Key highlights

- GDP in South Korea grew by 0.5% in Q4-2023, marginally slower than 0.6% in Q3-2023.

- The current policy rate in South Korea is 3.5% (the highest in 15 years).

- The top 5 banks in South Korea aggregated a 5.9% increase in net revenues from USD 33.2 billion in FY-2022 to USD 35.2 billion in FY-2023.

- Net profits declined by 1.8% from USD 11.5 billion in FY-2022 to USD 11.3 billion in FY-2023.

- Average net profits declined from USD 2.30 billion to USD 2.26 billion.

- Fee income increased by 2.2% from USD 3.75 billion in FY-2022 to USD 3.83 billion in FY-2023.

- Hana Bank reported the highest increase at 12.91%.

- Average NIM increased marginally to reach 1.68% in FY-2023.

- NPL increased from 0.36% in FY-2022 to 0.42% in FY-2023.

- Cost efficiency improved significantly from an average of 41.89% in FY-2022 to 38.38% in FY-2023.

- Shinhan Bank launched Super SOL, a super app with all the core features of Shinhan’s various financial services.

- Woori Financial Group merges Woori Asset Management and Woori Global Asset Management into a new entity with USD 30 billion worth of assets under management.

- Hana Bank is partnering with BitGo to integrate advanced custody solutions for enhanced transparency and security.

- The loan portfolio for the top 5 banks in South Korea increased by 4.9% from USD 851.5 billion to USD 893.6 billion. In contrast, deposits grew by 3.2% from USD 0.99 trillion to USD 1.02 trillion.

Digital measures of success

- Hana Bank

- 15.4 million digital platform users in FY-2023

- 74.2% of mortgages processed digitally in Q4-2023

- 95.4% of unsecured lending was done digitally in Q4-2023

- Shinhan Bank

- 5.3 million daily active users for major digital platforms (DAU of SOL Bank, SOL Play, SOL Securities and SOL Life)

- 25 million monthly active users for major digital platforms

- 14% CAGR growth in digital operating profit from USD 1.4 billion in FY-2022 to USD 1.6 billion in FY-2023

- Woori Financial Group

- 20.7 million Woori WON banking app subscribers in FY-2023

- 79.5% of unsecured loans were processed digitally in FY-2023

- 84.4% of savings accounts opened digitally in FY-2023

- KB Kookmin

- Over 11 million monthly active users in FY-2023

Top innovations by South Korean banks

- Shinhan Bank

Super SOL

Super SOL by Shinhan Bank offers customers a seamless and efficient banking experience by consolidating the core features of Shinhan’s various financial services. Key features include:

- A customisable interface tailored to users’ preferences and usage habits

- Secure login options – pattern, fingerprint, iris, or password identification

- Integrated money transfer functionality, i.e., transfers to phone numbers

- Wide feature-range accessibility from a single screen

- Speed and user-friendly design for an enhanced customer experience

- Enhanced security measures to ensure customer protection in transactions

- Facilitates financial transactions conveniently on mobile devices

Group-wide cloud-based AI contact center

The AI contact centre (AICC) platform aims to streamline operations, reduce costs and improve customer service across Shinhan’s Financial Group affiliates.

- Shinhan Bank and Shinhan Card upgraded AI counselling, notification, and customer support services, utilising multimodal web views and AI voice bots for improved customer experience.

- Shinhan Investment & Securities plans to offer additional services via chatbots, while Jeju Bank introduces AI counselling and chatbot services tailored to local needs.

Future enhancements include speaker authentication and sentiment analysis for greater customer consultation convenience and management efficiency.

Shinhan ONE Data

One Data is a single, group-wide network that connects and standardises data across all its affiliates – Shinhan Bank, Shinhan Card, Shinhan Securities, and Shinhan Life Insurance.

- Enables more efficient analysis of customised data, providing more customised services for clients

- Plays a central role in group-wide projects, nurturing new growth engines and maximises customer value

Shinhan Financial Group positions One Data as a cornerstone of digital finance, aiming to lead the finance industry’s data ecosystem.

