ICT spending for APAC banks increased by 13.4% to USD 30.3 billion in 2023

ICT investments continue to flood in for APAC (Asia Pacific) banks, with key focus areas being AI and ML, data analytics, cloud computing, blockchain, cybersecurity and Generative AI (Gen AI). As a result, the ratio of ICT expenses to net revenue for banks in the APAC region has become more significant despite its varied nature.

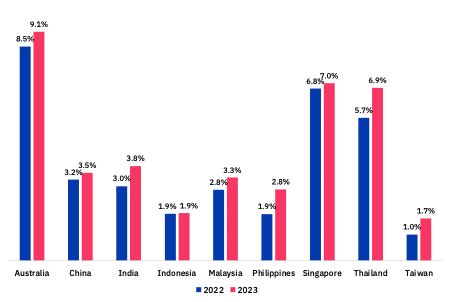

- Australian Banks have the highest ICT spend to net revenue in APAC

Australian banks have the highest ICT to net revenue spend among their APAC peers. The top six Australian banks spent USD 4.9 billion on ICT in 2023, a 6.1% increase from USD 4.6 billion in 2022.

- Banks in the Philippines reported a 52.8% increase in their ICT spend to net revenue

ICT to net revenue spend increased from 1.9% in 2022 to 2.8% in 2023 (Exhibit 1). Key areas of investment include big data & analytics and digital payments infrastructure.

Big Data & Analytics

- Bank of the Philippine Islands (BPI) – Leveraging big data analytics to derive customer behaviour insights, optimize marketing strategies, and enhance risk management.

- Metrobank – Deploying data analytics to improve decision-making, customer targeting, and operational efficiency.

Digital Payments Infrastructure

- BDO Unibank – Upgrading digital payments infrastructure to accommodate the increasing demand for cashless transactions, including QR code payments and mobile wallets.

- UnionBank – Advancing digital payment solutions via its EON digital banking platform, facilitating various cashless payment methods and seamless transactions.

- Indian Banks grew their ICT spend to net revenue by 27.1%

ICT to net revenue spend grew from 3% in 2022 to 3.8% in 2023, with heavy emphasis on AI & ML and open banking.

AI & ML

- HDFC Bank – Utilizes AI and ML for fraud detection, risk management, and personalized financial advice through its SmartHub 3.0 platform.

- ICICI Bank – Implements AI and ML to provide personalized customer services and enhance operational efficiency.

- Yes Bank – Introduced Yes ROBOT, an AI-powered chatbot for handling customer inquiries and transactions.

Open Banking

- Axis Bank – Launched an API Developer Portal providing APIs for fintech collaborations.

- The bank hosts more than 410 APIs, including more than 285 retail APIs and more than 25 connected APIs

- Axis Bank – Launched an API Developer Portal, offering over 410 APIs, including more than 285 retail APIs, facilitating fintech collaborations.

- Yes Bank – Established a comprehensive API ecosystem with over 450 APIs, fostering more than 30 fintech partnerships, with 15 additional partnerships in progress.

- Federal Bank – Offers a suite of over 300 APIs to more than 50 fintech companies, organized into 13 bundles, reinforcing its position in the fintech landscape.

Trends in the banking industry

- Artificial Intelligence and Machine Learning

- Customer Experience Enhancement – Leading financial institutions are leveraging AI to enhance customer interactions. AI-powered chatbots, such as DBS Bank’s Digibot in Singapore and Axis Bank’s AHA! in India, are at the forefront, providing instant responses to customer queries, facilitating account inquiries, and offering personalized product recommendations.

- DBS Bank Chatbots:

- Digibot – Available through the DBS Digibank app or website, offering 24/7 assistance for:

- Account inquiries – Balance checks, recent transactions, and cheque status.

- Card services – Card activation, lost/stolen card reporting, and credit limit changes.

- Payments – Bill payments and fund transfers.

- General information – Details on DBS products and services.

