Key takeaways

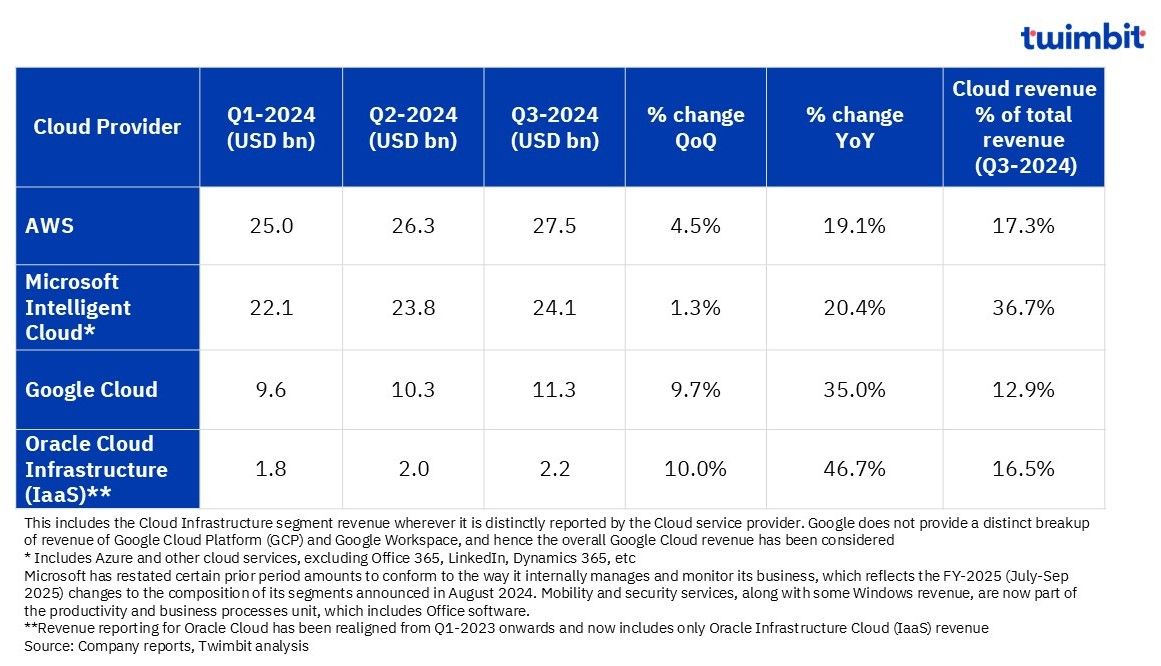

- The global cloud market exhibited robust growth in Q3- 2024, with AWS, Microsoft, Google, and Oracle collectively generating USD 65.1 billion in revenue. This represents a substantial Year-over-Year (YoY) increase of 22.9%, the highest quarterly YoY growth rate in the past seven quarters.

- Cloud revenue now accounts for highest revenue contribution for these companies overall top line averaging around 20% in Q3-2024 – the highest in past eleven quarters.

