Propelled by increased government spending, Q3 2023 marked a robust recovery for the Philippines, with its GDP (Gross Domestic Product) reaching 5.9%. This positive trajectory was facilitated by a turnaround in government expenditure, compensating for a decline in household consumption. However, this momentum may prove challenging to sustain due to elevated interest rates and the prevailing global economic slowdown.

Similarly, the Philippines is contending with a significant rise in inflation, leading to decreased demand. In response, the Central Bank of the Philippines has adopted a proactive approach by substantially increasing interest rates, albeit at the cost of economic growth.

The loan portfolios of the leading 4 banks expanded by 8.49%, rising from an average of USD 27.08 billion in Q3 2022 to USD 29.37 billion in Q3 2023. Alternatively, deposits also grew by 11.86%, going from an average of USD 34.77 billion to USD 38.89 billion in Q3 2023.

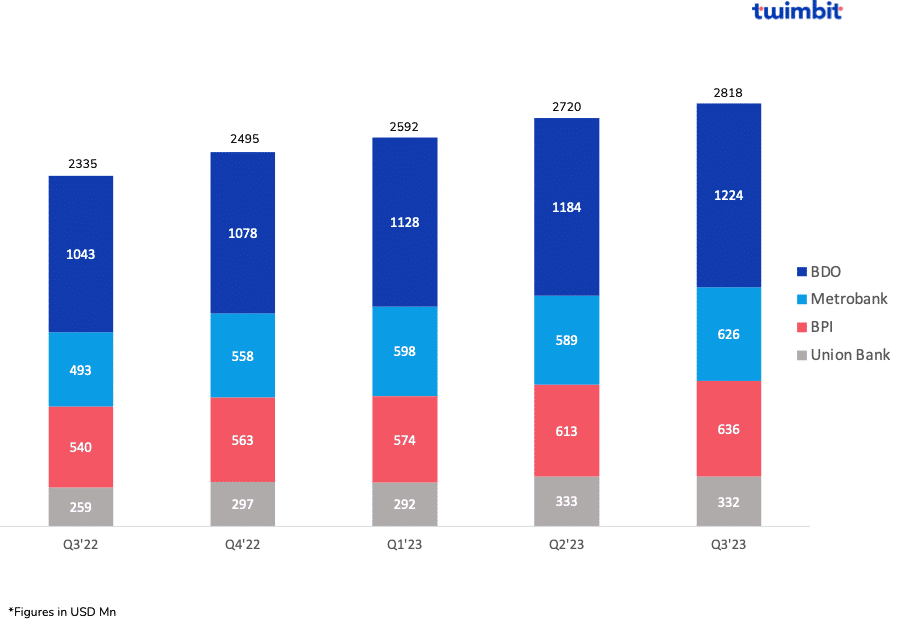

Revenue

Net revenues for the top 4 banks in the Philippines grew by 21% in Q3 2023 compared to Q3 2022

The top 4 banks in the Philippines increased from USD 2.33 billion in Q3 2022 to USD 2.82 billion in Q3 2023 (Exhibit 1). Average net revenues stood at USD 704 million in Q3 2023.

Exhibit 1: Net revenues of the Top 4 banks in the Philippines

Union Bank of the Philippines reported the highest YoY growth rate at 28.10%, increasing net revenues to USD 332 million in Q3 2023. This strong growth was attributed to the following factors:

- 24% net interest income increased from USD 194.72 million to USD 241.60 million.

- 43% non-interest income increase from USD 63.10 million to USD 90.15 million.

- The bank’s loan book expanded by 18.79% from USD 8.06 billion to USD 9.57 billion.

Despite being the smallest among the four banks, Union Bank of the Philippines recorded the highest growth. It should be noted that all other banks also reported double-digit increases in their net revenues between Q3 2022 and Q3 2023.

