Key Takeaways

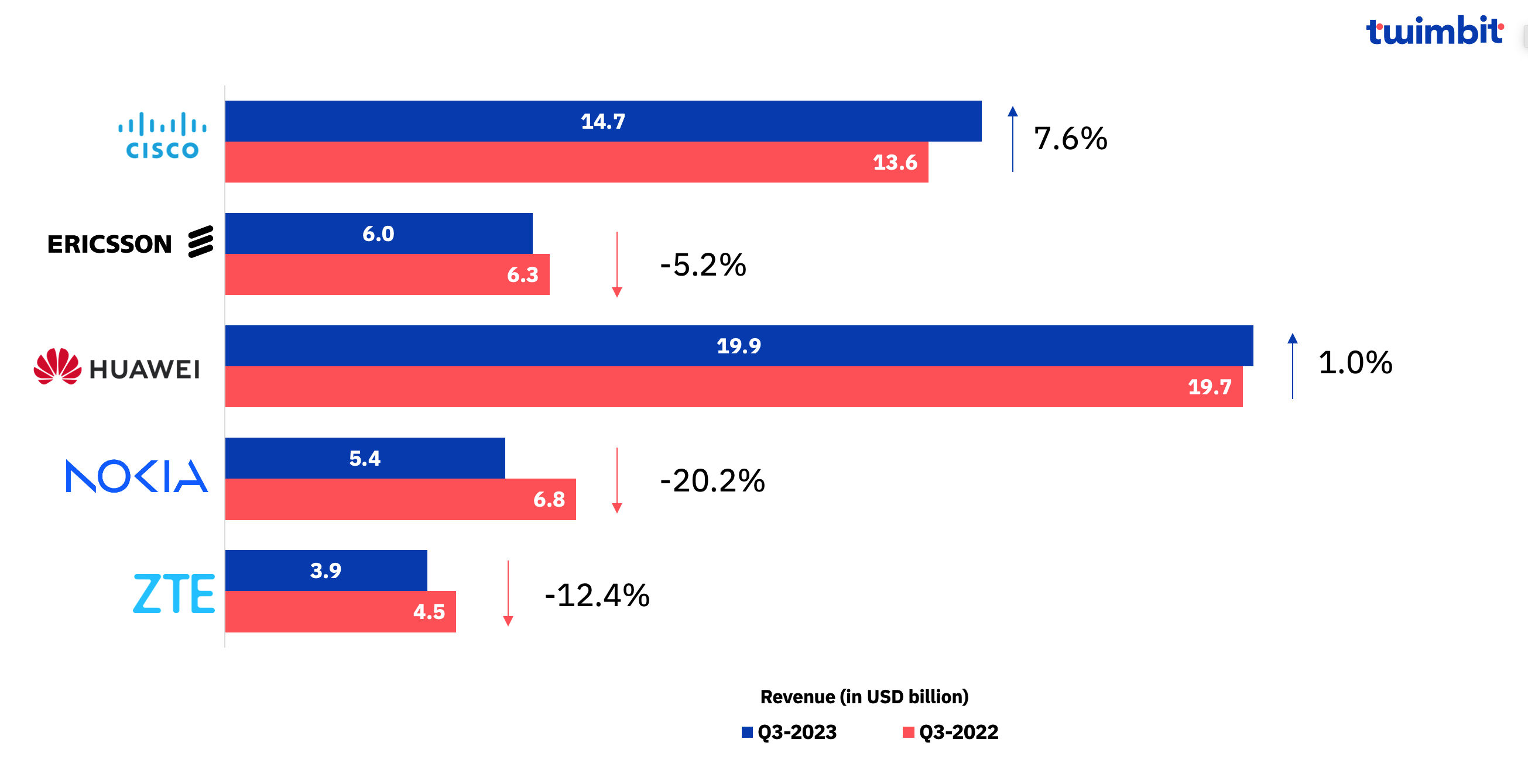

- The leading five telecom vendors witnessed a revenue decline of 2% (YoY basis) on a constant currency basis in Q3-2023, as the 5G deployment pace across leading geographies continues to stabilize and slow down.

- In Q3-2023, Cisco demonstrated notable single-digit growth at 7.6%, standing out as the sole performer in the equipment vendor market. Meanwhile, Huawei experienced minimal revenue growth, and Ericsson, ZTE, and Nokia all observed a decline in revenue.