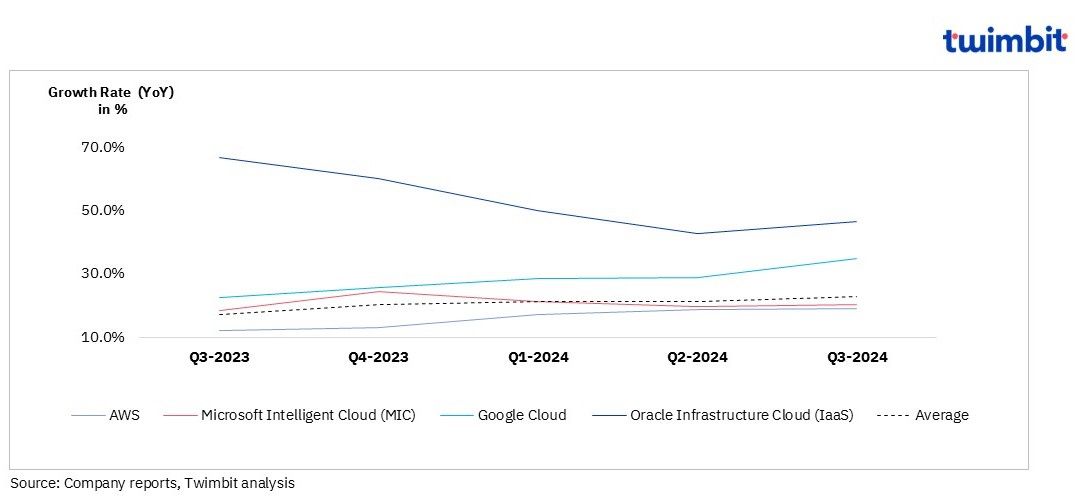

- While AWS continues to expand, its growth rate has moderated relative to Microsoft Intelligent Cloud (MIC), Google Cloud, and Oracle Cloud, which have demonstrated accelerated growth fuelled by AI advancements. It is crucial to note that Microsoft and Google’s revenue figures encompass more than cloud infrastructure services.

- AWS achieved a YoY growth rate of 19.1% in Q3-2024, reaching USD 27.5 billion, driven by growing demand of its AI solutions.

- Microsoft’s Intelligent Cloud segment (MIC) MIC revenue reached a record USD 24.1 billion, growing 20.4% YoY in Q2-2024, led strong demand for consumption-based offerings, including Azure and other cloud services.

- Google Cloud delivered its highest revenue and profitability ever in Q3-2024, with USD 11.3 billion in revenue (35% YoY growth) and ~ USD 1.9 in operating income. Growth was driven by Google Cloud Platform (GCP) followed by Google Workspace.

- Oracle Cloud Infrastructure (OCI) experienced exceptional YoY growth of approximately 46.7%, reaching ~USD 2.2 billion in revenue for Q3-2024. Surge in cloud infrastructure contracts along with AI workloads facilitated this growth.

- During Q3-2024, leading Cloud providers announced of significant Data centre and cloud initiatives, primarily in the Latam and APAC region. Select focus geographies included Brazil, Mexico, Uruguay, Malaysia, Fiji, India and Thailand.

- Leading Cloud providers continue to allocate substantial CAPEX allocation for Cloud, in order to upscale the technical infrastructure required to meeting the growing demand owing to the upsurge in capacity requirements primarily driven by increased AI adoption.

Key trends

Cloud providers boost CAPEX to fuel AI driven growth

AI has emerged as a significant revenue driver for cloud giants like AWS, Microsoft, Google, and Oracle. To capitalize on this opportunity, these cloud providers are substantially increasing their capital expenditure.

This investment is primarily focused on expanding their technical infrastructure, including data centers, servers, and networking equipment etc. For instance, Amazon planed CAPEX of over USD 75 billion+ in FY-2024, with a strong emphasis on AWS and generative AI. In Q3-2024, these cloud providers witnessed a YoY increase in CAPEX ranging from 60% to 81%.

Google Cloud breaks revenue records, Oracle Cloud Infrastructure continues revenue growth momentum

Google Cloud achieved a significant milestone in Q3-2024, surpassing USD 11 billion in revenue. This quarter also marked the highest revenue contribution and profitability for Google Cloud.

Oracle Cloud Infrastructure (OCI) revenue surged by 46.7% to ~USD 2.2 billion in Q3-2024, contributing a substantial 16.5% to the company’s total revenue.

Leading Cloud providers pour billions for global expansion in Latam and APAC

Major cloud providers are aggressively expanding their footprint across emerging markets.

- AWS is leading with bold investments:

- Mexico: USD 5 billion

- Malaysia: Major expansion planned

- Brazil: Significant investment commitment

- Microsoft follows with strategic focus:

- Brazil: USD 2.7 billion

- Mexico: USD 1.3 billion

- Google diversifies across regions:

- Thailand: USD 1 billion

- Uruguay: USD 850 million

- Fiji: USD 250 million (Green Data Centre initiative)

- Oracle targets strategic markets:

- Mexico: New hyperscale cloud region planned

- Thailand: Partnership with AIS for country’s first hyperscale cloud service

- Exhibit 1: Revenue growth rate (YoY) of Cloud service providers, Q3-2024

Exhibit 1: Revenue growth rate (YoY) of Cloud service providers, Q3-2024

Exhibit 2: Revenue trends and growth of Cloud service providers, Q3-2024

Cloud Infrastructure providers

1. Amazon Web Services (AWS)

Overview

- AWS generated USD 27.5 billion in revenue during Q3-2024, representing a 19.1% YoY increase. This growth was primarily fueled by the rising adoption of AWS AI services and the increasing demand for infrastructure modernization solutions.