- Budgeting tools – Budget optimizer for expense tracking.

- Joy (DBS IDEAL) – Designed for corporate customers, assisting with:

- Company account inquiries – Balance and transaction retrieval.

- Business transactions – Cheque and trade status tracking.

- Platform navigation – Guidance on using DBS IDEAL interface.

- Digibot – Available through the DBS Digibank app or website, offering 24/7 assistance for:

- Axis Bank’s AHA! – An AI-powered virtual assistant aiding with:

- Account inquiries – Balance checks, mini statements, and cheque status.

- Card services – PIN changes, limit requests, and lost card deactivation.

- Payments – Online bill payments and fund transfers.

- General information – Access to a wide range of banking FAQs.

- DBS Bank Chatbots:

- Fraud Detection and Prevention – AI and ML algorithms analyze vast amounts of real-time transaction data to identify suspicious activities and potential fraud attempts. ICICI Bank in India exemplifies this by detecting anomalies in transaction patterns, thereby preventing fraudulent transactions.

- Credit Risk Assessment – ANZ utilizes AI and ML algorithms to analyze data points such as credit scores, transaction history, and behavioural patterns for accurate credit risk assessments and personalized solutions.

- Automated Compliance and Regulatory Reporting – AI and ML streamline compliance processes, reducing manual efforts and operational costs. For instance, Mizuho Bank in Japan uses AI to automate anti-money laundering (AML) compliance and detect suspicious transactions more efficiently.

- Algorithmic Trading and Investment Management – AI’s ability to analyze market data, identify trading opportunities, and optimize investment strategies is exemplified by DBS Bank in Singapore, which uses AI-driven trading algorithms for effective trade execution and portfolio management.

- Digital Transformation and Automation – ICBC Bank in China employs AI-powered robotic process automation (RPA) to automate routine tasks such as data entry and document processing, enabling employees to focus on higher-value activities

- Generative AI

- OCBC’s Generative AI Chatbot (Microsoft Azure) – OCBC has deployed a generative AI chatbot for its 30,000 employees, including those at the Bank of Singapore. Donald MacDonald, head of the Group Data Office, emphasizes its potential to automate tasks and enhance customer service.

- United Overseas Bank (Microsoft) – As part of the Microsoft 365 Copilot Early Access Program, 300 UOB staff members will use AI tools to enhance operational efficiency and collaboration by:

- Summarizing extensive documents, emails, and virtual meetings.

- Converting raw data into graphical spreadsheet representations.

- Seamlessly searching and referring to internal bank information.

- Compiling relevant data for current tasks.

- Creating dynamic presentations and tailoring communication tone.

- BRI (Google Cloud and iZeno) – BRI’s collaboration with Google Cloud and iZeno aims to enhance digital banking services and promote financial inclusion across Indonesia. Key initiatives include:

- iZeno – Providing cloud infrastructure management, application modernization, and DevOps consultancy.

- Google Cloud Solutions – Accelerating API onboarding and data integration.

- Atlassian IT Service Management – Facilitating application development, testing, and deployment in a DevOps environment.

The partnership also includes a data analytics modernization proof of concept (POC) to migrate data sources onto Google Cloud, with iZeno currently developing applications to serve as a framework for this migration process.

- Data Analytics and Cloud Computing

- DBS Bank

- Adopted a cloud-first strategy, migrating core banking systems and digital channels to the cloud.

- Utilizes cloud-based data analytics for customer insights, personalized recommendations, and marketing campaigns.

- Develops and deploys mobile banking apps and digital wealth management platforms using cloud computing.

- Commonwealth Bank of Australia (CommBank)

- Migrated IT infrastructure, core banking systems, and customer-facing applications to the cloud.

- Analyzes transaction data in real time to identify and prevent fraudulent activities.

- Developed blockchain-based solutions like the CBA Bond-I for cloud innovation.

- ICICI Bank

- Embraces cloud computing for digital banking initiatives, mobile banking apps, and online loan application platforms.