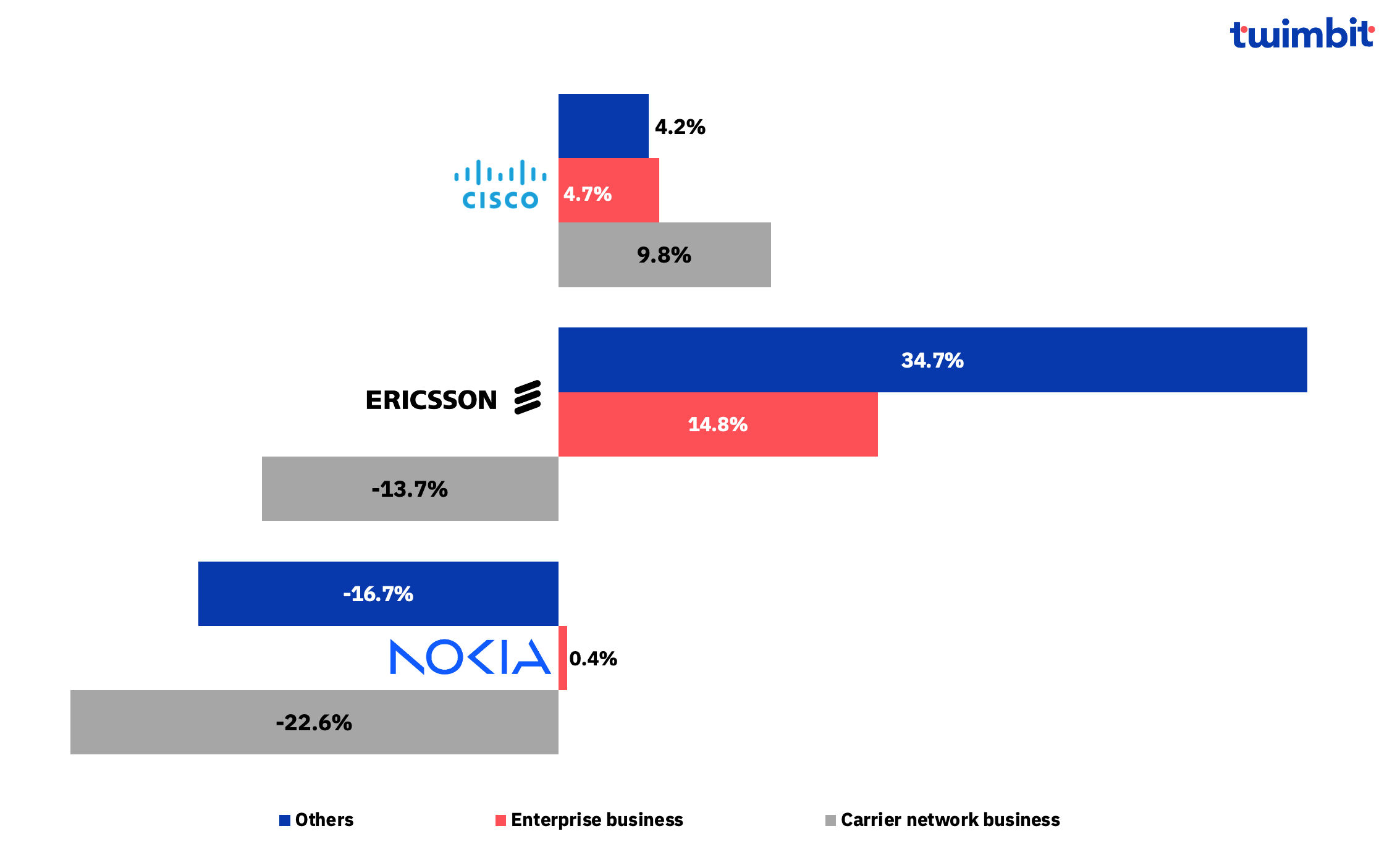

- Cisco and Ericsson continued to deliver strong performance in their enterprise business segment, driven by sustained demand for 5G deployment. Additionally, Private 5G deployments also provide revenue-earning opportunities for telecom services providers as well as vendors, by offering innovative digital capabilities like software-defined networking, cloud, and security services to the enterprises.

