Trending Middle East telcos performance insights

AI integration transforms telecom operations: Telcos in the Middle East are at forefront of AI adoption, in order to enhance operations and customer experiences.

- Leading telcos like Ooredoo Group, du, e& UAE and Omantel are partnering with tech companies such as Microsoft, Jio Haptik, and Nvidia, to enhance AI capabilities.

- Batelco has introduced “Basma,” an AI-powered digital assistant, offering 24/7 customer support via its app and website.

Infrastructure expansion and modernization: Telcos in the region continue to invest to expand and modernize digital infrastructure. These include constructing data centres, expanding networks, and deploying advanced technologies to support digital transformation and regional connectivity.

- Ooredoo Group secured a USD 550 million 10-year hybrid financing deal, to strengthen its data centre and AI infrastructure across the MENA region.

- Mobily, in collaboration with Telecom Egypt, is developing a submarine cable linking Saudi Arabia and Egypt to improve regional connectivity.

Building collaborative ecosystem for business agility: Leading telcos pursue strategic partnerships to enhance services, expand market reach, and drive innovation.

- du has teamed up with Telefónica to enhance B2B and digital services, while e& UAE collaborated with HPE on managed services.

- A partnership between Thales and Batelco facilitates the deployment of an IoT connectivity management platform.

Geographic expansion: Telcos pursue divergent strategies to scale efficiencies and diversify service offerings.

- STC increased its stake in Telefónica to 9.9%, while Zain Group completed the acquisition of IHS Kuwait, to strengthen its digital infrastructure strategy.

- e& secured a controlling stake in PPF Telecom’s assets across Bulgaria, Hungary, Serbia, and Slovakia, to expand its presence in Central and Eastern Europe.

Regulatory developments and Licensing adjustments: Regulatory frameworks continue to evolve in alignment with the market trends and technological progress.

- Egypt’s National Telecom Regulatory Authority (NTRA) has granted 5G licenses to Orange Egypt, Vodafone Egypt, and e& Egypt.

- In Saudi Arabia, stc Group, Mobily, and Zain KSA have acquired low-band spectrum (600 MHz, 700 MHz, and 380 MHz), and is projected to contribute SAR 25 billion to the national GDP by 2030.