- While AWS’s YoY revenue growth rate has moderated in recent quarters when compared to the levels of FY-2022, its revenue growth has rebounded in FY-2024. Each quarter of the current fiscal year (FY-2024) has delivered higher YoY growth rates than the corresponding period in FY-2023.

- AWS has achieved an annualized revenue run rate surpassing USD 110 billion, asserting significant reacceleration of growth for the last four quarters.

- AWS’s operating profit soared by approximately 50% YoY to reach ~ USD 10.5 billion in Q3-2024, accounting for 6.6% of total revenue.

- This substantial profit margin expansion was fueled by a combination of factors, including sales growth, rigorous cost control measures, including a measured hiring approach and increased operational efficiency and cost reduction initiatives across the business.

- AWS extended the estimated useful life of its servers in 2024, which contributed ~200 basis points to the YoY margin improvement in Q3-2024

- Amazon announced a significant increase in its capital expenditure (CAPEX) budget for FY-2025, in addition to the estimated allocation of over USD 75 billion+ in FY-2024. A substantial portion of this investment is earmarked for AWS and generative AI initiatives.

- The company remains committed to investing in data centres and high-performance computing equipment, such as NVIDIA GPUs, to support its artificial intelligence products. Furthermore, its investment in custom chips aims to address the burgeoning demand for AI and deliver improved price-performance for customers scaling AI workloads.

AWS global footprint

- AWS Cloud has 108 Availability Zones across 34 geographic regions globally.

- Plans for 18 more Availability Zones and six more AWS Regions in Mexico, New Zealand, the Kingdom of Saudi Arabia, Thailand, Taiwan, and the AWS European Sovereign Cloud.

- AWS Local Zones are available across 34 metropolitan areas globally, with 17 each outside of the US and within the US.

- Amazon CloudFront leverages a global network of 600+ Points of Presence (PoPs) distributed across 100+ cities in 50+ countries. These PoPs are strategically positioned within the AWS network and peer with major ISP networks.

- CloudFront utilizes 600+ embedded PoPs located within ISP networks to minimize latency and optimize delivery to end-users in 200+ cities across North America, Europe, and Asia.

Exhibit 3: AWS Cloud global capabilities

2. Microsoft Intelligent Cloud (MIC)

Overview

- Microsoft reported a 16% YoY revenue increase in Q3-2024, reaching USD 65.6 billion, with AI advancements, particularly within the cloud segment, driving this growth.

- Microsoft’s Intelligent Cloud (MIC) segment, comprising server products and cloud services, continued its strong performance in Q3-2024, contributing 36.7% to total revenue, up from 35.4% in the prior year.

- MIC revenue reached a record USD 24.1 billion in Q1-2024, growing 20.4% YoY, led by strong demand for consumption-based offerings, including Azure and other cloud services.

- Its AI business is estimated to surpass annual revenue run rate of USD 10 billion in Q4-2024.

- Server products and cloud services revenue increased 23% in Q3- 2024, driven by Azure and other cloud services, offsetting the decline in server revenue.

- The robust growth in MIC revenue was primarily driven by the strong demand for consumption-based offerings, particularly Azure and other cloud services, which experienced a 33% YoY growth, fueled by increased demand for a diverse range of offerings, including a 12-point contribution from AI services.

- Server products revenue decreased 1% driven by lower transactional purchasing ahead of the Windows Server 2025 launch, as well as lower purchasing of licenses running in multi-cloud environments.

- Microsoft forecasts stable MIC revenue for Q4-2024, projecting a 31%-32% growth in Azure and other cloud services in constant currency. However, the company acknowledges potential data centre capacity constraints that may impact growth during this period.

