Key takeaways

- The average Year-on-Year (YoY) revenue growth for APAC telcos reduced from ~6.1% in Q3-2023 to ~5.1% in Q3-2024.

- Despite the slowdown in growth, the 42 telcos analysed in Q3-2024 achieved a combined revenue of USD 139.1 billion. Around 74% of these telcos reported positive revenue growth, with 8 recording YoY gains exceeding 10%.

- The average EBITDA margin stabilized at around 38.5% in Q3-2024, led by Cost control measures, operational efficiency initiatives, and sustained top-line growth.

- About 72% of the 42 analysed telcos reported positive changes in EBITDA during Q3-2024, of which ~31% achieved a double-digit growth. Nearly ~21 % of telcos reported a slight EBITDA variation, within a manageable range (-3% to +3%).

- Average CAPEX intensity declined significantly from 16.9% in Q3-2023 to 14.8% in Q3-2024, owing to completion of 4G and 5G network rollouts in major markets alongwith telcos shifting focus on existing infrastructure modernisation and improving cash flow.

- Nearly 69% of the 32 telcos analysed reported a YoY CAPEX decline in Q3-2024, as compared to ~59% in Q3-2023.

- Out of the 33 analysed telcos, nearly ~46% reported increased ARPU levels in Q3-2024. Also, around 40% of the telcos reported higher YoY ARPU growth in Q3-2024 compared to Q3-2023.

- The increase in ARPU was led by strategic pricing, increased adoption of 4G and 5G services, and upselling higher-value packages

- APAC telcos are embracing technological advancements like AI, 5G, and cloud to improve network performance, enhance security, and offer innovative services. Strategic partnerships and mergers are accelerating innovation, enabling operators to future-proof their networks and provide advanced digital experiences to customers.

- Leading APAC telcos continue to make significant strides in AI investments and strategic expansions, underscoring AI’s crucial role. Telcos like Globe Telecom and LG U+ are reshuffling their leadership to drive digital transformation and AI-focused growth, whereas SK Telecom announced to restructure its business in 2025 to prioritize AI and communications, reflecting the industry’s shift towards AI-driven innovation.

Trending APAC telcos performance insights

- AI investment and strategic expansion: Leading APAC telcos continue to make significant strides in AI investments and strategic expansions, underscoring AI’s crucial role in network automation, customer experience enhancement, and monetizing networks beyond traditional connectivity.

- SK Telecom and SoftBank are at the forefront, with SK Telecom investing USD 200 million in a US based AI firm to establish a regional AI hub. Recently, SK Telecom also announced to restructure the company in 2025 into seven business divisions, to focus on AI and communications in its pursuit to become a global AI company. SoftBank’s USD 600 million acquisition of Graphcore aligns with its USD 9 billion annual investment strategy.

- Fibre network expansion and infrastructure investments: APAC telecom operators are actively expanding their optical fibre and fixed broadband networks to meet the growing demand for high-speed internet and future technological advancements.

- CelcomDigi in Malaysia has introduced “fibre-to-the-room” 1Gbps plans to cater to smart home needs and gaming. China Unicom, in partnership with Alcatel-Lucent, is deploying fibre broadband across 29 provinces using GPON technology, supporting high-demand services like IPTV. Telstra is enhancing its intercity fibre network in Australia, offering speeds up to 55 terabits per second to ensure robust connectivity between major cities.

- Mergers and market consolidation: Telecom industry consolidation is accelerating as companies seek to improve economies of scale, enhance service portfolios, and boost operational efficiency to remain competitive in a digital-first environment.

- In a bid to expand market presence, PTCL secured a USD 400 million IFC loan to acquire Telenor Pakistan, whereas Telstra announced to acquire Boost Mobile to gain access to customers seeking more affordable mobile connectivity. MobileOne (M1) acquired a 70% stake in ADG to expand in Vietnam’s tech sector Intouch Holdings merged with Gulf Energy Development in a USD 5.4 billion deal to strengthen telecom and satellite operations. Leveraging synergies of the acquisitions, AIS, Taiwan Mobile, and Far EasTone have increase their revenue and customer share.

- Leadership transitions and strategic realignments: Key leadership transitions in leading telcos signal shifts in strategic direction and adaptation to evolving digital priorities to sustain competitiveness.

- Airtel’s CEO Gopal Vittal will become Executive Vice Chairman beginning 2026 in addition to his role of Managing Director, potentially ushering new leadership. Axiata’s Dr Hans Wijayasuriya is taking on a national role to lead Sri Lanka’s digital strategy. Globe Telecom has appointed Carl Raymond Cruz as Deputy CEO and future CEO, with Juan Carlo Puno as CFO and Darius Delgado as CCO, to reinforce leadership for digital growth. LG U+ appointed Hong Bum-shik as CEO to spearhead its AI-driven transformation.

- Regulatory changes and Mobile licensing adjustments: Regulatory environments are shifting in response to market dynamics and evolving technology landscapes, as governments refine policies to align with evolving market needs.

- For instance, South Korea’s recent decision to cancel a mobile license of “Stage X” exemplifies policy adaptation to the changing telecom ecosystem. The Malaysian government awarded U Mobile a license to build the country’s second 5G network, aiming to accelerate nationwide 5G deployment alongside Digital Nasional Berhad. Telekom Malaysia withdrew from acquiring a 20% stake in DNB after missing a deadline, following Malaysia’s shift to introduce a second 5G network and privatize DNB.

