Key Highlights

- Net revenues increased from USD 14.3 billion in FY-2022 to USD 19.1 billion in FY-2023

- Net profits of the top 8 Indian banks increased by 36% from USD 16 billion in FY-2022 to USD 22 billion in FY-2023.

- All banks except for Axis Bank reported an increase in their net profit.

- Fee income of the top 8 Indian Banks increased from USD 14.2 billion in FY-2022 to USD 14.8 billion in FY-2023

- Kotak Mahindra Bank reported the highest increase in fee income at 25%, from USD 523 million in FY-2022 to USD 659 million in FY-2023.

- The average NIM (Net interest Margin) increased from 3.65% in FY-2022 to 3.99% in FY-2023.

- The average NPL (Non- Performing Loans) improved from 3.54% in FY-2022 to 2.99% in FY-2023

- Cost efficiency stood at 45.60 % in FY-2023, up from 45.13% in FY-2022

- The leading 8 banks’ loan portfolio grew by 23.9% YoY from USD 1.1 trillion in Q4-2022 to USD 1.3 trillion in Q4-2023

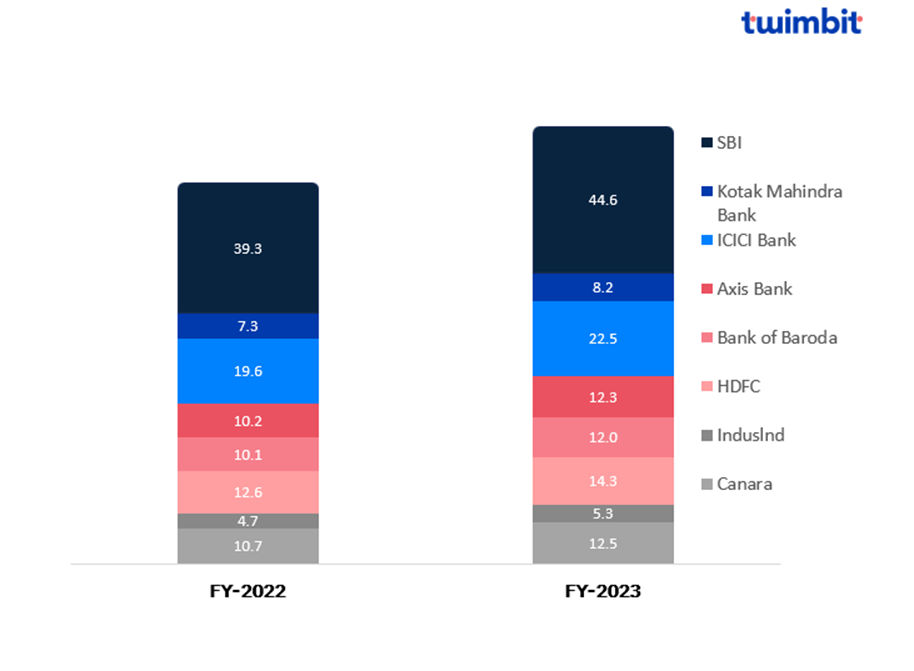

Revenue highlights

Top 8 Indian banks Net Revenue surge by 15%, showing a double-digit growth for all

Net revenues increased from USD 114.8 billion in FY-2022 to USD 132 billion in FY-2023 (Exhibit 1).

Exhibit 1: Net revenues of the top 8 Indian Banks

Source: Bank Financials, Twimbit analysis

Axis Bank

Axis Bank reported highest growth at 19.7%, increasing from USD 10.2 billion in FY-2022 to USD 12.3 billion in FY-2023. This is because of:

- Strong turnover in total deposits and advances by 16% by enhancing the quality and diversity of the financial products.

- The domestic loan book expanded by 23% YoY. Mid Corporate, SME and Small Business Banking (SBB) grew by 32% YoY and now constitute 20% of overall loan book.

All banks reported an increase in their net revenues between FY-2022 and FY-2023.