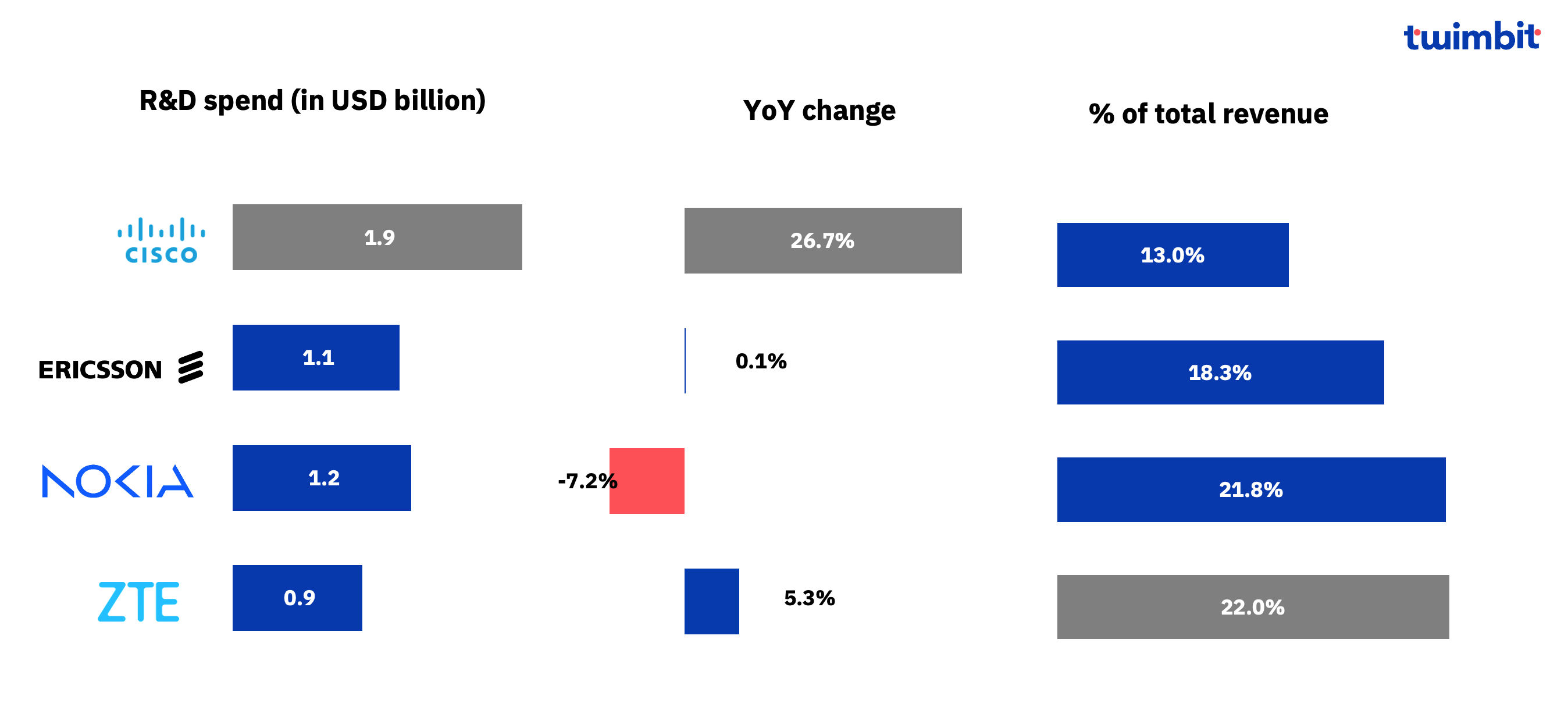

- Cisco accounted for the highest R&D spend of USD 1.8 billion in Q3-2023, whereas ZTE reported the highest growth of 22.0% on a YoY basis for R&D spend.