- Woori Financial Group

Merger of Woori Asset Management and Woori Global Asset Management

The new entity targets a comprehensive asset management company with USD 30 billion of operating assets, ranking as the 10th largest in the market. Woori aims to enhance its efficiency by leveraging each subsidiary’s expertise.

- Woori Asset Management – Stocks and bonds

- Woori Global Asset Management – Property, infrastructure, and alternative assets

The consolidation will result in a new entity, enhancing shareholder value and competitiveness by expanding non-banking sectors.

Global expansion

Woori Bank aims to achieve ~25% of net profits from global sales by 2030. Currently, overseas net profits accounted for 15.4% of total net profits in 2022, with Indonesia, Vietnam, and Cambodia accounting for 43%.

To achieve its goals, Woori Bank intends to:

- Invest USD 200 million each in Indonesia and Vietnam and USD 100 million in Cambodia in H1-2024

- Expand operations in Poland by converting its local office into a full-fledged branch to serve the financial service demands of Korean companies

Woori also aims to foster a strategic partnership with the US real estate platform BuildBlock.

- BuildBlock offers a wide range of real estate services, which encompass:

- Residential and commercial real estate brokerage

- Maintenance

- Post-sale payment recovery

- Tax support

- DinoLab (Woori Bank’s incubation initiative) aims to connect Woori Bank’s clientele with BuildBlock to streamline foreign real estate acquisitions and associated foreign exchange processes.

According to a Woori Bank official statement, the partnership can further enhance global property investments and facilitate easy entry for customers into overseas real estate investments.

- Hana Bank

Partnership with BitGO for digital asset custody

Accumulating over USD 448 billion in assets, Hana Bank aims to partner with BitGo to integrate advanced custody solutions to enhance transparency and security.

- Foster consumer trust by combining BitGo’s expertise with Hana Bank’s financial prowess and compliance standards

BitGo plans to establish an office in South Korea by late 2024 and recently secured USD 100 million in funding, raising its valuation to USD 1.8 billion.

Partnership of LINE Bank and CGV Cinemas Indonesia

This strategic collaboration aims to enhance banking services and support business expansion. For instance, using LINE FRIENDS characters can potentially attract customers to LINE Bank, as Park Jong Jin (CEO of Hana Bank) emphasised.

- Customers can easily conduct banking transactions and access CGV services using LINE Bank’s debit card and QRIS.

- The collaboration includes exclusive perks for BT21 Debit Card holders, such as discounted movie tickets.

The partnership aims to accelerate the growth of LINE Bank Debit Card users and enhance benefits for customers.

Revenue highlights

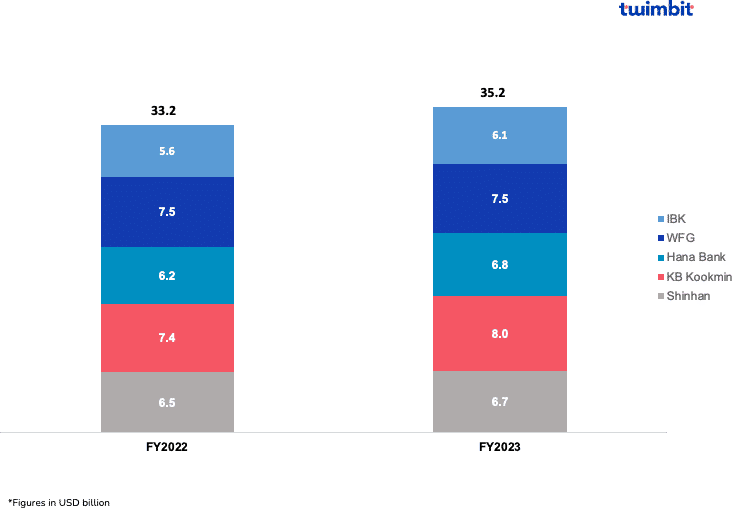

Net revenues for the top 5 South korean banks grew by 5.9% YoY

Aggregated net revenues increased from USD 33.2 billion in FY-2022 to USD 35.2 billion in FY-2023 (Exhibit 1). Average net revenues stood at USD 7 billion in FY-2023.