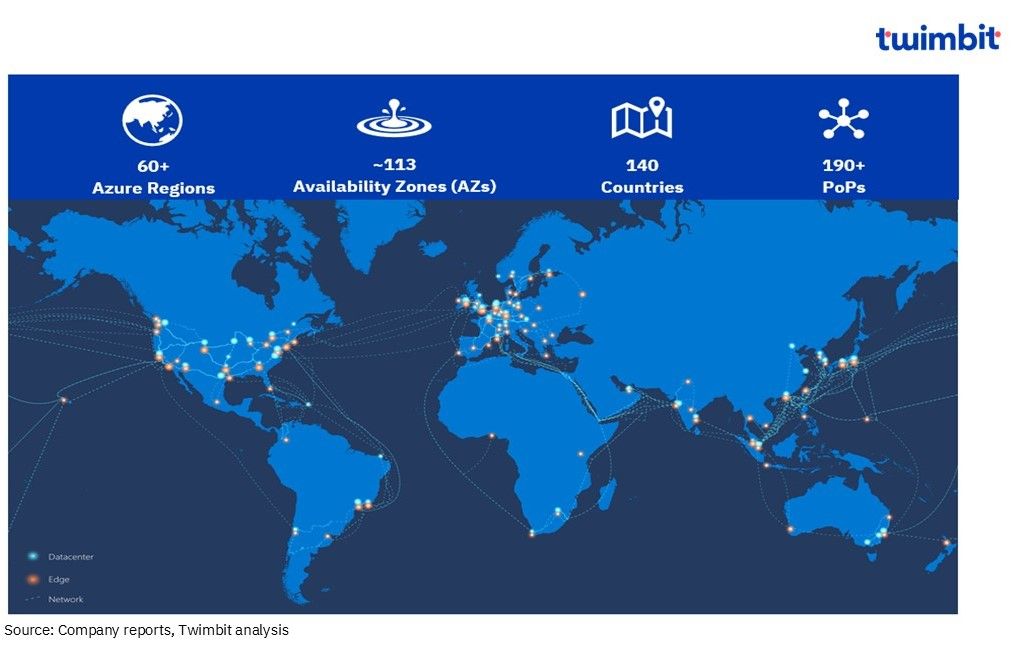

Microsoft Cloud global footprint

MIC has a presence across 60+ regions, and its Azure infrastructure comprises 300+ physical data centres across 30 countries

Exhibit 4: Microsoft Cloud global capabilities

C. Google Cloud

Overview

- In Q3-2024, Google Cloud’s revenue exceeded USD 11 billion (reaching ~USD 11.3 billion, marking a robust YoY growth of nearly 35%. This significant growth was primarily driven by Google Cloud Platform (GCP), followed by Google Workspace. Within GCP, infrastructure and platform services were the key contributors to this impressive performance.

- A substantial driver of Google Cloud’s revenue growth was its robust suite of artificial intelligence offerings, including enterprise subscription services.

- Cloud revenue contribution to overall revenue reached 12.9% in Q3-2024, up from ~11% in Q3-2023. The Cloud revenue contribution now accounts for the highest proportion of revenue over the last 23 quarters (from Q1-2019 onwards).

- Google Cloud reported its highest cloud revenue and profitability in Q3-2024, with an operating income of ~USD 1.9 billion (as compared to USD 266 million in Q3-2023).

- Operating income accounted for ~17.1% of the overall Google Cloud revenue in Q3-2024, as compared to ~3.2% in Q3-2023.

- Leveraging its AI expertise, Google Cloud targets significant growth in cloud services (computing power, software) for businesses. This strategy aims to gain ground on Amazon and Microsoft by attracting fast-growing AI start-ups, including those founded by former Googlers.

