In today’s fast-paced digital world, embedded insurance is revolutionizing how consumers access and purchase insurance. Imagine buying a new smartphone online and seamlessly adding insurance coverage with just a click. This is the essence of embedded insurance—integrating insurance products directly into the purchase journey of non-insurance offerings, making it more accessible and convenient for consumers.

Why embedded insurance?

Embedded insurance simplifies the insurance purchasing process for both consumers and providers. For customers, it offers tailored coverage bundled with their main product purchase, eliminating the need for separate transactions. For insurance companies, it reduces customer acquisition costs and opens new revenue streams by integrating insurance into existing consumer journeys.

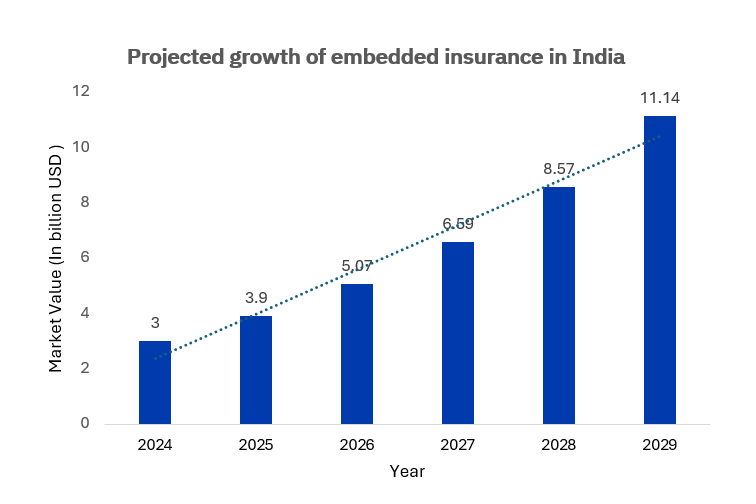

Market dynamics and growth potential

The embedded insurance market in India is valued at approximately US $3 billion in 2024, with an expected growth rate of 30% CAGR over the next five years.