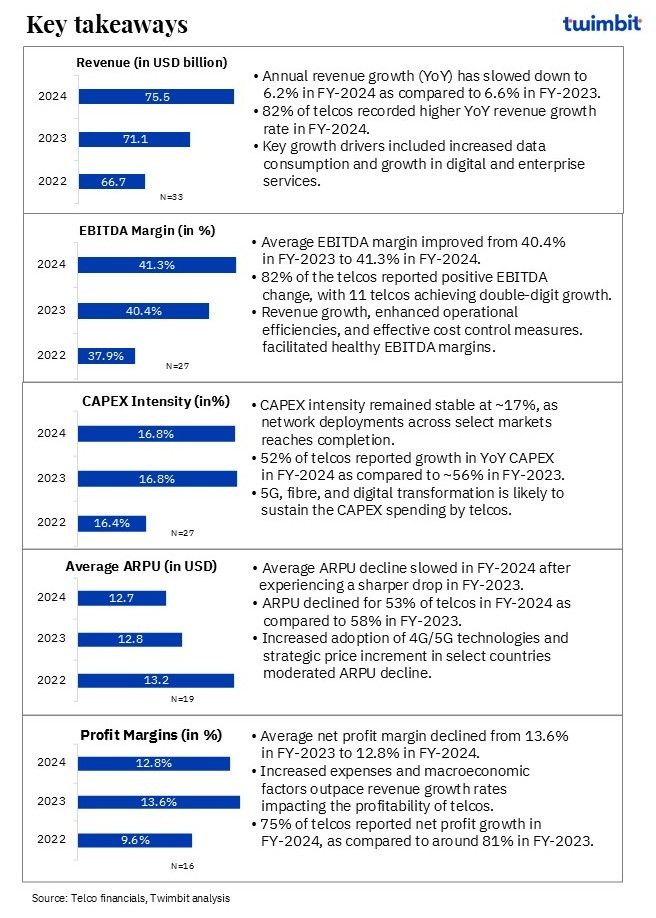

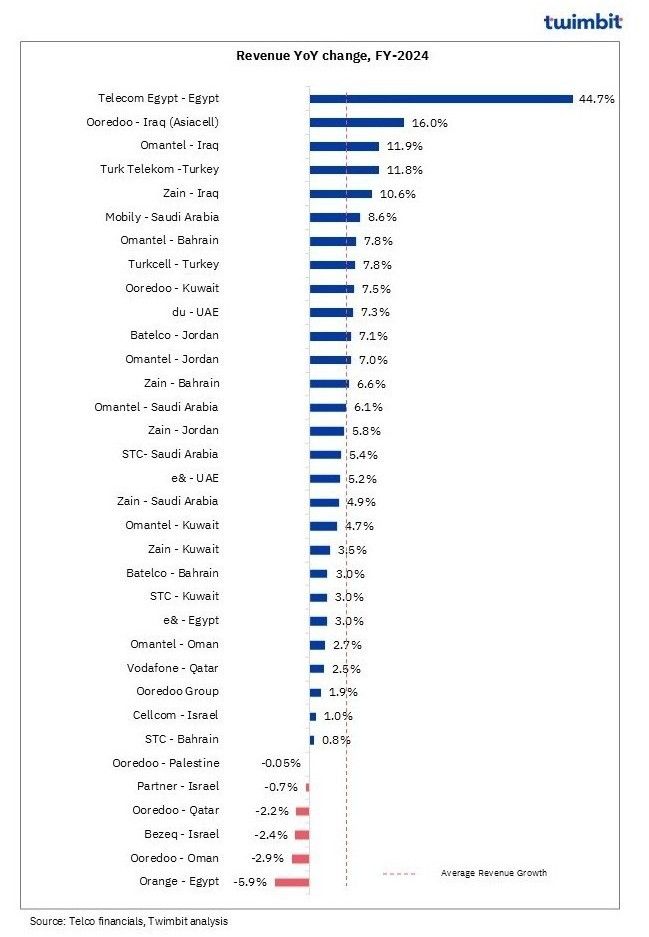

Revenue analysis of Middle East telcos: 2024

Average annual revenue growth for Middle East telcos declined from 6.6% in FY-2023 to 6.2% in FY-2024

As digital transformation accelerated, telcos in Middle East region grappled with surging data demand, expanding subscriber base, and the ever-present shadow of economic and currency challenges.

Nearly 82% of telcos recorded positive YoY revenue growth rates in FY-2024 as compared to ~79% in FY-2023. Cumulatively, this accounted for a total revenue of ~USD 76 billion in FY-2024, representing an incremental growth of ~USD 4.4 billion.

15% of the telcos achieved double-digit growth in FY-2024 as compared 18% in FY-2023, resulting in average annual YoY revenue growth declining to 6.2% in FY-2024.

Exhibit 1: Revenue trend of telcos in the Middle East, FY-2024

Key highlights

Telcos are navigating a dynamic landscape by expanding data services, growing their subscriber base, adjusting prices to economic conditions, diversifying revenue through digital and enterprise services, optimizing international operations, and addressing economic and currency challenges.

Data services growth: The insatiable demand for data emerged as a cornerstone of revenue growth, reflecting the region’s digital awakening. Telcos continue to shift towards data-centric offerings, meeting the region’s connectivity needs, and positioning them as digital enablers.

- Telecom Egypt’s revenue increased by 44.7% YoY, primarily driven by a 48% surge in data revenue. The growth was fuelled by rapid adoption of bandwidth intensive application, increasing smartphone penetration and growing shift towards cloud-based service. Growth in other segments like Domestic Wholesale, International Carriers and International Customer & Networks also facilitated the revenue growth.

- du – UAE’s revenue grew by 7.3% YoY, driven by growth in mobile and fixed services, both of which registered growth in subscriber count and ARPU.

- e& – UAE reported 5.2% YoY revenue increase in FY-2024, benefitting from strong performance in the mobile segment which grew by 5.3% YoY facilitated by growth in both prepaid and postpaid segments.

