 261 billion (USD 3.2 billion) driven by 9.2 million net subscriber additions.

- The growth was driven by a 5G customer acquisition plan with increased investment in True5G to complete a pan-India 5G rollout by December 2023.

- Furthermore, the launch of the JioBharat phone in Q2 2023 played a pivotal role in advancing its ‘2G-MUKT BHARAT’ vision and driving the customer acquisition plan.

- In Q2 2023, Bharti Airtel group achieved the highest revenue growth of 14.1% YoY, reaching INR 374 billion (~USD 4.6 billion) backed by strong and consistent performance delivery across the portfolio.

- China Telecom revenue increased by 6% YoY in Q2 2023, to reach CNY 130 billion (~USD 18.6 billion).

- This growth was driven by a 6.6% increase in mobile service revenue and a 16.4% rise in industrial digitization revenue on a YoY basis in H1 2023.

- Telenor reported a revenue growth of 5.1% in Q2 2023 to reach NOK 20.2 billion (~USD 1.9 billion).

- The growth was driven by an increase in mobile service revenues, which grew by 5% and was supported by price adjustments in all markets mainly in Asia, and increased subscriber base in Sweden and Finland.

- Asia service revenues for Telenor increased by 5% YoY, primarily driven by increased data usage and price adjustments in Grameenphone.

- Moreover, the Group’s service revenue growth was supported by good development in Telenor Maritime and the IoT provider Telenor Connexion in Amp.

- Softbank reported revenue growth of 5% to reach JPY 1.4 trillion (~USD 10.4 billion) in Q2 2023. This growth was driven by a steady growth of ICT business for enterprise customers by 9.2%.

- Despite a 5.5% increase in postpaid service revenue, T-Mobile’s, total revenue declined by 2.6% primarily due to a decline of 23.3% in its equipment revenue. Its equipment sales revenue declined by 17.2% and lease revenue declined by 82.1% in Q2 2023.

- The decline in equipment revenue can be attributed to the lower number of devices sold primarily driven by higher postpaid upgrades related to Sprint customers moving to devices that are compatible with the T-Mobile network

- The longer device lifecycles, and lower prepaid sales in Q2 2023 also impacted the equipment revenue.

- SingTel’s revenue declined by 2.7% YoY in Q2 2023 reaching SGD 3.5 billion (~USD 2.6 billion).

- This decline can be attributed to a 21% YoY drop in Singtel Singapore TV revenue coupled with a 7.1% YoY decline in fixed voice revenue impacted the overall revenue.

- Additionally, challenges in the legacy carriage business by SingTel Singapore had an impact on overall revenue.

- For Q2 2023, despite an increase of USD 204 million in service revenue, Verizon’s revenue declined by 3.6% YoY, primarily attributed to the decline in its wireless equipment revenue by 21.7%.

- Vodafone revenue declined by 4.8% YoY in Q2 2023, due to a decline in its revenue in Germany, Spain, and Italy. However, Vodafone revenue grew by 5.7% in the UK, but could not offset the overall revenue decline.

- Also, in June 2023, Vodafone Group Plc and CK Hutchison Group Telecom Holdings Limited (a wholly owned subsidiary of CK Hutchison Holdings Limited) announced to merge their UK telecommunication businesses.

- Vodafone will hold a 51% stake in the combined entity, while CK Hutchison will have 49% ownership.

- The new combined entity will invest GBP 11 billion (~USD 13.8 billion) in the UK over ten years to create one of Europe’s most advanced standalone 5G networks, in full support of UK Government targets.

- The merger will establish a third operator, enhancing market competition and balancing the playing field. This merger will intensify competition for the UK’s top two converged operators while simultaneously expanding options for wholesale partnerships among the already competitive MVNOs in the UK.

- This new combined entity will cover more than 99% of the UK population with its 5G standalone network, delivering to customers up to a six-fold increase in average data speeds by 2034.

- Also, in June 2023, Vodafone Group Plc and CK Hutchison Group Telecom Holdings Limited (a wholly owned subsidiary of CK Hutchison Holdings Limited) announced to merge their UK telecommunication businesses.