- Canara Bank: 16.8%

- IndusInd Bank: 13.5%

- HDFC Bank: 13.1%

- Bank of Baroda: 19%

- Axis Bank: 19.7%

- ICICI Bank: 14.9%

- Kotak Mahindra Bank: 12.9%

- State Bank of India: 13.4%

In FY-23, The top 8 Indian banks have seen strong revenue growth due to a few key factors like increase in net interest income, boosted by higher lending and deposits which played a significant role in increase of revenue. Moreover, the economy’s robust GDP growth of 7.2% has stimulated economic activity, leading to greater demand for loans and deposits.

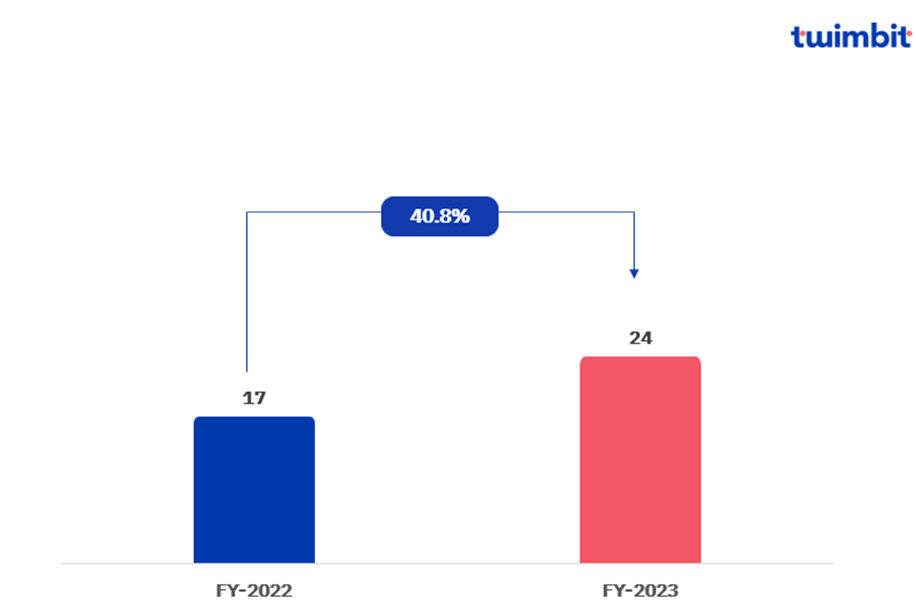

Profitability

The top 8 Indian banks saw a robust 40.84% year-on-year increase in net profit, reflecting significant double-digit growth

Net profits increased from USD 17 billion in FY-2022 to USD 24 billion in FY-2023 (Exhibit 2). Average net profits increased from USD 2.1 billion in FY-2022 to USD 2.9 billion in FY-2023.

Exhibit 2: Aggregated net profits of the top 8 Indian banks

Source: Bank Financials, Twimbit analysis

Bank of Baroda

Bank of Baroda reported highest growth at 88.7%, increasing from USD 906.2 million in FY-2022 to USD 1.7 billion in FY-2023. This is because of:

- The Net Interest Income (NII) of the bank increased reflecting a YoY growth of 26.8%.

- The Operating Income of the bank increased showing a YoY growth of 16.5%.

All banks reported an increase in their net profits in FY-23.

- Canara Bank: 81%

- IndusInd Bank: 50.6%

- HDFC Bank: 16%

- Bank of Baroda: 88.7%

- Axis Bank: 63.7%

- ICICI Bank: 32.9%

- Kotak Mahindra Bank: 20%

- State Bank of India: 54%

The increase in net profit is due to factors such as improved Return on Assets (ROA) and Return on Equity (ROE) which shows greater efficiency in leveraging assets and equity to boost earnings. Additionally, growth in Net Interest Income (NII) signified the enhanced profitability from the core banking activities, supported by effective management of interest rate spreads and asset quality.