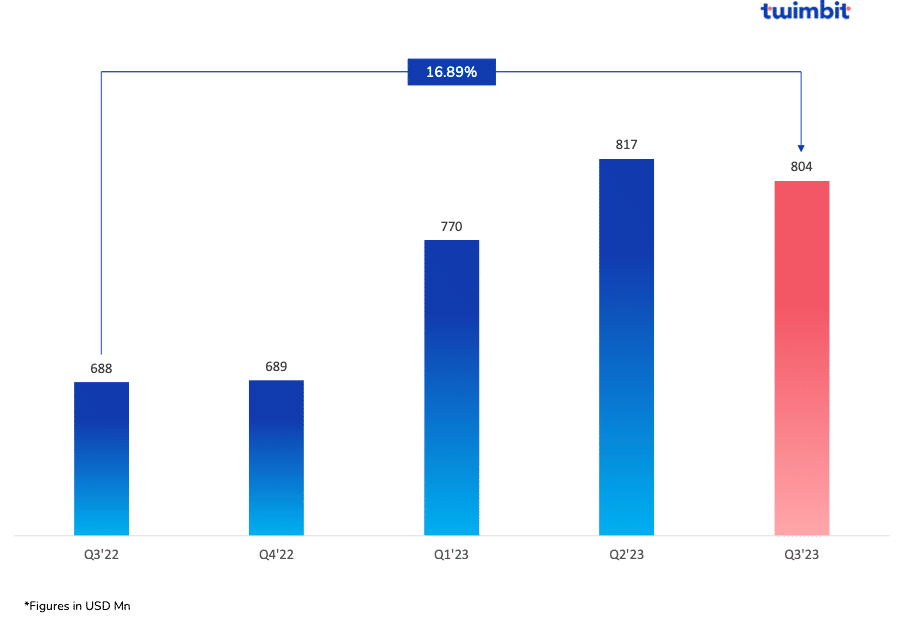

Profitability

Net profit for the top 4 banks in the Philippines grew by 16.89% in Q3 2023 compared to Q3 2022

The top 4 banks in the Philippines aggregated net profits from USD 688 million in Q3 2022 to USD 804 million in Q3 2023. Average net profits grew by 16.89% (Exhibit 2) from USD 172 million in Q3 2022 to USD 201 million in Q3 2023.

Exhibit 2: Consolidated net profits of the Top 4 banks in the Philippines

- Metrobank: 39.13% net profit growth

- Banco de Oro (BDO): 14.67% net profit growth

- Bank of the Philippine Islands: 32.78% net profit growth

- Union Bank of the Philippines: 57.69% net profit decline

Strong Metrobank net profit growth is driven by:

- 20% increase in the net interest income from USD 407 million to USD 481 million

- 62% YoY growth in interest from investments due to higher accrual income from investment securities

- 49% YoY growth in interest on loans due to expanding portfolio and better margins

- 63% increase in the non-interest income from USD 88 million to USD 144 million

- 63% YoY growth in income from trading and FX gains from USD (18.03) million in Q3 2022 to USD 9 million in Q3 2023

- 7% YoY growth in income from service fees & trust from USD 75.73 million in Q3 2022 to USD 81.13 million in Q3 2023

- 400% YoY growth in income from sale of assets from from USD 5.42 million in Q3 2022 to USD 27.04 million in Q3 2023

The decline in net profits for Union Bank of the Philippines by 57.69% between Q3 2022 and Q3 2023 is due to:

- On-time integration cost of Citibank’s portfolio

Another factor is how Union Bank became the legal owner of Citibank’s consumer business on 1 August 2022 but will likely continue recording costs associated with the integration for the next quarter.

