Introduction

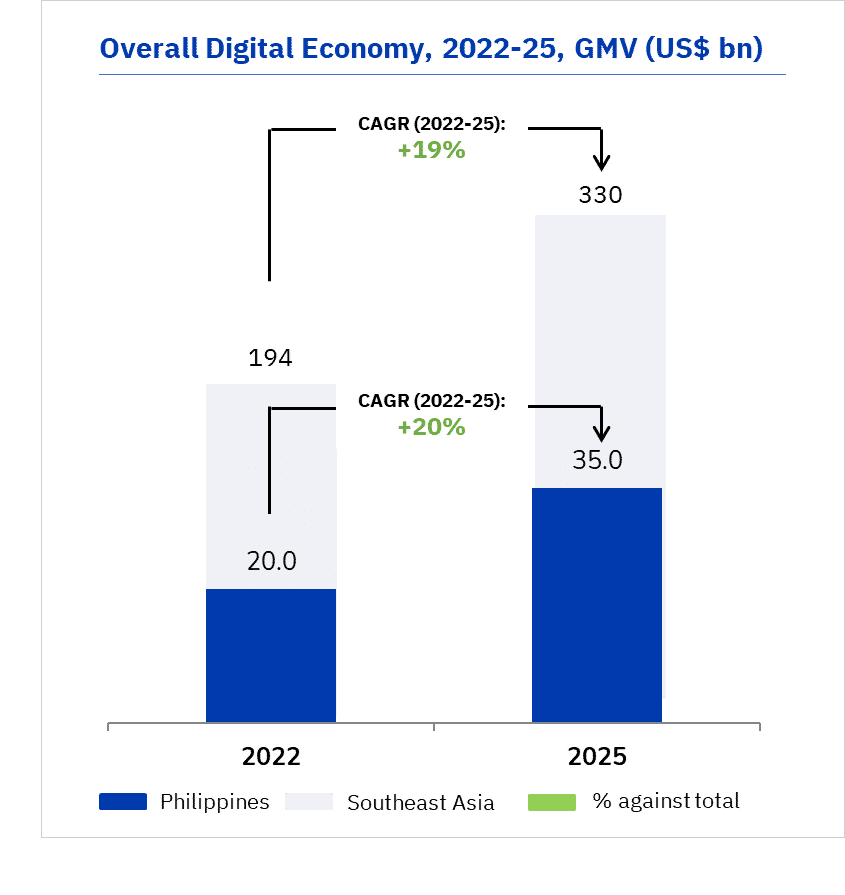

The digital economy in the Philippines is experiencing remarkable growth, boasting a Compound Annual Growth Rate (CAGR) of 20%. With a surge in consumer penetration of digital services and the rise of digital financial services (DFS), the landscape of the financial sector is undergoing significant transformation. Traditional banks are finding themselves amid intense competition, as digital banks equipped with innovative technology are emerging as powerful contenders. This report will delve into this digital revolution and explore how traditional banks are adapting to these changes.

Overall digital economy of the Philippines

Source: e-Conomy SEA 2022 by Google, Temasek, Bain & Company, Twimbit analysis, 2023

The rise of digital financial services

The digital financial services (DFS) sector in the Philippines is poised for continued growth. This encompasses a broad range of services, including mobile payments, digital wallets, and online lending, which are reshaping the financial industry.

- DFS is expected to sustain growth with lending hitting USD 8 billion by 2025 at a CAGR of 53% between 2022 and 2025

- Remittances to also have a gross transaction value of USD 8 billion by 2025 growing with a CAGR of 25%

