Key takeaways

- Average YoY (Year-on-Year) revenue growth slowed from 3.2% in Q2-2023 to 1.9% in Q2-2024.

- Aggregate revenue increased by USD 6.2 billion to USD 322.5 billion in Q2-2024, with only a single telco (Reliance Jio) exhibiting double-digit growth.

- Cost-containment measures and operational streamlining efforts resulted in positive EBITDA change for ~79% of the analysed telcos.

- Nearly 55% of the telcos analysed reported minimal EBITDA variation, within a manageable range (-3% to +3%).

- Telcos maintained EBITDA margin stability of 37% due to cost-containment measures, operational efficiency initiatives, and continued incremental top-line growth.

- Bharti Airtel and Reliance continue to exhibit robust and stable EBITDA margins (around 50%), indicating resilience amidst global pressures.

- The maturation of 4G and 5G networks in major markets led to a CAPEX decline for around ~73% of the 22 analysed telcos in Q2-2024.

- CAPEX spending across select major geographies like USA, India, China continue to stabilise, owing to lower CAPEX spend by leading telcos.

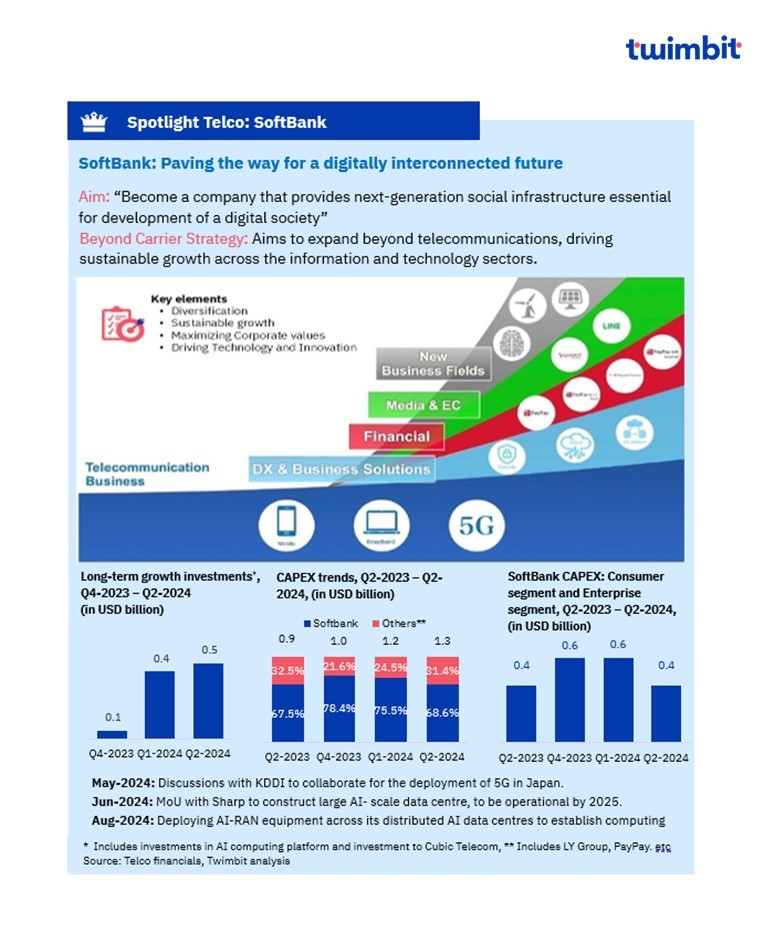

- CAPEX spending by SoftBank surged as the telco continues to focus on strategic spend to build digital infrastructure within the country.

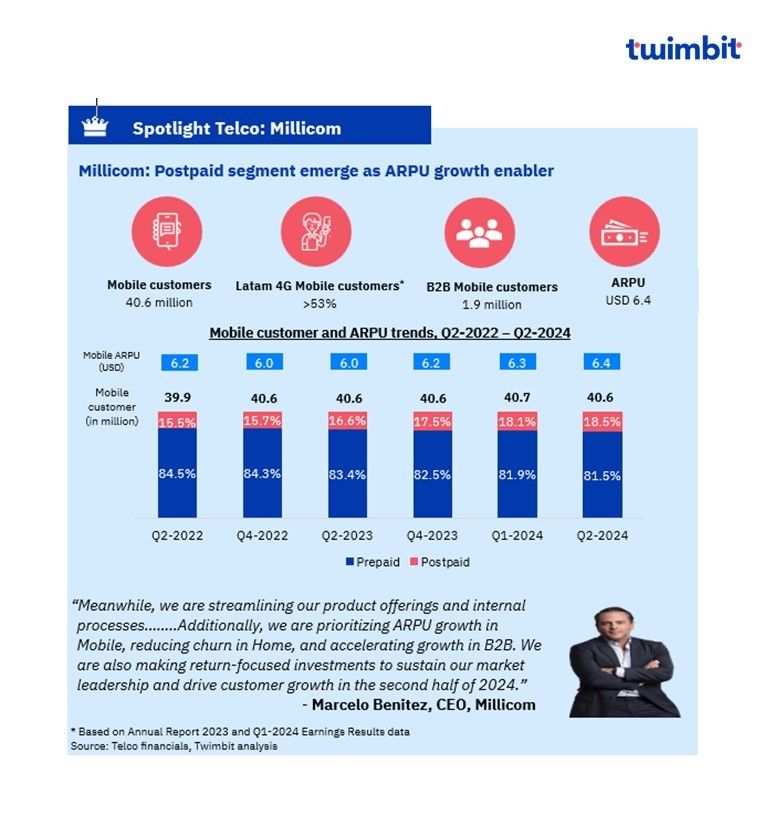

- Average ARPU growth remained virtually stagnant (0.6% YoY growth), reaching USD 23.7 in Q2-2024, impacted by growth in Millicom, Verizon and AT&T.

- ARPU for Indian telcos increased due to a growing mix of data (4G/5G) subscribers and strategic ARPU upliftment initiatives adopted by the telcos.