- Telcos collaborate to monetize Network APIs: Telecom operators are embracing network APIs to unlock new business models and streamline digital service delivery.

- South Korean telcos SK Telecom, KT, and LG U+ are establishing common open APIs to lower entry barriers and expedite app development. Operators like AIS, Maxis, and Singtel are creating regional API exchanges for network-based authentication. In China, major telecom players such as China Mobile, China Telecom, and China Unicom have launched a One-Time Password (OTP) API to enhance the security of mobile apps and online services, illustrating the global shift towards API-driven innovation.

- Investment in Digital Infrastructure Capabilities: Telcos are focusing on digital-led innovation to facilitate smarter operations, enhanced customer experiences, and accelerated digital transformation.

- Singtel, IOH, and SK Telecom are leveraging AI-powered cloud services to streamline processes and drive digital transformation. AI is being deployed in data centres to optimize energy consumption and support advanced data processing, as demonstrated by Nxtra by Airtel and China Mobile’s investments. Rakuten is deploying Ampere Arm CPUs across its data centres to reduce power consumption.

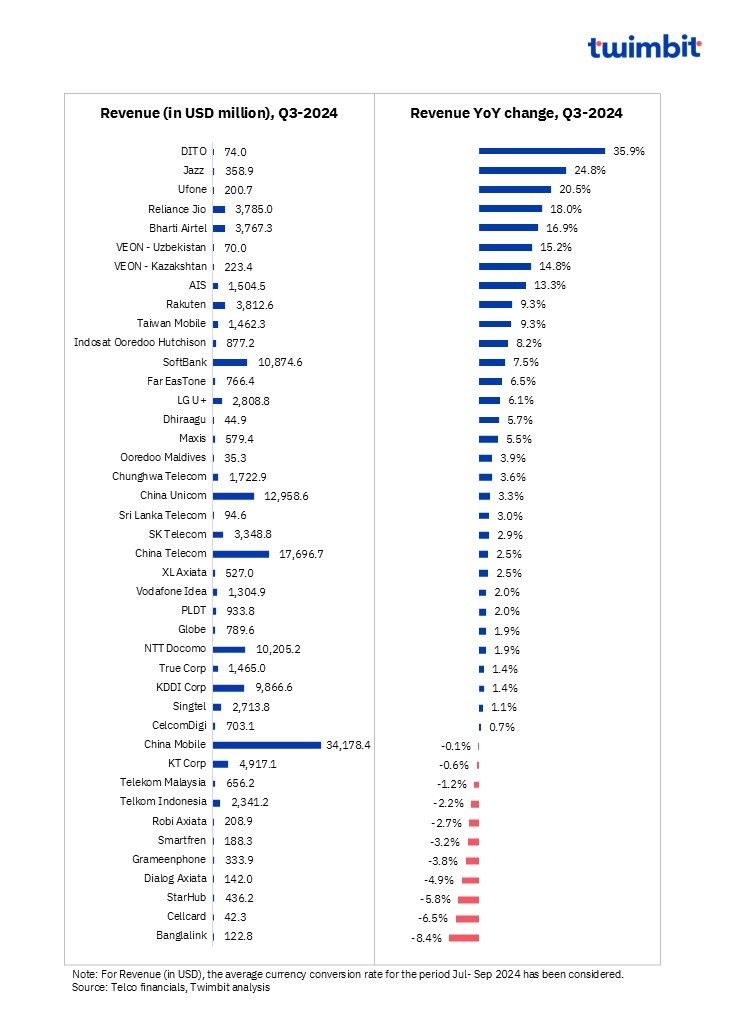

Revenue analysis of APAC telcos: Q3-2024

Average revenue growth for leading global telcos slowed from ~6.1% in Q3-2023 to ~5.1% in Q3-2024

Approximately 74% of telcos achieved YoY revenue growth in Q3-2024 (as compared to ~83% in Q3-2023). The combined revenue of the 42 analysed telcos increased by ~USD 4.2 billion to ~USD 139.1 billion in Q2-2024, with 8 telcos (around 19% of the total) of the total telcos exhibiting double-digit growth.

Exhibit 1: Revenue trends for APAC telcos, Q3-2024

Key highlights

- Telcos in the Asia-Pacific (APAC) region experienced varied revenue trends, influenced by factors such as subscriber growth, strategic pricing, digital service expansion, and external challenges.

- Several telecom operators have achieved revenue growth through expanding their subscriber base and implementing strategic pricing strategies.

- DITO reported a 35.9% YoY revenue increase to USD 74 million (PHP 4.2 billion) in Q3-2024, driven by subscriber growth and a 66% YoY surge in data revenue as network coverage expanded to 886 cities.

- India’s leading telcos Bharti Airtel and Reliance Jio reported robust revenue growth driven by strategic tariff increases and an expanding subscriber base resulting in strong performance in the mobility segment.

- Reliance Jio’s revenue increased by 18% YoY to USD 3.8 billion (INR 317.1 billion) in Q3-2024. This growth was driven by tariff hikes in the mobility segment, subscriber growth in home broadband, and an expansion in digital services.

- Bharti Airtel’s revenue increased by 16.9% YoY to USD 3.8 billion (INR 315.6 billion) in Q3-2024, driven by improved mobile segment realizations and sustained momentum in the Homes and Airtel Business segments.

