High base year effects and a slowdown in merchandise export growth have proven challenging for Malaysia’s overall economic growth, evident with its 2.9% year-on-year decline in Q2 2023. In the second quarter of 2022, Malaysia’s GDP experienced a remarkable surge of 8.8% YoY. This subsequently led to elevated base year effects influencing the YoY GDP growth rate in the second quarter of 2023.

The top nine banks in Malaysia recorded an average growth of 6.54% in their loan portfolio from USD 49.7 billion in Q2 2022 to USD 53 billion in Q2 2023. The growth was mainly driven by mortgage and hire purchase financing. On the other hand, deposits grew by 5.32% from USD 54.8 billion in Q2 2022 to USD 57.8 billion in Q2 2023

Malaysian banks are still new to open banking. However, banks like Maybank and CIMB have recently launched their developer portals which give developers access to the bank’s APIs. This initiative aims to create innovative financial solutions and services.

Fintech partnerships in Malaysia are on the rise, as both established financial institutions and fintech start-ups recognize the benefits of working together. Some of the notable fintech partnerships in Malaysia are:

- CIMB and Grab – Offers a range of financial products and services to Grab customers, including co-branded credit cards.

- RHB and Fave – Offers a personalised financial management app to track spending, budget and invest.

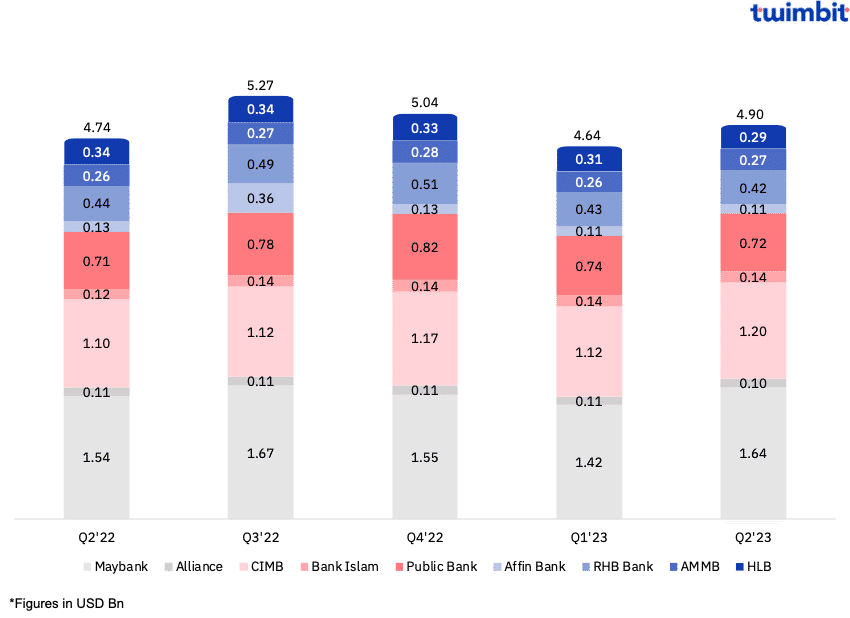

Net revenues for the top 9 banks in Malaysia grew by 3.4% YoY

The top 9 banks in Malaysia grew from USD 4.74 billion in Q2 2022 to USD 4.9 billion in Q2 2023.

CIMB reported the highest YoY growth rate at 9.17%, increasing net revenues from USD 1.1 billion in Q2 2022 to USD 1.2 billion in Q2 2023. This growth was driven by a 39% increase in non-interest income from USD 272 million in Q2 2022 to USD 389 million in Q2 2023. The major contributor towards this increase were the bank’s trading and FX income which grew by 103% from USD 93 million in Q2 2022 to USD 189 million in Q2 2023.

HLB reported the highest YoY decline at 12.95%, decreasing net revenues from USD 336 million in Q2 2022 to USD 293 million in Q2 2023. This was primarily attributed to a decline in net interest income by 6% from USD 260 million in Q2 2022 to USD 245 million in Q2 2023. Fee income also declined by 5.2% from USD 35 million in Q2 2022 to USD 33 million in Q2 2023.