Google Cloud global footprint

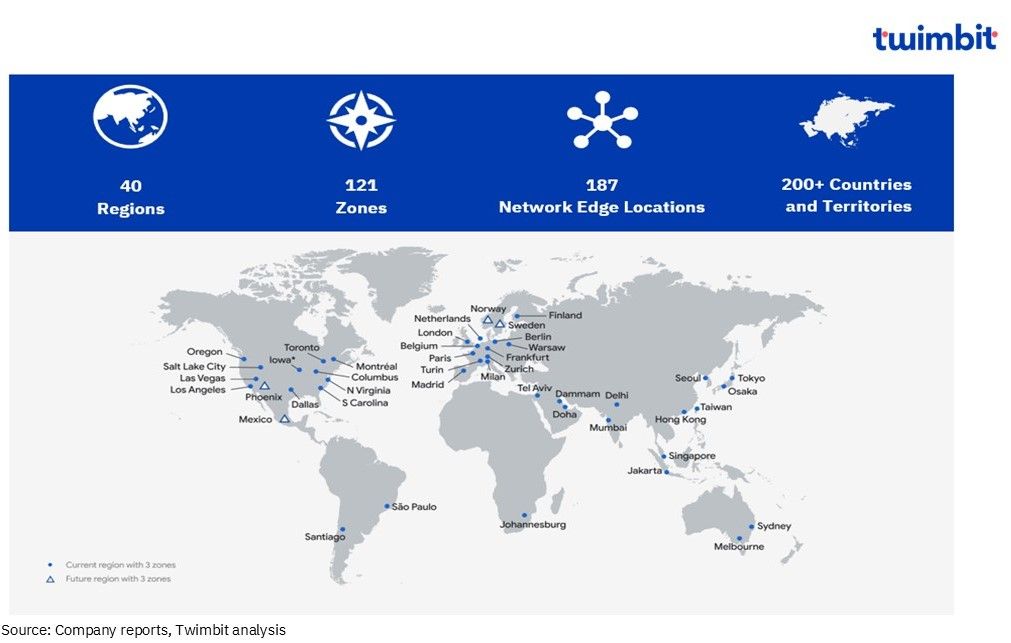

Google currently operates in 40 regions with 121 Zones across 200+ countries.

Plans to operate in new regions, including Austria, Greece, Malaysia, Mexico, New Zealand, Norway, Sweden and Thailand.

Exhibit 5: Google Cloud global capabilities

D. Oracle Cloud

Overview

- Oracle Cloud Infrastructure (OCI-IaaS) offering, experienced remarkable YoY growth in Q3-2024. Revenue surged by approximately 47%, reaching a record-breaking USD 2.2 billion.

- This has positioned OCI as a significant contributor to Oracle’s overall revenue stream, reaching its highest point since 2021 at 16.5% in Q3-2024, a significant increase from 12% in the same quarter of the previous year (Q3-2023).

- During the period, Oracle signed 42 additional cloud GPU contracts totaling USD 3 billion.

- Infrastructure Cloud annualized revenue surged to USD 8.6 billion, with a 56% increase in consumption revenue and persistent high demand.

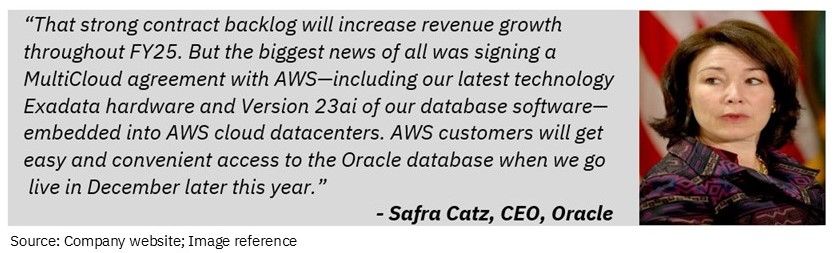

- Forged strategic alliances with AWS, Microsoft Azure, and Google Cloud to offer OCI and other Oracle services on their respective cloud platforms.

- Cloud RPO grew by over 80%, comprising nearly three-quarters of total RPO. Approximately 38% of this RPO is projected to be recognized as revenue within the next year, driven by increasing customer adoption of longer-term contracts due to the demonstrated value of Oracle Cloud services.

- Oracle’s multi-cloud strategy, encompassing Azure, Google Cloud, and soon AWS, along with the flexibility of its cloud regions, offers significant market advantages.

- As of Aug-2024, Oracle has 7 live cloud regions on Microsoft Azure with 24 in development, and 4 live cloud regions on Google Cloud with 14 more in development.

- Oracle continues to reinforce its global expansion strategy with investments in Mexico and Spain and launch of its second cloud regions in Saudi Arabia and Singapore.