Subscriber base expansion: Growing the subscriber base proved another vital theme for revenue growth for key telcos in the region. This expansion, often in selected markets, underscored a tale of scaling operations to capture new users, particularly in less saturated regions.

- Mobily – Saudi Arabia’s revenue increased by 8.6% YoY in FY-2024, supported by its customer acquisition strategy resulting in mobile subscriber base reaching to 12.3 million (+3.9% YoY) which facilitated 4.6% growth in Consumer segment revenue.

- Zain Group also reported strong performances across its operations in Iraq, Bahrain, Jordan, and KSA, with implied subscriber growth contributing to this success.

Price adjustments: Price adjustments emerged as a critical strategy, especially in inflationary environments.

- Turkcell – Turkey reported revenue growth of 7.8% YoY in FY-2024, with Turkcell Türkiye’s revenues increasing by 8.3% YoY, primarily driven by price adjustments and a higher postpaid customer base, illustrating effective pricing strategies in a competitive market.

Digital and Enterprise services: The shift towards digital and enterprise services marked another significant theme, with telcos diversifying their offerings to capture new revenue streams.

- Turkcell’s Techfin segment revenue surged 30.9% YoY in FY-2024, contributing significantly to its overall growth and highlighting its successful diversification into digital financial services.

- Etisalat (e&)’s enterprise segment grew by 7.5% YoY in FY-2024, adding to its revenue growth, driven growing demand for cloud and cybersecurity offerings, thereby demonstrating the increasing importance of B2B services in the telecom sector.

International and subsidiary performance: For some telcos, international operations and subsidiaries were growth engines, as telcos leverage diverse markets to offset domestic saturation.

- Omantel Group’s revenue growth was supported by strong performances in Iraq, Bahrain, Jordan, Saudi Arabia, and Kuwait, underscoring its effective regional strategy.

- STC Group achieved YoY revenue increase was also supported by growth in its operations in Bahrain and Kuwait, showcasing the benefits of a diversified international presence.

Geographic, Economic and Currency challenges: Economic conditions and currency fluctuations posed significant challenges, shaping telco strategies.

- Ooredoo – Oman reported revenue declined of 2.9% YoY in FY-2024, impacted by competitive telecommunications landscape with intensified market activity.

- Bezeq – Israel’s overall revenue decreased by 2.4% YoY in FY-2024. although core revenues grew by 1.3%. The decline can be partly attributed to currency depreciation and decline in roaming revenue impacting its financial performance.

- Ooredoo – Qatar’s revenue declined 2.2% YoY in FY-2024, as 2023 base included revenue from data centres and one-off projects.

- Partner – Israel’s revenue declined by 0.7% YoY in FY-2024, with a 10% drop in cellular service revenues due to reduced interconnection and roaming fees, reflecting the impact of regulatory and economic pressures on its operations.

- Ooredoo-Palestine operations were impacted by the ongoing conflict and foreign exchange fluctuations. However, it delivered a resilient FY-2024 performance.

