Key highlights

- Economic growth slowed to 3.7% in H1 2023 from 8% in 2022, yet is expected to make a rebound in H2’23 at a moderate growth rate of 4.7%.

- A Challenging external environment and weaker domestic demand are leading to the slowdown.

- SBV (The State Bank of Vietnam) established a credit growth target of 15% for 2023 to address the economy’s capital requirements.

- The actual credit growth through August 2023 was at 4.3%.

- This is due to low capital absorption and subdued demand for business expansion.

- Overseas investors provide an essential source of capital for Vietnamese banks, helping to improve their capital adequacy ratios, which were among the lowest in the region.

- In 2022, Vietnam’s banking sector’s aggregate common equity Tier 1 ratio stood at 6.71%.

- Indonesia, Malaysia, Thailand and the Philippines were at 22.46%, 16.21%, 15.44% and 14.55% respectively.

- NPLs of many banks surged in H1’23 due to poor business performance of the whole economy.

- The average NPL of the top six banks increased by 37.23% between Q2 2022 and Q2 2023.

- The Central Bank of Vietnam has no regulatory framework for digital-only banks; therefore, the banks need to partner with licensed incumbent banks or function as a unit under them.

- Banks are in the digitalisation process by focusing on front-end channel development, including mobile banking, e-KYC, QR code payments and virtual assistants.

- BIDV has launched iBank, an omnichannel digital banking application for its institutional customers.

- Techcombank and VietinBank have completely revamped their mobile applications.

- BNPL is forecasted to witness exponential growth, creating an immense opportunity for banks to capitalise on this trend.

- Currently, none of the top Vietnamese banks offer a BNPL service.

Revenue

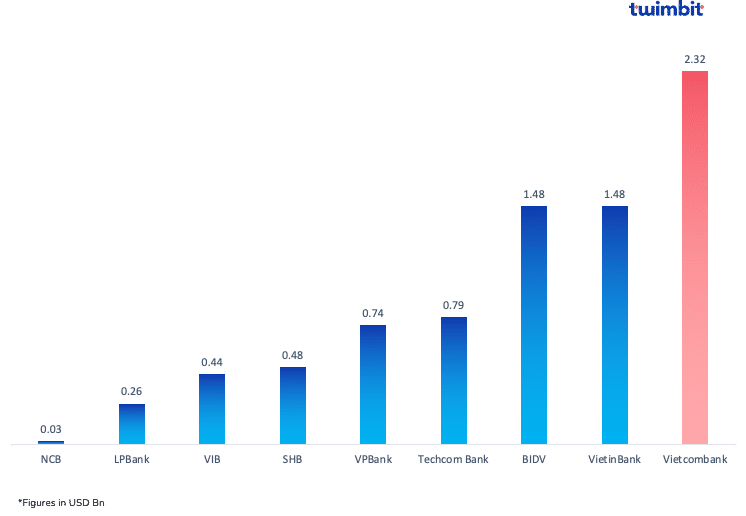

Vietnamese banks generated USD 7.75 billion in net revenues in H1 2023

The credit market experienced a decline starting in FY2022 and continued into FY2023 due to reduced borrowing amid the global economic downturn. Factors such as decreased export orders, high lending rates, and subsequent production declines contributed to this stagnation. However, government interventions aimed at supporting both borrowers and lenders have been instrumental. Anticipated reductions in policy rates are forecasted to reignite credit demand in the latter part of 2023.