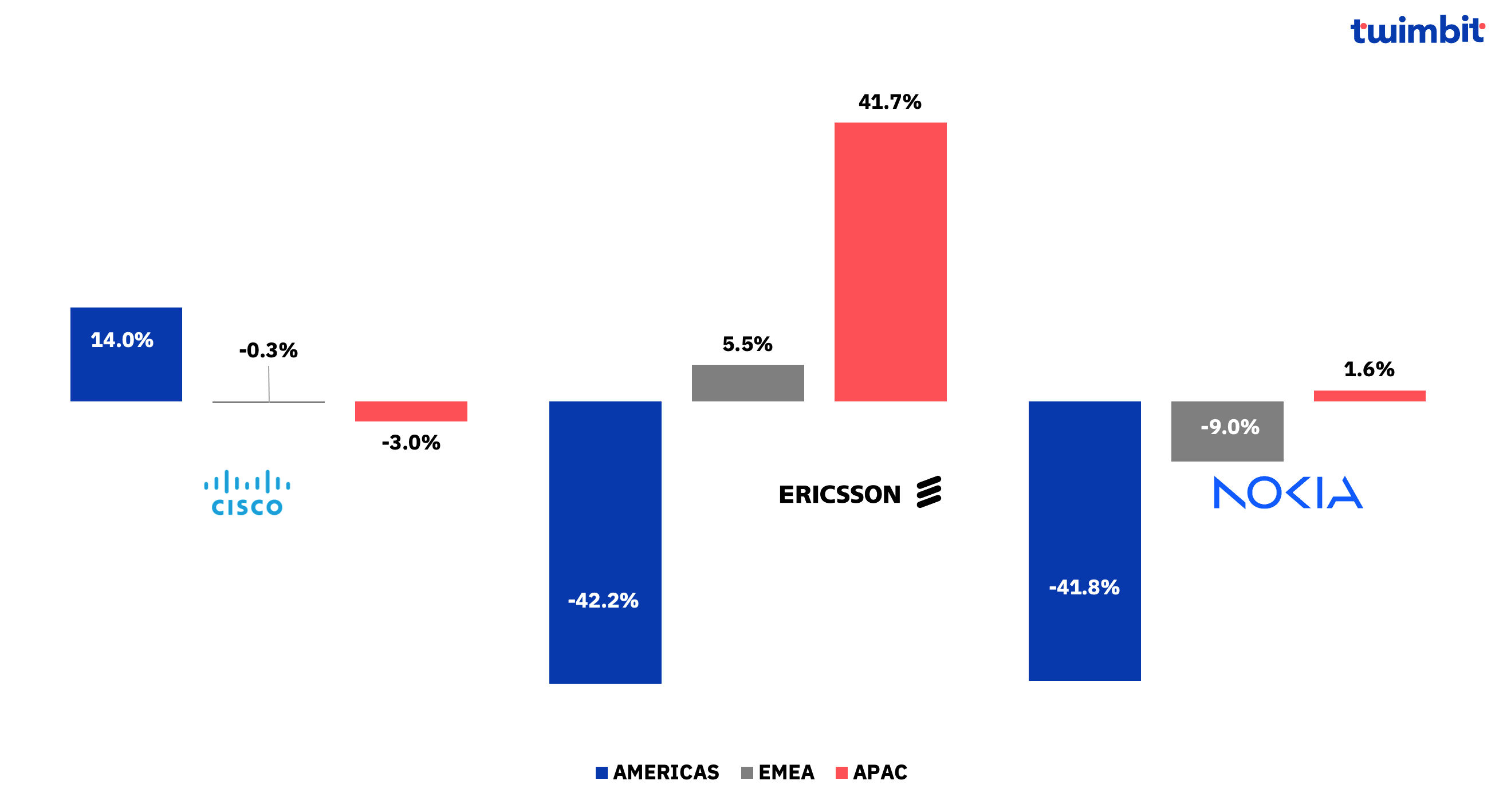

- With the 5G networks largely deployed throughout North America and other mature markets, operators have dramatically slowed their network investments. This has resulted in vendors like Ericsson and Nokia witnessing more than a 40% decline in revenue from the Americas region, with Cisco being the only equipment vendor to witness revenue growth from the region.

- South Asian region led by India emerged as a key growth driver for the revenue of Ericsson and Nokia, as the region continues to witness increased 5G network deployment intensity by the telcos.

- Nokia announced a cost reduction plan given the decline in Q3-2023 sales and a waning interest in 5G equipment. It plans to reduce up to 14,000 jobs by 2026, with aims to reduce Nokia’s cost base by ~USD 872 million (EUR 800 million) to ~ USD 1.3 billion (EUR 1.2 billion) over three years.