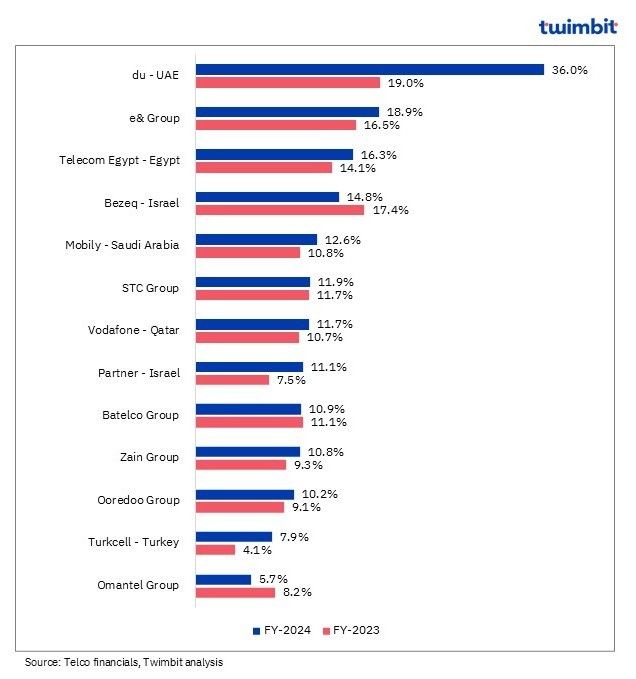

EBITDA analysis of Middle East telcos: FY-2024

Average EBITDA margin increases marginally to ~41% in FY-2024

Nearly 82% of the Middle East telcos reported positive EBITDA growth, with 11 telcos (or about 41% of the total), achieving double-digit growth. This was led by revenue increase, enhanced operational efficiencies, and effective cost control measures. Consequently, this resulted in the average EBITDA margin improving marginally from 40.4% in FY-2023 to 41.3% in FY-2024.

Exhibit 2: EBITDA trends of Middle East telcos, FY-2024

Key highlights

As digital transformation accelerated, telcos navigated a mix of opportunities and challenges, with EBITDA serving as a critical measure of operational success. Strong top-line revenue growth, complemented by strategic cost optimisation initiatives, facilitated EBITDA growth for many Middle East telecom operators.

Data services and digital transformation: The shift towards data services and digital transformation has been a major driver of EBITDA growth, reflecting the region’s digital awakening. Telcos that have invested in high-margin data and digital offerings have seen significant profitability improvements.

- Telecom Egypt achieved a 45.4% YoY growth in EBITDA in FY-2024, driven by robust top-line revenue growth (driven by its strong focus on data services) and cost optimisation efforts.

- du – UAE reported 11.6% YoY growth in EBITDA in FY-2024, likely benefiting from its emphasis on data and digital services, aligning with its revenue performance.

- Turkcell – Turkey’s EBITDA grew 10.2% YoY in FY-2024, with growth in its Techfin segment’s expansion, alongwith increased data consumption (growth of 7.1% YoY), resulting in higher top-line revenue growth.

Cost efficiency and optimisation: Effective cost management has been crucial for maintaining and improving EBITDA, especially in a challenging economic environment. Telcos that have optimized operations have seen improved profitability despite flat or declining revenues.

- Turk -Telecom Turkey reported 30.5% YoY growth in EBITDA owing to lower operating expenses.

- Partner – Israel reported EBITDA growth of 12.8% YoY in FY-2024 despite a slight revenue decline, indicating successful cost reduction strategies, possibly through operational efficiencies.

- Vodafone – Qatar registered 6.1% YoY growth in EBITDA, owing to the continued success of its cost optimisation programme.

Macroeconomic factors and Operational performance: Factors such as low services service and high cost impacted Ooredoo – Oman, whereas Ooredoo- Kuwait’s EBITDA was impacted owing to one-off bad debt provisions in 2024. Factors like foreign exchange fluctuations impacted Ooredoo – Palestine EBITDA. Bezeq-Israel also reported EBITDA decline mainly due to lower telephony revenues resulting from the MOC tariff reduction and the impact of the war on roaming revenues.