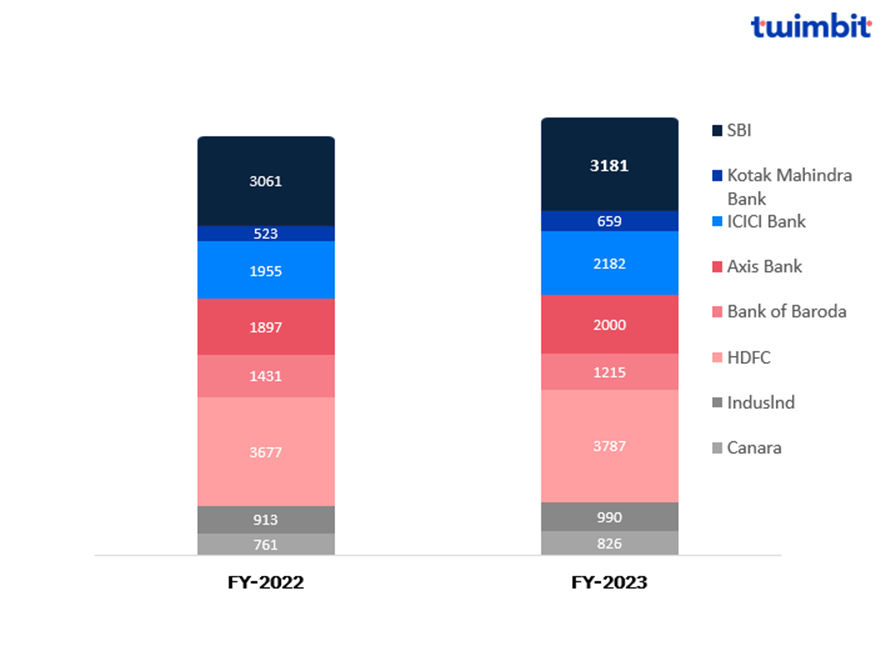

Fee-based income

Fee income for the top 8 Indian banks grew by 4.3% YoY

The top 8 Indian banks grew their fee income from USD 14.2 billion in FY-2022 to USD 14.8 billion in FY-2023 (Exhibit 3).

Exhibit 3: Fee income of the top 8 Indian banks

Source: Bank Financials, Twimbit analysis

Kotak Mahindra Bank reported the highest fee income increase at 25%, from USD 523 million in FY-2022 to USD 659 million in FY-2023. This growth was due to:

- 8.7% increase in commission, exchange and brokerage fees from USD 0.9 billion in FY-2022 to USD 0.99 billion in FY-2023.

- 15% increase in premium fees for insurance business from USD 1.6 billion in FY-2022 to USD 1.9 billion in FY-2023.

Other factors include increased income from the profit on:

- Sale of investments

- Sale of building and other assets

- Exchange on transactions

Bank of Baroda is the only bank that reported a decline in fee incomes by 15% from USD 1.4 billion in FY-2022 to USD 1.2 billion in FY-2023.

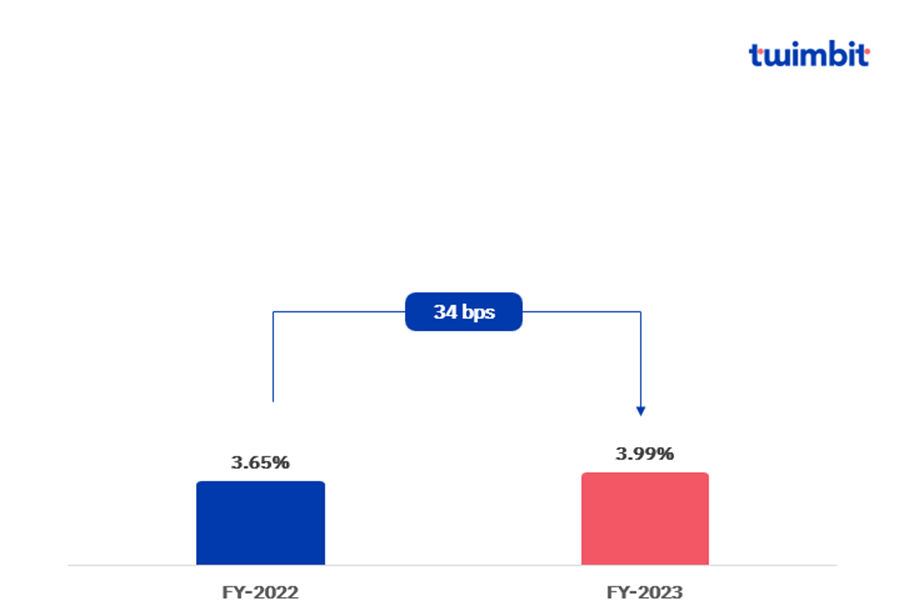

Net interest margin (NIM)

Average NIM increased by 34 basis points in FY-23

The average NIM increased from 3.65% in FY-2022 to 3.99% in FY-2023 (Exhibit 4)

Exhibit 4: Average net interest margin of the top 8 Indian banks

This measurable change in the average NIM reflects the banks’ ability to manage interest income relative to funding costs, improving its impact on overall financial performance.