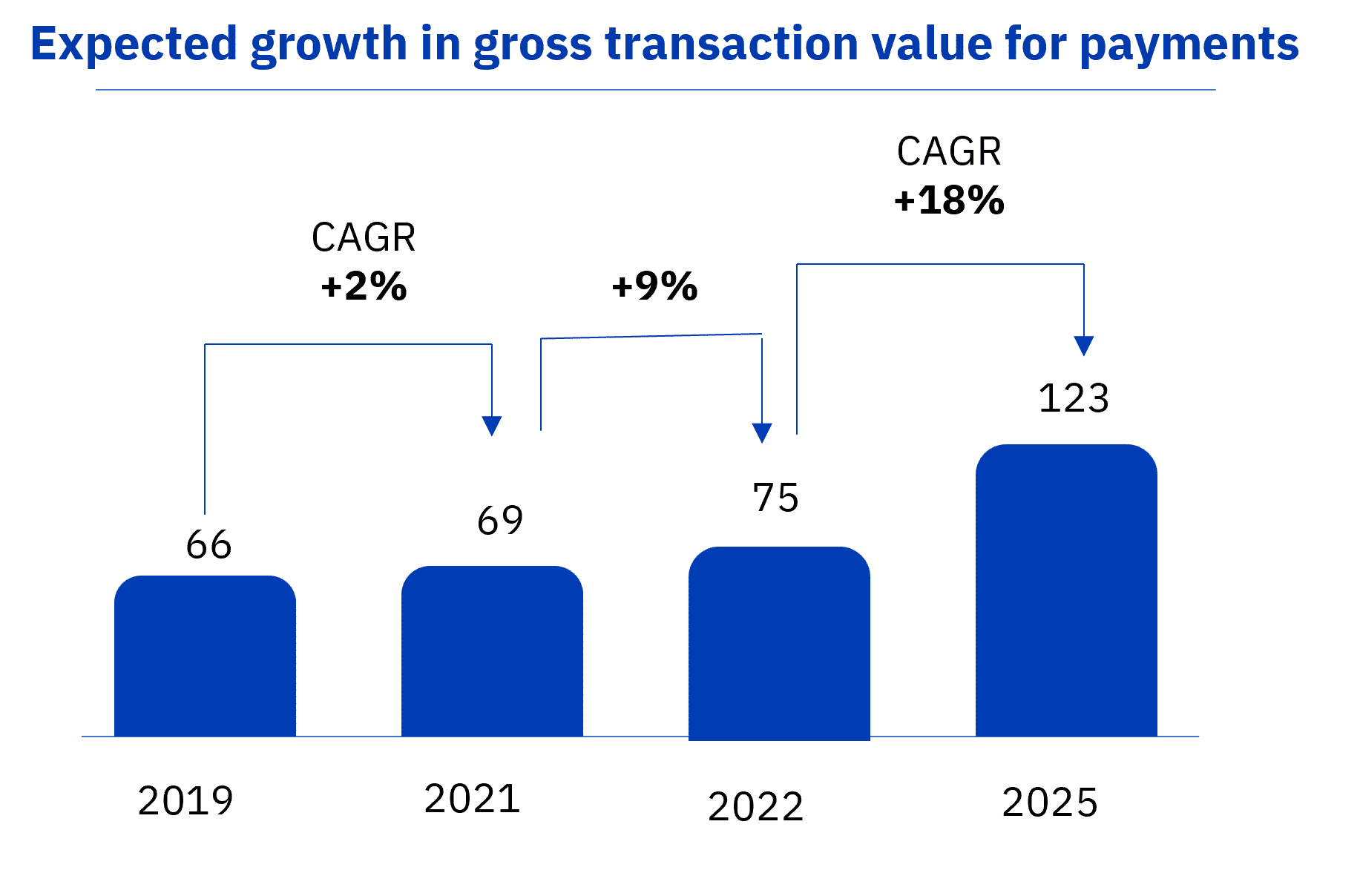

- Payments gross transaction value to reach USD 123 billion by 2025 at a CAGR of 18%