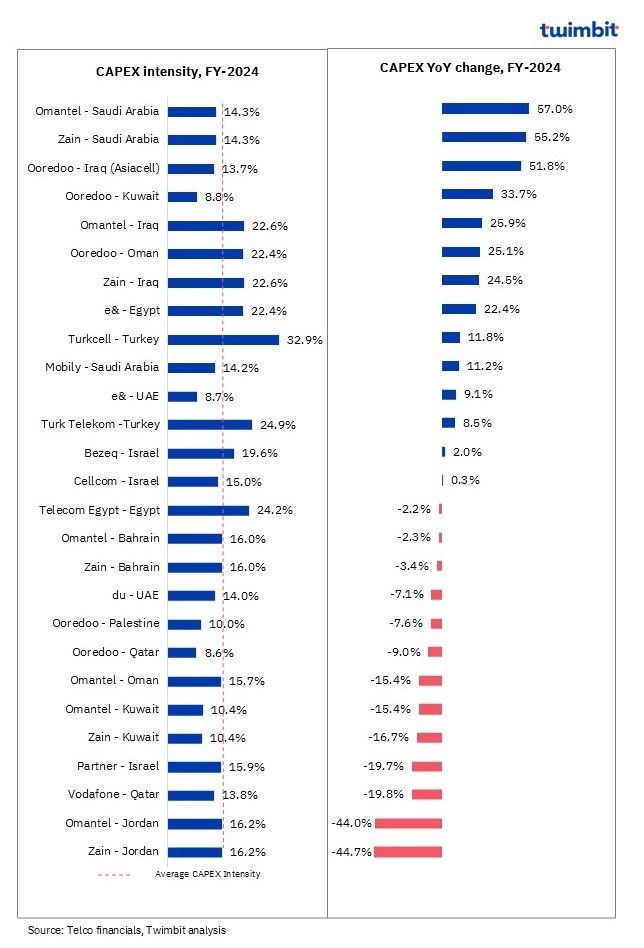

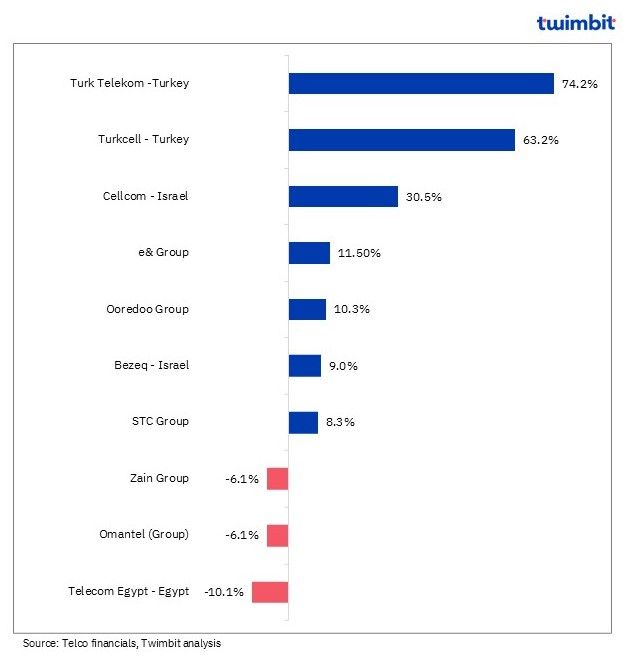

CAPEX analysis of Middle East telcos: FY-2024

CAPEX intensity remained stable at ~17%, as network deployments across select key markets reaches completion

Nearly 52% of the telcos in Middle East reported annual growth in YoY CAPEX spending in FY-2024 as compared to ~56% in FY-2023. CAPEX allocations are projected to stabilise as telcos reach completion of their 4G and 5G network deployments. However, new additional imperatives of growth and efficiency, driven by the relentless march of 5G, fibre, and digital transformation is likely to sustain the CAPEX spending by telcos.

Exhibit 3: CAPEX intensity trends of Middle East telcos, FY-2024

Key highlights

Middle East telcos in FY-2024 showed mixed CAPEX spending pattern, reflecting their strategic priorities. Key CAPEX spending drivers included 5G network investment, fibre infrastructure, and digital services.

5G Network expansion and enhancement: The deployment and enhancement of 5G networks have been a primary driver for CAPEX growth, reflecting the region’s digital ambitions.

- Zain – Saudi Arabia’s CAPEX increased by 55.2% YoY in FY-2024, led by 5G network expansion and core infrastructure modernisation.

- Ooredoo – Iraq reported 51.8% YoY rise in CAPEX in FY-2024, indicating investments for 5G infrastructure and submarine cable deployments.

- Ooredoo – Oman’s CAPEX increased 25.1% YoY in FY-2024, as it expands its 5G footprint and enhancing mobile and fixed connectivity offerings.

- e& – Egypt’s CAPEX grew 22.4% YoY in FY-2024, driven by networks quality and capacity enhancements, to support the growing demand for data services.

Investment in broadband and digital infrastructure: Telcos continue to enhance their infrastructure to support higher data transmission rates and advanced services like FTTH.