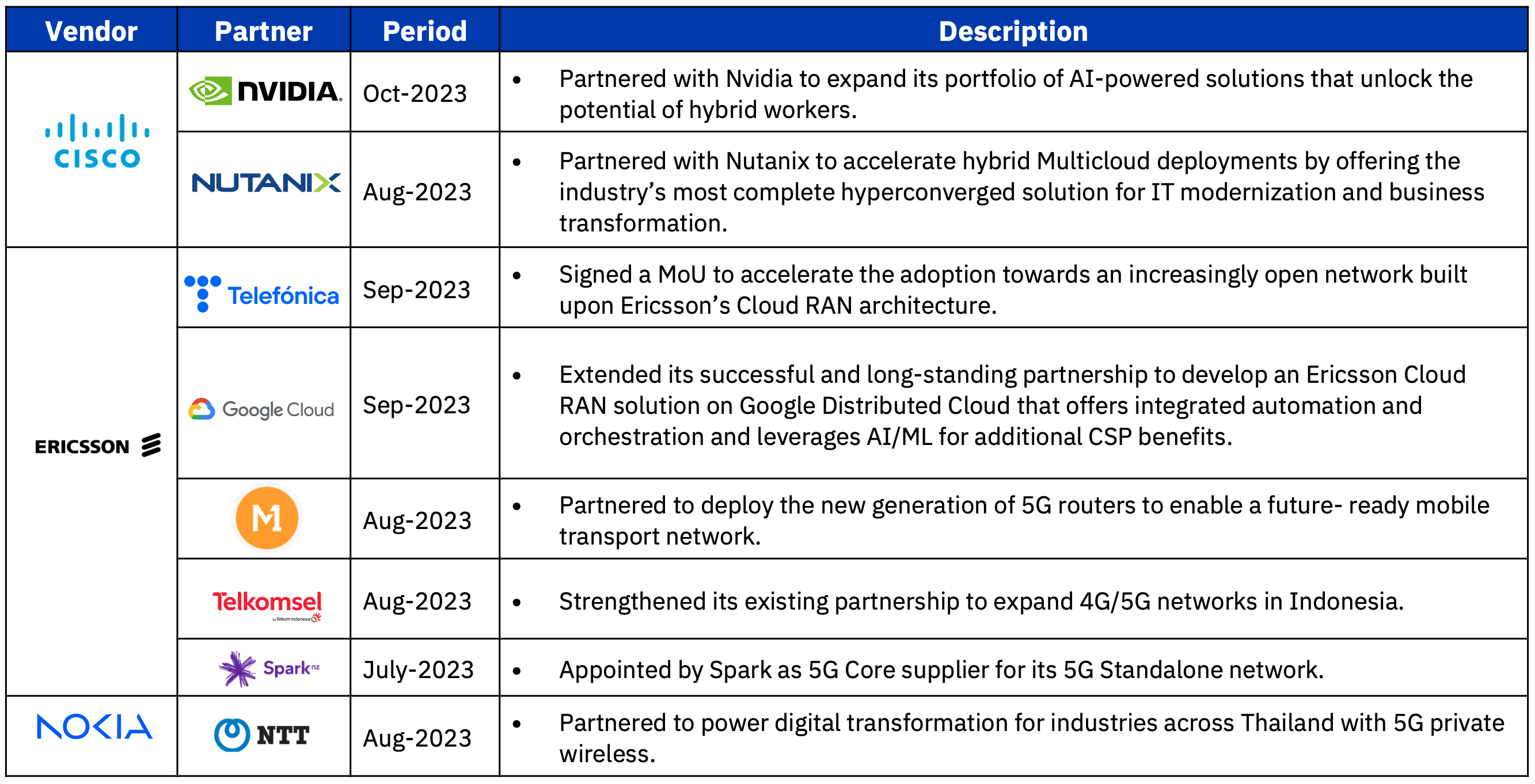

- Prominent partnerships during Q3-2023 featured Ericsson collaborating with Telefonica, Google Cloud, M2, Telkomsel and Spark for AI/ML and 5G initiatives. Nokia partnered with NTT for private wireless 5G, whereas Cisco partnered with NVIDIA and Nutanix.

Financial Performance

Mixed results for telecom vendors as global 5G deployment begins to stabilize globally

The financial results of the top five telecom vendors in Q3-2023 underscore a blend of progress and challenges. Factors such as the rollout of 5G, regional dynamics, and strategic collaborations have played pivotal roles in shaping their performance trajectories. Collectively, the foremost five telecom equipment vendors recorded a 2.0% decline on a constant currency basis. Below is a summary of the revenue performance of these vendors during the given period:

- Cisco exhibited a significant single-digit growth of 7.6%.

- Huawei (including its consumer business) attained single-digit growth of 1%.

- Conversely, Ericsson, Nokia and ZTE (including consumer business) witnessed a drop in their revenues, experiencing a fall of 5.2%, 20.2%, and 12.4% respectively during Q3-2023.

Exhibit 1: Leading telecom vendor revenue trends YoY basis, Q3-2023

Note:

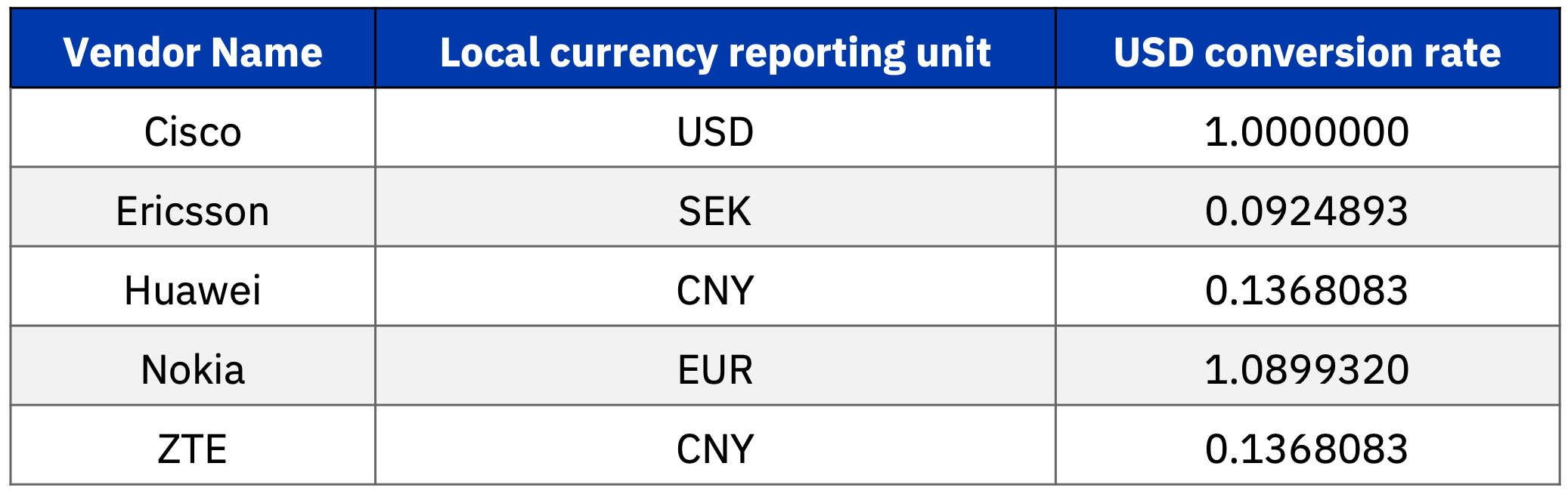

1. USD conversion is on a constant currency basis

2. Cisco’s financial performance is from Aug 2023 to Oct 2023

3. Huawei and ZTE revenue includes its consumer business revenue

With 5G networks largely deployed throughout North America and other mature markets, operators have dramatically slowed their network investments resulting in vendors feeling the pain from that sudden decline. Cisco and Ericsson experienced growth in their enterprise business. Ericsson’s enterprise business growth was fueled by the rising demand for private 5G deployment driven by the wireless solutions of Vonage. The carrier network business for Ericsson and Nokia faced challenges in Q3-2023.

Exhibit 2: Revenue growth by customer type, Q3-2023

Note:

1. Cisco’s financial performance is from Aug 2023 to Oct 2023

2. Huawei and ZTE doesn’t disclose revenue by customer type every quarter

Cisco

Cisco reported its strongest first quarter results for the financial year (August – July) 2024 in its history in terms of revenue and profitability. Revenue increased by 7.6% YoY during the quarter to reach USD 14.7 billion. The revenue growth was primarily driven by a 13% YoY increase in total software revenue and a similar rise in software subscription revenue. Additionally, it also reported a growth in its annualised recurring revenue (ARR), which was USD 24.5 billion, marking a 5% increase from the previous year.

Cisco experienced a deceleration in new product orders during the quarter, attributing it to customers prioritizing the installation and implementation of products received in the preceding three quarters. Notwithstanding this temporary setback, the company maintains a positive outlook, anticipating a resurgence in product order growth rates in the latter half of the year. It continues to witness revenue growth on account of prior strategic actions executed to mitigate the supply chain constraints. Additionally, it also made progress in transitioning its business model to deliver increased software and subscriptions. Both Software and Subscription revenue increased by 13% each in Q3-2023 (YoY basis), with subscription services accounting for ~85% of its software revenue, which reached USD 4.4 billion during the quarter.

Cisco has provided guidance for its Q2-2024 (Nov-2023 to Jan-2024), projecting revenue to decline by 5.8% to 7.3%. However, the company anticipates its full-year revenue to grow in the range of 1.2%-3.5%.

During this period, Cisco completed acquisitions of several companies, including Accedian, Working Group Two, Oort, SamKnows, and Code BGP. Additionally, the company announced its intention to acquire data analytics software provider Splunk for USD 28 billion. Cisco believes that this acquisition will position it to secure over USD 1.0 billion worth of orders related to AI infrastructure from cloud providers in fiscal year 2025.

Ericsson

Ericsson revenue declined by 5.2% YoY, totalling USD 6.0 billion (SEK 64.5 billion) in Q3-2023. The company’s carrier networks business declined by 13.7% YoY, despite the growth in Southeast Asia, Oceania, and India, which almost doubled in the quarter. However, the growth in those markets couldn’t offset the sharp decline in North America, where network sales declined 60% in the quarter to USD 1.2 billion (SEK 13.5 billion), down from USD 2.4 billion (SEK 26.5 billion) in the same quarter in 2022. This was due to a reduction in the inventory levels as well as the roll-out pace, owing to saturation in 5G network deployment, which followed the high investment levels already done by the telcos in 2021 and 2022.