Exhibit 2: Revenue trends (% change) YoY basis, Q2 2023

Note: Bharti Airtel, Deutsche Telkom, Ooredoo Singtel, Telenor, and Vodafone group performance is considered for the report

EBITDA Performance

Combined EBITDA margin for top 20 global telcos grow to reach 36.4%

The top 20 telcos recorded a combined increase of 86 basis points on a YoY basis in their EBITDA margin to reach 36.4% in Q2 2023. Leading Indian telcos Bharti Airtel and Reliance Jio, maintained a robust EBITDA margin above 50%, showcasing their strong financial performance. Meanwhile, Telenor and China Telecom reported an increase in EBITDA on a YoY basis but reported a decline in its EBITDA margin by 50 basis points and 20 basis points respectively.

- Bharti Airtel Group’s EBITDA increased by 18.9% YoY in Q2 2023 to reach INR 197.4 billion (USD 2.4 billion). EBITDA margin improved by 212 basis points to 52.7% in Q2 2023.

- The increase in EBITDA margin was driven by their “War on Waste” cost optimization program, which successfully reduced operating expenses, leading to improved EBITDA margin.

- Reliance Jio’s EBITDA margin grew from 48.7% (Q2 2022) to 50.2% (Q2 2023), with EBITDA up 14.6% YoY in Q2 2023 to a total of INR 131.1 billion (USD 1.6 billion).

- Despite a 9% YoY rise in total expenses, consistent subscriber additions and ARPU growth boosted its operating revenue, which enabled it to achieve a better EBITDA margin.

- Deutsche Telkom EBITDA margin improved by 150 basis points to 42.7%, on account of increased revenue in Germany and Europe.

- SingTel group reported a 7.7% YoY decline in EBITDA to SGD 902 million (USD 673.5 million) in Q2 2023, due to inflationary cost pressures.

- Their EBITDA margin decreased by 1.4 percentage points to 25.9%, owing to an increase in operating expenses, which was impacted by higher maintenance, staff, and administrative costs from Digital InfraCo.

- EBITDA for KDDI Corp declined by 7.4% YoY in Q2 2023, due to increased cost of sales and selling, general and administrative expenses by 1.9% each on a YoY basis in Q2 2023. Its operating revenue declined by 1.4% YoY, which resulted in a decrease of 10.3% in its operating income. As a result, EBITDA margin declined by 210 basis points in Q2 2023 to reach 32.8%.

- For Q2 2023, Ooredoo Group’s EBITDA declined mainly due to a decline in its EBITDA margin in Qatar and Oman operations by 500 basis points and 550 basis points respectively.

- EBITDA margin for Qatar declined in Q2 2023, due to bad debt and competitive pressure.

- Oman’s EBITDA was impacted by a lower gross margin and higher OPEX. There is an ongoing evaluation of the cost structure, to improve efficiency in the operation.

Exhibit 3: EBITDA performance, Q2 2023

Note: Bharti Airtel, Deutsche Telkom, Ooredoo Singtel, Telenor, and Vodafone group performance is considered for the report

CAPEX Performance

CAPEX spending slows down, as the 5G network reaches peak coverage

As 5G adoption reached its peak in specific areas during 2022, it comes as no surprise that telecommunications companies witnessed a 180-basis point reduction in their CAPEX spending, dropping to 14.1% in Q2 2023. This decline underscores the industry’s commitment to aligning investments more effectively with market demands. Only three telcos, Bharti Airtel, Telstra, and SK Telecom reported an increase in CAPEX spending on a YoY basis. Major CAPEX decline was observed for Orange, Ooredoo, KDDI Corp, Telenor, and Soft Bank.

- Bharti Airtel group reported an increase of 63.9% YoY in CAPEX spending in Q2 2023 to reach INR 104.8 billion (~USD 1.3 billion). This increase is attributed to its plans to roll out 5G in India.

- India operations reported an increase of 76.4% YoY in CAPEX spending in Q2 2023, reaching INR 93.2 billion (USD 1.1 billion). Africa operations reported an increase of 5.7% YoY to reach INR 11.5 billion (~USD 140 million), while South Asia operations CAPEX declined by 60.6%.