DFS sector is poised for continued growth

Source: : Google – commissioned Ipsos e-Conomy SEA research, Twimbit analysis

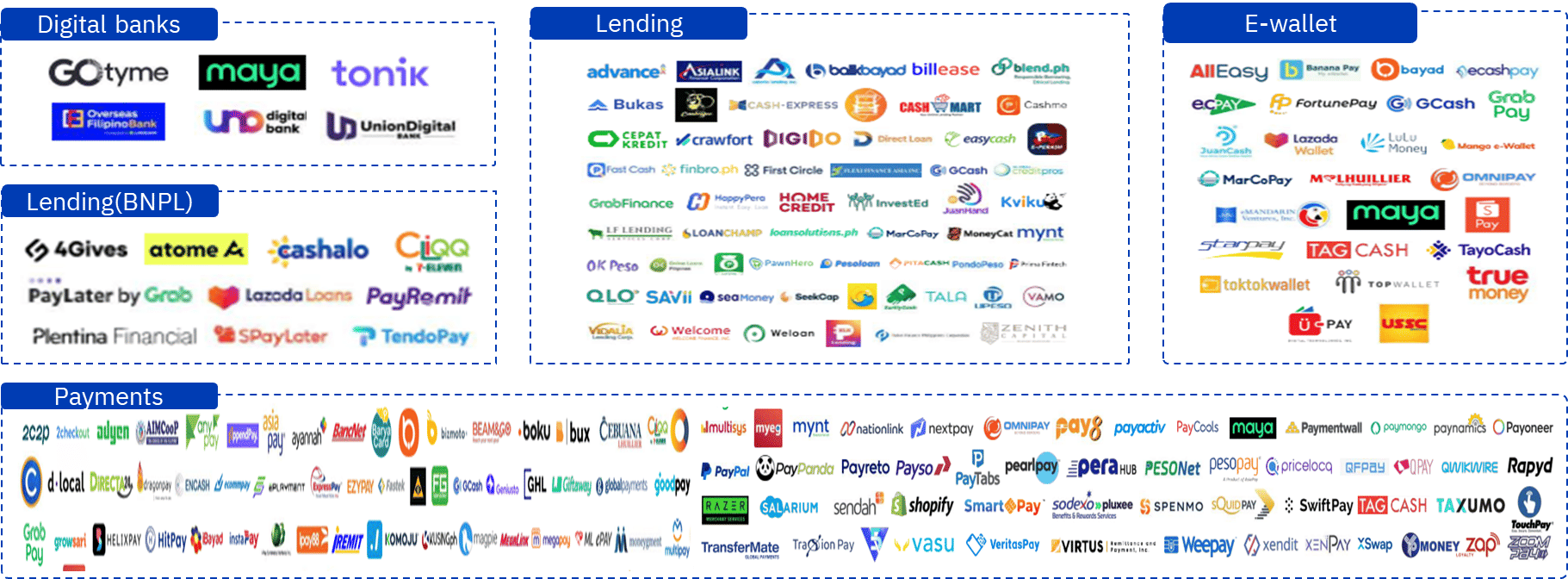

DFS industry faces intensified competition

The DFS industry is undergoing fierce competition, with various players vying for market share. Digital-only banks have entered the scene, offering innovative and convenient solutions that challenge traditional banking models.

Among the 285 fintech applications in the Philippines, digital banking and e-wallets are the most prominent, constituting 18.8% and 15.5% of the total, respectively. Payments and transfers follow at 11.9%, with wealth management at 9.9%, and digital lending at 9.6%.

E-wallets, digital lending, and e-commerce have experienced significant user growth over the last five years at +1026%, +330%, and +222%, respectively.

Telcos such as Globe and PLDT have their own DFS apps called GCash and Maya, respectively. These telcos have diversified their services to include lending, investment, insurance, and marketplace offerings. Maya has secured a dedicated digital banking license, while GCash provides consumer-finance loans from both its platform and third-party sources.

DFS sector is facing fierce competition with various players vying for market share

Source: : Digido, Philippines Fintech Report 2023, Twimbit analysis

Bangko Sentral ng Pilipinas has granted 6 digital banking licenses

Recognizing the potential of digital banking, the Bangko Sentral ng Pilipinas (BSP) has granted licenses to six digital banks.

The 6 digital banks to get licenses from BSP

Source: : Twimbit analysis

Since receiving regulatory approval in August 2022, the digital-only banks have set noteworthy milestones:

- Overseas Filipino Bank, a government digital-only bank, introduced a streamlined digital account opening platform for overseas Filipinos and their beneficiaries, enabling them to submit all required documents securely and conveniently online.

- UnionDigital Bank and Tala joined forces to introduce an e-wallet tailored for unbanked Filipinos, providing easy access to loan applications, money transfers, and bill payments.

- UNO Digital Bank partnered with 1Sari Financing Corporation to offer financial solutions aimed at supporting the growth of sari-sari store owners and micro-enterprises.

- Tonik has amassed over 1 million customers since its full launch.

- GoTyme has expanded its presence with more than 300 digital kiosks across the Philippines and plans to reach 450 kiosks by the end of 2023.

- Maya initiated the “My Money. My Bank. My Way” campaign, seeking to popularize digital banking and empower Filipinos with innovative, personalized, and rewarding money management solutions.

A deep dive into the digital-only banks

Taking a closer look at the digital-only banks reveals how these innovative institutions are reshaping the financial landscape. We will explore their strategies, offerings, and impact on the industry.

#1 Uno Digital bank

UNO Digital Bank aims to simplify, enhance, and make banking services more accessible, and thus elevate the overall banking experience for its customers.

- Products

- Savings Account- #UNOready, UNO Debit Mastercard (physical card)

- Time Deposit- #UNOboost, #UNOearn

- Loans – #UNOnow [Quick Cash Loan]

- UNO x Gcash

- Coming soon: Insurance products, Investment products

- Partners

- Strategic Partners: Gcash, Trusting Social

- Payment Partners: Brankas, PESONet, Paynamics

- Bills Payments: Bayad, Converge, Globe, Innove communications, Maynilad, Meralco, PLDT, Skycable, Smart, Sun, Visayan electric, Manila water

- Solution Providers: Mambu, HPS, AWS, Oracle, Mastercard, iexceed, Zoloz, Infobip, Moengage

- Revenue

- Gross operating income in 2022: PHP 112.7 million (compared to PHP 34.0 million in 2021)

- Major income source: Foreign exchange gains from USD to PHP conversion

- Positive net interest margin: PHP 15.2 million from funds placed with BSP

- Net loss in 2022: Almost PHP 177 million

- Operating expenses: PHP 339.5 million due to employee base expansion and tech costs

- Total assets at year-end 2022: PHP 1.788 billion (increase of PHP 650 million)

- Funds utilization: Invested in intangible assets and software development to enhance mobile app.

- Customer support

- UNObank’s CAMS effectively monitors and controls consumer protection risks.

- CAMS ensures compliance with consumer protection standards and laws.

- Customers can provide feedback, inquiries, and complaints 24/7 through various channels: UNObank Phone Banking Support, UNObank Mobile In-App Message, UNObank Mobile In-App Chat, UNObank Viber, and Whatsapp Messaging.