Oracle Cloud global footprint

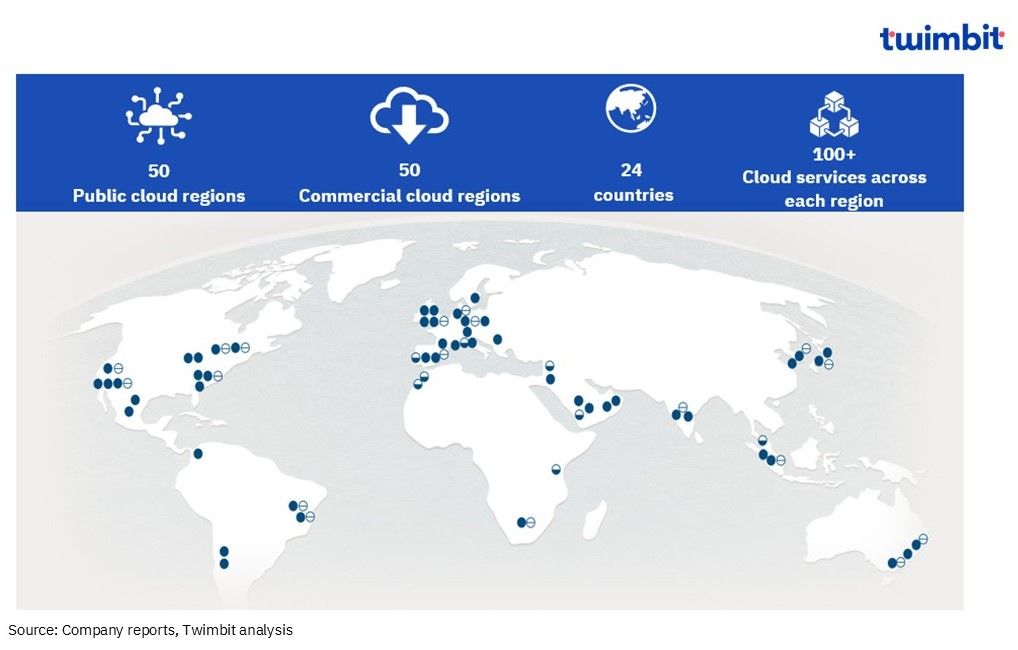

Oracle offers 100+ cloud services across 50 Public cloud regions across 24 countries.

Oracle operates and is constructing a global network of 162 cloud datacentres.

As of Sep-2024, 7 Oracle Cloud regions are live on Microsoft’s Azure platform, with an additional 24 regions under development. Similarly, 4 Oracle Cloud regions are currently live on Google Cloud Platform, and 14 more are in the process of being built.

Exhibit 6: Oracle Cloud global capabilities

Key strategic developments

Key launches and announcements

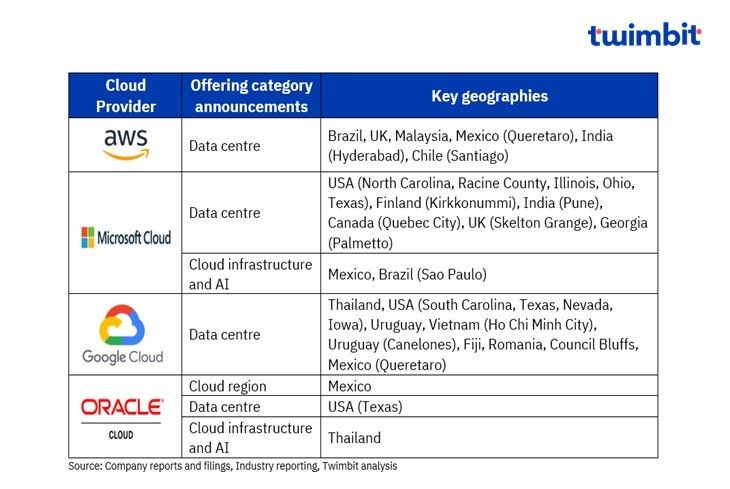

- AWS is significantly investing in its cloud infrastructure, with a focus on key regions like Brazil, the UK, Singapore, Malaysia, Mexico, and India, to expand data centre capacity, enhance cloud services, and support the growing demand for AI and ML capabilities.

- Key data centre investments announced includes ~USD 1.8 billion in Brazil, ~USD 10.5 billion in UK, ~USD 6.2 billion in Malaysia, and ~USD 5 billion in Mexico.

- Microsoft is significantly investing in global cloud and AI infrastructure, to boost its digital transformation capabilities across various regions

- This includes a ~USD 1.3 billion investment in Mexico to boost AI and digital skills and a ~USD 2.7 billion expansion in Brazil

- Google is significantly investing in global cloud infrastructure, with a focus on key regions like Thailand, South Carolina, Uruguay, Vietnam, Mexico and Romania. These investments, totalling billions of dollars, aim to expand data centre capacity, enhance cloud services, and support the growing demand for AI and digital services.