- Uses cloud computing for regulatory compliance, ensuring data security and privacy.

- OCBC Bank

- Migrated core banking systems to the cloud for scalability and resilience.

- Utilizes ML algorithms to analyze transaction data and customer interactions for personalized recommendations.

- Employs chatbots and virtual assistants for personalized customer service across digital channels.

- Cybersecurity

- ICICI Bank – Implements multi-factor authentication (MFA) using passwords, OTPs, biometrics, and device authentication to prevent unauthorized access.

- Mizuho Bank – Conducts regular cyber drills and simulations to test incident response procedures and ensure cybersecurity readiness.

- Taiwan Cooperative Bank – Collaborates with industry peers to defend against cyber threats and strengthen overall cybersecurity posture.

- Blockchain / Distributed ledger Technology (DLT)

- National Australia Bank (NAB) – Collaborated with eight banks to develop Carbonplace, a DLT-based marketplace for carbon offsets. Key features include:

- Secure and Transparent Trading – Transactions of certified carbon credits are conducted through a network of participating banks, ensuring a standardized and trustworthy environment.

- Focus on Voluntary Carbon Credits (VCCs) – These credits represent emission reductions achieved through projects not mandated by regulation.

- Commonwealth Bank of Australia (CBA) – Partnered with Biodiversity Solutions Australia to create a blockchain-based platform for “BioTokens” under the NSW Biodiversity Offsets Scheme. Benefits include:

- Transparent and efficient real-time credit trading.

- New income sources for landowners maintaining biodiversity.

- CBA Bond-i – Developed Bond-i, the first blockchain-operated debt instrument, in partnership with the World Bank, enhancing efficiency, transparency, and security.

- DBS DDEX – Launched a digital asset exchange platform allowing institutional and accredited investors to trade digital currencies like Bitcoin, Ethereum, and XRP.

- CIMB – Collaborated with Ripple to enable instant cross-border payments, expanding Speedsend by opening new payment corridors and improving consumer access to remittances.

- Opening new payment corridors to improve consumer access to cross-border remittances, both inbound into ASEAN and outbound to other countries

- Enabling remittances via corridors such as Australia (in partnership with Instarem, also a member of RippleNet), the USA, the UK and Hong Kong

ICT Contracts

- Westpac signs five-year deal with AWS

In a significant move to bolster its hybrid cloud strategy, Westpac has signed a new five-year agreement with Amazon Web Services (AWS) in 2023. This partnership, which began in 2015 with AWS hosting Westpac’s website, underscores Westpac’s ongoing commitment to cloud services. Key elements of the deal include:

- Leveraging AWS Technology – Utilize AWS’s machine learning, computing, and data analytics capabilities to enhance cost efficiency.

- Cloud Adoption – Demonstrate Westpac’s continued integration of cloud services.

- Employee Training – Provide Westpac employees access to AWS Industry Quest, a training platform for building cloud solutions.

Westpac remains cautious about fully adopting generative AI, preferring human oversight in customer interactions while exploring advanced technologies like Conversational AI and Banking-as-a-Service.

- ANZ and HCL Tech partner for digital transformation

ANZ has partnered with HCL Tech in 2023 to transform the digital employee experience across 33 countries. The partnership aims to:

- Next-Gen Technologies – Employ GenAI, extended reality, and IoT-powered workspaces to create immersive, sustainable, and inclusive work environments.

- Digital Workplace Services – Provide comprehensive digital workplace services and experience management for end-user devices and applications.

- Bank Muamalat’s multi-year partnership with Google Cloud

In 2024, Bank Muamalat entered a multi-year partnership with Google Cloud to accelerate its digital transformation. The key objectives are:

- Personalized Digital Services – Offer personalized and inclusive digital Islamic banking services.

- Cloud Solutions Adoption – Implement Google Cloud’s infrastructure modernization, developer cloud, cybersecurity, and data storage solutions.