Exhibit 1: Net revenues of Vietnamese banks in H1 2023

Note – Conversion rate used: 1 USD = VND 0.0007688

Fee-based income

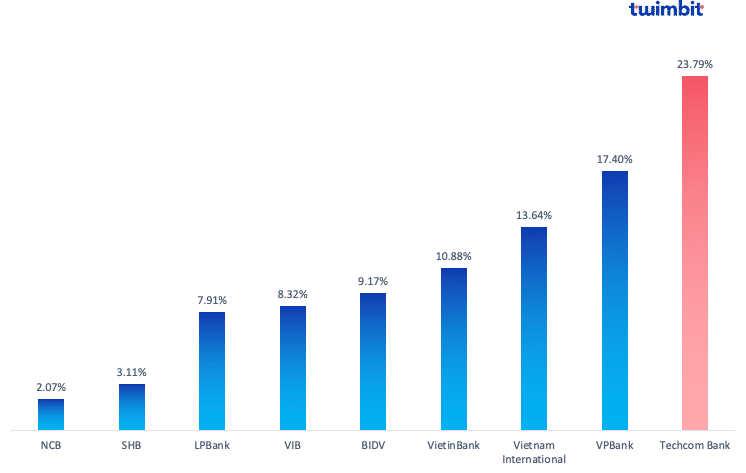

Vietnamese banks generate 11% fee income to revenue in H1 2023

- Techcom Bank generated the highest fee income to net revenues at 23.79%

- VietcomBank generated the highest fee income (regarding dollar value) at USD 193 million

Exhibit 2: Fee income to revenue of Vietnamese banks in H1 2023

Net interest margin (NIM)

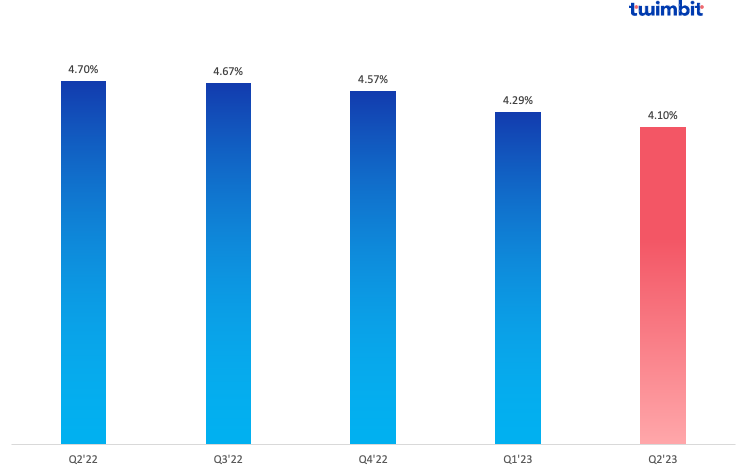

Top 6 banks in Vietnam witnessed a decline in average NIMs to 4.10% in Q2 2023

Interest income growth will slow down further due to decreasing net interest margins. The average net interest margins (NIM) of the top 6 banks in Vietnam have been steadily decreasing. This decline is due to low credit growth. The central bank anticipated a credit growth of 15% for 2023, but as of June 2023, the credit growth was far below the target at just 4.73%.

Exhibit 3: Consolidated NIM of the top 6 banks in Vietnam

Non-performing loans (NPL)

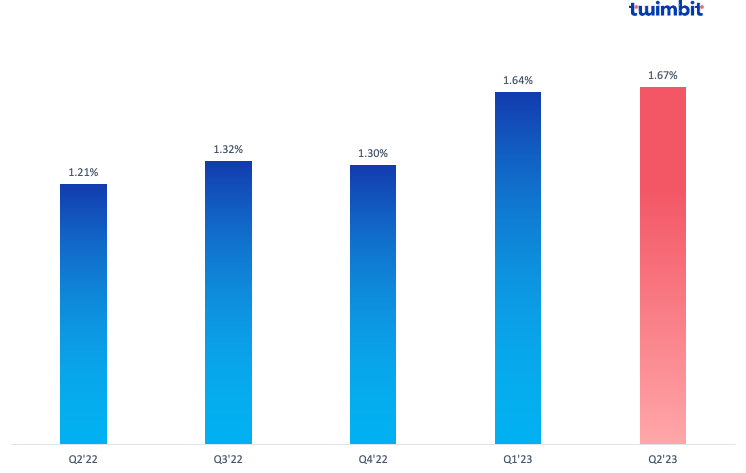

Top 6 banks in Vietnam recorded an average NPL of 1.67% in Q2 2023

The non-performing loan (NPL) situation escalated sharply by February 2023, reaching around 3% and doubling from the previous year-end. This rise has pushed numerous commercial banks beyond the 3% threshold, primarily due to struggling real estate and the corporate bond market, both sectors plagued by high NPLs and slow recovery. Banks are responding by reinforcing risk management measures, albeit at the expense of their profitability.