- 3.8% increase in the net interest income from USD 31.3 billion to USD 32.5 billion

- 43.8% increase in the non-interest income from USD 1.9 billion to USD 2.8 billion

Exhibit 1: Net revenues of the top 5 South Korean banks

- Hana Bank

- 10.4% YoY (year-on-year) increase in net revenues from USD 6.2 billion in FY-2022 to USD 6.8 billion in FY-2023

- 4.1% increase in net interest income from USD 5.8 billion in FY-2022 to USD 6.1 billion in FY-2023

- 116% increase in non-interest income from USD 0.4 billion in FY-2022 to USD 0.8 billion in FY-2023

The substantial growth in non-interest income was due to improvements in the bank’s accumulative fee income and fixed-income investment profits.

- Industrial Bank of Korea (IBK)

- 9.1% YoY increase in net revenues from USD 5.6 billion in FY-2022 to USD 6.1 billion in FY-2023

- 6.1% increase in net interest income from USD 5.4 billion in FY-2022 to USD 5.7 billion in FY-2023

- 92.8% increase in non-interest income from USD 0.2 billion in FY-2022 to USD 0.4 billion in FY-2023

KB Kookmin and Shinhan Bank reported an increase of 8.3% and 3.1% in net revenues, respectively. In contrast, Woori Financial Group did not report any change in net revenues between FY-2022 and FY-2023.

Profitability

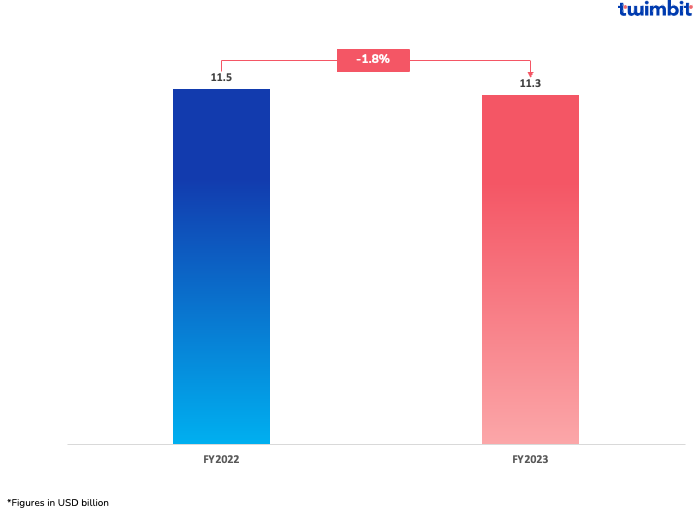

Net profits for the top 5 South Korean banks declined by 1.8% YoY

Aggregated net profit declined from USD 11.5 billion in FY-2022 to USD 11.3 billion in FY-2023 (Exhibit 2). Average net profit declined from USD 2.30 billion in FY-2022 to USD 2.26 billion in FY-2023.

Exhibit 2: Consolidated net profits of the top 5 South Korean banks

- Woori Financial Group

- 21.3% YoY decline in net profit from USD 2.6 billion in FY 2022 to USD 2 billion in FY 2023

- Driven by a 100% increase in impairment on credit loss from USD 678 million in FY-2022 to USD 1.4 billion in FY-2023

- Hana Bank

- 9.7% YoY increase in net profit from USD 2.4 billion in FY 2022 to USD 2.7 billion in FY 2023

- Driven by a 114.2% increase in the disposition and valuation income from USD 337.6 million to USD 723.1 million

Hana Bank also increased net interest incomes by 4.1% from USD 5.8 billion in FY-2022 to USD 6.1 billion in FY-2023. This increase was driven by a 6% increase in the bank’s loan portfolio from USD 209.9 billion to USD 222.5 billion.