- Data Consolidation – Use the Google Marketing platform and business intelligence tools to consolidate and analyze first-party data for Gen AI applications.

- AI-Driven Insights – Leverage Google’s Vertex AI Search and Conversation platform for better data insights.

- Enhanced Offerings – Complement existing cloud-based core banking and engagement platforms with enhanced Sharia-compliant financing and deposit offerings.

- Public Bank and Maxis collaborate for SME digital adoption

In 2024, Public Bank and Maxis collaborated to promote digitalization among Malaysian SMEs. The collaboration includes:

- Awareness Programs – Joint initiatives to promote digital solutions and financial assistance to SMEs.

- Digital Partnership – Maxis Business becoming the official telco and digital partner of Public Bank’s PB enterprise Digital SME Assist Program.

- Government Grants – Assistance for SME customers to obtain government digitalization grants and financing solutions.

- BRI invests in financial inclusion with E9pay

BRI’s 2024 investment in E9pay aims to enhance financial services for Indonesian migrant workers, students, and spouses in Korea. Key aspects include:

- Specialized Services – Provide convenient and accessible financial services akin to those in Indonesia.

- Remittance Services – Strengthen remittance services between Korea and Indonesia with native-language support and efficient money transfers.

- Bank of Thailand and Bank of Laos cross-border QR payments agreement

The 2023 agreement between the Bank of Thailand and the Bank of Laos facilitates cross-border QR payments. Highlights include:

- Payment Convenience – Enable users to scan QR codes for payments across both countries.

- Economic Boost – Enhance trade, investment, tourism, and local currency usage, supporting a tourism sector that reached two million travelers in 2023.

Participating banks, including Bank of Ayudhya and Krungthai Bank from Thailand and several Laotian banks, will offer these services via mobile apps.

- Union Bank of India and Accenture’s data-driven transformation

The 2023 collaboration between Union Bank of India and Accenture focuses on accelerating data-driven transformation through:

- Advanced Analytics – Utilize predictive analytics, machine learning, and AI to generate actionable insights.

- Data Visualization – Develop robust data visualization and reporting capabilities for improved business intelligence.

- Banking Segments – Apply these technologies across corporate, retail, MSME banking, risk management, and customer service.

- AI Models – Create AI models for business forecasting, personalized offers, and fraud detection.

- Cultural Shift – Foster a customer-centric, agile, and innovative culture by democratizing data-driven insights.

- IndusInd Bank and Viamericas launch ‘Indus Fast Remit’

In 2023, IndusInd Bank and Viamericas launched the ‘Indus Fast Remit’ platform for NRIs in the US, offering:

- Competitive Rates – Competitive exchange rates for digital inward remittances to India.

- Convenient Transactions – Options for auto debit payments and overseas bank transfers.

- Real-Time Updates – Real-time updates on payment status, amount, and expected delivery time.

- Bank of Baroda partners with Tech Mahindra

Bank of Baroda’s partnership with Tech Mahindra aims to enhance customer service through digital solutions. Key initiatives include:

- Centre of Excellence – Establish a groundbreaking Centre of Excellence (CoE) for Bank of Baroda’s Contact Centre.

- Operational Efficiency – Enhance efficiency and provide immersive customer experiences using digital solutions.

- Advanced Technologies – Implement AI, Blockchain, 5G, AR, and VR to improve customer experiences.

- Innovative Tools – Introduce speech analytics, quality monitoring, knowledge management portals, conversational IVR, and BOT-based training tools.

- Indian banks and JPMorgan’s blockchain-powered settlement system

In 2023, HDFC, ICICI, Axis Bank, Yes Bank, and IndusInd Bank collaborated with JPMorgan to explore blockchain technology for 24×7 dollar-based settlement services. Objectives include:

- Addressing Limitations – Overcome the limitations of the Swift messaging system and Nostro accounts.