Exhibit 1: Net revenues of the top 9 Malaysian banks

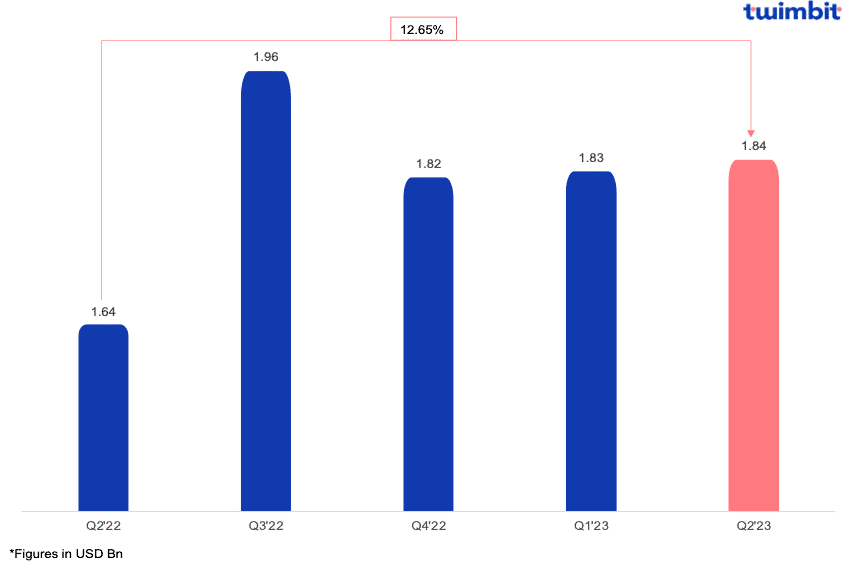

Net profits for the top 9 banks in Malaysia grew by 12.65% YoY

The top 9 banks in Malaysia aggregated their net profits from USD 1.64 billion in Q2 2022 to USD 1.84 billion in Q2 2023.

On average, the top 3 Malaysian banks were Maybank, CIMB and Public Bank, which led the chart with an average net profit of USD 1.29 billion in Q2 2023. Individually, Maybank, CIMB and Public Bank net profits grew by 26%, 15% and 14% respectively.

On the other hand, Alliance Bank reported the highest decline in its net profits at 29% followed by Affin Bank at 28%.

Exhibit 2: Consolidated net profits of the top 9 Malaysian banks

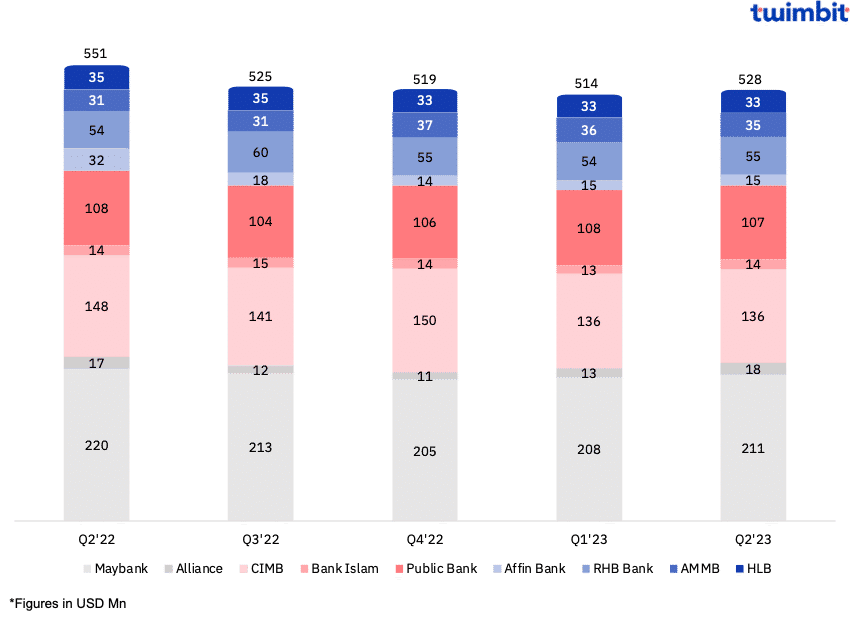

Fee income for the top 9 banks in Malaysia declined by 5.42% YoY

The top 9 banks in Malaysia witnessed a decline in fee income from USD 551 million in Q2 2022 to USD 528 million in Q2 2023.