Despite its average, NPLs across the Vietnamese banking system have reached 3%, double the level at the end of 2021. This surge in NPL is reported as a result of poor business performance across the economy. However, these figures do not portray an accurate picture because the payment of many debts is rescheduled, and the number of NPLs will be higher.

Exhibit 4: Consolidated NPL of the top 6 banks in Vietnam

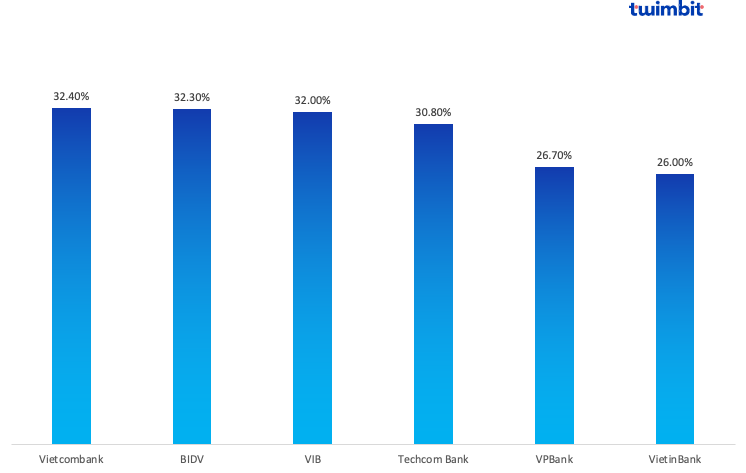

Cost efficiency (CE)

The CE of the top 6 banks in Vietnam ranges between 26% and 33%

Exhibit 5: CE of the top 6 banks in Vietnam

Growth opportunities for Vietnamese banks

- #1 Ensure credit growth at a steady and consistent rate

Outstanding loans over USD 526 billion significantly stifle the country’s aim to propel its credit growth by an additional 15%. This slow credit growth is due to:

- High-interest rates

- The central bank raised interest rates to combat inflation, making borrowing more expensive and reducing credit demand.

- Weak real estate market

- A slowing real estate market lowered demand for mortgage and real estate-related loans.

To boost credit growth, banks can:

- Offer competitive rates to attract borrowers and depositors with higher deposit rates

- Expand and introduce new products such as microfinance and green loans

- Digitalize and automate loan processes for faster and more efficient processing

- Promote financial inclusion by increasing customers’ access to credit and expanding the customer base

- #2 Focus on the development of digital-only banks

Neo banking in Vietnam is still in its early stages of development compared to other more established APAC markets. However, with increasing competition in Vietnam, banks are more focused than ever on narrowing their potential within the digital banking space.

Furthermore, the absence of a distinct licensing framework further incentivises digital banks in Vietnam to collaborate with established licensed banks or operate as a subsidiary within them.

- 70% of Vietnam are either unbanked or underbanked.

- The youthful demographic (under 35) comprises 70% of its population.

- Gen Z’s population is projected to reach 15 million by 2025.