Revenue analysis of Global telcos: Q2-2024

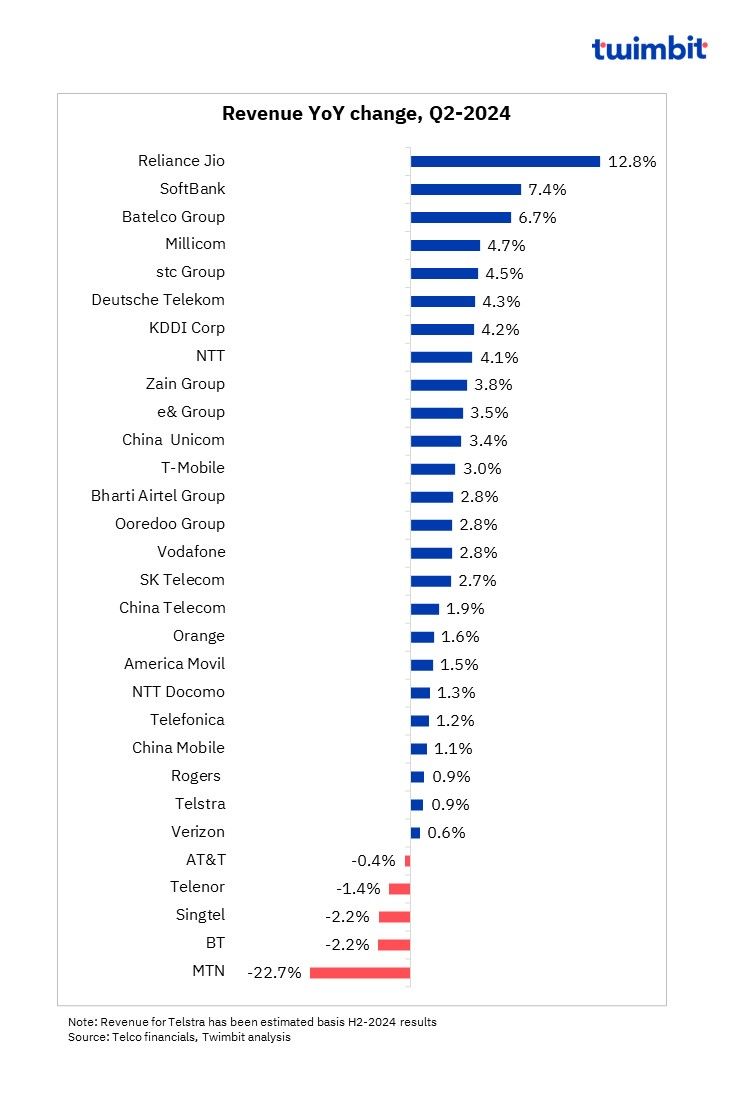

Average revenue growth for leading global telcos slowed from ~3.2% in Q2-2023 to ~1.9% in Q2-2024

Approximately 83% of telcos achieved YoY revenue growth in Q2-2024 (as compared to 70% in Q2-2023). The combined revenue of the 30 analysed telcos increased by ~USD 6.2 billion to ~USD 322.5 billion in Q2-2024, with only a single telco (Reliance Jio) exhibiting double-digit growth.

Exhibit 1: Revenue trends (% change) for Global telcos (YoY basis), Q2-2024

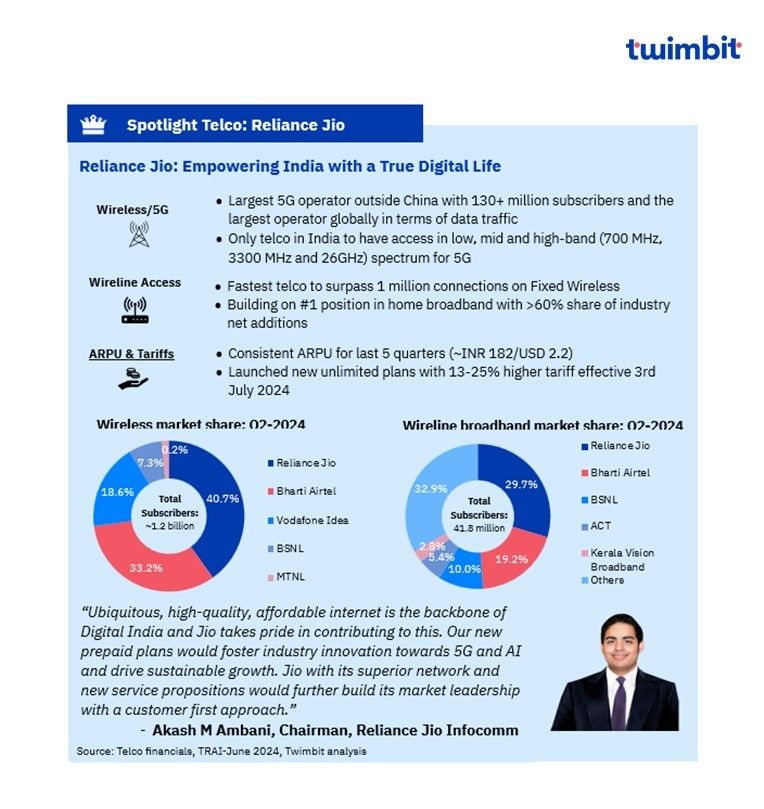

Reliance Jio

Reliance Jio’s revenue surged by 12.8% YoY to USD 3.5 billion (INR 294.5 billion) in Q2-204, primarily driven by robust subscriber growth across its Mobility and Home broadband segments.

- The telco’s mobile subscriber base expanded by 9.2% YoY to 489.7 million during the quarter, fuelled by 8 million net additions.

- ARPU was USD 2.2 (INR 181.7), reflecting a favourable subscriber mix. However, the ARPU was partially offset by an increasing mix of promotional 5G traffic offered on an unlimited basis to subscribers.

- Jio’s 5G subscriber base reached ~130 million in Q2-2024, up from 108 million in the previous quarter.

- Total data and voice traffic increased by 32.8% and 6.6% YoY to 44.1 billion GB and 1.42 trillion minutes, respectively, with 5G accounting for approximately 31% of the wireless data traffic.

- Reliance Jio’s home broadband service, JioAirFiber, continued to witness strong demand, adding 1.1 million home connections in Q2-2024, accounting for over 60% of the industry’s net additions.

SoftBank

SoftBank’s revenue increased by 7.4% YoY to USD 9.9 billion (JPY 1.5 trillion), primarily driven by growth in the Enterprise business segment alongwith incremental contribution from its other operating segments as well.

- During Q2-2024, SoftBank’s Enterprise business revenue increased by 10.5% YoY to USD 1.4 billion (JPY 215.6 billion), led by growth in all its reporting subsegments, including Mobile, fixed line, and Business solutions.

- Mobile segment revenue increased ~1.4% YoY to USD 491.5 million (JPY 76.6 billion), driven by increase in mobile device sales and telecommunications revenue.

- Fixed-line segment reported revenue decline of ~2.4% YoY to USD 273.4 million (JPY 42.6 billion), due to decrease in the number of subscribers to telephone services.

- Business solution segment revenue increased 26.9% YoY to USD 618.5 million (JPY 96.4 billion), on account of the business of WeWork Japan GK through subsidiary WWJ Corp, in addition to incremental revenue from cloud services, IoT solutions and security solutions by catering to enterprise customers’ demand for digitalization.