- The telco expanded its network coverage in India by rolling out 9,200 new towers, showcasing its commitment to delivering an exceptional network experience, which is evident in its investment, which includes adding 38,600 towers YoY.

- Telstra’s CAPEX spending increased by 36.8% to reach AUD 1 billion (~USD 675 million) in Q2 2023.

- This growth is attributed to its investment in 5G, to facilitate it in reaching 5G population coverage to 85% and achieving 41% of its mobile traffic on its 5G network.

- Telstra’s new intercity fibre project, which possesses strong interest from hyper‐scalers, other operators, satellite providers, and national enterprises, also fuelled the increased CAPEX spending by Telstra.

- CAPEX for Orange reported a significant decline of 35.6% YoY in Q2 2023, as 5G and FTTH deployment peak passed in 2022. Similarly with the completion of 5G coverage deployment CAPEX for Soft Bank and Telenor declined 17.4% and 22.5% respectively in Q2 2023.

- Ooredoo’s CAPEX spending declined by 19.6%, resulting in a CAPEX intensity decrement of 200 basis points to reach 8.3% in Q2 2023.

- Except for Iraq and the Maldives, Ooredoo faced a decline of more than 20% in CAPEX spending in almost all the regions, while Myanmar operations reported a decline of 48.3% in Q2 2023. However, Iraq and Maldives operations reported growth in CAPEX spending by 28.9% and 47% respectively but were unable to offset the overall decline.