Changes in net profits of other South Korean banks:

- Shinhan Bank – 2.9% decline

- IBK – 1.8% decline

- KB Kookmin – 8.9% increase

Fee-based income

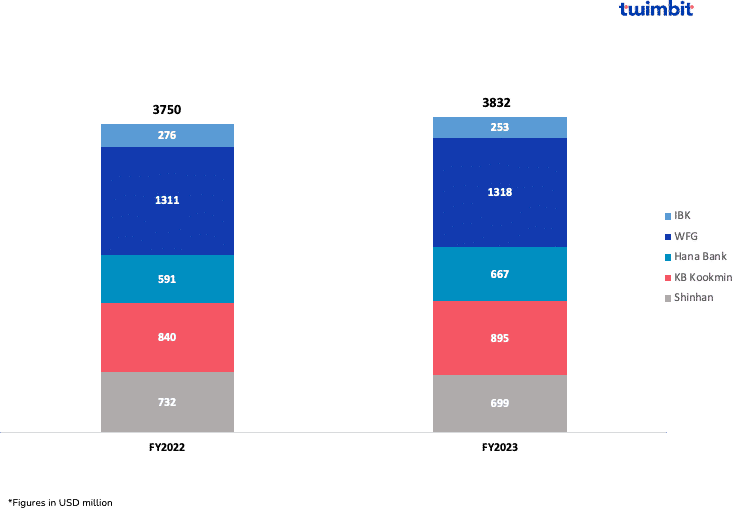

Fee income for the top 5 South Korean banks grew by 2.2%

Fee income grew from USD 3.75 billion in FY-2022 to USD 3.83 billion in FY-2023 (Exhibit 3).

Exhibit 3: Fee incomes fo the top5 South Korean banks

- Hana Bank

- 12.9% increase in fee income from USD 591 million in FY-2022 to USD 667 million in FY-2023

- Strong performance in fee items related to loans, bancassurance, and operating leases

- KB Kookmin

- 6.5% increase in fee income from USD 840 million in FY-2022 to USD 895 million in FY-2023

- 19.9% increase in trust income from USD 154 million to USD 184.62 million

- 23.51% increase in forex income from USD 244.4 million to USD 301.8 million

- Industrial Bank of Korea

- 8.2% decline in fee income from USD 276 million in FY-2022 to USD 253 million in FY-2023

Compared to its APAC peers, fee income is low in South Korea due to tighter rules and consumer behavior.

- Banks in South Korea cannot impose account-related fees such as monthly charges and commission fees due to government pressure and consumer backlash.

Net interest margins (NIM)

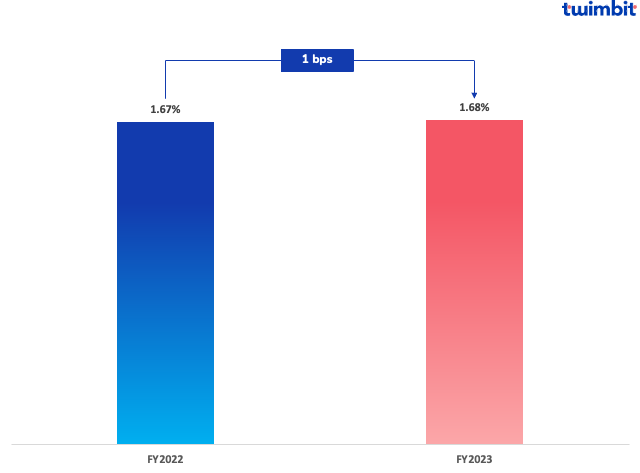

NIM for the top 5 South Korean banks increased by 1 basis point

The average NIM (net interest margin) increased from 1.67% in FY-2022 to 1.68% in FY-2023 (Exhibit 4).

- KB Kookmin – 10 bps increase

- IBK – 2 bps increase

- Shinhan Bank – no change

- Hana Bank – 2 bps decline

- WFG – 3 bps decline

Exhibit 4: Average NIM of the top 5 South Korean banks

South Korean banks have low-interest margins due to the following:

- Low-interest rates – Maintaining low-interest rates to spur economic growth has posed challenges for banks in generating interest income from loans, thereby exerting pressure on their profit margins.