- The Consumer segment accounted for the largest share of overall revenue (~44.4% in Q2-2024) and reported growth of ~2% YoY to USD 4.4 billion (JPY 681.7 billion), primarily driven by growth in the mobile segment.

- Mobile service revenue grew by approximately 2% YoY to 2024 to USD 2.5 billion (JPY 392.3 billion), reflecting the growth in smartphone subscribers, led by the Y! mobile brand.

- The cumulative smartphone subscriber count reached 30.9 million in Q2-2024, compared to 29.6 million in the previous quarter.

- ARPU levels reported a slight increase due to contributions from new price plans introduced in October 2023.

- Broadband revenue increased by 1% YoY to ~USD 650 million ((JPY 101.3 billion), driven by growth in subscribers of the SoftBank Hikari fibre-optic service.

- Mobile service revenue grew by approximately 2% YoY to 2024 to USD 2.5 billion (JPY 392.3 billion), reflecting the growth in smartphone subscribers, led by the Y! mobile brand.

Batelco Group

Batelco Group’s overall revenue increased by 6.7% YoY in Q2-2024 to USD 298.4 million (BHD 112.5 million), driven by growth across all operating segments, products, and services.

- Revenue grew across Bahrain, Jordan, Maldives, and the Sure Group.

- Bahrain, the largest segment, reported revenue growth of 8.6% YoY to USD 148.3 (BHD 55.9 million).

- Mobile telecommunication services accounted for largest share of revenue amongst all the service offerings, growing by 4.1% YoY to USD 137.7 million (BHD 51.9 million).

- Data communications circuit revenue increased by 7% YoY to USD 46.4 million (BHD 17.5 million).

- Fixed broadband revenue declined by 3.4% YoY to USD 49.7 million (BHD 18.7 million).

- Fixed-line telecommunication services revenue fell by approximately 7% YoY to USD 11.2 million (BHD 4.2 million).

- Wholesale services revenue increased by 12.2% YoY to USD 24.9 million (BHD 9.4 million).

- Equipment revenue and revenue from the provision of services increased by 30.6% and 4.7% YoY respectively, to reach USD 28.3 million (BHD 10.7 million) and USD 270.1 million (BHD 101.8 million).

Millicom

Millicom’s revenue rose by 4.7% YoY in Q2-2024 to USD 1.5 billion, driven by growth across operating regions except Bolivia.

Service revenue grew by 5.5% YoY to USD 1.4 billion, driven by growth in mobile and fixed services.

- Mobile service revenue increased by 7.3% YoY to USD 792 million, driven by growth in ARPU.

- Fixed and other services revenue grew by 2% YoY to USD 548 million, despite a decline in the Home segment.

- Home segment service revenue declined by 3.6% YoY to USD 376 million, owing to decline in customers (~6% YoY) which offset the marginal increase in ARPU (5.2% YoY).

stc Group

stc’s revenue increased by 4.5% YoY to USD 5.1 billion (SAR 19.1 billion), mainly attributed to increased revenue from stc KSA and its subsidiaries.

- stc KSA revenue increased by 0.11%, driven by an increase of ~5.3% in commercial unit revenues.

- Additionally, stc’s subsidiaries reported revenue growth of ~13.9% YoY during the period

MTN

MTN Group’s service revenue declined by 22.7% YoY in Q2-2024 to USD 2.3 billion (ZAR 42.4 billion) in Q2-2024, primarily due to a major decline in revenue from Nigeria.

- Nigeria’s revenue declined by 52.8% YoY to USD 552.5 million (ZAR 10.3 billion), driven by rising inflation and the continued depreciation of the naira against the US dollar.

- Revenue from the Middle East and North Africa (MENA) region plummeted from USD 116.3 million (ZAR 2.2 billion) in Q2-2023 to USD 4.1 million (ZAR 75 million) in Q2-2024, impacted by revenue declines in Ghana and Afghanistan.

- South Africa’s revenue increased by 5.8% YoY to USD 576.3 million (ZAR 10.7 billion), driven by an increase in subscriber count to 38.1 million in June 2024.

- Postpaid subscriber count increased by 9.4% to 9.4 million in H1-2024, driven by stronger uptake of integrated voice and data plans as well as home propositions.

- Prepaid customers increased by 3.3% to 29.0 million in H1-2024.

- Revenue from the Southern and East Africa (SEA) region grew by 14.3% YoY in Q2-2024 to USD 325.7 million (ZAR 6.1 billion), supported by sustained growth in Rwanda.

- Revenue from the West and Central Africa (WECA) region increased by 13.8% YoY to USD 776.7 million (ZAR 14.4 billion), driven by growth in Cameroon and Ghana.

During H1-2024, the overall revenue was also impacted by a decline in data and voice revenue by 17.2% and 33.7% YoY, respectively, offsetting the 7.3% YoY growth in Fintech revenue.

BT

BT’s revenue declined by 2.2% YoY in Q2-2024 to USD 6.4 billion (GBP 5 billion), attributed to declines in the Consumer and Business segments, which offset growth in the OpenReach segment.

- Consumer segment revenue declined by ~ 1% YoY to USD 3 billion (GBP 2.4 billion), driven by intense competition.

- Business segment revenue declined by 4.6% YoY to USD 2.4 billion (GBP 1.9 billion), due to a decline in legacy managed contracts, reduced low-margin sales activity, and portfolio contraction.

- OpenReach segment revenue increased by 2.1% YoY to USD 2 billion (GBP 1.6 billion), driven by broadband price increases and FTTP and Ethernet base growth.

Singtel

Singtel Group’s revenue declined by 4.2% YoY in Q2-2024 to USD 2.5 billion (SGD 3.4 billion), driven by decline in Optus and Singtel Singapore, which offset growth from NCS and Digital InfraCo.

- Optus revenue declined by 3.5% YoY to USD 1.3 billion (SGD 1.7 billion), driven by growth in mobile revenue and Home segment revenue.

- Overall mobile revenue increased 3.9% YoY in Q2-2024 to ~USD 1 billion (SGD 1.3 billion), driven by 4.7% increase in mobile service revenue.

- Growth on mobile service revenue was on account of 0.7% increase in mobile customers coupled with 3.7% growth in Blended ARPU which reached 10.5 million and USD 21.1 (AUD 32) in Jun-2024.

- Singtel Singapore reported a revenue decline of 0.5% YoY to USD 689.5 million (SGD 933 million), driven by growth in mobile service revenue, which offset declines in Fixed voice, fixed broadband, and PayTV revenue.