Ericsson’s cloud software and services unit was one bright spot for the company with its quarterly sales up 10% to USD 1.4 billion (SEK 15.6 billion).

Ericsson also reported a decline in Vonage’s core operations due to higher interest rates and a drop in its market capitalization has resulted in non-cash impairment charges of USD 3 billion (SEK 32 billion). While the Enterprise vertical has been affected by the Vonage slowdown, healthy demand for Enterprise Wireless Solutions supported the top line in this segment.

For Q4-2023, the company expects similar market trends, with an anticipated increase in cost-out impact. It expects the group Q4-2023 EBITA margin to be ~10%, which was 0.8% and 5.9% in Q2-2023 and Q3-2023 respectively.

Huawei

Huawei achieved a revenue of USD 19.9 billion (CNY 145.7 billion) during Q3-2023, representing a single-digit 1% YoY increase. In the first 9 months of 2023, Huawei generated USD 62.5 billion (CNY 456 billion), an increase of 2.4% YoY and net profit margin reached 16%. Notably, the overall performance aligned closely with projected expectations.

Huawei’s Rotating Chairman, Ken Hu claimed that their performance is in line with forecasts. Moving forward, Huawei aims to increase its R&D investment to make the most of its business portfolio and further scale up the competitiveness of its products.

Nokia

Nokia’s revenue declined by 20.2% in Q3-2023 due to macroeconomic uncertainty and higher interest rates, which continue to pressure operator spending. Nokia is currently experiencing some headwinds, which are largely related to a return to more normal lead times, macroeconomic uncertainty, and customer inventory digestion. Carrier network business declined by 22.6%, reflecting weakness in North American CSPs as customers continue to evaluate their spending. Moreover, as 5G penetration reached maturity in certain regions like Northeast Asia, the overall carrier network business revenue declined.

Enterprise net sales increased 0.4% YoY. In constant currency, it reported an increase of 5.0% in Q3-2023, as growth in enterprise verticals more than offset a decline in net sales to webscale customers. Customer engagement remains positive as Nokia added 85 new enterprise customers in the quarter. Private wireless continued to show strong double-digit growth in Q3-2023 and now has more than 675 customers.

Despite its net sales being impacted by the ongoing uncertainty, the company expects to see a more normal seasonal improvement in its network businesses in the fourth quarter. The company anticipates net sales to decline in the range of 1.3% – 6.8% for FY2023.

In response to a decline in Q3-2023 sales and a waning interest in 5G equipment, Nokia has announced a cost-reduction plan that includes the elimination of up to 14,000 jobs by 2026. This initiative aims to reduce Nokia’s cost base by ~USD 872 million (EUR 800 million) to ~ USD 1.3 billion (EUR 1.2 billion) over three years. The primary areas targeted for cost savings are Mobile Networks, Cloud and Network Services, and Nokia’s corporate functions.

ZTE

ZTE was hit by weakness in global demand in Q3-2023, recording a double-digit decline (-12.4 on a YoY basis) in operating revenue. The decline can be attributed to the uncertainty of the global macroeconomic environment since this year has posed challenges to the development of the ICT industry. ZTE stated in its semi-annual report that the external environment is complex and severe, global economic growth is under pressure, and the normalization of uncertainty has brought many challenges to business operations.

In the Q3-2023 report, ZTE did not list the specific performance of each business. However, looking back at its H1 performance, the operator network business, which brought the most important contribution to overall revenue, was relatively stable, but government and enterprise revenue declined due to domestic integration projects and a decline in international market revenue. Additionally, its consumer business also witnessed a YoY decline in revenue from international mobile phone products.

R&D performance

Cisco leads the R&D spend amongst telecom vendors in Q3-2023

Exhibit 3: R&D performance of vendors, Q3-2023

Note:

1. Cisco’s financial performance is from Aug 2023 to Oct 2023

2. Huawei does not report R&D expenses every quarter

Cisco

Cisco witnessed a significant 26.7% YoY increase in its R&D spending, reaching an impressive USD 1.9 billion during Q3-2023. In this quarter, with the acquisition of Splunk, it aims to boost its internal R&D in line with its strategy to strengthen its position in cloud, security, observability and AI with targeted strategic M&As.

Ericsson

R&D expenses amounted to USD 1.1 billion including restructuring charges of USD 18 million. R&D expenses increased in the Enterprise segment through the acquisition of Vonage (which was consolidated from the date of the acquisition on July 21, 2022) as well as through increased investments to expand the Enterprise Wireless Solutions portfolio. R&D expenses declined in Networks and Cloud Software and Services.

Nokia

Nokia reported a 7.2% YoY decline in its R&D expenses in Q3-2023. Despite this decrease, the impact on the allocation of R&D spending as a proportion of revenue increased by 300 basis points, resulting in R&D accounting for 21.7% of the total revenue.