- High reliance on retail banking – The heavy dependence on retail banking (which generally yields lower profits) has contributed to the diminished interest margins of Korean banks. Credit growth in South Korea has been slow, with an average growth of 6.3% to USD 1.1 trillion in Q3-2023.

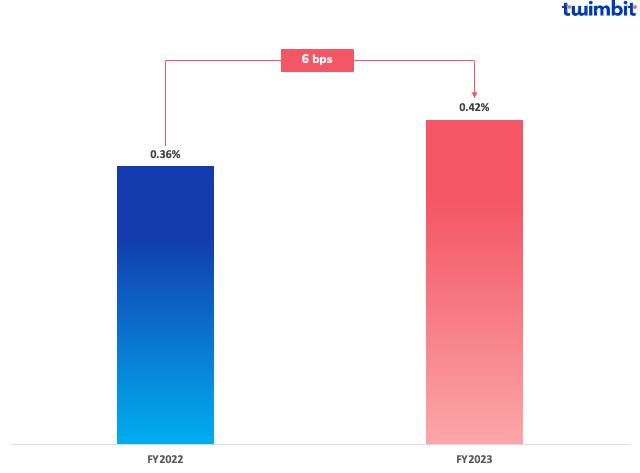

Non-performing loans (NPL)

NPL for the top 5 South Korean banks increased by 6 basis points

The average NPL increased from 0.36% in FY-2022 to 0.42% in FY-2023 (Exhibit 5). All banks reported an increase in NPL, with 3 of 5 reporting double-digit growths.

Exhibit 5: Average NPL of the top 5 South Korean banks

Typically, banks in South Korea have the lowest NPLs among APAC regions. This is due to:

- Strict lending standards – The stringent lending standards prevent loan extension to borrowers with doubtful repayment capabilities.

- Conservative provisioning – South Korea’s mandate to allocate substantial provisions for potential loan losses is vital because it allows banks to prepare the necessary funding required in case of non-repayment. This conservative strategy contributes to maintaining low Non-Performing Loan (NPL) ratios, even amid economic downturns.

- Effective debt collection – Banks in South Korea have leveraged the support of the country’s robust legal system to recover defaulting loans.

However, the recent increase in NPL among banks in South Korea is due to:

- Economic slowdown led to an increase in bankruptcies and loan defaults

- Rising interest rates increased the difficulty for businesses and individuals to repay their loans

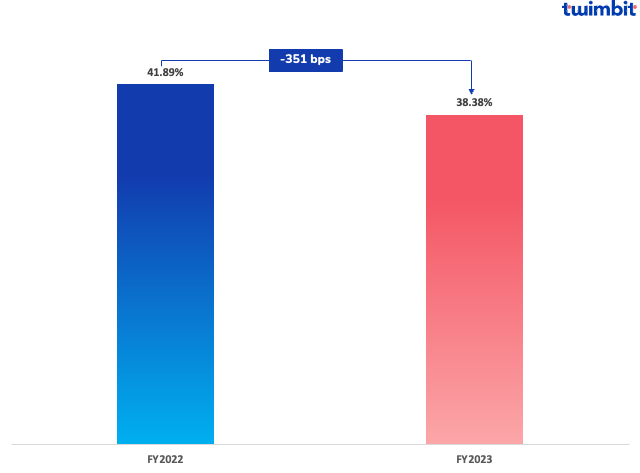

Cost efficiency (CE)

Cost efficiency for the top 5 South Korean banks improved by 351 basis points

The CE ratio significantly improved from 41.89% in FY-2022 to 38.38% in FY-2023 (Exhibit 6).

Exhibit 6: Average CE ratio of the top 5 South Korean banks

- KB Kookmin – 670 bps improvement

- Hana Bank – 605 bps improvement

- IBK – 478 bps improvement

- WFG – 20 bps improvement

- Shinhan Bank – 17 bps decline

- KB Kookmin

- Highest improvement in cost efficiency from 46.90% in FY-2022 to 40.20% in FY-2023

- Driven by a 3.8% decline in the bank’s operating expenses from 3.6 billion to USD 3.5 billion

Growth opportunities for South Korean Banks

- Embracing digitalisation

- Investing in AI and machine learning – South Korean banks should move beyond chatbots and leverage AI and machine learning (ML) to personalise customer experiences, automate tasks, and improve fraud detection.