- Mobile service revenue increased due to a 6.2% YoY increase in subscribers, which reached 4.6 million in Jun-2024.

- Fixed voice, fixed broadband, and PayTV revenue declined by 8.5%, 1.3%, and 0.6% YoY, respectively in Q2-2024.

- NCS revenue increased by 3.8% YoY to USD 522.4 million (SGD 707 million).

- Digital InfraCo’s revenue increased by 5.8% YoY to USD 80.5 million (SGD 109 million).

Telenor

Telenor’s revenue declined by 1.4% YoY to USD 1.8 billion (NOK 20 billion) in Q2-2024, driven by declines in the Nordic region, Infrastructure segments, and the Amp segment, which offset marginal revenue growth from the Asia region.

- Nordic region revenue declined marginally by approximately 1% YoY to USD 1.3 billion (NOK 13.9 billion), impacted by declines in Norway and Denmark, offsetting growth from Finland.

- Asia revenue grew by 1.2% YoY to USD 48.2 million (NOK 5.2 billion), driven by growth in Telenor Pakistan, which subdued the decline in revenue from Grameenphone Bangladesh.

- Infrastructure and Amp segment revenue declined by 3.3% and ~34% YoY, respectively to USD 76.2 million (NOK 819 million) and USD 75.3 million (NOK 809 million).

AT&T

AT&T’s revenue declined by 0.4% YoY to USD 29.8 billion, due to decline in Business Wireline service and Mobility equipment, which were mostly offset by higher Mobility service, Consumer Wireline, and Mexico revenues.

- Mobility revenue grew by 0.8% YoY to USD 20.5 billion, driven by higher growth in service revenue, which offset a decline in equipment revenue.

- Service revenue increased by 3.4% YoY to USD 16.3 billion, driven by increase in total subscriber count and postpaid ARPU.

- Equipment revenue declined by 8% YoY to USD 4.2 billion due to lower sales volumes.

- Consumer Wireline revenue increased by approximately 3% YoY to USD 3.3 billion, driven by broadband revenue (mainly attributed to fibre), which grew by 7% to USD 2.7 billion.

- Latin America (Mexico) segment revenue grew by 14.1% YoY to USD 1.1 billion, driven by higher equipment sales, subscriber growth, and favourable foreign exchange rates.

- Business Wireline revenue declined by 9.9% YoY to USD 4.8 billion, primarily impacted by lower demand for legacy voice and data services and product simplification.

EBITDA analysis of Global telcos: Q2-2024

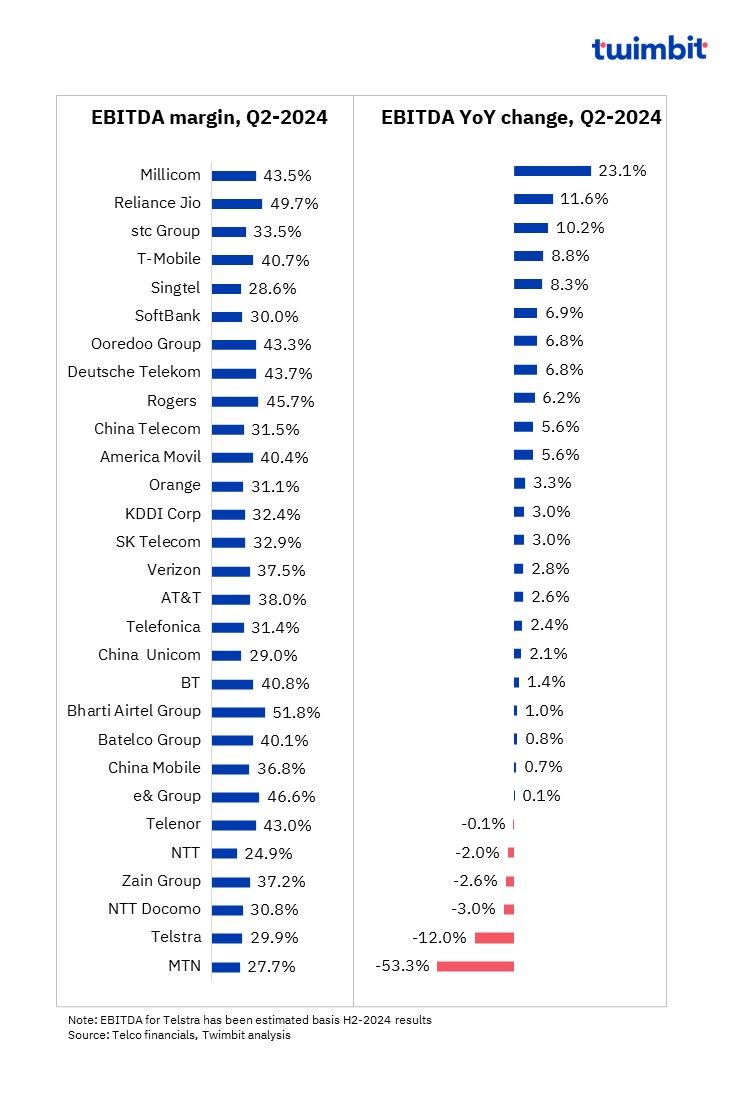

Average EBITDA margin for the leading global telcos stabilised at 37% in Q2-2024

Cost control measures, operational efficiency initiatives, and sustained top-line growth have stabilized EBITDA for ~79% of the analysed telcos. Nearly ~55 % of telcos reported a slight EBITDA variation, within a manageable range (-3% to +3%).

Exhibit 2: EBITDA and EBITDA margin trends for Global telcos, Q2-2024

Millicom

Millicom’s EBITDA surged by 23.1% YoY (organic growth of 19.7%) to USD 634 million, driven by growth across all countries.

- Colombia experienced the highest EBITDA growth, increasing by 54.6% YoY to USD 141 million, on account of cost savings, higher ARPUs and lower sales and marketing spend in its Home business.

- Guatemala accounted for the highest overall EBITDA at USD 217 million in Q2-2024, with a growth of 9.1% YoY, owing to growth in service revenue and impact of cost savings.

The EBITDA margin increased from 37% in Q2-2023 to 43.5% in Q2-2024.

Reliance Jio

Reliance Jio’s EBITDA grew by 11.6% YoY to USD 1.7 billion (INR 146.4 billion), driven by robust revenue growth and efficient utilization of operating capacities.

The EBITDA margin remained relatively stable at 49.7% in Q2-2024, as compared to 50.2% in Q2-2023.

stc

stc’s EBITDA grew by 10.2% YoY in Q2-2024 to USD 1.7 billion (SAR 6.4 billion), driven by positive impacts resulting from the cost efficiency program.