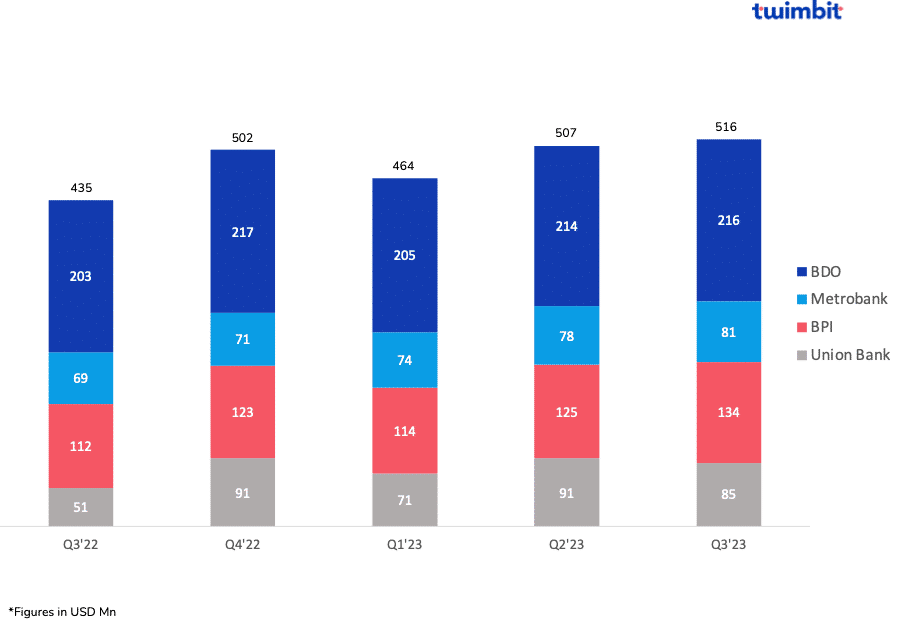

Fee-based income

Fee income for the top 4 banks in the Philippines grew by 18.71% in Q3 2023 compared to Q3 2022

Philippines banks generate most of their fee income from traditional sources. There are also a lot of cross-border remittances that contribute to the overall fee income, such as the rise in Filipinos working in other Asian countries.

The top 4 banks in the Philippines grew their fee income from USD 435 million in Q3 2022 to USD 516 million (Exhibit 3) in Q3 2023.

Exhibit 3: Fee incomes of the Top 4 banks in the Philippines

Union Bank of the Philippines reported the highest fee income increase at 67.12% (USD 85 million) between Q3 2022 and Q3 2023.

- The recent popularity of credit cards has led to higher non-interest income growth among banks in the Philippines.

However, the fee income has declined compared to Q2 2023, when it was USD 91 million.

BPI, which reported a decline in its fee income in the previous quarter, reported double-digit growth in Q3 2023 at 19.15% (USD 134 million).

- Card fees generated 28.8% of the bank’s fee income and reported a 34.6% YoY increase.

- Wealth management made up 16.7% of the bank’s fee income and reported a 2% YoY growth.

- Insurance made up 9.5% of the bank’s fee income and reported the highest YoY growth at 46.2%.

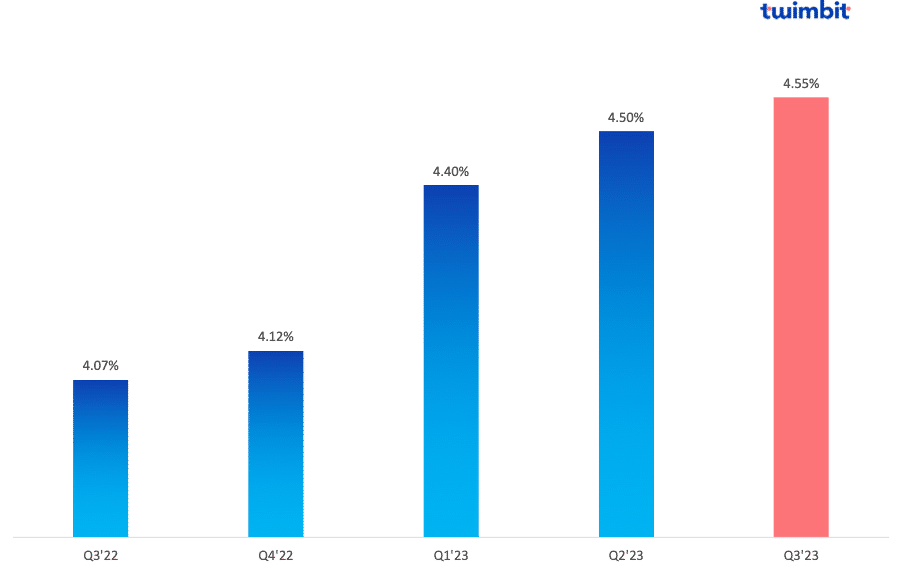

Net interest margins (NIM)

NIM for the top 4 banks in the Philippines increased by 48 basis points in Q3 2023 compared to Q3 2022

The average NIM increased by 48 basis points from 4.07% in Q3 2022 to 4.55% in Q3 2023 (Exhibit 4).