Uno bank app

Source: : Twimbit analysis

#2 UnionDigital bank

UnionDigital bank is a wholly owned subsidiary of UnionBank of the Philippines (UBP). It is a lending focused bank that plans to offer mass market credit products to low-income wage earners, SMEs, OFWs, and unbanked Filipinos. The bank’s goal is to be a “super-embedded app” in the day-today lives of Filipinos.

- Products

- Savings Account- UD Main Bank Account

- Time Deposit- UD Time Deposit

- Loans

- Virtual credit and debit cards

- QR payments

- Partners

- Community development leaders

- Wholesale communities such as LGUs

- FinTechs, e-commerce, and other strategic partners

- Payment partnerships: Visa, Euronet

- Technology partnerships: Thought Machine, Callsign, Metaco, IBM

- Strategic partnership- mwell

- Revenue

- Gross operating income in 2022: PHP 209.7 million

- Major income source: Loans

- Net interest margin: 4.97%

- Operating expenses: PHP 804 million due to professional fees, employee base expansion and tech costs

- Total assets at year-end 2022: PHP 12.68 billion (increase of PHP 11 billion)

- Loans

- Loan portfolio: Grew to P5.3 billion, focusing on unsecured quick cash loans

- Targeted community segments: Served within UBP and AEV ecosystems

- Expansion plan: UnionDigital to integrate lending services with ecosystem partners

- Customer deposits: Increased to P9.4 billion

- Growth efforts: Focused on expanding depositor base and building low-cost CASA deposits with high-interest Time Deposit product

Union digital bank app

Source: : Twimbit analysis

#3 Maya bank

Maya Bank is the digital banking arm of Voyager Innovations, the leading technology company in the Philippines.

- Reach

- Maya Bank registered more than one million customers and reached PHP10 billion deposit balance in just five months after its public launch – affirming its position as the leading digital bank in the Philippines.

- The bank had 1.8 million monthly active users and a gross total loan portfolio of PHP 2.2 billion in 2022.

- Partners

- Partnerships in categories such as

- Communication

- Entertainment

- Food

- Gas Station

- Pharmacy and Medicine

- Supermarkets

- Retail

- Education

- Service

- Travel and Transportation

- Utilities

- Hospital

- Government

- Partnerships in categories such as

- Products

- Deposits & Savings

- Maya Savings

- Business Deposit

- Personal Goals

- Loans

- Maya Credit

- Pay in 4

- Flexi Loan

- Deposits & Savings

Maya bank app

Source: : Twimbit analysis

#4 Overseas Filipino bank

Overseas Filipino Bank, a LANDBANK subsidiary, utilizes digital and electronic channels to cater to the banking needs of Overseas Filipinos (OFs), Overseas Filipino Workers (OFWs), and their beneficiaries by providing various financial products and services.

- Products

- Digital Onboarding System with Artificial Intelligence

- Fund Transfer Module

- Bills Payment Facility

- Investment Services- Retail treasury bonds/premyo savings bonds, Retail dollar bonds

- Partners

- Bancnet Payment system

- Reach

- OFBank handled 458,090 inbound transactions worth P6.61 billion and 1,311,636 outbound transactions worth P5.09 billion.

- The growth is attributed to increased account openings and expanded global reach.

- In 2022, OFBank opened 110,968 accounts using DOBSAI, reaching customers in 126 countries.

- There was a 160.3% increase in the total number of accounts opened in 2022 due to rising demand for digital interactions.

- Revenue

- OFBank’s key revenue sources in 2022 included interest income from the Purchase of Receivable Program (PRP), investments in BSP facilities, Retail Treasury Bonds, and transaction fees.

- The bank reported a net loss of P13.86 million, a significant improvement from the P130.38 million loss in the previous year, primarily due to increased interest income from loans and investments, which outweighed expenses, loan loss provisions, and outsourced service costs.

- The CET 1 ratio decreased to 52.20% in 2022 from 136% the previous year, primarily due to an increase in operational risk-weighted assets.

Overseas Filipino bank app

Source: : Twimbit analysis

#5 GoTyme bank

GoTyme Bank is a joint venture of Tyme, a multi-country digital banking group, with members of the Gokongwei Group, namely Robinsons Bank, Robinsons Land Corporation, and Robinsons Retail Holdings, Inc.

- Products

- Since the launch of the Bank in October of 2022, GoTyme has launched 3 core propositions to the market:

- Send: Avail of 3 free bank transfers to other banks per week while sending money between GoTyme bank accounts is always free.

- Shop: Boost points up to 3x GoRewards when purchasing within GoRewards partner stores. Customers can also redeem their GoRewards points as cash instantly within the GoTyme application.

- Save: Better savings rate without any limits.

- Since the launch of the Bank in October of 2022, GoTyme has launched 3 core propositions to the market:

- Partners

- Technology partner: Mambu

- Security tech partner: Daon

- 17 brand partners for 3x Go Rewards

- Opportunities

- By the end of 2023, GoTyme is targeting to acquire over 1.5 million customers, deploy over 380 kiosks and activate over 5,000 deposit and withdrawal points nationwide.