- Key investment announcements include ~USD 1 billion in Thailand, ~USD 5 billion+ across South Carolina, Texas and Iowa (USA), ~USD 850 million in Uruguay, ~USD 200 million in a “green” data centre in Fiji and ~USD 1 -2 billion in Romania.

- Oracle is expanding its global cloud footprint with significant investments in key regions. This includes a new hyperscale cloud region in Mexico, a partnership with AIS for Thailand’s first hyperscale cloud service, and the leasing of a Texas data centre for AI hardware hosting.

Exhibit 7: Key strategic developments

Some of the notable Data centre and Cloud related launches during Q3-2024 include

- Google has opened a new data centre near Fredericia, Denmark, enhancing its infrastructure and services in the region.

- Oracle launched its second public cloud region in Saudi Arabia, hosted in a Centre3 data centre in Riyadh

- Oracle has opened its second cloud region in Singapore to meet the increasing demand for AI and cloud services, enabling customers to migrate mission-critical workloads to Oracle Cloud Infrastructure (OCI).

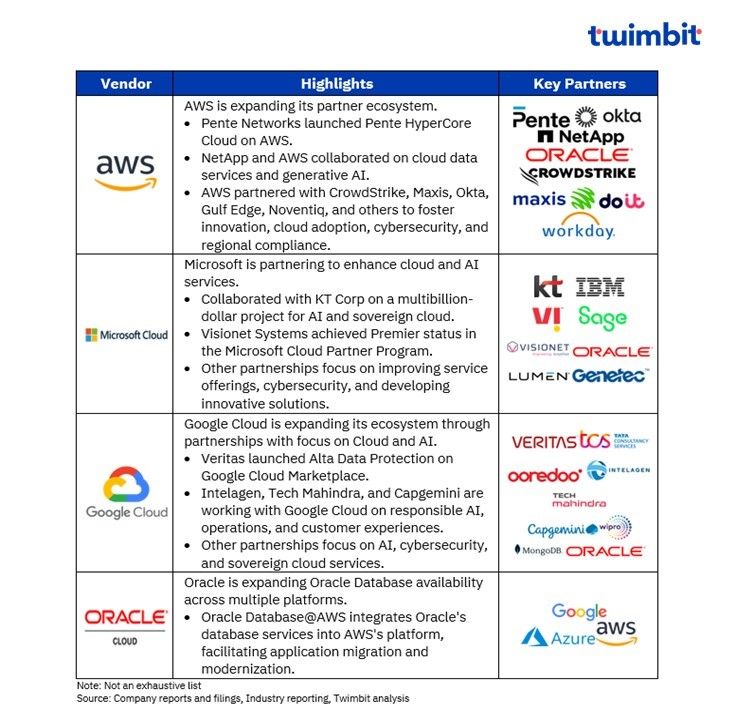

Key strategic partnerships and alliances

AWS, Google Cloud, Microsoft, and Oracle are expanding their partner ecosystems. Collaborations focus on cloud, AI, cybersecurity, and data services.