Exhibit 4: CAPEX performance, Q2 2023

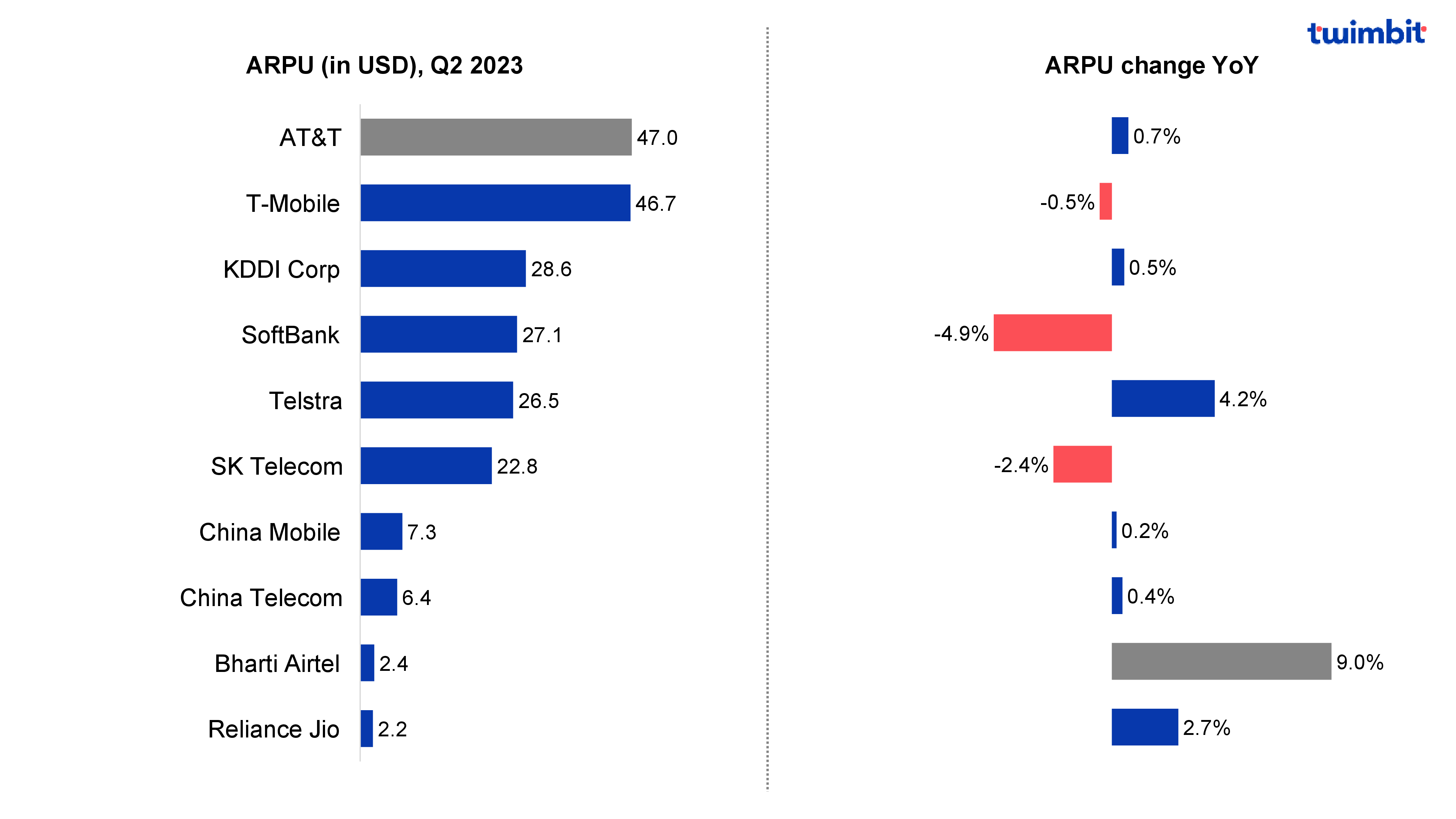

ARPU Performance

Indian telcos sustain ARPU growth, while US telcos maintain the highest ARPU

Most telcos witnessed a single-digit increase in ARPU, except for Soft Bank, KDDI Corp, SK Telecom and T-Mobile. The Indian telcos reported a significant increase in ARPU levels in 2022, and the growth momentum continued in 2023 as well. In Japan, the impact of tariff reduction and regulatory pressure impacted telcos ARPU but is expected to diminish, with growth anticipated from early next year.

- Indian telcos continued to experience the positive impact of the tariff adjustments made in November and December 2021, increasing ARPU. Indian telcos have set ambitious targets to raise their ARPU to INR 250 (~USD 3.1) by 2025, to be driven by a better subscriber mix.

- Jio witnessed a single-digit growth in ARPU by 2.7% in Q2 2023 to reach INR 180.5 (~USD 2.2), primarily attributed to the heightened data usage associated with the introduction of 5G technology.

- Airtel achieved a significant 9% YoY increase in ARPU in Q2 2023 to reach INR 200 (~USD 2.4), the highest growth rate among the top 20 global telcos included in this analysis. This exceptional growth was facilitated by a more favourable subscriber mix, with an influx of postpaid customers during the quarter. Additionally, Airtel reaped the full benefits of its tariff adjustments initiated from November 2022 to March 2023.

- Telstra witnessed an increase in Postpaid ARPU by 6.1% to reach AUD 51.7 (~USD 34.5) primarily driven by price rises and higher international roaming, while its Prepaid ARPU declined by 2.1% to reach AUD 24.7 (~USD 16.5) in H1 2023 (Jan 2023 – June 2023).

Exhibit 5: ARPU trends, Q2 2023

Note:

1. ARPU for Bharti Airtel is for India operations only

2. ARPU for T-Mobile is calculated using [(Postpaid ARPU * Postpaid Subscribers) + (Prepaid ARPU * Prepaid subscribers) \ (Postpaid subscribers + Prepaid Subscribers)]