- Turkcell -Turkey reported 11.8% YoY increase in CAPEX for FY-2024, as it continued to increase its solar energy, data centre and cloud investments.

- Mobily – Saudi Arabia’s focus on 5G network expansion, investments in IoT, data centres, and submarine cables, resulted in its CAPEX increasing by 11.2% YoY in FY-2024.

- e& – UAE reported 9.1% YoY increase in CAPEX in FY-2024, as it continues to invest in both 5G and FTTH networks, enhancing its digital backbone to meet rising broadband demands.

Prior committed investments and investment normalisation: Telcos have moderated their CAPEX, possibly due to completing initial 5G deployments or shifting focus to optimisation.

- Partner-Israel reported 19.7% YoY declined in CAPEX in FY-2024, owing to lower payments in fixed assets and intangible assets.

- du – UAE’s CAPEX declined 7.1% YoY in FY-2024. However, it continues to invest in 5G densification and indoor coverage, reflecting a strategic shift towards refining rather than expanding its network.

- Telecom Egypt’s CAPEX declined 2.2% YoY in FY-2024, as the telco had accelerated its spending in 2023 to pre-empt potential currency fluctuations and rising interest rates imposed by the Central Bank.

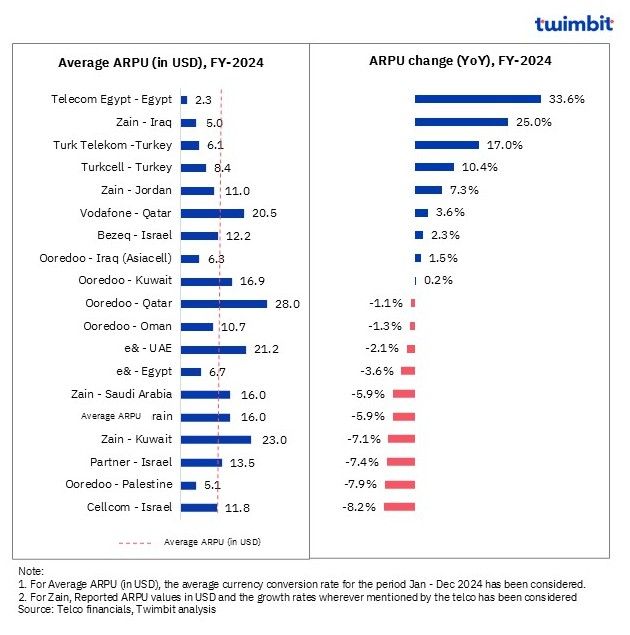

ARPU analysis of Middle East telcos: FY-2024

The average ARPU decline slowed in FY-2024 after experiencing a sharper drop in FY-2023

Nearly 47% of telecom operators in the Middle East reported YoY ARPU growth in FY-2024, facilitated by increased adoption of 4G/5G technologies and strategic price increment in select countries.

However, adverse macroeconomic conditions in geographies like Israel, Palestine, and Egypt exerted a counterbalancing effect on overall ARPU growth. Consequently, the average ARPU declined to USD 12.7 in FY-2024 as compared to USD 12.8 and USD 13.2 in FY-2023 and FY-2022 respectively. Nearly 36% of the 19 telecom operators maintained stable ARPU levels, with YoY change ranging from -3% to 3%.

Exhibit 4: ARPU trends of Middle East telcos, FY-2024

Key highlights

Telcos continue to strategize in maintaining a stable ARPU balance amidst digital transformation and economic shifts. Telcos showed diverse ARPU performance in FY2024, with some achieving strong growth while others faced decline. Key drivers included data service adoption, pricing strategies, and economic factors, with each telco navigating its unique market conditions.

Data services adoption: The insatiable demand for data has been a cornerstone of ARPU growth, reflecting the region’s digital awakening. Telcos that have invested in high-margin data services have seen significant per-user revenue increases.

- Zain – Group’s telcos operations in across multiple countries reported increased data and digital services adoption, translating into strong ARPU growth in emerging markets like Iraq (+25%) and Jordan (+7.3%).

- Telecom Egypt’s strong ARPU growth of 33.6% YoY in FY-2024, driven by surge a surge of 48% in data revenue.