Kotak Mahindra Bank

Kotak Mahindra Bank reported the highest increase by 70bps in its NIM, from 4.70% in FY-2022 to 5.40% in FY-2023.

- The yield on interest-earning assets increased from 7.43% for FY-2022 to 8.49% for FY-2023 due to a 22% increase in the yields of advances and investments.

- Cost of funds increased from 3.23% in FY-2022 to 3.71% in FY-2023 due to a change in the liability mix and an increase in the interest rates of term deposits, certificate of deposits and borrowings.

All the banks reported an increase in its NIM in FY-23. This increase is due to favourable economic and operational factors. A robust GDP growth rate of 7.2%, driven by strong domestic private consumption and increased public investment by loan demand and economic activity. A substantial rise in deposits has expanded banks funding base at potentially stable or lower costs. Furthermore, higher yields on loans and investments have bolstered Net Interest Income (NII).

Non-performing loans (NPL)

Average NPL of the top 8 Indian banks improved by 55 basis points in FY-23

The average NPL improved from 3.54% in FY-2022 to 2.99% in FY-2023 (Exhibit 5).

Exhibit 5: Average NPL of the top 8 Indian banks

Source: Bank Financials, Twimbit analysis

Of the 8 Indian banks, 7 experienced a decrease in their NPL which is a positive development for the banks as it shows the enhanced financial performance.

- Bank of Baroda – Bank of Baroda showed a significant improvement in its NPL by decreasing from 6.61% to 3.79%, marking a reduction of 282 bps

- Canara Bank – Canara Bank showed an unfavourable increase in its NPL from 5.35% to 7.51%, marking an increase of 216 bps.

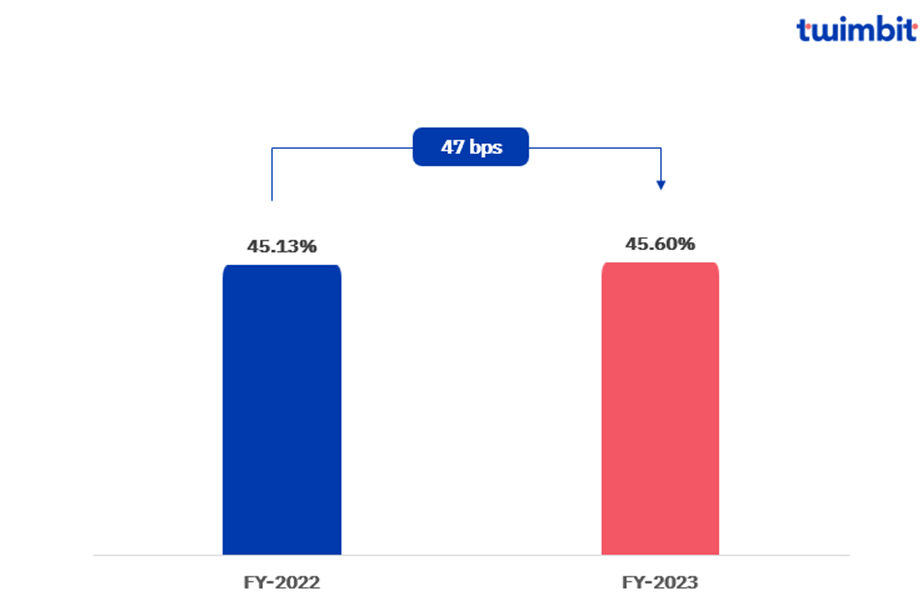

Cost efficiency (CE)

CE for the top 7 Indian Banks increased by 47 basis points in FY-23

Cost efficiency stood at 45.60 % in FY-2023, up from 45.13% in FY-2022 (Exhibit 6). This indicates operational inefficiencies among these banks.