- The bank will continue to improve and expand its product offerings to include disruptive investment, savings and credit propositions that would support the vision of unlocking the financial potential of all Filipinos.

- Revenue

- Gross operating income in 2022: PHP 15 million

GoTyme bank app

Source: : Twimbit analysis

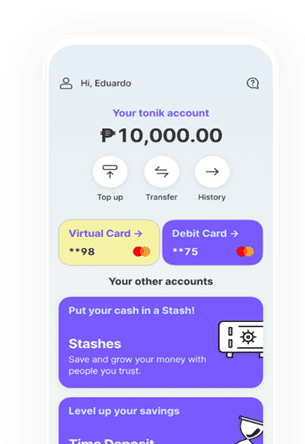

#6 Tonik bank

Tonik is officially the Philippines’ first neobank to secure a digital bank license from the Bangko Sentral ng Pilipinas (BSP).

- Products

- Tonik Account (Transactional Savings Account) with an instant virtual Mastercard

- Inbound and Outbound payments (powered by PESONet)

- Stash (Savings Account)

- Group Stash (Savings Account)

- Time Deposits

- Quick Loan (Cash Loan)

- Physical debit card (powered by Mastercard)

- Shop Installment Loan

- Partners

- Technology partnerships for core system, security and payments:

- Finastra

- Mastercard(payments)

- Daon

- V-key

- Bpc(payments)

- Credolab

- CRIF

- NICE Actimize

- Technology partnerships for core system, security and payments:

- Reach

- Tonik made its commercial launch to the Filipino market on March 18, 2021. Within only a month of operations, the Bank secured over Php1B in consumer deposits.

- After eight months, this number grew to more than Php5B. The main strategic focus of the Bank for 2022 was to rapidly funnel these deposits to a more profitable lending portfolio.

- It is addressing the USD 140 billion retail deposit and USD 100 billion unsecured retail lending opportunities in the Philippines.

- Revenue

- Gross operating income in 2022: PHP 331 million

Tonik bank app

Source: : Twimbit analysis

As the digital economy in the Philippines continues to thrive, traditional and digital-only banks are engaged in a dynamic competition that promises to reshape the financial services sector.