Ambank Malaysia reported the highest increase in fee income at 11.7% YoY, from USD 31 million in Q2 2022 to USD 35 million in Q2 2023. This growth was due to the following:

- Corporate advisory fees grew by 53% from USD 0.8 million to USD 1.23 million.

- Portfolio management fees grew by 77% from USD 2.3 million to USD 4.1 million.

- Bancassurance fees grew by 227% from USD 0.58 million to USD 1.9 million.

Affin Bank reported the highest decline of 16.1% YoY, in its fee income from USD 32 million to USD 27 million. This decline was due to the following:

- Stockbroking service fees declined from USD 3.95 million to USD 0.7 million, representing an 82.4% decline.

- Wealth management fees declined from USD 3 million to USD 1.68 million, representing a 43.6% decline.

- Advisory service fees declined from USD 0.63 million to USD 0.04 million, representing a 93% decline.

Exhibit 3: Fee incomes of the top 9 banks in Malaysia

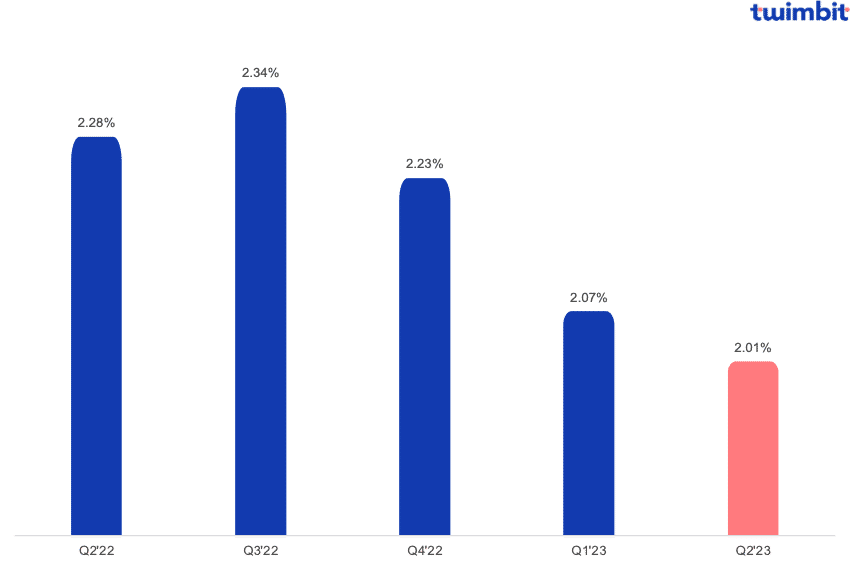

Net interest margins (NIM) declined by 27 basis points in Q2 2023

The average NIM dropped from 2.28% in Q2 2022 to 2.01% in Q2 2023. Malaysian banks tend to have lower NIM when compared to the APAC average of 3.16% in Q2 2023.

As of Q2 2023, none of the banks reported an increase in NIM, with Affin Bank reporting the highest decline from 1.99% to 1.57%.

Exhibit 4: Consolidated net interest margins of the top 9 banks in Malaysia

The declining NIMs in Malaysia are due to the following factors:

- Rising funding costs – The overnight policy rate (OPR) in Malaysia has been raised by 100 basis points from 2% to 3%. This has led to higher funding costs for banks, as they have to pay more interest on deposits.

- Competition for deposits – Banks are competing for deposits, especially in the current rising interest rate environment. This is putting downward pressure on deposit rates, which is squeezing the banks’ margins.

- Slowing loan growth – Loan growth is expected to slow further in 2023, due to the rising interest rate environment. This will reduce the banks’ interest income and further decline their NIMs.