Like the previous quarter, Banco de Oro (BDO) reported the highest NIM increase at 60 basis points, from 4.10% to 4.70%. Meanwhile, the Union Bank of the Philippines registered the highest NIM at 5.30%, up 43 basis points.

A key factor for these banks’ high NIMs is their high lending and low deposit rates. For instance, the Union Bank of the Philippines reported:

- 18.79% loan portfolio increase to USD 9.6 billion.

- 18.18% deposit increase to USD 12.66 billion.

- 75.64% loan-to-deposit ratio (LDR)

Exhibit 4: Consolidated net interest margins of the Top 4 banks in the Philippines

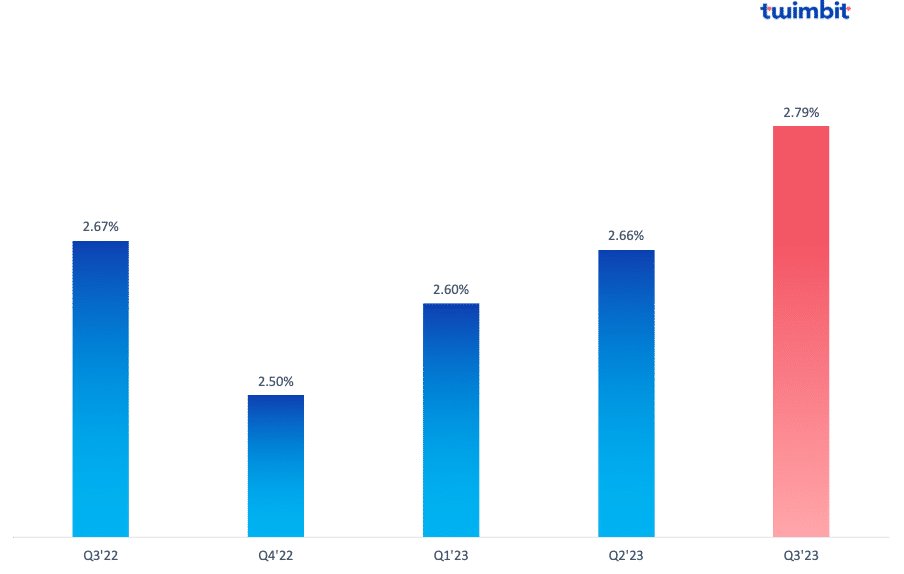

Non-performing loans (NPL)

NPL for the top 4 banks in the Philippines increased by 12 basis points in Q3 2023 compared to Q3 2022

The average NPL increased by 12 basis points from 2.67% in Q3 2022 to 2.79% in Q3 2023 (Exhibit 5).

Metrobank and BDO reduced their NPLs by 40 bps and 24 bps, respectively, between Q3 2022 and Q3 2023. Meanwhile, NPLs from Union Bank and BPI increased by 110 and 3 bps, respectively.

It should be noted that the NPL level for the Philippines’ banks is high due to the high NPL of Union Bank. The current NPL of Union Bank is at 5.5%, whereas the NPLs for all other banks in the Philippines are below 2%.

Exhibit 5: Consolidated non-performing loans of the Top 4 banks in the Philippines