- Selling and Marketing expenses declined by 3.2% YoY to USD 404.5 million (SAR 1.5 billion).

The EBITDA margin increased by 170 basis points (bps) to 33.5% in Q2-2024.

T-Mobile

T-Mobile’s EBITDA increased by 8.8% YoY in Q2-2024 to USD 8.1 billion, driven by higher total service revenue and lower cost of services.

- An increase in operating income (growth of 15.8% YoY) positively impacted EBITDA growth.

The EBITDA margin increased by 220 bps to 40.7% in Q2-2024.

Singtel

Singtel’s EBITDA increased by 8.3% YoY in Q2-2024 to USD 722 million (SGD 977 million), driven primarily by growth in Optus and NCS.

- Optus’s EBITDA increased by 4.2% YoY to USD 351 million (SGD 475 million), driven by improved mobile performance coupled with effective cost management.

- NCS’s EBITDA increased by 12.6% YoY to USD 62.1 million (SGD 84 million), on account of higher operating revenue and continued cost optimisation efforts.

- Singtel Singapore’s EBITDA increased by 3.5% YoY to USD 284.1 million (SGD 385 million), owing to increase in operating income. Decline in operating expenses, owing to reduction in direct cost of sales and total manpower cost from lower average headcount, facilitated operating income growth.

The EBITDA margin increased from 25.9% in Q2-2023 to 28.6% in Q2-2024.

MTN

MTN’s EBITDA decreased by 53.3% YoY in Q2-2024, to USD 633.1 million (ZAR 11.7 billion) in Q2-2024.

- EBITDA from South Africa increased by 9.5% YoY to USD 272.5 million (ZAR 5.1 billion).

- EBITDA from Nigeria declined by 71.7% YoY to USD 0.2 million (ZAR 3.287 billion), impacted by various factors including naira devaluation, VAT introduction, higher CPI adjustments, and higher energy costs.

- Operational inefficiencies exacerbated by the Sudan conflict also contributed to the decline.

These factors led to a decline in the EBITDA margin from 45.8% in Q2-2023 to 27.7% in Q2-2024.

Telstra

Telstra’s EBITDA declined by 12% YoY in Q2-2024 to USD 1.2 billion (AUD 1.8 billion).

- EBITDA growth in certain segments (Mobile, Fixed – C&SB, International and Infrastructure) was offset by a decline in Fixed – Enterprise.

- Decline in Fixed – Enterprise EBITDA was driven by lower revenue and increased costs in Network Applications and Services (NAS) and Data and Connectivity (DAC) segments.

- NAS EBITDA declined due to lower revenue from calling applications and professional services revenue, coupled with increased costs.

- DAC EBITDA declined due to reduction in revenue and increased costs.

The EBITDA margin declined from 34.3% in Q2-2023 to 29.9% in Q2-2024.

NTT Docomo

NTT Docomo’s EBITDA decreased by 3% YoY to USD 2.9 billion (JPY 455 billion), impacted by a decline in the Consumer segment EBITDA.

- Consumer segment EBITDA declined by 3.9% YoY in Q2-2024 to USD 2.2 billion (JPY 347.9 billion), due to decline in Consumer communications EBITDA.

- Enterprise segment EBITDA remained stable at USD 687.2 million (JPY 107.1 billion).

The EBITDA margin declined from 32.2% in Q2-2023 to 30.8% in Q2-2024.

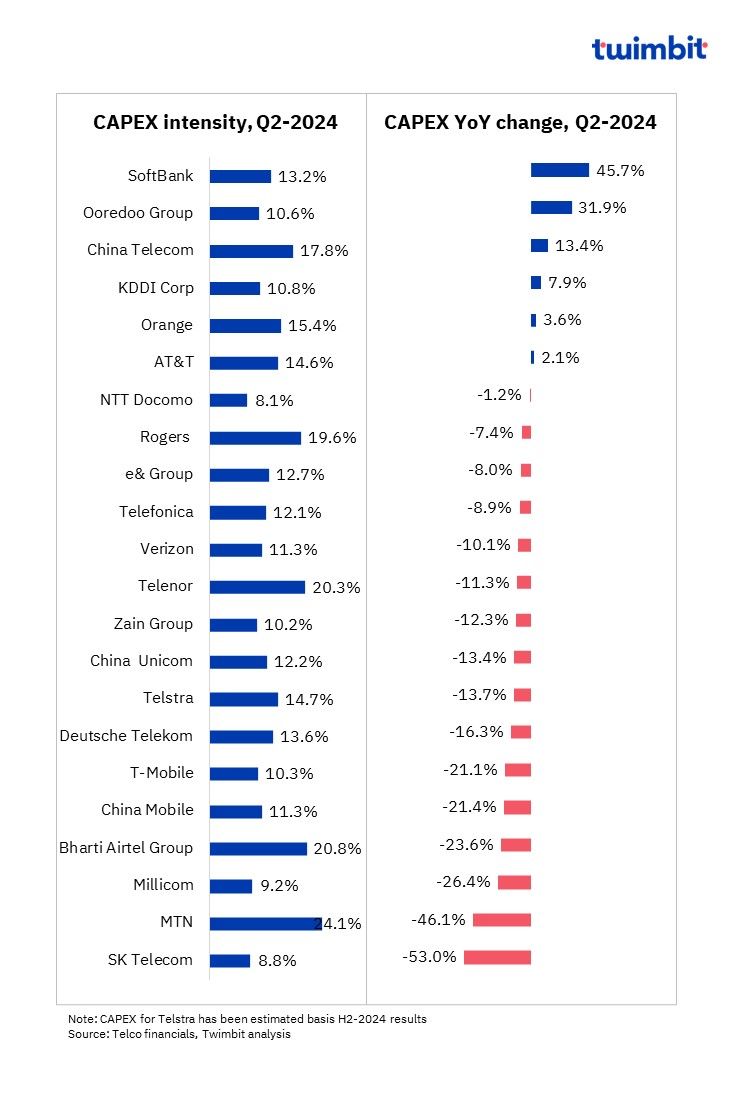

CAPEX analysis of Global telcos: Q2-2024

Average CAPEX intensity declined to 13.7% in Q2-2024 as compared to 15.9% in Q2-2023, as 4G/5G network deployment of leading telcos reaches completion

Nearly 73% of the 22 telcos analysed reported a YoY CAPEX decline in Q2-2024, up from ~64% in Q2-2023. The maturation of 4G/5G network rollouts in major markets like the US, India, China, Europe and select Middle East & Africa geographies is likely to result in CAPEX stabilization or decrease in coming years.