- Vodafone Idea too experienced revenue growth of 2% YoY in Q3-2024 through price increases, contributing to a 5.6% increase in customer revenues.

- XL Axiata saw a 2.5% YoY revenue growth in Q3-2024, fuelled by modest subscriber gains and increased data consumption, leading to a higher blended ARPU.

- The expansion of digital and data services has been a significant revenue driver for several telecom companies.

- Jazz saw a 24.8% YoY revenue increase in Q3-2024, led by a rise in 4G subscribers and a 27.2% increase in digital revenue, with JazzCash and Mobilink Microfinance Bank growing by 85.5% and 56.3%, respectively.

- VEON – Uzbekistan achieved its 16th consecutive quarter of YoY revenue growth in Q3-2024, with a 15.2% YoY increase driven by higher demand for data and digital services.

- Rakuten’s revenue growth was primarily driven by its FinTech and mobile segments. During Q3-2024, the FinTech segment grew 12.8% YoY, supported by an expanding customer base, improved card shopping GTV, and rising interest rates. Rakuten Mobile’s revenue grew 19.5% YoY, with a 39.9% increase in subscribers to 7.9 million and higher data usage

- Merger synergies facilitated revenue growth for telcos like AIS, Taiwan Mobile, and Far EasTone.

- AIS in Thailand reported revenue growth from the TTTBB consolidation, broadband service expansion, and increased mobile data consumption. Fixed broadband revenue grew 146% YoY in Q3-2024 led by increased subscribers through TTTBB acquisition and ARPU uplift from bundled FBB products.

- Taiwan Mobile’s revenue increased 9.3% YoY in Q3-2024, driven by T Star’s merger contribution, a 5.8% ARPU increase in smartphone post-paid users, and growth in roaming and gaming revenues.

- Far EasTone reported a 6.5% YoY revenue growth in Q3-2024, driven by merger synergy with Asia Pacific Telecom, 5G plan upgrades, and growth in pre-paid and roaming business.

- Growth in fixed broadband and enterprise services also emerged as key revenue drivers for select telcos like Maxis, Chunghwa Telecom, and PLDT.

- Maxis’ revenue grew 5.5% YoY in Q3-2024, driven by 10.8% growth in Fibre and 4.2% growth in Enterprise business revenue.

- Chunghwa Telecom’s revenue growth was led by a 2.1% increase in consumer revenue and a 5.9% increase in enterprise revenue, driven by a 22% growth in ICT business.

- PLDT reported increased revenue from Mobile, Fibre, and Enterprise segments, driven by upselling and higher demand for connectivity and ICT services. Enterprise revenue growth was high due to increased demand in core connectivity and ICT services.

- In contrast, Chinese telecom operators have faced stagnancy in revenue growth since the start of FY-2023, particularly in FY-2024, due to challenges in monetizing 5G mobile services amid competitive pressures.

- While China Telecom and China Unicom reported revenue growth, China Mobile’s revenue declined by 0.1% YoY in Q3-2024.

- Additionally, several telcos faced revenue declines due to external challenges such as political unrest, natural disasters, and market pressures.

- Robi Axiata, Grameenphone, and Banglalink in Bangladesh experienced revenue declines due to political unrest, internet shutdowns, and floods, negatively impacting ARPU.

- StarHub’s revenue declined in Q3-2024 due to lower revenue from Mobile and entertainment segments, offsetting broadband growth. Mobile revenue fell due to lower post-paid ARPU, VAS revenues, and usage revenue, while entertainment revenue declined due to lower subscription and advertising revenue.