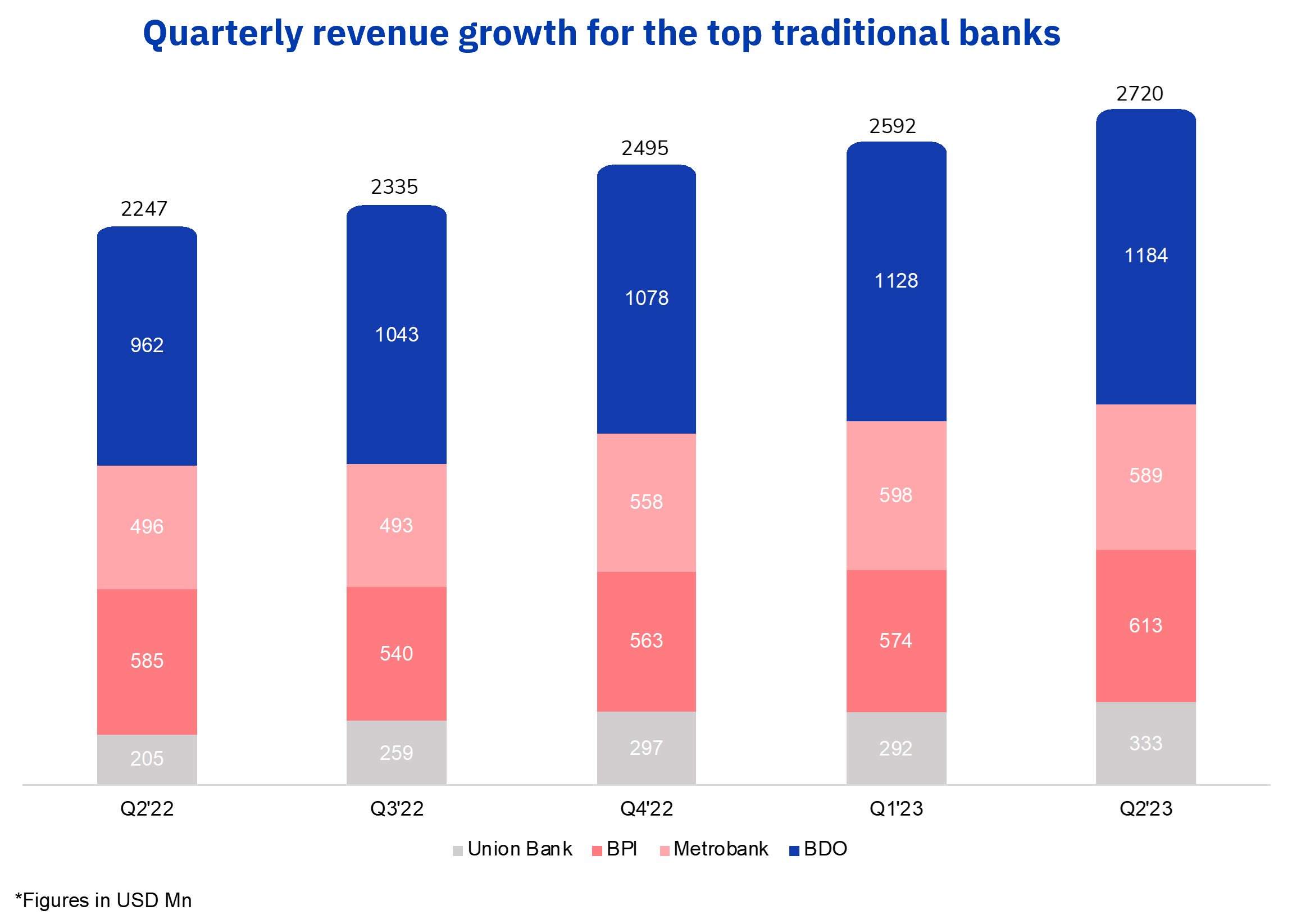

Market overview of top traditional banks

- Union Bank of the Philippines recorded the highest growth in its net revenues at 62.83%.

The traditional banks witnessed a growth of 21% in their net revenues. The net revenues stood at USD 2.72 billion in Q2 2023. All four banks analyzed reported growth in their net revenues between Q2 2022 and Q2 2023 and the average net revenues for these banks stood at USD 680 million in Q2 2023.

Union Bank of the Philippines recorded the highest growth in its net revenues at 62.83%. This strong growth was attributed to the following factors:

- Union Bank recorded the highest net revenue growth at 63% (USD 333 million).

- Non-interest income grew by 146% from USD 43 million in Q2 2022 to USD 107 million in Q2 2023, driven by increased fee income through customer transactions.

- Customer transactions recorded an increase of 211% between Q2 2022 and Q2 2023.

- Fee income grew from USD 31 million in Q2 2022 to USD 91 million in Q2 2023, accounting for 85% of the bank’s total non-interest income.

- Net interest income also grew by 40% from USD 161 million to USD 226 million.

- The bank’s loan book expanded by 42% from USD 6.6 billion to USD 9.4 billion.

Union Bank of the Philippines recorded not just the highest growth in the Philippines but also the highest growth in the APAC region.