Exhibit 3: CAPEX and CAPEX intensity trends for Global telcos, Q2-2024

SoftBank

SoftBank’s Capital Expenditure (CAPEX) increased by 45.7% YoY to USD 1.3 billion (JPY 203.4 billion) in Q2-2024, driven by increased spending across various segments.

- CAPEX spending for SoftBank and the combined entity of Line, LY Group, and PayPay segments increased by 48.2% and 40.5% YoY, respectively.

Increased CAPEX was primarily due to investments in AI computing platforms and network quality improvements.

This resulted in a CAPEX intensity increase from 9.8% in Q2-2023 to 13.2% in Q2-2024.

Ooredoo Group

Ooredoo Group’s CAPEX increased by 31.9% YoY to USD 172 million (QAR 629 million) in Q2-2024, driven by increased investments in Algeria, Iraq, Qatar, Tunisia, and Kuwait.

- CAPEX spending in Algeria and Iraq increased significantly due to network rollout activities.

- Tunisia’s CAPEX reached USD 34.3 million (QAR 124.8 million) in H1-2024, driven by investments in fibre, submarine cable, and TDD projects.

- Qatar’s CAPEX was USD 29.3 million (QAR 106.8 million) in Q2-2024, due to network investments and security management.

- CAPEX spending in Oman, Palestine, and other geographies also contributed to the overall CAPEX increase.

As a result, CAPEX intensity increased from 8.3% in Q2-2023 to 10.6% in Q2-2024.

China Telecom

China Telecom’s CAPEX increased by 13.4% YoY to USD 3.3 billion (CNY 23.6 billion), driven by a focus on accelerating the transformation and upgrading of digital information infrastructure.

- Mobile network and Industrial Digitalization accounted for 39% and 34%, respectively, of the total CAPEX spending in H1-2024.

Investments in initiatives such as constructing a 400Gbps all-fibre high-speed network, deploying 50G PON, and spending on intelligent computing resulted in higher CAPEX.

This led to a CAPEX intensity increase to 17.8% in Q2-2024, compared to approximately 16% in Q2-2023.

KDDI

KDDI’s CAPEX increased by 7.9% YoY to USD 964 million (JPY 150.2 billion), driven by continued investments in 5G base stations.

- The Sub6 area (3.7GHz/4.0GHz), which enables high-volume and high-speed 5G telecommunications, expanded significantly in the Kanto region and across Japan.

Increased CAPEX resulted in a marginal increase in CAPEX intensity to 10.8% in Q2-2024.

SK Telecom

SK Telecom’s CAPEX declined by 53% YoY to USD 3.3 billion (JPY 4.4 trillion), resulting in a significant decline in CAPEX intensity from 19.2% in Q2-2023 to 8.8% in Q2-2024.

MTN

MTN’s CAPEX declined by 46.1% YoY to USD 550.9 million (ZAR 10.2 billion), primarily reflecting lower spending by MTN Nigeria.

- CAPEX (excluding leases) declined by 25.9% YoY to USD 433.6 million (ZAR 8 billion).

During H1-2024, overall CAPEX declined by 43.1% YoY to USD 1 billion (ZAR 19.2 billion).

This resulted in a decline in CAPEX intensity from 34.5% in Q2-2023 to 24.1% in Q2-2024.

Millicom

Millicom’s CAPEX declined by 26.4% YoY to USD 134 million, reflecting both efficiencies and the optimization of capital investment.

- The decline in CAPEX was also due to different phasing of investment plans compared to 2023.

As a result, CAPEX intensity declined from 13.1% in Q2-2023 to 9.2% in Q2-2024.

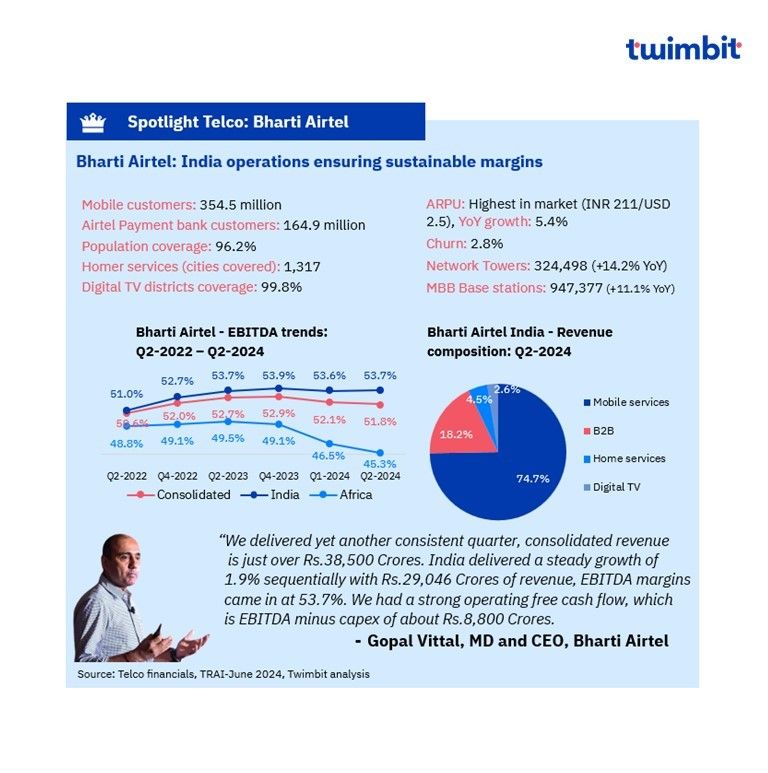

Bharti Airtel Group

Bharti Airtel’s CAPEX declined by 23.6% YoY to USD 960 million (INR 80.1 billion), primarily impacted by reduced CAPEX from India operations.

- CAPEX in India operations declined by 27.3% YoY due to reduced spending in the Mobile services segment.

- CAPEX for Home services, Digital services, and Airtel Business segments increased significantly.

- CAPEX in Africa operations increased by 6.5% YoY, while CAPEX in South Asia operations declined.

CAPEX of Africa operations increased 6.5% YoY in Q2-2024 to USD 146.2 million (INR 12.2 billion), whereas South Asia operation declined from ~USD 1 million (INR 87 million) to USD 0.04 million (INR 4 million).