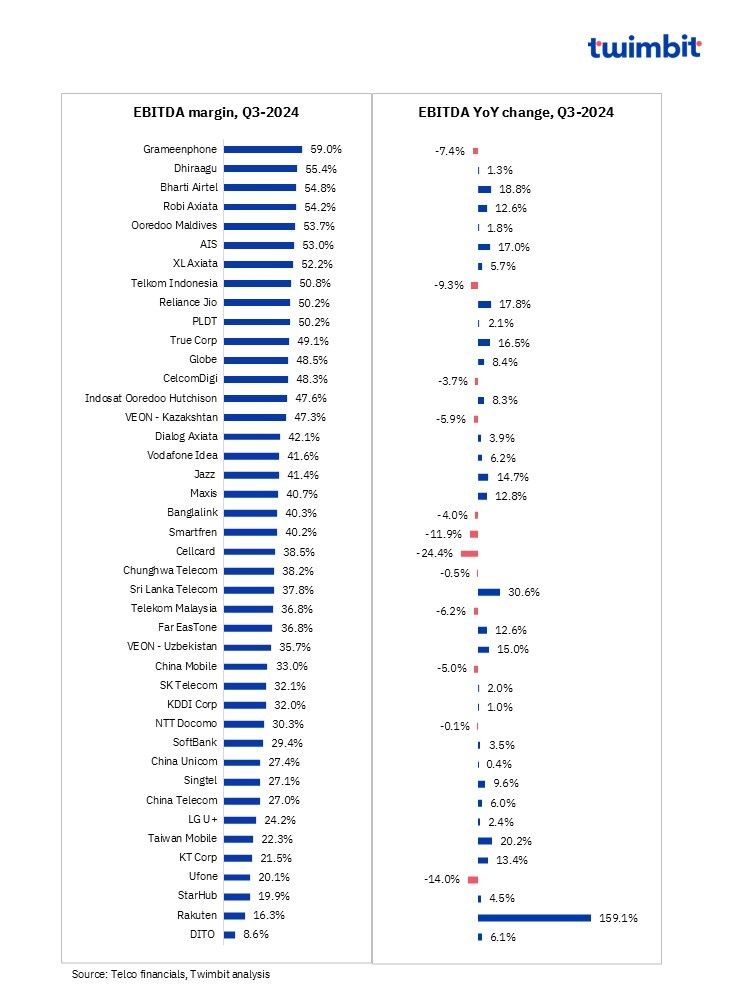

EBITDA analysis of APAC telcos: Q3-2024

Average EBITDA margin for APAC telcos stabilised at ~38.5% in Q3-2024

Cost control measures, operational efficiency initiatives, and sustained top-line growth have stabilized EBITDA for ~72% of the analysed telcos, with 13 telcos (or about 31% of the total), achieving double-digit growth.

Exhibit 2: EBITDA and EBITDA margin trends for APAC telcos, Q3-2024

Key highlights

- The EBITDA trends among APAC telecom operators reveal a landscape marked by strategic adaptation and market challenges. While some telcos achieved EBITDA growth through revenue increases and cost optimization, others faced pressures from rising costs and market challenges. This duality underscores the imperative for telecom companies to innovate and adapt strategies to sustain financial performance.

- Rakuten’s EBITDA surged YoY in Q3-2024 owing to the impact of Mobile ecosystem contribution incorporation which was reflected in segment results from Q3-2024 onwards.

- Revenue growth driven by subscriber additions and higher ARPU facilitated EBITDA growth for telcos like DITO, Bharti Airtel, Reliance Jio, and Jazz.

- Bharti Airtel’s EBITDA grew 18.8% YoY to USD 2.1 billion (INR 173 billion) in Q3- 2024, driven by higher revenue growth, with a stable EBITDA margin of 53.1%.

- Reliance Jio’s EBITDA increased by 17.8% YoY to USD 1.9 billion (INR 159.3 billion) in Q3-2024, driven by strong revenue growth and efficient utilization of operating capacities. The EBITDA margin remained stable at 50.2%.

- Jazz reported EBITDA growth of 14.7% YoY in Q3-2024, supported by consistent revenue growth and margin expansion in digital services (JazzCash).

- DITO reported significant EBITDA improvement due to continuous revenue growth offsetting operating costs, reflecting effective financial management.

- Vodafone Idea reported its highest quarterly EBITDA in Q3-2024 since the merger, facilitated by increased ARPU.

- Cost savings, optimization efforts, and operational efficiency initiatives also contributed to EBITDA growth for select telcos.

- Robi Axiata’s EBITDA growth of 12.6% YoY in Q3-2023 was driven by structured measures on OPEX and CAPEX optimization, enhancing financial performance.

- Singtel’s EBITDA increased by 9.6% YoY in Q3-2024, driven by improved performance and cost optimization. Optus and NCS also reported significant EBITDA growth due to disciplined cost management and higher operating revenue.

- XL Axiata’s EBITDA grew 5.7% YoY in Q3-2024 through cost savings and efficient operations.

- Dialog Axiata reported EBITDA growth of 3.9% YoY in Q3-2024, benefiting from cost rescaling efforts, maintaining financial stability despite market challenges.

- Increased customer count, network consolidation, and cost benefits from merger synergies facilitated EBITDA growth for telcos like AIS, Taiwan Mobile, and Far EasTone.

- Taiwan Mobile’s EBITDA grew by 20.2% YoY in Q3-2024, supported by merger synergies and network integration.

- AIS reported EBITDA growth of 17% YoY in Q3-2024, benefiting from TTTBB contributions and core business growth.

- Far EasTone reported EBITDA growth of 12.6% YoY in Q3-2024, driven by merger synergies and enhanced margins.

- In China, telecom operators such as China Unicom and China Telecom experienced EBITDA growth, while China Mobile’s EBITDA saw a slight decline due to decreased revenue.

- Conversely, some telcos faced pressures from increased costs and market challenges, resulting in EBITDA decline during the quarter.

- Cellcard’s EBITDA declined 24.4% YoY in Q3-2024, as operating profit decreased by 33% due to revenue decline and increased operating costs.

- Ufone’s EBITDA declined in Q3-2024 on YoY basis, due to cost inflation and a one-off benefit in the prior year.

- VEON – Kazakhstan’s EBITDA decreased by 5.9% YoY in Q3-2024, due to a higher base effect from a previous tax benefit and increased charitable donations.

- Telekom Malaysia’s EBITDA declined as revenue growth slowed while costs remained stable, impacting overall profitability.

- Telkom Indonesia’s EBITDA declined due to increased expenses from IndiHome integration and a new wholesale agreement, alongside a YoY revenue decline.

- Banglalink’s EBITDA decreased by 4.0% YoY in Q3-2024, impacted by increased SIM taxes, higher electricity tariffs, and network expansion costs, despite effective cost control measures.

- Grameenphone experienced a significant decline in operating profit due to revenue decrease and rising costs, resulting in a 7.4% YoY EBITDA decline in Q3- 2024.