- On-Chain Nostro Accounts – Establish on-chain Nostro accounts with JPMorgan’s branch in Gift City.

- Instant Settlements -Enable instant, round-the-clock settlements between accounts.

- Intra-Correspondent Network – Create a private banking network for seamless transfers.

- BRI partners with Tencent Cloud and Hi Cloud Indonesia

BRI’s collaboration with Tencent Cloud and Hi Cloud Indonesia aims to drive banking technology innovation through:

- Customer Service Improvement – Enhance customer service and transactional experiences with cutting-edge technology.

- Cloud Infrastructure – Leverage Tencent Cloud’s advanced infrastructure to boost digital solutions in Indonesia.

- Krungthai and IBM collaboration for sustainable growth

Krungthai Bank’s partnership with IBM aims to establish the IBM Digital Talent for Business (IBMDT) initiative, focusing on:

- Technological Enhancement – Enhance traditional banking services with advanced technology for efficiency and sustainability.

- Strategic Alignment – Align with Krungthai’s “7 North Star” strategies to maintain competitiveness and innovation.

- Agile Methodology – Utilize IBM GarageTM methodology for greater agility and operational speed.

IBMDT will contribute to modernizing Krungthai Bank’s IT infrastructure, ensuring security, stability, and efficiency to support the bank’s technology-driven growth plans.

Innovation insights

- Blockchain

The Indian Banks’ Blockchain Infrastructure Co Pvt Ltd (IBBIC) consortium is spearheading the adoption of blockchain technology among Indian banks. This consortium includes:

- Public Sector Banks – State Bank of India (SBI), Bank of Baroda (BoB), Canara Bank, and Indian Bank.

- Private Sector Banks – ICICI Bank, HDFC Bank, Kotak Mahindra Bank, Axis Bank, IndusInd Bank, Yes Bank, RBL Bank, South Indian Bank, Federal Bank, and IDFC First Bank.

- Foreign Bank – Standard Chartered.

These banks are leveraging the Infosys Finacle Connect platform to:

- Digitize and automate the handling of inland letters of credit (LCs)

- Reduce transaction times from several days to a few hours

- Minimize paperwork and enhance security by preventing fraud

This initiative is anticipated to significantly benefit medium and small-scale enterprises (MSMEs) by making the process more efficient and secure, thereby facilitating smoother trade finance operations.

For banks in other countries looking to adopt blockchain technology, we recommend the following steps:

- Form a Consortium – Pool resources and expertise from multiple banks to share costs and benefits.

- Select a Robust Platform – Utilize a proven blockchain platform like Infosys Finacle Connect.

- Engage Regulators Early – Ensure compliance through early and continuous engagement with regulatory authorities.

Pilot programs and collaboration with technology firms are essential to test and refine the system before a full-scale rollout. To effectively implement blockchain, banks should consider:

- Pilot Programs – Test and refine the system in collaboration with technology firms before full-scale rollout.

- Staff Training – Invest in training for staff and specific use cases like digitizing letters of credit.

- Security Measures – Implement strong security measures to protect sensitive data.

- Customer Communication – Clearly communicate the benefits of blockchain to customers and stakeholders.

- Scalability – Design the system for scalability and future integration with other financial institutions.

- Data Analytics

- Hyper-Personalized Products and Services – JPMorgan Chase uses data analytics to tailor investment products and wealth management strategies to each client’s risk tolerance and financial goals.

- Fraud Detection and Risk Management – Citigroup employs advanced machine learning models and data analytics to identify hidden patterns and flag suspicious activity in real-time, preventing financial losses.

- Dynamic Pricing and Revenue Optimization – Bank of America uses data analytics to adjust loan interest rates dynamically based on real-time market conditions and customer profiles.

- Cloud Computing

- Improved Scalability and Agility – Banks can scale IT infrastructure up or down based on demand, enabling greater cost savings and faster response times to change market conditions. Banks like HSBC have migrated core banking operations to the cloud, achieving greater scalability and agility to better respond to fluctuating customer demands.