- Leverage AI for data analysis to spot trends, helping banks offer personalised products to customers with different requirements

- Detect abnormalities early to prevent fraud and reduce loan defaults by restructuring loans

- Predictive analysis with AI can create risk models to calculate the likelihood of defaults and market volatility

- Develop AI-powered wealth management tools that tailor investment strategies to individual risk profiles and goals

- Expanding into new markets

- Focus on specific industries – South Korean banks can grow their international business through the following:

- Target high-growth sectors like healthcare, technology and renewable energy, offering industry-specific solutions

- Offer specialised financial products and services to Korean companies expanding into new markets

- Entering new geographical markets – Southeast Asia and China are new entry points for South Korean banks, providing the opportunity to:

- Partner with regional banks for cross-border financial services

- Explore untapped markets and uncover highly potential revenue streams

However, banks must carefully consider the risks of expanding into new markets.

- Focusing on the underserved segment

- Small and medium-sized enterprises (SMEs) – Banks should offer data-driven credit scoring models and alternative financing options like invoice or supply chain finance to overcome collateral limitations.

- Financial Literacy Programs – Partner with government agencies or NGOs to educate unbanked populations and build trust in the financial system, leading to increased account opening.

- Microfinance Services – Develop bite-sized microfinance products, including small loans and savings accounts, tailored to the needs of low-income individuals and entrepreneurs.

- Gamified finance and financial inclusion

- Develop gamified investment platforms – Target younger generations with engaging and educational finance apps that gamify investment and wealth management, fostering financial literacy and early engagement.

- Partner with educational institutions – Offer financial literacy programs within schools and universities, equipping students with essential financial knowledge and promoting early banking relationships.

- Create financial wellness programs – Partner with employers to offer financial wellness programs for employees, addressing financial stress and promoting financial security.

Increasing competition from Kakao Bank

Kakao Bank is South Korea’s most profitable digital bank. Primarily driven by Kakao Talk, the bank has gained over 21 million users and revenues totalling USD 823 million in FY-2022.

To compete with Kakao Bank, traditional banks must emphasise digital transformation, customer-centricity and strategic partnerships with other traditional banks. These also include:

- Leveraging the APIs of social media giants or creating in-house instant messaging banking capabilities to simplify the customer banking journey

- Adopting gamification practices to make your customers’ banking, budgeting, and savings experiences fun and engaging

- Extending your product offerings with an ecosystem approach to drive more diversified revenue streams

Outlook for 2024

The South Korean economy expanded by 0.5% in Q4-2023, with a YoY growth of 1.4%, slightly exceeding expectations. However, projected growth rates for 2023 and 2024 remain subdued at 1.3% and 2.4%, respectively, compared to the country’s potential growth rate of 2.9% between 2014 and 2019.

The Bank of Korea maintained the key interest rate at 3.5% for the eighth consecutive session to combat inflation. Despite concerns about potential fallout from project financing loans, the Bank of Korea stated that a rate cut is not imminent, focusing on market stability rather than individual crises.

The BOK’s current high interest rate environment is expected to dampen domestic activity, with the policy rate remaining at its highest level since 2008. Anticipated monetary loosening in the second half of 2024 may alleviate the impact, but sectors sensitive to interest rates, such as consumption and investment, may still face challenges. Retail trade volumes have declined, and consumer sentiment remains pessimistic, indicating ongoing weakness in domestic demand. After assessing the rate hike cycle’s effects, the Bank of Korea is anticipated to cut interest rates starting in the third quarter of 2024.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023. The current conversion rate is 1 USD = 0.00076608 KRW.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for 5 banks.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To know about the State of Australian banks in 2024, click here.

To know about the State of Thailand banks in 2024, click here.