ZTE

Despite some headwinds, ZTE’s R&D push reaps industry recognition. R&D investment increased by 5.3% YoY and amounted to USD 859 million (~ RMB 6.3 billion) in Q3-2023, accounting for 21.9% of its revenue compared with 18.2% in the same period in 2022. R&D investment is mainly in the three fields of networks, computing power, and computing network integration.

Specifically, in terms of intelligent computing, ZTE has created an end-to-end full-stack intelligent computing solution that includes 10,000 card large-scale clusters, all-in-one training machines, etc. In terms of big models, ZTE has developed its generic big model and pre-trains large models in various fields through incremental domain knowledge, such as R&D code, communication, and government affairs.

Geographic performance

Ericsson witnessed revenue increase in EMEA and APAC, whereas Cisco grew in the Americas and Nokia in the APAC region

Exhibit 4: Regional revenue trends, Q3-2023

Note:

1. Cisco’s financial performance is from August 2023 to October 2023

2. Huawei and ZTE don’t report geographic-wise revenue every quarter

Cisco

Cisco’s performance exhibited remarkable growth in the Americas region, experiencing a substantial 14.0% increase, while in other regions they witnessed a decline. The growth observed in the Americas was primarily attributed to a surge in service revenue, underscoring the significance of Cisco’s service-oriented approach.

Ericsson

Ericsson faced challenges in the Americas but saw significant growth in EMEA and the APAC region with 5.5% and 41.7% respectively. There was a notable 74% increase in revenue in the Southeast Asia, Oceania, and India regions due to 5G market share gains in India. In Northeast Asia, the revenue declined as investments declined in several markets after elevated 5G investment levels in 2022.

America’s sales dropped due to a decline in North America because of customers’ reduced inventory levels and lower roll-out pace following high investment levels in both 2021 and 2022. While Europe and Latin America were impacted by high investment levels in 2022. Also, sales in Europe were impacted by a decline in managed services due to the descoping of contracts. However, the Middle East and Africa reported an increase primarily driven by the next wave of 5G investments in countries in the Middle East.

Nokia

Nokia experienced a decline in every region they operate except single-digit growth in APAC. APAC growth was driven by India, reporting a growth of 101.8% in Q3-2023 to reach ~USD 618 million. This can be attributed to mobile Networks, as 5G deployments continued to drive YoY growth. At the same time, sales volumes moderated significantly on a sequential basis as the pace of deployment started to slow.

Network Infrastructure also saw strong growth, mainly driven by Optical Networks, while the Middle East and Africa region witnessed a growth of 8% YoY, primarily driven by Mobile Networks and Network Infrastructure.

Europe’s net sales were somewhat impacted by the decline in Nokia Technologies (which is entirely reported in Europe). Net sales in Europe, excluding Nokia Technologies, decreased at a double-digit rate. The growth in Cloud and Network Services was more than offset by a decline in Mobile Networks and Network Infrastructure, particularly in Fixed Networks and IP Networks. Within Greater China, net sales decreased in both Mobile Networks and Network Infrastructure.

Net sales performance in Latin America reflected a decline across each of the businesses within the Network Infrastructure. The strong decline in North America reflected weakness in both Mobile Networks and Network Infrastructure as customers continued to evaluate their spending and digest inventories. To a lesser extent, Cloud and Network Services also declined.

Key partnerships

Cloud, AI/ML and 5G are the key themes driving telecom partnerships

Exhibit 5: Key partnerships, Q3-2023

Research Methodology and Assumptions

- Data collection was conducted through secondary research by utilizing research databases, telecom equipment vendors’ websites, and financial reports and filings.

- The performance of the telecom equipment vendors in Q3-2023 is indicative of their overall performance and can be used to predict future trends in the market.

- This report offers a comprehensive evaluation of the Q3-2023 performance of prominent global telecom vendors including Cisco, Ericsson, Huawei, Nokia, and ZTE. The report’s primary focus is to provide valuable insights into the benchmarking of their carrier and enterprise business operations. The Chinese equipment vendors have not reported their quarterly earnings based on segments and geographical areas.

- The report covers the third quarter of 2023 for each of the telecom equipment vendors. Notably, Cisco’s fiscal year concludes in July. To align their reporting cycle with the calendar year, Q1- FY2024 is considered equivalent to Q3-CY2023.

- For fair representation, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value for the period July-August 2023. The below table reflects the currency conversion rate used in this report:

Thank you for reading! Reach out to us for any feedback

You might also like:

Cloud stories – Q3 2023

Global telecom vendors update – Q2 2023