These factors, if left unchecked, could pose a potential issue towards the profitability of Malaysian banks moving forward.

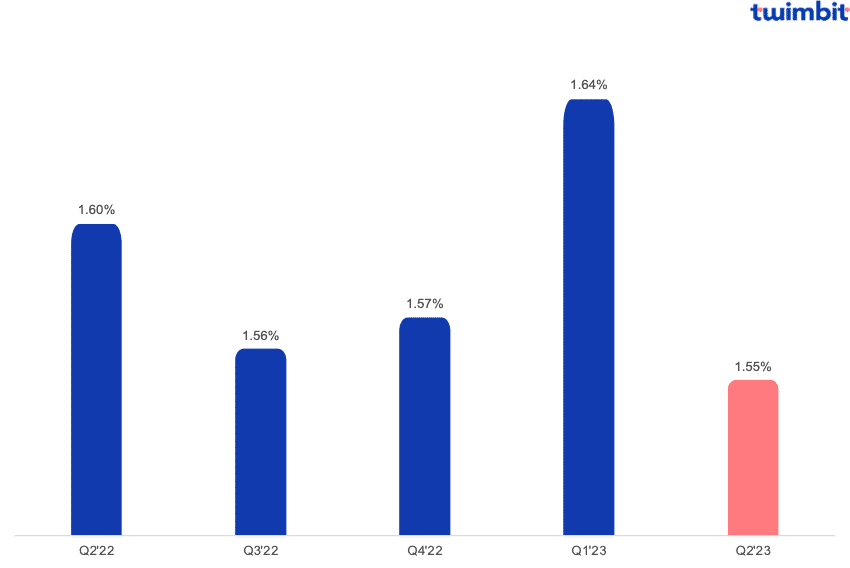

NPLs for the top 9 banks in Malaysia decline by 5 basis points

The top 9 banks in Malaysia reported a decline in average non-performing loans, from 1.60% in Q2 2022 to 1.55% in Q2 2023, which is below the APAC average of 1.9%.

Six of the nine banks analysed reported declining NPLs with Affin Bank reporting the highest decline at 22% from 2.28% in Q2 2022 to 1.78% in Q2 2023.

Alliance Bank reported the highest growth in its NPLs in Q2 2023, with a growth of 46.1% YoY, from 1.8% in Q2 2022 to 2.63% in Q2 2023.

HLB and RHB reported an increase of 16.3% and 1.2% respectively. However, their current NPLs are very low at 0.57% and 1.64%.

Exhibit 5: Consolidated non-performing loans of the top 9 Malaysian banks

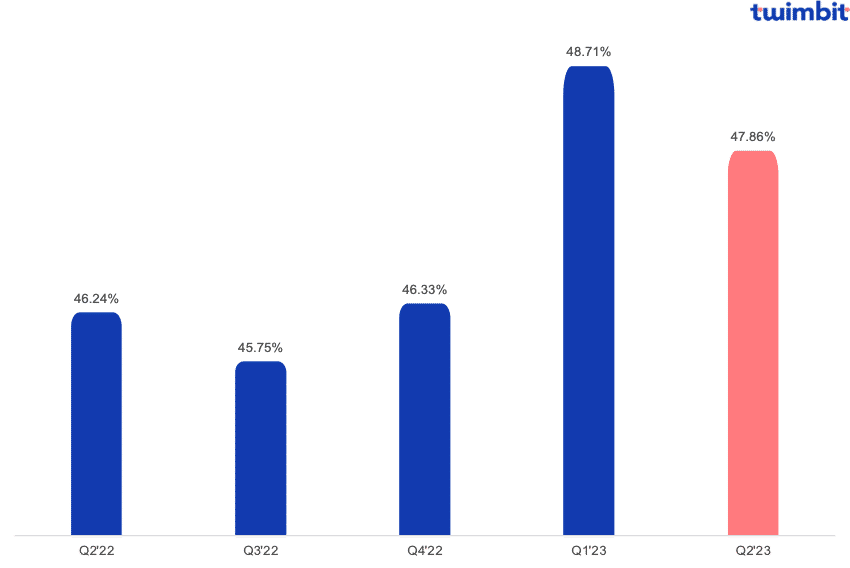

Cost efficiency for the top 9 banks in Malaysia declined by 162 basis points between Q2 2022 and Q2 2023

The average cost efficiency for the top 9 banks in Malaysia stood at 47.86% in Q2 2023, above the APAC average of 42% in Q2 2023. This indicates a lack of operational efficiency in Malaysian banks as compared to their APAC peers.