Market landscape

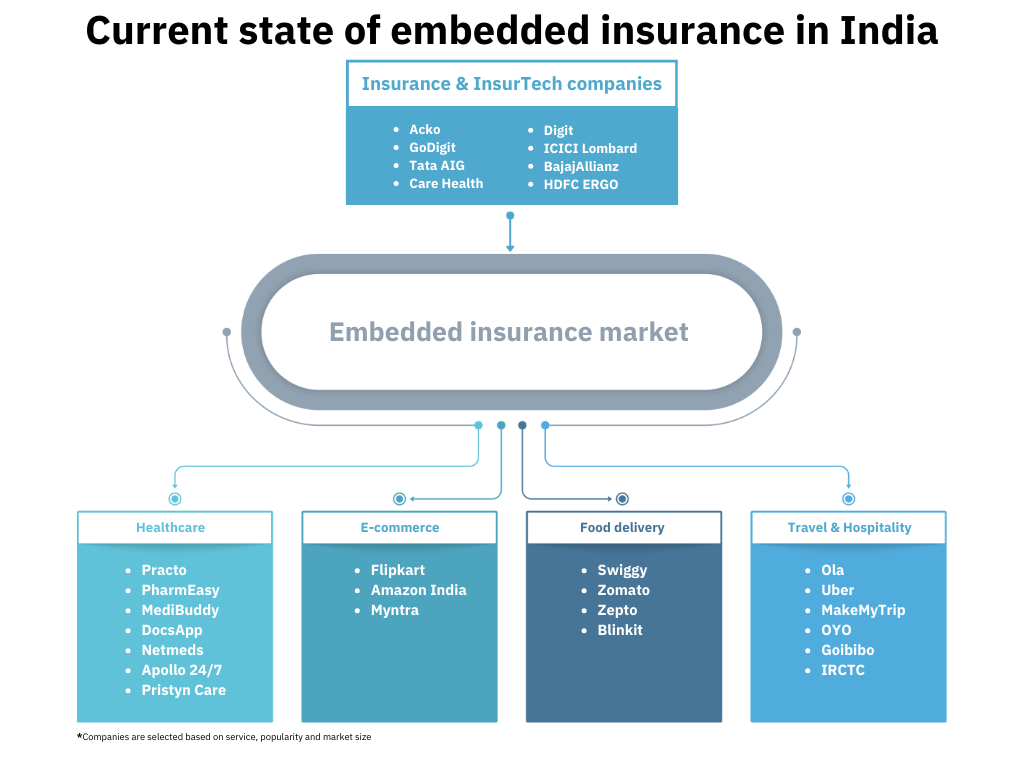

The embedded insurance market landscape in India is characterized by a dynamic integration of traditional insurance providers and innovative InsurTech companies. These entities collaborate to offer integrated insurance solutions across key sectors such as healthcare, e-commerce, food delivery, and travel & hospitality, facilitating seamless insurance solutions embedded within everyday services.

3 Growth drivers

- Digital-native consumers: With over 751 million active internet users in India, predominantly millennials and Gen Z, there is a growing demand for quick and easy insurance options integrated into daily activities.

- Ecosystem expansion: The rise of e-commerce platforms, fintech services, and digital healthcare providers has created vast opportunities for embedding insurance into consumer journeys.

- Cost and speed advantages: Integrating insurance into existing purchase processes reduces customer acquisition costs and speeds up the purchase process, benefiting both consumers and providers.

3 Powerful forces propelling revenue growth in India’s embedded insurance market

1. Rising middle-class income:

The burgeoning middle class, now comprising over 432 million individuals. The Union Budget 2025 introduced significant income tax reforms, enhancing disposable incomes and increasing the capacity to invest in insurance products.

2. Growing customer demand for digital payments

In the fiscal year 2022-2023, over 70% of insurance premiums were paid online, reflecting a significant shift towards digital transactions. Insurers are leveraging digital platforms to offer frictionless purchase experiences, personalized policies, and efficient claims processing, thereby attracting a broader customer base.

3. Regulatory support from IRDAI:

The Insurance Regulatory and Development Authority of India (IRDAI) has been instrumental in fostering digital insurance innovations. Notable initiatives include:

a. Regulatory Sandbox Regulations, 2025: Establishing a framework for insurers to pilot innovative products and services in a controlled environment, thereby encouraging experimentation and rapid deployment of digital insurance solutions.

b. Maintenance of Information by the Regulated Entities and Sharing of Information by the Authority Regulations, 2025: Requiring insurers to adopt electronic record-keeping with robust security measures, facilitating efficient data management and fostering consumer trust in digital insurance platforms.

c. Issuance of e-Insurance Policies Regulations, 2022: Mandating the electronic issuance of all insurance policies to streamline policy management and improve consumer accessibility.

4 Winning strategies of embedded insurance

Several successful partnerships highlight the potential of embedded insurance:

- OLA and InsureMO: By integrating ride insurance into its platform, OLA offers real-time coverage for passengers, enhancing safety and customer trust.

- ACKO & Amazon: ACKO’s collaboration with Amazon has streamlined the insurance process for e-commerce, offering affordable microinsurance and rapid claims settlement.

- Paytm & HDFC Ergo: The “Paytm Payment Protect” plan safeguards digital transactions against fraud, boosting customer confidence in mobile payments.

- Goibibo & ACKO: By embedding travel insurance into its booking platform, Goibibo provides a convenient safety net for travelers, enhancing their overall experience.

Conclusion

Embedded insurance is not just a trend; it’s a transformative approach that is reshaping the insurance landscape in India. By integrating insurance into everyday platforms, it makes financial security more accessible and convenient for consumers. As India continues to embrace digital transformation, embedded insurance is set to become a game-changer, offering a seamless and efficient way to access insurance coverage.