Quarterly revenue growth for the top traditional banks

Source: : Twimbit analysis

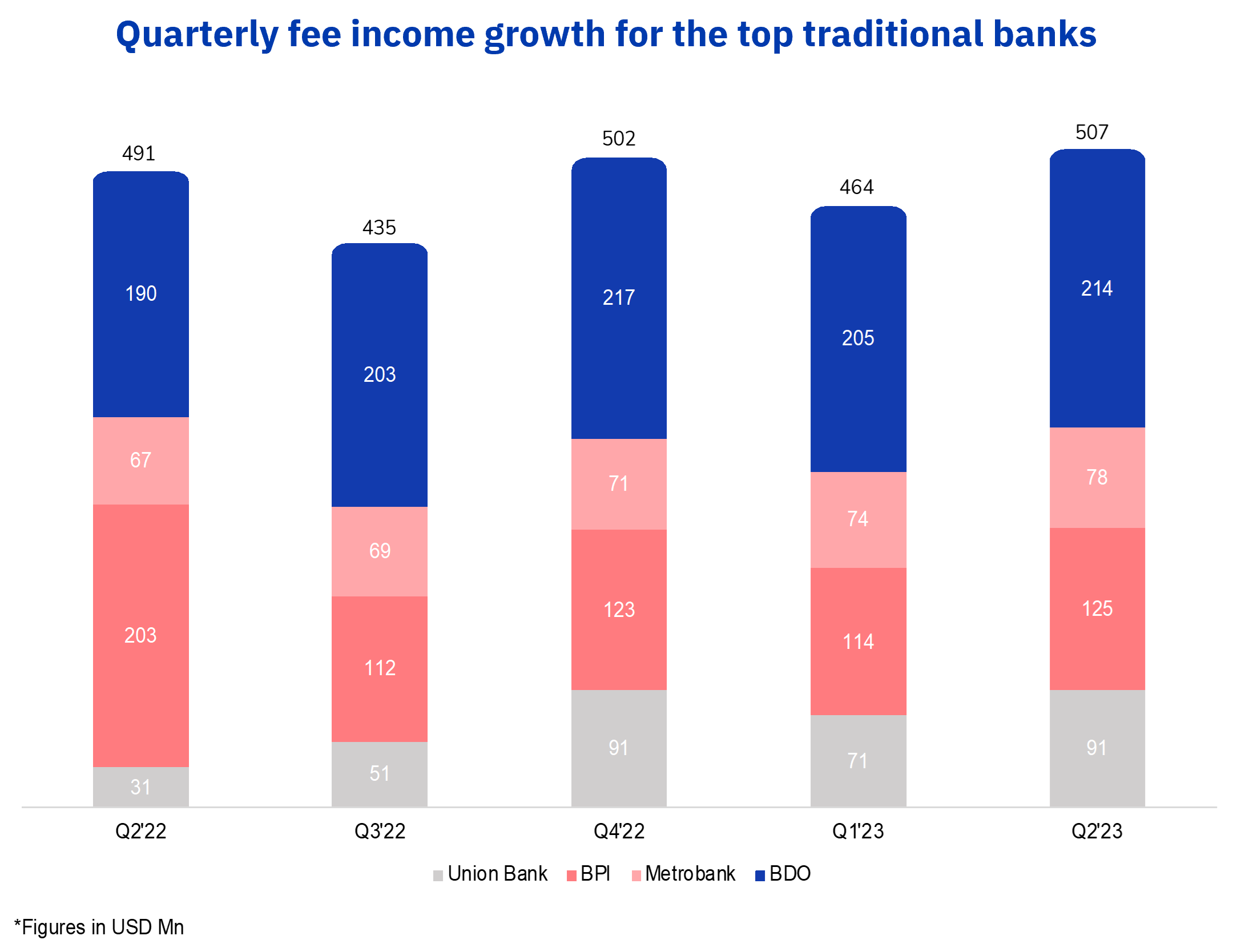

- Union Bank of the Philippines reported an exponential increase of 194.12% in its fee income

The traditional banks’ fee income grew by 3.28% YoY, from USD 491 million in Q2 2022 to USD 507 million (Figure 3) in Q2 2023.

Union Bank of the Philippines reported an exponential increase of 194.12% in its fee income from USD 31 million in Q2 2022 to USD 91 million in Q2 2023. The driver for the increase in fee income was customer transactions, which accounted for ~75% or USD 68 million of the income generated.

Post-COVID-19, the Philippines has experienced rising inflation which has led to higher prices, this is being offset by the use of credit cards that extend the purchasing power of the consumer. This has led to an exponential growth in credit card transactions in the economy. The rise in credit card usage is attracting transaction fees which is leading to higher growth of non-interest income among banks, especially for Union Bank.

On the contrary, BPI recorded the highest fee income decline at 38.5% (USD 125 million).

- 45% or USD 91 million of the fee income generated by the bank in Q2 2022 was the result of a one-off gain from the sale of an asset.

- Excluding the gain from this sale, the fee income for the bank was USD 112 million in Q2 2022.

- Excluding the one-off gain, the bank recorded an 11.29% increase in fee income.

Quarterly fee income growth for the top traditional banks

Source: : Twimbit analysis

How are traditional banks embracing the rise of digitalization?

Traditional banks are responding to the rise of digitalization by embracing technology and innovation. They are increasingly investing in digital platforms, enhancing customer experiences, and offering innovative digital banking services.

#1 Banco De Oro

- BDO prioritizes creating seamless phygital banking experiences

BDO prioritizes offering a seamless blend of physical and digital banking experiences to their customers. The bank’s IT investments have transformed their operations into a modern, agile platform, resulting in improved speed, reliability, and flexibility. These advancements are advantageous for customers and employees alike, facilitating automated branch transactions, cardless biometrics-based ATM withdrawals, and digital account openings.

- BDO made investments to move key applications to a plug-and-play, cloud-centric infrastructure, enhancing product capabilities for better customer experience and efficiency.

- Uses a CRM system for a unified customer view, simplified onboarding, reduced KYC processes, and utilized data analytics for effective cross-selling of products and services.

- BDO Pay, integrates CASA, debit, and credit card accounts for convenient digital payments and financial management. Expanding access to non-BDO clients extends BDO Pay’s market reach, particularly within the unbanked segment.

- BDO launched end-to-end customer journey program with a full QR code processing system rollout, enabling 80% of over-the-counter transactions by straight-through processing.

- BDO has implemented paperless self-service technologies, enhancing the banking experience, reducing transaction times, and boosting operational efficiency. The bank’s robust combination of physical and digital networks resulted 14% higher deposits of P3.2 trillion, driven by a 5% CASA increase, making up over 79% of total deposits, all while maintaining low funding costs.

#2 Bank of the Philippine Islands

- BPI establishes digital partner-led ecosystem for enhanced CX

BPI leverages its digital capabilities as a mechanism to reimagine banking by focusing on solving the customers’ biggest challenges. BPI increased its IT spending by 50% in 2022.