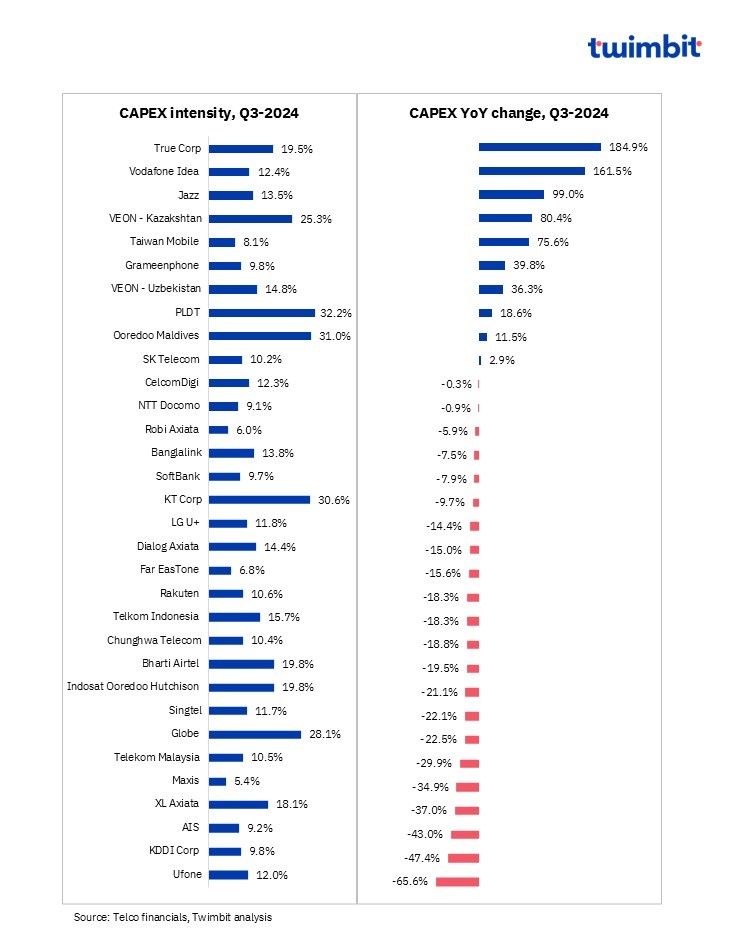

CAPEX analysis of APAC telcos: Q3-2024

Average CAPEX intensity declined to 14.8% in Q3-2024 as compared to 16.9% in Q3-2023, as 4G/5G network deployment of leading telcos reaches completion

Nearly 69% of the 32 telcos analysed reported a YoY CAPEX decline in Q3-2024, up from ~59% in Q3-2023. The maturation of 4G and 5G network rollouts in major markets alongwith telcos focussing on existing infrastructure modernisation and improving cash flow and profitability suggests CAPEX stabilisation or a potential decrease in the upcoming years.

Exhibit 3: CAPEX and CAPEX intensity trends for APAC telcos, Q3-2024

- The telecommunications industry in the APAC region is witnessing a dynamic shift in Capital Expenditure (CAPEX) strategies. As the rollout of 4G and 5G networks reaches maturity, telecom operators are recalibrating their investment focus to optimize cash flow and enhance profitability.

- Telcos are strategically reducing their capex as they transition from aggressive network expansion to optimizing existing infrastructure. This shift is driven by the need to improve cash flow and profitability while maintaining network quality.

- CAPEX for Ufone reduced by 65.6% YoY in Q3-2024 due to project phasing, with the telco focusing on FTTH expansion and enhancing mobile and fixed network capacity.

- KDDI and AIS are examples of telcos that have peaked in their CAPEX investments and are now slightly reducing spending, leveraging existing network assets. AIS benefited from synergies with TTTBB’s broadband footprint.

- Although PLDT’s CAPEX increased YoY in Q3-2024, the company aims to reduce CAPEX and CAPEX intensity to achieve positive cash flow, targeting a reduction to USD 1.3–1.4 billion (PHP 75-78 billion) from a peak of USD 1.7 billion in FY 2022 (PHP 97 billion).

- Several telcos are focusing on cost optimization and CAPEX reduction to improve financial performance and accelerate profitability.

- Globe Telecom has reduced its CAPEX in line with its strategy to optimize capital utilization while maintaining network quality, aiming for positive free cash flows by 2025.

- Rakuten is working on cost optimization and planning significant CAPEX reductions to accelerate profitability.

- Aligning with the FMC strategy, Telkom Indonesia prioritized optimizing CAPEX synergy across access networks, backbone, and IT systems for better efficiency, resulting in reduced CAPEX with a focus on digital connectivity.

- CAPEX for telcos like Banglalink and Bharti Airtel in India declined due to peak investments in 4G and 5G rollouts in previous years.

- Banglalink CAPEX intensity reduced to 13.8% in Q3-3024 as the major phase of its 4G rollout concluded in previous years.

- With CAPEX peaking in FY-2023 for 5G rollout, Bharti Airtel’s CAPEX declined 19.5% YoY in Q3-2024, primarily impacted by a ~30% decline in the B2C segment.

- Contrasting the trend of optimization, some telcos continue investing in ICT infrastructure and capabilities to meet growing demand and enhance service quality.

- Telcos like SK Telecom, KT Corp, Softbank, and Singtel are focussing on data centres, cybersecurity, and AI-related investments as key growth areas.

- In China, after substantial 5G investments, telecom operators concentrate on strengthening digital capabilities, including cloud, big data, IoT, and 5G commercial projects like smart cities and factories.

- Taiwan Mobile’s CAPEX increased 75.6% YoY in Q3-2024, due to network consolidation payments and strategic investment in ICT firm Systex.