Several Vietnamese banks have adopted digital transformation strategies during the digital financial services boom to enhance their financial service accessibility and convenience. These are:

- Timo

- Launched by VPBank in 2015 as Vietnam’s first digital bank

- Creative collaborations with 7-Eleven and McDonald’s to create Timo’s ‘hangouts’ – a location for prospective customers to sign up as Timo clients in just a few minutes

- Strong marketing team focus on its target segment: early adopters (individuals between 25 and 35)

- Customer base of more than 350,000 users

- TNEX

- Launched by Maritime Bank as Vietnam’s first digital-only bank

- Serve the Gen-Z population of the country with an agile and customer-centred, end-to-end digital banking offering

- Customer base of more than 1.5 million users

- Cake

- Launched as a collaboration between Be Group and VPBank

- Seamless integration with the ‘Be’ ride-hailing app enables VPBank to be the first Vietnamese bank to offer immediate mobile access to financial services to millions of consumers

- Targets the Gen-z and millennial groups

- Customer base of more than 3 million users

- #3 Buy Now Pay Later (BNPL)

In 2021, the BNPL market in Vietnam was valued at USD 496 million, projected to grow at a 45.2% CAGR from 2022 to 2028, reaching USD 4.7 billion.

This growth is driven by the expanding middle-class population and increasing consumer demand for flexible payment options. This phenomenon is further reinforced due to a low 6% credit card penetration. Because of this, the Vietnamese e-commerce market is expected to reach USD 32 billion by 2025, contributing to the popularity of BNPL.

While the top banks in Vietnam don’t currently offer BNPL services, certain smaller and international banks do.

A competitive BNPL offering will help Vietnamese banks in the following ways:

- Attract younger customers who prefer flexible payment options

- Increase customer engagement by offering a seamless and user-friendly payment experience

- Form new merchant partnerships to strengthen their network and expand the market reach

- Increased revenue from offering the service and thereby improved profitability

- Utilise customer data and insights from BNPL transactions and use them to cross-sell other products and services

In contrast, the BNPL model will take time as it will require banks and businesses to collaborate and:

- Educate customers on the benefits and convenience of BNPL services

- Integrate BNPL seamlessly into existing digital payment systems

- Embed BNPL services with popular shopping categories

- #4 Fee-based income generated through open banking

Slow credit growth continues to be a key factor in declining net interest margins, incentivising banks to uncover new revenue streams and generate fee income through open banking in the following ways:

- Account aggregation

- Consolidate customers’ financial information into a single platform or app.

- View all financial information in one place and help banks become a central hub for managing finances.

- Example: PhonePe, India – The API-based account aggregation services enable users to manage their finances, track transactions, transfer funds, and make payments seamlessly from the PhonePe app.

- Streamlined payments and transfers

- Simplify payment processes and facilitate more secure transfers through open banking.

- Initiate payments directly using open banking APIs.

- Eliminate the need for traditional payment methods and reduce transaction costs.

- Example: Paytm, India – This service leverages open banking APIs for faster and real-time transactions, improving payment and transfer speed for users.

- Lending and credit scoring

- Enhance lending processes by utilising customer financial data for accurate credit assessments and personalised loan products.

- Provide secure access to customer financial information.

- Example: MYbank, China – Mybank uses open APIs and collaborations with other financial institutions to gain access to consumer financial information. This enables them to assess the creditworthiness of borrowers accurately.

- Identity verification

- Simplify account verification and KYC processes with open banking.

- Verify customer identities more efficiently and securely by accessing customer financial data through open banking APIs.

- Enable more secure sharing of customer data for identity verification purposes.

- Example: CIMB Bank, Philippines – This bank leveraged Junio’s AI-powered end-to-end identity verification and authentication solution.

- Real-time fraud prevention

- Enhance fraud prevention capabilities through open banking APIs.

- Analyse customer financial data in real-time.

- Detect suspicious transactions or patterns.

- Take proactive measures to prevent fraud.

- Example: CommBank, Australia – CommBank utilises a fraud detection engine, driven by Al, equipped with real-time decline and hold intervention capabilities.