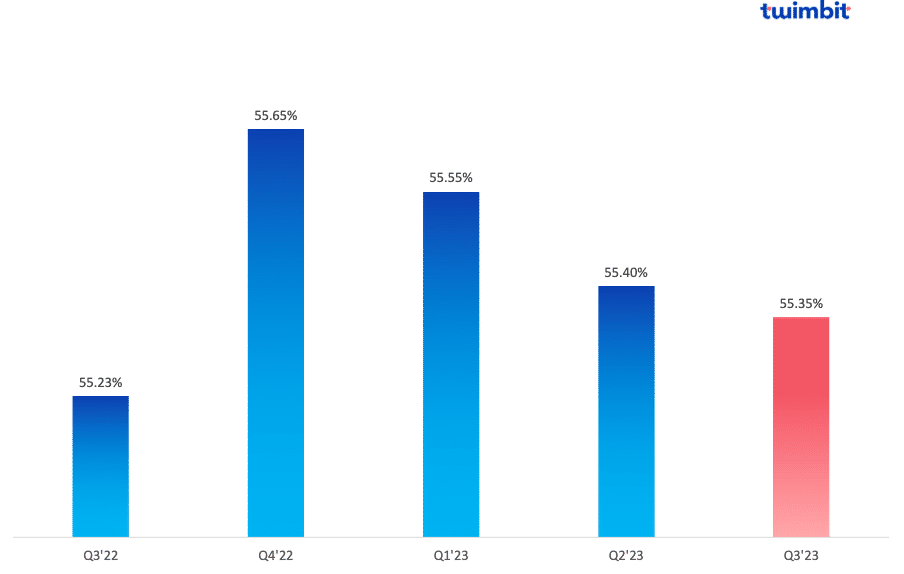

Cost efficiency (CE)

CE for the top 4 banks in the Philippines increased by 12 basis points in Q3 2023 compared to Q3 2022

Cost efficiency stood at 55.35% in Q3 2023 (Exhibit 6), indicating a lack of operational efficiency. This has slightly improved from the average cost efficiency of 55.40% in Q2 2023.

Although banks such as BPI, Metrobank and BDO reported improved cost efficiencies by 40 bps, 300 bps and 210 bps, respectively, only BPI has its cost efficiency below the threshold value of 50%.

Union Bank reported an increase in cost efficiency from 57% in Q3 2022 to 63% in Q3 2023. This significant increase in the bank’s cost efficiency is due to the integration and one-off expenses associated with acquiring Citibank’s consumer business. Excluding the integration costs and one-offs, the cost efficiency was 57% in Q3 2023.

Furthermore, the integration added USD 22 million to the bank’s operating expenses and accounted for 10.25% of these expenses.

Exhibit 6: Consolidated cost-efficiency ratio of the Top 4 banks in the Philippines

Initiatives by the top banks in the Philippines

- #1 Union Bank of the Philippines

Union Bank of the Philippines has received a certificate of authority from Bangko Sentral ng Pilipinas (BSP) to operate as a virtual asset service provider. This makes it the first universal bank in the Philippines to offer cryptocurrency trading on its mobile app.

- UnionBank will introduce a feature allowing some app users to trade Bitcoin directly.

- The bank plans a gradual rollout of this feature throughout the last quarter of 2023, offering customers a secure and convenient platform for cryptocurrency trading within a reputable financial institution.

- This development enables UnionBank’s customers to manage traditional banking and digital assets on a single mobile platform.

- Before obtaining this license, virtual asset exchange services were limited to a select group, accessible through a restricted virtual asset license.

- #2 Bank of the Philippine Islands

BPI Wealth, the wealth and asset management arm of BPI, is taking a major step in global expansion. The company has revealed intentions to launch a subsidiary in Singapore by Q1 2024. This move signifies BPI Wealth’s second foray into international markets, building on its earlier success in establishing a unit in Hong Kong during the early 2000s. The Hong Kong unit is licensed by both the Hong Kong Monetary Authority and the HK Securities and Futures Commission.

The Philippines’ banking sector is set for a promising 2023

In October, the Philippines experienced a notable reduction in annual inflation, declining from 6.1% to 4.9%, marking the first slowdown in three months. However, the central bank expressed concerns about inflation risks, emphasizing a notable inclination towards an upside trajectory. In response to the inflationary pressures, the central bank took proactive measures by resuming rate hikes. An off-cycle 25 basis point increase in October broke the trend of maintaining steady rates over the past four scheduled rate-setting meetings. This decision aimed to prevent inflation from escalating uncontrollably.

Despite the economy’s robust growth in the third quarter, surpassing expectations, the central bank anticipates moderate growth over the next few quarters. This cautious outlook is attributed to weak global growth and tighter financial conditions, indicating a comprehensive strategy to balance economic expansion and inflation control.

To learn more about the Philippines’ digital banking outlook, click here.

To learn about how the leading Indian banks performed in Q3 2023, click here.

To learn about how the top 3 Singapore banks performed in Q3 2023, click here.

To learn about how the top 5 Indonesian banks performed in Q3 2023, click here.

To learn about how the leading banks in South Korea performed in Q3 2023, click here.