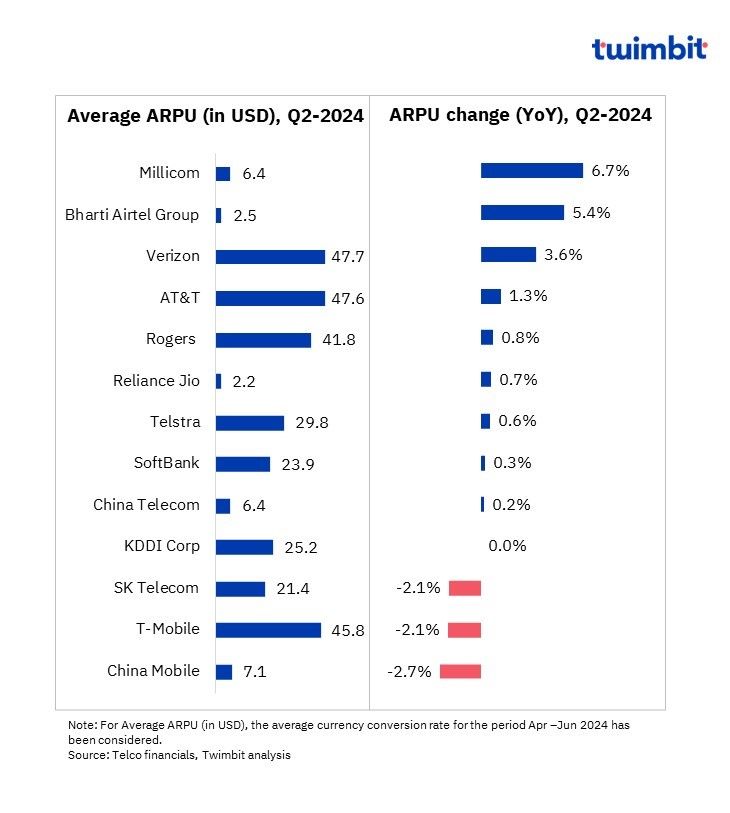

ARPU analysis of Global telcos: Q2-2024

The average ARPU level witnessed a modest growth of 1.8% YoY to USD 29.2 in Q2-2024

The growing data (4G/5G) subscriber mix and strategic ARPU upliftment initiatives have increased ARPU for Indian telcos.

Healthy postpaid subscriber contributions resulted in the ARPU growth for the telcos in the Americas, including Verizon. AT&T and Millicom.

Exhibit 4: ARPU trends for Global telcos, Q2-2024

Millicom

ARPU increased 6.7% YoY to USD 6.4 in Q2-2024, driven by:

- Growth in local currency terms across all operating countries except Bolivia.

- A 11.6% YoY increase in postpaid subscribers to 7.5 million in Q2-2024, despite overall mobile subscriber count remaining almost flat (+0.1% YoY growth).

Bharti Airtel Group

Bharti Airtel Group’s ARPU in India increased by 5.4% YoY to USD 2.5 (INR 210.6) in Q2-2024, primarily led by positive impacts from its India operations.

Mobile ARPU growth in India was driven by a combination of factors including

- Strong 4G/5G customer additions, accounting for 97.1% of data customers in Q2-2024.

- A sustained focus on acquiring quality customers, resulting in an improved customer mix, with its postpaid subscriber reaching 6.7% of total subscribers in Q2-2024 as compared to 6.1% in Q2-2023.

- An increase in average data usage per customer to 23.7GB in Q2-2024 as compared to 21.1GB in Q2-2023.

- Strategic price increases in the range of 10-20% in recent quarters.

Mobile ARPU for Africa operations increased by approximately 7.8% YoY to USD 2.0, primarily led by growth in data ARPU.

Verizon

Verizon’s ARPU increased by 3.6% YoY to USD 47.7 in Q2-2024, primarily driven by improvements in postpaid ARPU and subscriber count.

- Consumer Wireless Postpaid ARPA increased by 5.1% YoY to USD 138.44, offsetting the decline in the prepaid segment, which declined from USD 31.4 in Q2-2023 to USD 30.9 in Q2-2024.

- This growth was driven by recent pricing actions, increased adoption of premium unlimited plans, and greater contribution from Fixed Wireless Access (FWA).

China Mobile

China Mobile’s ARPU declined by 2.7% YoY to USD 7.1 (CNY 51) in Q2-2024, due to factors such as:

- A decline in Minutes of Usage (MOU) by approximately 9% YoY to 225 minutes, as the Handset data traffic DOU remained stagnant at 15.5GB

- A decline in 5G ARPU from USD 11.3 (CNY 81.1) in 1H-2023 to USD 10.7 billion (CNY 76.7) in 1H-2024, in addition to decline in Average Handset Data Traffic per User per Month (DOU) for 5G by 5.4% to 20.7GB.

T-Mobile

T-Mobile’s Blended ARPU declined by 2.1% YoY in Q2-2024 to USD 45.8, primarily due to a decline in prepaid ARPU.

SK Telecom

SK Telecom’s Blended ARPU declined by 2.1% YoY in Q2-2024 to USD 21.4 (KRW 29,298), owing to a relatively higher decline rate in LTE subscribers offsetting the impact of 5G subscribers’ growth.

- During Q2-2024, 5G subscribers grew by 10.6% YoY to 16.3 million, while LTE subscribers declined by 58.4% to 6.6 million.

Key strategic developments: Q2-2024

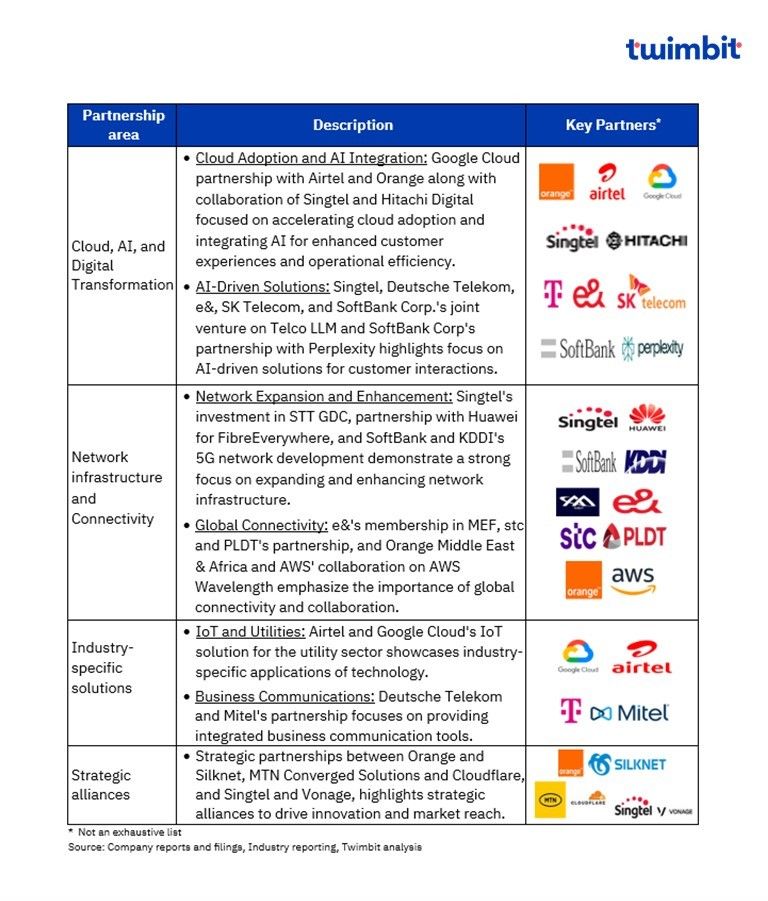

Key strategic partnerships and alliances: Q2-2024

Leading telcos are undergoing a digital transformation characterized by cloud adoption, AI integration, and robust network infrastructure. This shift is driven by the need to enhance customer experiences, optimize operations, and explore new revenue streams through innovative solutions and global connectivity.