Price adjustments: Price adjustments have been a critical strategy, especially in inflationary environments, directly impacting ARPU.

- Turk Telecom – Turkey registered a 17% YoY increase in ARPU for FY-2024, growth in both prepaid (5.8% YoY) and postpaid ARPU (18.2% YoY), facilitated by a strong focus on higher postpaid plans and varied prepaid tariffs through promotional campaigns.

- Turkcell – Turkey’s ARPU increased 10.4% YoY in FY-2024, owing to price adjustments, upsell efforts and the expansion of its postpaid subscriber base.

- Vodafone – Qatar reported ARPU growth of 3.6% YoY in FY-2024, owing to potential positive impact of the telco revamping its postpaid portfolio by introducing new plans with enhanced features in Q3-2024.

Geopolitical and operational challenges: Challenging geopolitical conditions, currency volatility, and intensified market competition have significantly impacted telcos ARPU.

- Partner – Israel reported 7.4% YoY declined in ARPU in FY-2024, due to lower roaming revenue (impact of the War) and the end of recognition of deferred revenue from Hot Mobile.

- Cellcom – Israel’s ARPU declined 8.2% YoY in FY-2024, due to increased competition and as well as potential macroeconomic challenges.

- Ooredoo – Palestine’s ARPU declined 7.9% YoY in FY-2024, due to ongoing conflict and foreign exchange fluctuations, despite increase in mobile subscribers.

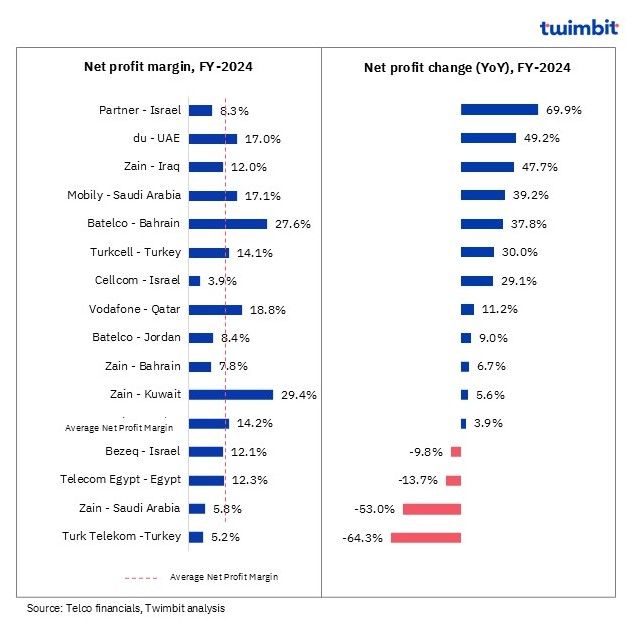

Profitability analysis of Middle East telcos: FY-2024

Increased expenses coupled with macroeconomic factors outpace revenue growth rates impacting the profitability of telcos in Middle East

Among the 16 telcos analysed, 75% reported net profit growth in FY-2024, compared to around 81% in FY-2023. As a result, the average net profit margin declined from 13.6% in FY-2023 to 12.8% in FY-2024, indicating underlying expenses and macroeconomic factors overshadowing the impact of revenue growth.

Exhibit 5: Profitability trends for Middle East telcos, FY-2024

Key highlights

Middle East’s telecom sector is transforming, with profitability driven by operational excellence, digital innovation, and strategic investments, while some telcos face challenges like currency fluctuations and geopolitical risks.

Revenue growth and cost efficiency: For many telcos, profitability in 2024 was propelled by a dual focus on revenue expansion and disciplined cost management.

- du – UAE exemplifies this strategy, with net profit surging by 49.2% YoY in FY-2024, largely attributed to EBITDA performance, interest income improvements, and controlled depreciation costs.

- Mobily – Saudi Arabia net profit grew 39.2% YoY in FY-2024, supported by strong revenue growth and cost efficiencies.

Digital transformation wave: Companies investing in AI-driven network management and customer experience optimisation are reaping financial rewards.