Best Practices by Vietnamese Banks

- #1 BIDV

Omni BIDV iBank:

- Launched an omnichannel digital banking application to provide customers with a seamless website and mobile platform experience

- Offers automated payroll payments, domestic and international money transfers, term deposits, state budget payments and many more

BIDV iConnect:

- Introduced iConnect to help businesses integrate banking services into their management software seamlessly for better payroll management, reconciliation, payments and invoicing

BIDV SMEasy:

- The first bank to provide a digital platform for SMEs

- Allows SMEs to access financial and non-financial services under a ‘One Stop Shop’ model both on the website and through the mobile app

- Developed through the cooperation of BIDV and the Asian Development Bank (ADB)

- #2 VietinBank

iPay:

- A revamped version of the bank’s Internet banking application

- Offers over 150 features and services with over 2,400 suppliers connected to fully meet customers’ needs

- Over 7 million monthly active users and more than 500 million transactions in H1 2023

eFAST:

- Provides businesses with a comprehensive suite of digital banking services, including account management fund transfers, payment processing and supply chain finance solutions

- More than 130 features and accounted for 82% of customer transactions in H1 2023

- Vietnam’s only digital banking platform that offers supply chain finance solutions

- #3 Vietcombank

VCB Digibank:

- A unified digital banking platform provides a seamless experience across all banking channels

- Offers services ranging from account management and bill payments to loan applications and investment services

- Facilitate online payment services for public services on the National Public Service Portal in Vietnam

- More than 7.5 million users in 2022

VCB CashUp:

- VCB CashUP is a wholesale banking platform powered by iGTB’s Payments and Cash Management solution

- Developed to digitise payment and cash management operations of businesses of all sizes

- Some of the features offered by CashUp:

- Enhanced liquidity management – Real-time visibility into cash flows

- Supply chain finance – Automate and streamline supply chain payments and receivables

- #4 TechcomBank

Mobile App:

- Functions as a “personal assistant in your pocket”

- Recorded over 840 million transactions in 2022 (90% of all annual retail transactions)

- The app allows customers to:

- Get instant credit card approval

- Improve their financial well-being by tracking spending and savings

- Automate bill payments and review their credit scores

BusinessOne:

- A suite of digital banking solutions designed for businesses of all sizes

- Offer solutions to streamline business operations and manage finances

- The BusinessOne package includes the following:

- BusinessOne Plus – Targets customers who incur large volumes of overseas transactions

- BusinessOne Connect – Targets customers who incur large volumes of domestic payment transactions

- BusinessOne Premium – Targets larger-scale enterprises with more incentives, decentralised account approval and two-layer security

- #5 Vietnam International Bank

MyVIB 2.0:

- The new mobile banking app is a technology product which focuses on implementing digitalisation and digital banking services

- The project focuses on investment converging three factors – Mobile first, Cloud first, and AI first

- The app is the first cloud-native app in Vietnam to provide an augmented reality (AR) experience and optimised customer experience on mobile devices

VIB Checkout:

- The proposition was implemented to meet the needs of MSME customers and provide them with access to digital banking services and a digital payment ecosystem

- The application allows customers to:

- Actively manage account information and transactions arising on the account

- POS payments on the application allow customers to accept payments from credit cards through NFC

Outlook for Vietnamese Banks in 2024

To control the rising tide of inflation in Vietnam, the State Bank has increased its interest rates to counteract the strain on bank profits and encourage greater borrowing between businesses and consumers. However, the country is also preparing itself for the inevitable high inflation rates that will persist through 2024, fuelled by escalating energy and food costs. Additionally, economic progress is anticipated to decelerate in 2024, influenced by global economic sluggishness and the ongoing US-China trade tensions, which are further likely to reduce loan demands and slow bank deposit growth.

The USA and Vietnam have introduced multiple economic growth propositions impacting the banking ecosystem and the local population. Entry of large players like DBS and UOB with their established banking environments will help Vietnamese banks learn.

To know about the State of Australian Banks in 2023, click here.

To know about the State of Indian Banks in 2023, click here.

To know about the State of Singapore Banks in 2023, click here.

To know about the State of Malaysian Banks in 2023, click here.