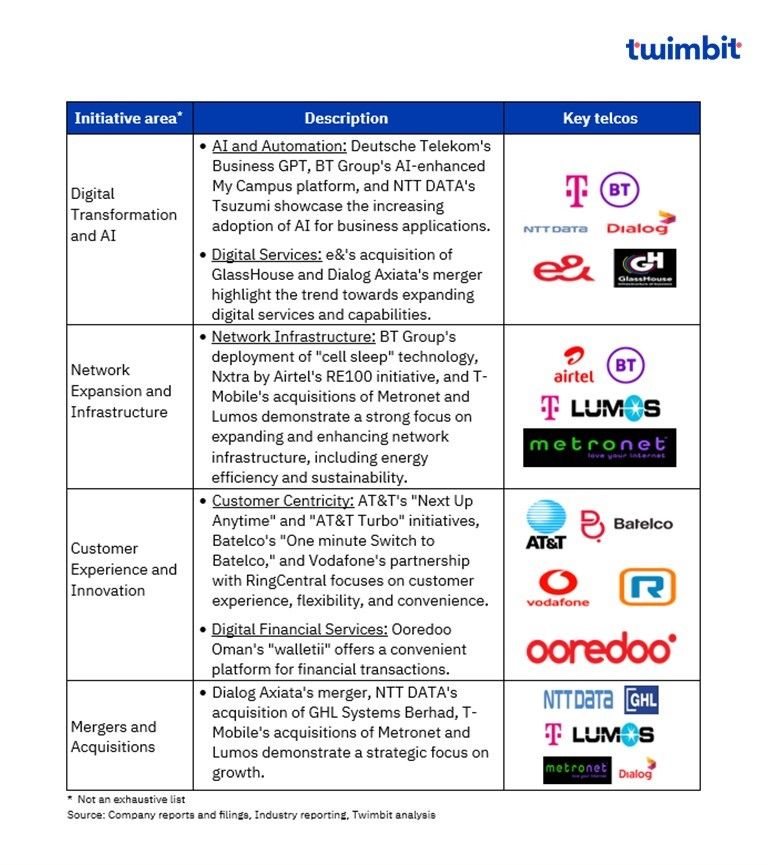

Key strategic initiatives: Q2-2024

The telecommunications industry is undergoing rapid transformation, with leading telcos focussing on customer experience, driven by technology and innovation, coupled with significant investments in network infrastructure. Leading telcos continue to embrace AI, automation, and strategic partnerships to improve efficiency, expand services, and maintain competitiveness in an evolving market.

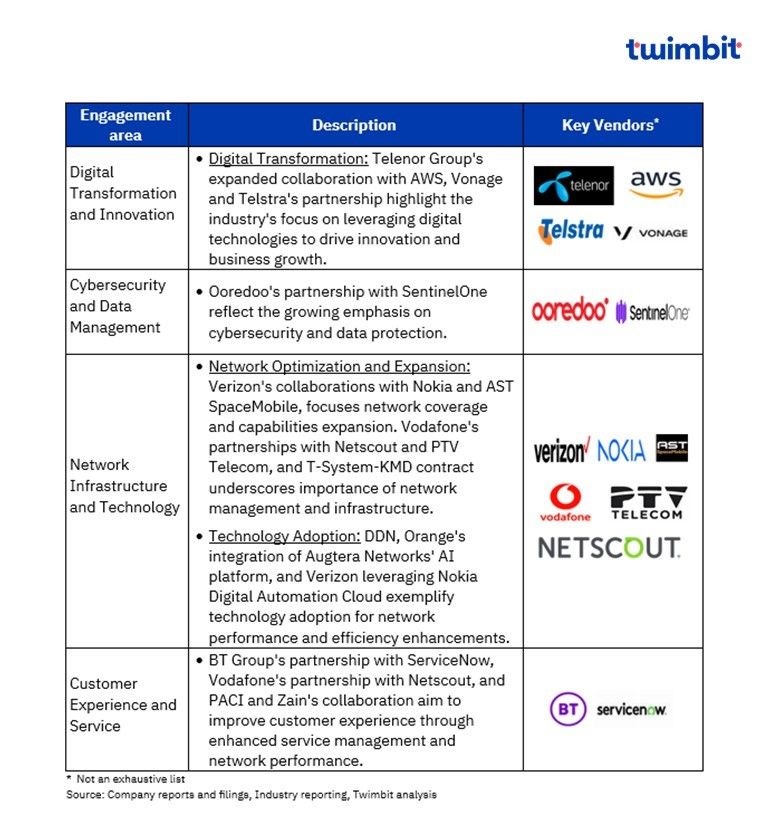

Key contract wins: Q2-2024

Telecommunications providers are strategically investing in network infrastructure, advanced technologies, and strategic partnerships to enhance service delivery, customer experience, and overall business performance. Key focus areas include network expansion, cybersecurity, AI integration, and operational efficiency.

Research Methodology and Assumptions

- The “Global telcos performance benchmarks: Summer 2024” report presents key findings on the performance of 30 strategically selected leading telcos across diverse geographies, offering a comprehensive global perspective on telco performance. Key performance metrics analysed include Revenue, EBITDA, CAPEX, and ARPU for the period April – June 2024.

- This report leverages data acquired from telecommunications companies and includes extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the period from January to December.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate representing the average USD exchange rate for the period April – June 2024 (January-June, wherever applicable for H1-2024) has been applied throughout the report.

- The report presents a comprehensive assessment of Revenue and EBITDA for 30 and 29 telecommunication companies, respectively. Additionally, CAPEX and ARPU analyses encompass data from 22 and 13 telcos, respectively.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- Verizon’s ARPU has been standardized starting from Q2-2024, now representing the average ARPU computed using Consumer wireless service revenue and total wireless retail connections data for each quarter. Previously, Wireless retail postpaid ARPA was used for ARPU calculation

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.