It has developed unique journey-specific apps to radically transform customer outcomes. From its AI powered banking app to its lifestyle app Vybe, BPI puts the customer first. BPI has established a digital partner-led ecosystem and introduced technology-enabled innovations

- BPI Online: This is the bank’s AI powered mobile banking app for its retail customers

- BPI eDonate: The bank’s dedicated portal for charities and sustainability initiatives, allowing customers to donate anytime to the foundations they support

- BPI BANKO: Digital banking solution dedicated for the underbanked and underserved population of the country

- Vybe: It is a lifestyle app which acts a digital wallet and rewards platform. It also forays into interoperable payments through QR Ph

- BizKo: It is a dedicated online banking platform for sole proprietors, freelancers and professionals, partnerships, and start-up businesses. It features a wide range of digital solutions such as- creating invoices for customers, collecting payments, transferring funds to suppliers and employees and generating financial reports

- BPI also has 2 more core apps: BPI trade for equity securities trading and BPI Bizlink- for SMEs and corporate customers

- The bank also has a partnership with Lazada to have a virtual bank on the e-commerce platform. It aims to grow its user base and offer a more convenient and seamless banking experience for its customers.

#3 Metrobank

- Metrobank boosts digital presence through infrastructure modernisation

Metrobank is placing a strong emphasis on enhancing its digital presence. Metrobank has plans to substantially invest in robust IT infrastructure to enhance its data management and analytics capabilities. The bank plans to be more mobile-centric and will enhance and upgrade their digital platforms by migrating some branch services digitally.

Furthermore, the bank is focused on increasing investments to bolster information security, optimize processes, and implement advanced risk management and control systems.

- Metrobank launched the new Metrobank mobile app in 2022, enabling users with customizable dashboards, bills payment, credit card installments, and lost credit card reporting.

- Uses Consumer Assistance Management System (CAMS) to standardize the handling of complaints in the bank. The process includes the filing and turnaround time for complaint investigation, resolution, and response to the customer.

- Leverages Metrobank Chatbot, a 24/7 channel that complements Metrobank’s website in providing automated replies to clients’ general and frequently asked questions (FAQs) about its products and services.

- In 2022, Metrobank introduced a new digital onboarding platform where customers can enjoy a seamless and straight-through experience when applying for credit cards and personal loans. The credit approval is done within five minutes.

- Metrobank made a substantial investment in an advanced fraud management system to enhance credit card account security.

#4 Landbank of the Philippines

- Landbank focuses on creating smooth digital experiences

Landbank deeply focuses on continuously enhancing its products and services to provide accessible, convenient, and safe banking solutions centered on balancing service delivery while ensuring the privacy and security of its customers. Landbank continues to take strides in expanding its digital banking reach through:

- Landbank launched LANDBANK Pay in April 2022 – an all-in-one mobile wallet providing customers versatile mobile payment options to pay bills, load cell phones and tollway RFID accounts, perform online purchases and fund transfers.

- The Landbank Mobile Banking App (MBA) provides customers with convenient access to various financial and non-financial services via their smartphones.

- Landbank provides National Government Agencies with real-time banking convenience via the LANDBANK Electronic Modified Disbursement System (eMDS). This secure internet-based platform simplifies MDS transactions, reduces costs, and eliminates the need for physical document transmission. The bank registered 2.5 million amounting to P2.1 trillion for eMDS in 2022.

- Landbank’s Digital Onboarding System (DOBS) allows customers to easily open accounts and update their information, providing enhanced convenience.

- LANDBANK’s Link.BizPortal, an electronic payment system, enables users to conveniently make payments to various government and private entities. It exhibited robust growth, with a 49% surge in transactions, reaching 5.8 million in volume and totaling P11.6 billion in value in 2022.

#5 Unionbank of the Philippines

- Unionbank has huge investments towards next-generation technologies

Unionbank’s commitment to digital transformation has seen significant investments in cloud computing, automation, blockchain, artificial intelligence (AI), and application programming interfaces (APIs), setting the stage for a future-proof banking infrastructure. Unionbank uses next-gen tech to enable seamless CX through these initiatives:

- Its digital-only bank subsidiary is one of six digital banks approved to operate by the BSP. It acquired 1.73 million customers and recorded Php4.8 billion in loans and Php9 billion in deposits just five months after its commercial launch.

- The bank launched Bonds.PH, the first mobile app in Asia to utilize blockchain for distributing retail treasury bonds, enabling global risk-free bond transactions, with an initial oversubscribed sale of Php11 billion.

- The bank is an early proponent of open banking and open finance in the Philippines. It has more than 100 partners and has facilitated more than 78.7 million transactions amounting to Php597 billion. The marketplace has more than 200 API products and 500 API endpoints

- It uses artificial intelligence (AI) and data science in various areas, including sales, customer service, risk management, and fraud detection.

- The bank has been using a data vault platform that serves as a central data hub with AI and ML capabilities. By using cross-sell models, it increased total bancassurance bookings by 138% compared to a non-model approach.

- It uses AI to detect irregular customer transaction patterns linked to money mule activities. This system automatically identifies up to 40% of potential money mules among newly opened accounts at a 5% detection rate.

Download our report above to explore this exciting transformation and the evolving role of banks in the digital age.