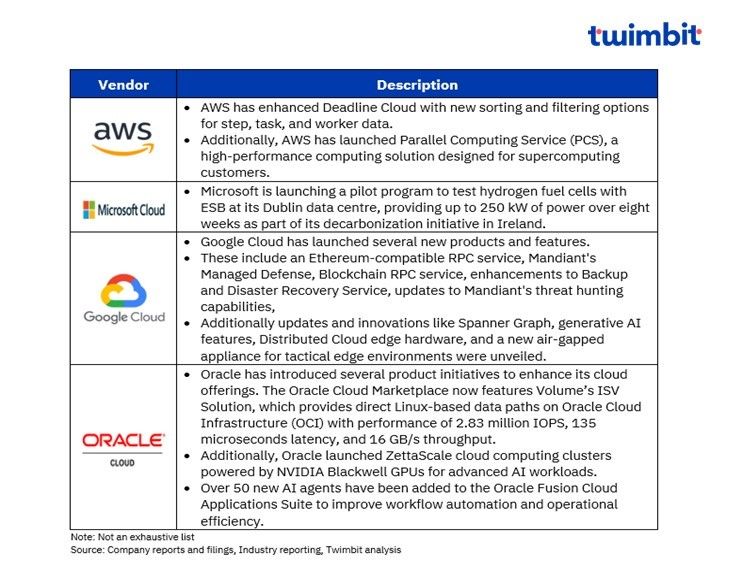

Key product initiatives

AWS, Google Cloud, Microsoft, and Oracle are innovating in cloud computing. AWS launched new features for Deadline Cloud and Parallel Computing Service. Google Cloud introduced products like Ethereum-compatible RPC service and Mandiant’s Managed Defense, whereas. Microsoft piloted hydrogen fuel cells. Oracle launched Volumez’s ISV Solution, ZettaScale cloud computing clusters, and added AI agents to Oracle Fusion Cloud Applications Suite.

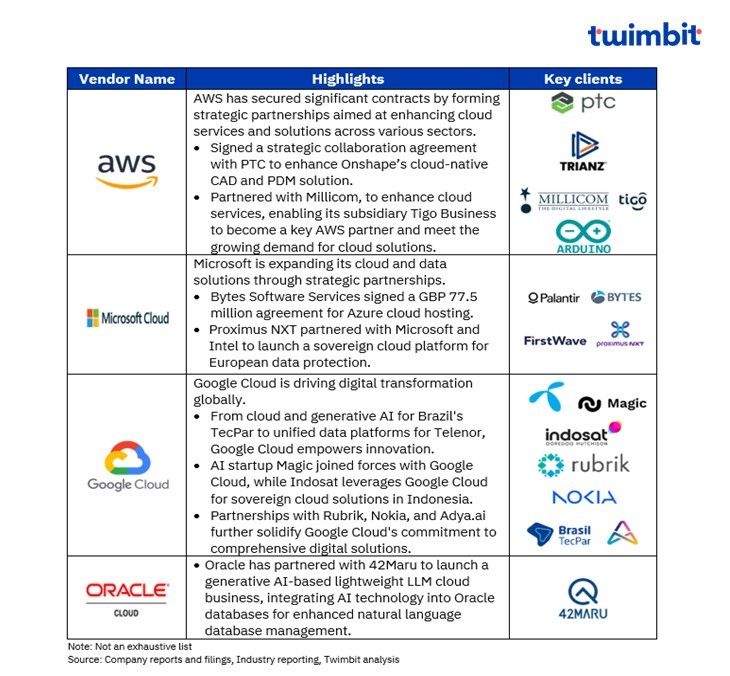

Key contract wins

Leading cloud providers continue to establish strategic partnerships to expand services: AWS boosts cloud-native CAD with PTC, Google Cloud empowers innovation globally, and Microsoft secures cloud hosting deals. Oracle partners for generative AI integration in databases.

Research methodology and assumptions

- The “Cloud Stories – Autumn 2024” report provides insights of the leading 4 cloud infrastructure providers (AWS, Microsoft Intelligent Cloud, Google Cloud and Oracle Cloud). The report also provides information related to product initiatives, partnerships, and contract wins for the period July- September 2024.

- The report primarily leverages company websites and publicly disclosed information from major cloud service providers.

- The report analyses aggregate performance and future plans of leading providers and is used to project potential demand trends, wherever applicable.

- The report aligns Oracle’s fiscal year with the calendar year by considering Q4-FY2024 equivalent to Q2-CY2024.

- Oracle Cloud revenue reporting (IaaS + SaaS) has been realigned from Q1-2023 onward and now tracks only Oracle Infrastructure Cloud (IaaS) revenue.

- Microsoft’s previous quarter figures have been adjusted to align with their new internal reporting structure, announced in August 2024. These adjustments reflect organizational changes planned for FY-2025 (July-Sep 2025). Our analysis focuses on Microsoft Intelligent Cloud (MIC), which includes Azure and its related services.

- Specifically for Google, the revenue numbers are for Google Cloud, encompassing various services like Workspace, Google Cloud Platform, data & analytics platforms, infrastructure, and collaboration tools. It’s important to note that Google doesn’t report GCP revenue separately but as part of the broader Google Cloud segment.

Click here for more contents on telecom

Related Cloud performance insights

Top APAC telcos to ace beyond connectivity revenue – H1 2024