Exhibit 6: Consolidated cost-efficiency ratio of the top 9 banks in Malaysia

Of the nine banks analysed, only Ambank and CIMB have been able to improve their cost efficiency by 20 and 90 basis points respectively.

Bank Islam and Affin Bank reported a cost-efficiency ratio of 59.6% and 64.7%, respectively. All the other banks have their cost efficiency ratio below the threshold value with Public Banks leading with an impressive ratio of 33.7%.

This lack of operational efficiency could stem from the compressions in net interest margins, resulting in elevated cost-efficiency ratios for these banks.

Initiatives by the top banks in Malaysia

- #1 Public Bank

Payment ecosystem:

- Public Bank became the first Malaysian bank to launch DuitNow online banking/wallets and QR-based cross-border payments.

- Public Bank accepted QR international payments from Indonesia, Singapore and Thailand.

Empowering SMEs:

- The bank has partnered with digital solution providers in the PB Enterprise Digital SME Assist program.

- The partnership offers customers various digital business solutions, including human resource management, property management, and cloud-based accounting and payroll solutions.

- #2 HLB

CX Lab:

- Promotes cross-departmental cooperation with conducive settings for product idea generation and prototyping.

- Gathers insights through various techniques, including A/B testing, gaze tracking, quantitative research, ethnographic research, and qualitative research.

- Enables the Lab to evaluate and act upon comprehensive consumer insights to better address consumer needs.

- In FY2022, the Lab ran:

- 27 customer research projects

- 59 usability testing sessions

- 13 post-launch evaluation initiatives

- #3 Maybank

Open Banking:

- Launched its Maybank Sandbox, a developer portal that offers access to Maybank’s APIs.

- It enables developers to build and test their applications using Maybank’s banking data and services.

- Maybank generated USD 866.4 million from fee-based income in FY22, where 46% of it is contributed by service charges and fees.

- #4 CIMB

CIMB Octo:

- The bank launched its first fully digital savings account and introduced the CIMB Octo Debit Mastercard as part of its strategy to expand the CASA base.

- The account opening and onboarding process is conducted entirely online under five steps.

- Customers receive their debit cards directly through the mail, offering a convenient branchless experience.

- Users can engage in a gamified experience, complete with missions and challenges, allowing them to earn points and receive instant rewards.

Open Banking:

- Launched its open banking platform called CIMB Developer Portal.

- The portal provides developers with access to CIMB’s APIs, allowing them to create innovative financial solutions and services that leverage CIMB’s banking capabilities.

- CIMB fee income contributes to around 10.5% of total revenue, generating USD 665 million in FY22.

- #5 RHB

Open Banking:

- Launched its RHB Fintech & Innovation Lab, collaborating with Fintechs and startups to develop new digital solutions and services.

- This initiative includes exploring opportunities in open banking and fostering partnerships with third-party providers.

- RHB fee-based income stood at USD 230 million in FY22.

The Malaysian banking sector remains steady against global headwinds in Q2 2023

Despite the ascent of interest rates, inflation and increased competition from fintech, the Malaysian banking sector continues to display resilience even amidst economic uncertainties. Overall, the Malaysian banking industry’s prospects appear optimistic, with predictions to sustain profitability and experience growth in the forthcoming years.

To learn more about how the top banks in APAC performed in Q2 2023, click here.

To learn more about how the leading 8 banks in India performed in Q2 2023, click here.

To learn more about how the top banks in Indonesia performed in Q2 2023, click here.

To learn more about how the top banks in the Philippines performed in Q2 2023, click here.