Exhibit 6: Average cost efficiency ratio of the top 7 Indian banks

Source: Bank Financials, Twimbit analysis

Most banks have reported cost-efficiency ratios below the industry average of 50% with ICICI Bank leading at 40.11%. However, HDFC Bank reported an increase of 350 bps from 36.9% to 40.4%, indicating operational inefficiencies. Conversely, the cost efficiency of the Bank of Baroda decreased by 152bps from 49.24% in FY-2022 to 47.72% in FY-2023, indicating improvements in the bank’s operational efficiency.

Of the 7 banks, the State Bank of India (SBI) reported the highest cost-efficiency ratio at 53.87% in FY-23 from 53.31% in fiscal year 2022. This increase was driven by higher provisions associated with wage hike negotiations.

Key initiatives by Indian Banks

ICICI Bank

Several key initiatives envelop ICICI Bank as it aims to expand its rural footprint and increase its reach through a wide range of digital and financial solutions.

- Increased focus towards micro-finance institutions, self-help groups, cooperatives, and SMEs involved in agricultural activities.

This focus has increased the bank’s portfolio by 13.8% YoY to USD 874.31 billion as of March 31, 2023. Of the 5,900 business centres and 4,299 ATMs and cash recycler machines, 51% are now located in rural and semi-urban areas. This includes 561 centres established in previously unbanked villages. As a result, ICICI Bank can provide comprehensive financial services and last-mile access in remote and underserved regions across India.

- The introduction of iLens, an end-to-end digital lending platform.

iLens enables the bank to provide a wide range of digital solutions like instant transanctions, digital disbursements (e-sign and e-stamp) and digital KYC verifications for existing and new customers.

HDFC Bank

The integration of AI and ML models have enhanced the bank’s customer engagement, strengthened risk assessment and advanced its fraud detection systems.

- The AI and ML models have been in implemented in the Vyapar application by HDFC Bank and its risk assessment system.

By identifying risks and developing appropriate strategies, HDFC Bank ensures a robust risk management. This implementation also enhances the efficiency in various functions like estimating and quoting, cost sharing with customers, and seamless conversion of estimates into bills. The system also provides order tracking, invoicing with customizable themes, efficient expense management, and comprehensive tracking of payables and receivables.

- AI and ML techniques enable the identification and prevention of fraudulent activities.

The future development of Faceless Authentication by HDFC Bank aims to enhance its fraud detection system and provide better measures in safeguarding customer transactions.

Kotak Mahindra Bank

The launch of its new portal “Kotak fyn” and credit card signify the latest initiatives from Kotak Mahindra Bank

- Collaborated with Metro to launch a new credit card that aims to expand the bank’s product range.

The card provides interest free credit up to 48 days to over 3 million Indian metro users. The bank also incentivises new users with its tagline of “First Day, First Month”. Here, credit card holders can earn a cashback of Rs 500 upon spending Rs 10,000 in a single day within the first 30 days of the card issuance.

- The new portal “Kotak fyn” is personalised for business banking and corporate clients.

From offering improved client usability to an integrated digital platform for seamless banking, the second phase of the platform received major updates. These included EDPMS / IDPMS settlements and system efficiency upgrades. Furthermore, “Kotak fyn” is now equipped with an arsenal of industry-first features, such as:

- Trade Services

- Account Services

- Collection Services and Payments

- Accessibility for all customers

Cumulatively, these features helped deliver improved speeds during the facilitation of collections and liquidity transactions.

Outlook for 2024

In 2024, the Indian banking sector anticipates growth which is supported by stable interest rates, strong GDP, and lower inflation. Increased lending and deposit activities are expected, driven by ongoing investments in technology and infrastructure. However, challenges include global economic volatility, potential interest rate hikes, and heightened competition from FinTech firms. Despite challenges, the banks are well-positioned with robust asset quality and profitability, emphasizing on adaptability and customer-centric strategies for sustainable growth.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements.

- Twimbit follows the fisical year approach for the analysis in this report (Q1=April-June Q4=January-March)

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for the top 8 Indian banks.

- The 3 public sector banks in the report are SBI, Bank of Baroda and Canara Bank. The 5 private sector banks are HDFC Bank, ICICI Bank, IndusInd Bank, Kotak Mahindra Bank and Axis Bank.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.