- Ooredoo Maldives’ higher CAPEX in Q3-2024 was driven by strategic projects, including Disaster Recovery site and Subsea Cable investments.

- Investment in 4G and 5G network expansion, fibre rollout, and digital capability investments continue to drive CAPEX spending for select telcos like VEON (in Kazakhstan, Pakistan, and Uzbekistan), TrueCorp (Thailand), Vodafone (India), Taiwan Mobile (Taiwan), Grameenphone (Bangladesh), and PLDT (Philippines).

- True Corp’s CAPEX increased significantly in Q3-2024, focusing on network modernization, with over 10,800 towers upgraded as part of its “3Zero” strategy to transform its network into an AI-driven intelligent infrastructure.

- Vodafone Idea has embarked on a transformative three-year CAPEX plan, investing significantly in network equipment to expand 4G and 5G coverage, aiming for 4G population coverage of 1.2 billion by September 2025 and starting 5G rollout in early 2025.

- Veon Group operating telcos in APAC region enhanced their CAPEX to expand and upgrade 4G networks, addressing demand and enhancing network leadership.

- Jazz continued expanding its 4G network and increased investment in digital products.

- VEON – Kazakhstan increased CAPEX to meet demand and strengthen network leadership, focusing on massive MIMO technology and 4.9G wireless technology rollouts.

- VEON – Uzbekistan reported higher CAPEX for 5G network expansion.

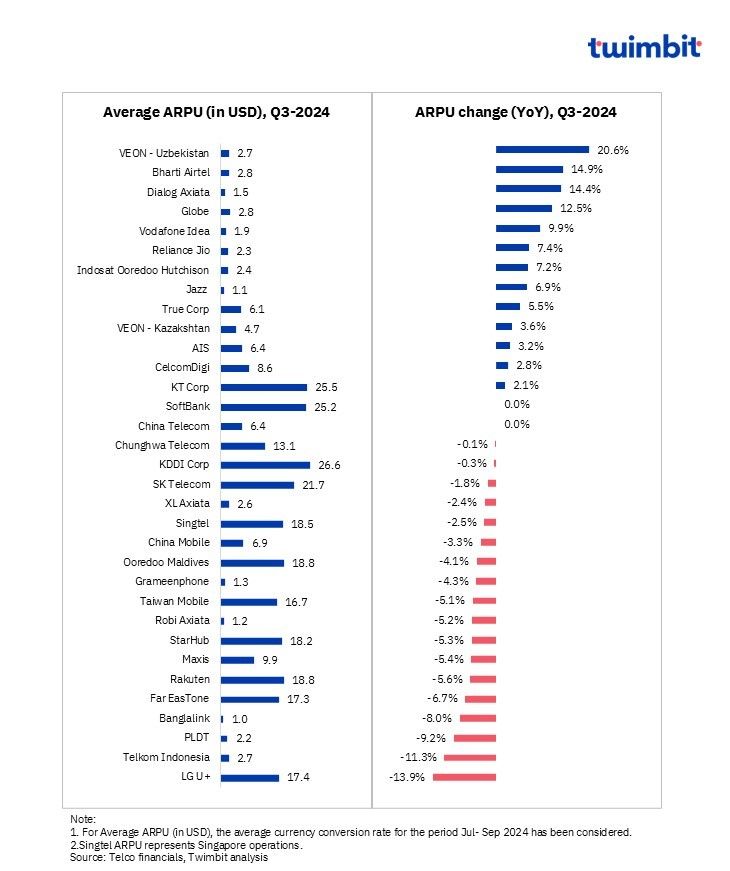

ARPU analysis of APAC telcos: Q3-2024

Average ARPU remained stagnant (2.2% YoY growth), reaching USD 9.6 in Q3-2024

The ARPU analysis for the 33 telcos analysed is as follows:

- Nearly 46% reported increased ARPU levels in Q3-2024

- Nearly 40% reported higher YoY ARPU growth in Q3-2024 compared to Q3-2023

- Nearly 27% of the telcos % stabilized their ARPU levels in Q3-2024, with YoY changes ranging from -3% to 3%

Exhibit 4: ARPU trends for APAC telcos, Q3-2024

Key highlights

- Telcos in the APAC region are experiencing diverse ARPU with some benefiting from strategic pricing, increased adoption of 4G and 5G services, and upselling higher-value packages, others face challenges from intense competition and market saturation.

- VEON Group’s operating telcos reported ARPU growth driven by increased adoption of 4G and digital services.

- VEON – Uzbekistan saw a 20.6% YoY ARPU increase in Q3-2024, supported by higher 4G user penetration and digital product uptake.

- Jazz experienced a 6.9% YoY ARPU increase in Q3-2024, with a 23% growth in multiplay B2C customers, driven by digital services like JazzCash and entertainment platforms.

- VEON – Kazakhstan expanded its digital portfolio, resulting in higher ARPU and lower churn among multiplay customers, who contributed 66.8% of B2C revenues. Multiplay customers who used services such as IZI, Simply, My Beeline, Hitter and BeeTV reached over 3.9 million, up 2.7% YoY.

- IOH’s ARPU increased 7.2% YoY in Q3-2024, facilitated by increased data usage, with data traffic rising 11.2% to 4,085 PB.