- Enhanced Security and Compliance – Standard Chartered leverages cloud computing to ensure robust data security and streamline regulatory compliance processes.

- Innovation and Collaboration – Barclays uses cloud computing to foster innovation and collaboration with fintech startups, facilitating secure data sharing and co-creation of new financial solutions.

- Cybersecurity

- Harnessing AI and ML – JPMC (JPMorgan Chase) utilizes AI to analyze network traffic and identify potential breaches, thus mitigating the impact of cyberattacks.

- Investing in Zero Trust Architecture – This security model assumes no user or device is inherently trustworthy and requires continuous verification. Citigroup’s zero-trust security model ensures only authorized users and devices access sensitive information, significantly reducing the attack surface.

- Building a Culture of Cybersecurity – Cybersecurity is not just a technical issue; it’s an organizational one. HSBC promotes cybersecurity awareness through training programs and simulations, empowering employees to identify and report suspicious activity.

- Embracing Secure Cloud Solutions – Banks can leverage secure cloud solutions offered by major cloud providers like Microsoft Azure or Amazon Web Services (AWS) to benefit from robust security features and expertise. Barclays has migrated a significant portion of its infrastructure to the cloud, utilizing cloud providers’ advanced security features.

- Collaboration and Information Sharing – Cybercriminals often target multiple institutions. By collaborating and sharing threat intelligence with other banks and law enforcement agencies, banks can stay ahead of evolving threats and improve their collective defences. Industry-wide efforts like the Financial Services Information Sharing and Analysis Center (FS-ISAC) facilitate information sharing and collaboration on cybersecurity threats.

- Generative AI

- Enhanced Risk Management – Gen AI can analyze massive datasets to unearth patterns and assess creditworthiness. This empowers banks to make informed lending decisions, like those at Wells Fargo. They use a Gen AI-powered feature that analyzes customer data to predict potential financial difficulties and tailor loan products accordingly, reducing defaults and improving risk profiles. Additionally, Gen AI can automate tasks like generating reports and flagging suspicious activity for fraud prevention.

- Personalized Customer Experiences – The Royal Bank of Canada (RBC) developed the “Aiden Platform” – a virtual assistant powered by Gen AI. This platform personalizes the customer experience with product recommendations, targeted financial advice, and custom reports.

- Efficient Content Creation – Gen AI can automate the generation of various reports, contracts, and marketing materials. This frees up valuable staff time and ensures consistency in messaging across the bank.

- Regulatory Compliance – Gen AI can stay updated and automatically adjust internal processes to ensure compliance. This reduces the risk of fines and penalties for non-compliance, as seen with PKO Bank Polski in Poland. They utilize Gen AI to automate the Know Your Customer (KYC) process, which involves analyzing customer data to verify identity and prevent fraud. Gen AI streamlines the process and reduces onboarding times for new customers, while also adhering to KYC regulations.

- Improved Fraud Detection – Gen AI can analyze transaction patterns to identify anomalies and flag potential fraudulent activity. By implementing Gen AI for fraud detection, banks can significantly reduce the number of fraudulent transactions.

Research Methodology

- Our data collection process leveraged secondary research, drawing on information provided by the respective banks through their investor presentations and quarterly financial statements. To ensure consistency and comparability, Twimbit adheres to a calendar year approach for this analysis, defining Q1 as the period from January to March of the year.

- For a fair representation and analysis, we utilized a constant currency rate for converting local currencies to USD. The USD conversion rate used in this report is the average value calculated from January to March 2024.

- This report examines the ICT expenditure relative to net revenue for banks across several key markets, including Australia, China, India, Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Taiwan.

- It is important to note that communication expenses have been excluded from our analysis. This decision was made because the reported communication expenses encompass other variables (such as branch communication and marketing communication) that do not constitute a part of a bank’s ICT spend.

To learn about the State of APAC Banks in 2024, click here.