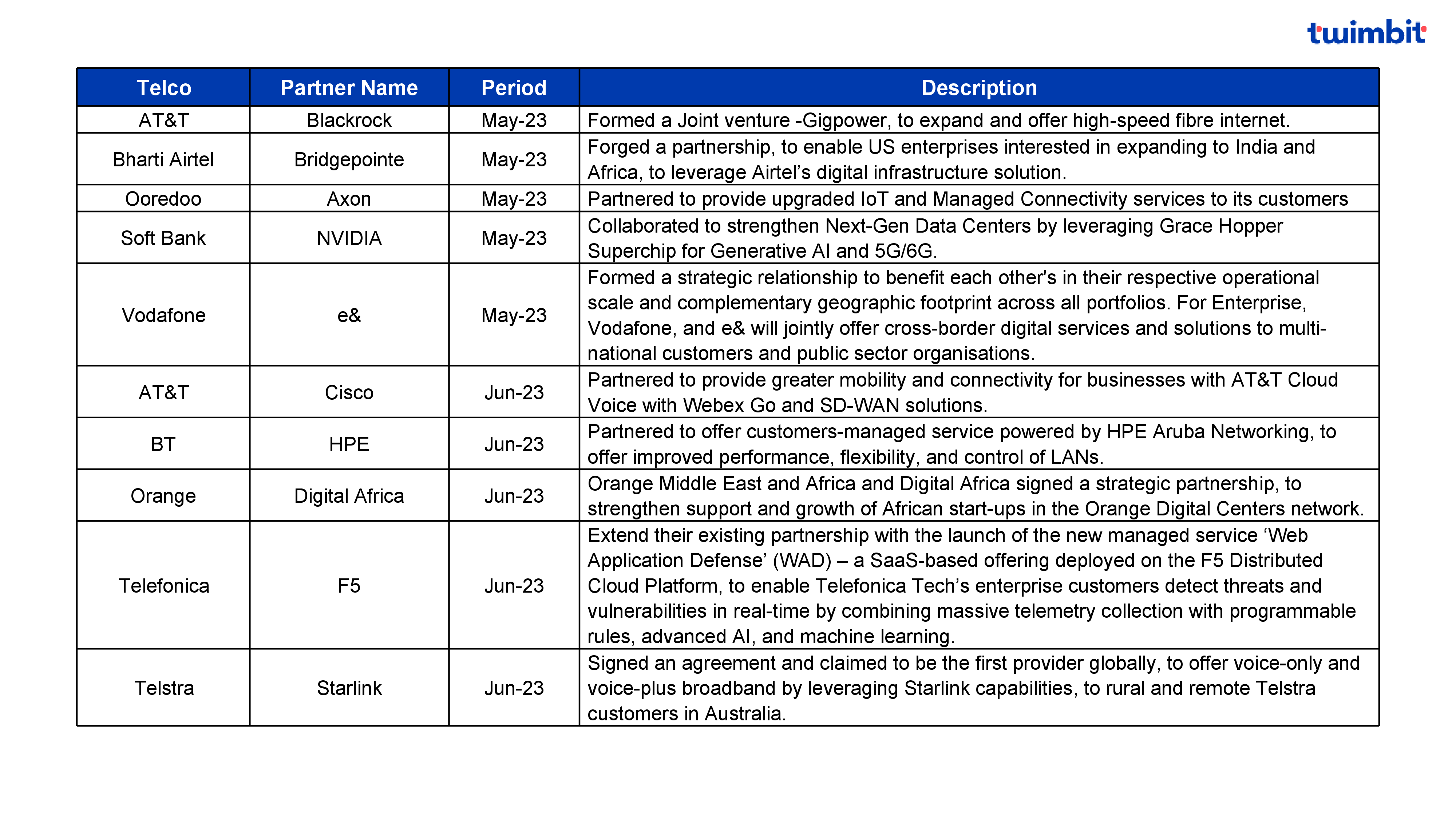

Key Partnership

Telcos formed strategic partnerships to drive enterprise solutions

Exhibit 6: Key partnership, Q2 2023

Research Methodology and Assumptions

- Data collection has been done leveraging secondary research methodologies and the information provided by the respective telcos. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period Jan-Mar of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value for the period April-June 2023.

- The report analyses revenue and EBITDA for 20 and 19 telcos respectively, as Vodafone doesn’t report EBITDA every quarter. Additionally, for CAPEX and ARPU, the analysis is for 15 and 10 telcos respectively.

- Telstra reports on a half-year basis. Hence, for the analysis, an average of the half-yearly reported numbers has been taken with equal weightage to the underlying quarters, to derive the quarterly numbers. As a result, Telstra is not part of our Q1 and Q3 analysis for the current and previous years.

- Bharti Airtel, Deutsche Telkom, Ooredoo Singtel, Telenor, and Vodafone group performance are considered in this report.

- Blended mobile ARPU is considered for the analysis, wherever applicable.

Thank you for reading! Reach out to us for any feedback

You might also like:

APAC telco update – Q2 2023

Cloud stories – Q2 2023

Global Telecom vendors – Q2 2023

Indonesia Telecom Update 2023

Japan telecom market update