- In Q3- 2024, Indian telcos experienced significant ARPU growth due to tariff hikes implemented in July 2024, with Bharti Airtel maintaining its leadership position, followed by Reliance Jio. However, these tariff increases led to a subscriber shift towards the government-owned BSNL, which did not raise its tariffs.

- The full impact of these hikes on ARPU is expected to become apparent over the next few quarters. ARPU growth is also anticipated to continue, driven by the migration from 2G to 4G networks and an increase in post-paid subscribers, boosting average data usage per customer.

- Bharti Airtel’s ARPU grew 14.9% YoY in Q3-2024, supported by an expanded subscriber base and a higher concentration of data users, increasing mobile data and voice usage in both Africa and India.

- Vodafone Idea also experienced a 9.9% YoY ARPU growth due to tariff increases.

- Reliance Jio reported a 7.2% YoY ARPU growth in Q3-2024, driven by strategic tariff revisions, strong subscriber growth, and increased data and voice consumption.

- The full impact of these hikes on ARPU is expected to become apparent over the next few quarters. ARPU growth is also anticipated to continue, driven by the migration from 2G to 4G networks and an increase in post-paid subscribers, boosting average data usage per customer.

- Strategic upselling, content bundles, and personalized value-based packages facilitated growth for select telcos in the region.

- True Corp achieved a 5.5% YoY ARPU growth in Q3-2024 by removing discounts and upselling customers into higher-value packages.

- CelcomDigi reported growth in Blended ARPU led by strong adoption of 5G plans including high-value plan upgrades in the post-paid segment.

- AIS continued to grow its mobile ARPU by focusing on value-based offerings and personalized packages.

- Conversely, some telecom operators are facing ARPU declines due to intense competition, market saturation, and external disruptions.

- In Singapore, despite increased subscriber counts for SingTel and StarHub, ARPU levels have been pressured by aggressive pricing strategies from Simba Telecom.

- StarHub’s ARPU declined 5.3% YoY in Q3-2024 to USD 18.2 (SGD 24).

- Singtel’s ARPU declined 2.5% YoY in Q3-2024 to USD 18.5 (SGD 24.4).

- In Singapore, despite increased subscriber counts for SingTel and StarHub, ARPU levels have been pressured by aggressive pricing strategies from Simba Telecom.

- Intense competition in the Chinese telecommunications market has exerted downward pressure on ARPU levels as telcos strive to maintain low pricing.

- China Telecom’s ARPU remained stable at USD 6.4 (CNY 45.6), despite a 12% increase in 5G package subscribers to 345 million in Q3-2024.

- China Mobile experienced a 3.3% YoY ARPU decline to USD 6.9 (CNY 49.5), despite a 4.9% growth in 5G network customers to 539 million, as average Minutes of Usage and Data Traffic per User remained unchanged.

- In Bangladesh, telcos faced ARPU declines due to social unrest in July and August, leading to internet shutdowns.

- In South Korea, SK Telecom and LG U+ saw ARPU declines despite growth in 5G subscriptions, while KT Corp managed to increase ARPU through a rise in 5G handset adoption.

Key strategic developments: Q3-2024

Key strategic partnerships and alliances: Q3-2024

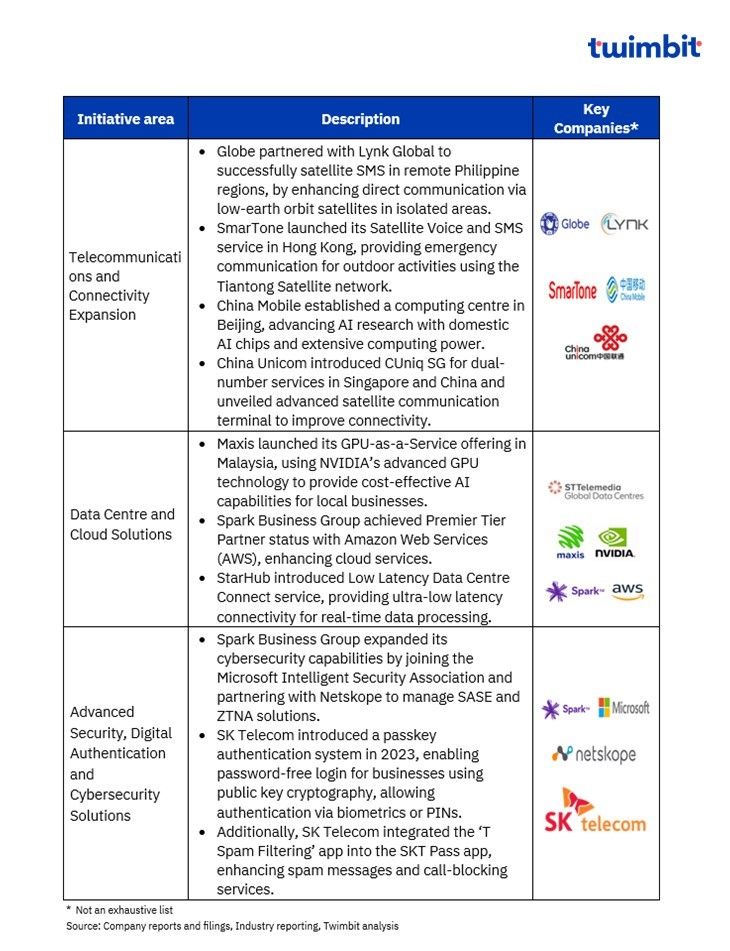

Telcos are leveraging AI, cloud technologies, and network innovations to enhance services, improve network performance, and explore new business opportunities like satellite communication and cloud-based solutions. These collaborations aim to future-proof networks and provide advanced digital experiences to customers.

Key strategic initiatives: Q3-2024

APAC telecommunications industry is rapidly evolving, driven by technological advancements like AI, 5G, cloud computing, and satellite technology. Operators are focusing on improving network performance, enhancing security, and offering innovative services to meet the evolving needs of their customers.

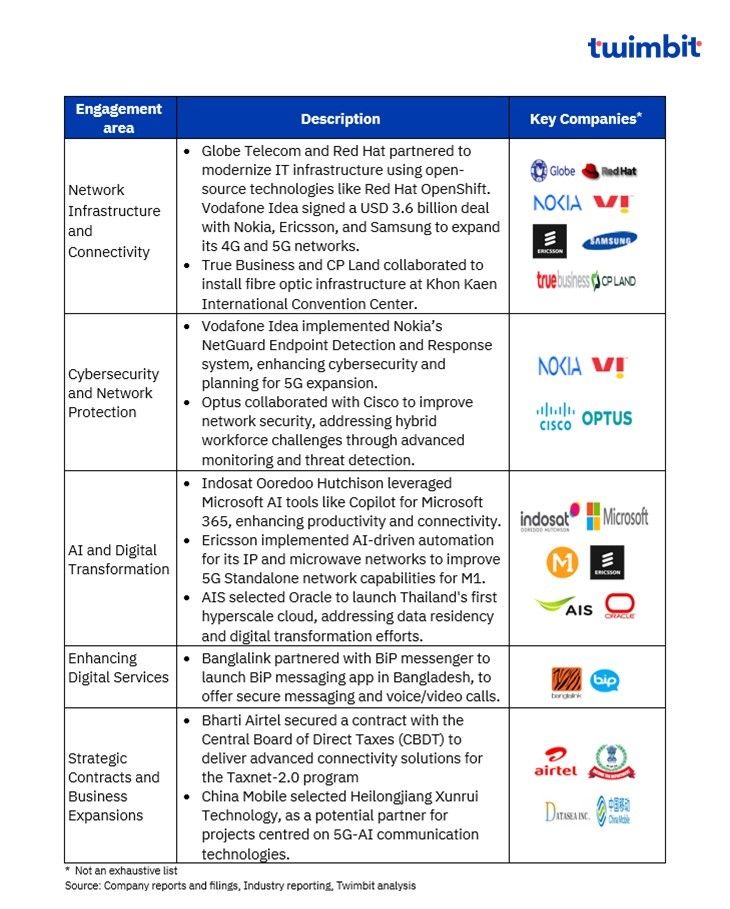

Key contract wins: Q3-2024

APAC telcos continue to witness the technological transformation shift, driven by partnerships and advancements in technology, such as open-source solutions, 5G networks, AI, and cloud infrastructure, to enhance operational efficiency, cybersecurity, and customer experience.

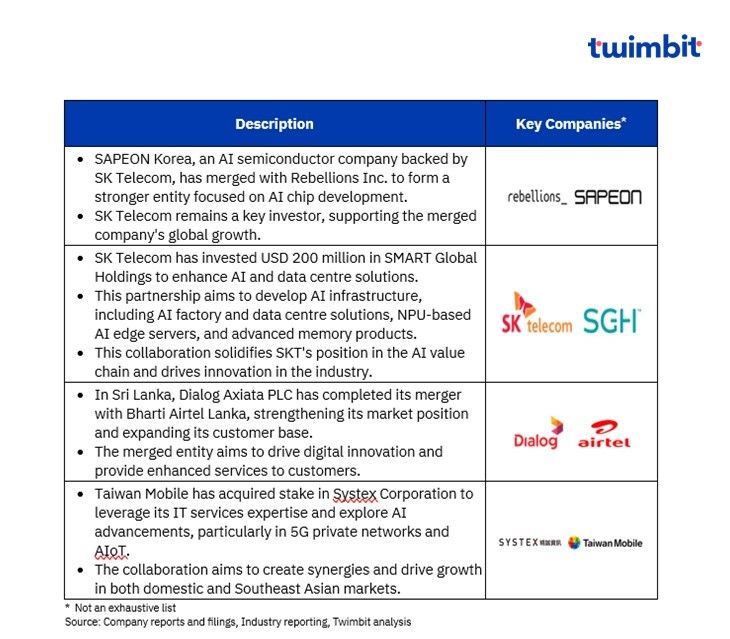

Key M&As and Divestures: Q3-2024

The business of APAC telcos is undergoing a significant transformation, driven by advancements in AI and semiconductor technologies. Strategic mergers are accelerating innovation, enabling operators to enhance network capabilities, explore new business opportunities, and strengthen their position in the global market.

Research Methodology and Assumptions

- The “APAC Telcos Performance Benchmarks: Autumn 2024” report provides key findings regarding the performance of telcos for key financial metrics, including Revenue, EBITDA, CAPEX, and ARPU for July – September 2024.

- This report uses data from telecommunications companies and extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the January-December period.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate representing the average USD exchange rate for the period July – September 2024 has been applied throughout the report.

- The report presents a comprehensive assessment of Revenue and EBITDA for 42 telecommunication companies each. Additionally, CAPEX and ARPU analyses encompass data from 32 and 33 telcos, respectively.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.