- Vodafone Qatar’s net profit growth of 11.2% YoY in FY-2024, was underpinned by improvements in EBITDA, reflecting efficiencies gained through digital service enhancements.

- STC Group also recorded the highest net profit in its history in Q4-2024. The telcos’ decision to divest assets like TAWAL and the Digital Infrastructure Company, yielded USD 3.4 billion (~ SAR 12.9 billion).

Macroeconomic factors and market dynamics: For telcos operating in volatile economic environments, currency depreciation and inflation have introduced significant financial headwinds.

- Turk Telekom – Turkey reported net profit declined 64.3% YoY in FY-2024, after recording 65.7% effective tax rate, because of inflation accounting and changes in corporate tax legislation, leading to a significant hit on its bottom line.

- Telecom Egypt’s net profit declined 13.7% YoY in FY-2024, due to USD 111.3 million (EGP 4.9 billion) in foreign exchange losses, USD 13.6 million (EGP 0.6 billion) in early retirement compensation and EGP devaluation.

- Bezeq- Israel’s 9.8% YoY net profit decline in FY-2024 was owing to adjustments in roaming revenue due to geopolitical tensions.

ROCE trends of Middle East telcos: FY-2024

ROCE improves for most of the telcos in Middle East in FY-2024, indicating better capital utilisation

- ROCE increased for ~77% of the telcos (including group conglomerates) in FY-2024.

- Growth in revenue alongwith increased profitability (due to a reduction in expenses) resulted in positive ROCE growth for majority of the telcos.

- ROCE for du-UAE increased significantly in FY-2024, owing to relatively higher growth in revenue and finance income, coupled with reduced cost and Federal royalty on regulated revenue resulting in higher “Profit before federal royalty on profit and corporate income tax”.

Exhibit 6: ROCE trends for Middle East telcos, FY-2023 and FY-2024

Total Shareholder Return of Middle East telcos: FY-2024

Majority of telcos in Middle East reported positive Total Shareholder Return (TSR) in FY-2024, indicating better revenue growth and dividend payout

- 70% of the telcos (including group conglomerates) reported positive TSR in FY-2024.

- Increase in Share price alongwith dividend payout facilitated better TSR.

- 90% of the telcos facilitated dividend payout in FY-2024, of which 55% (or 5 telcos) reported positive TSR.

- Exhibit 7: TSR for Middle East telcos, FY-2024

Key strategic developments: Q4-2024

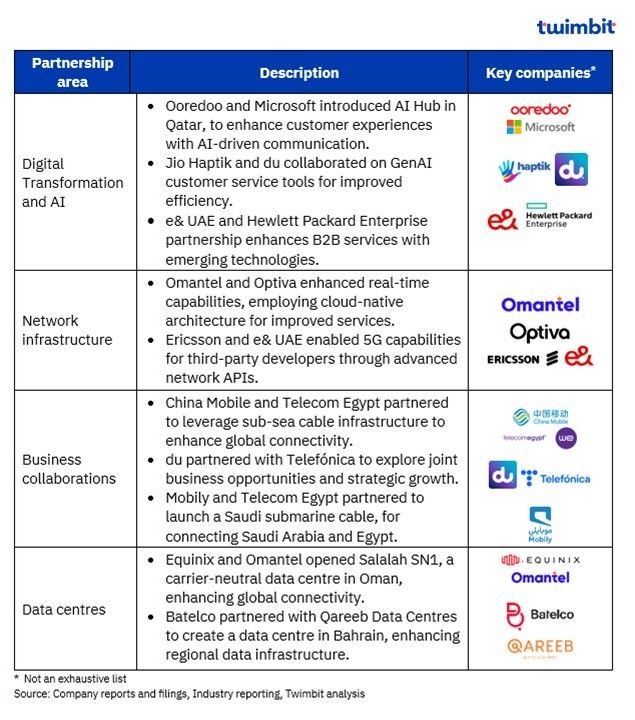

Key strategic partnerships and alliances: Q4-2024

Telcos in the Middle East continue to engage in partnerships to enhance strategic collaborations, advance digital transformation and AI, improve network infrastructure, and develop digital storage facilities, promoting global connectivity and business expansion.

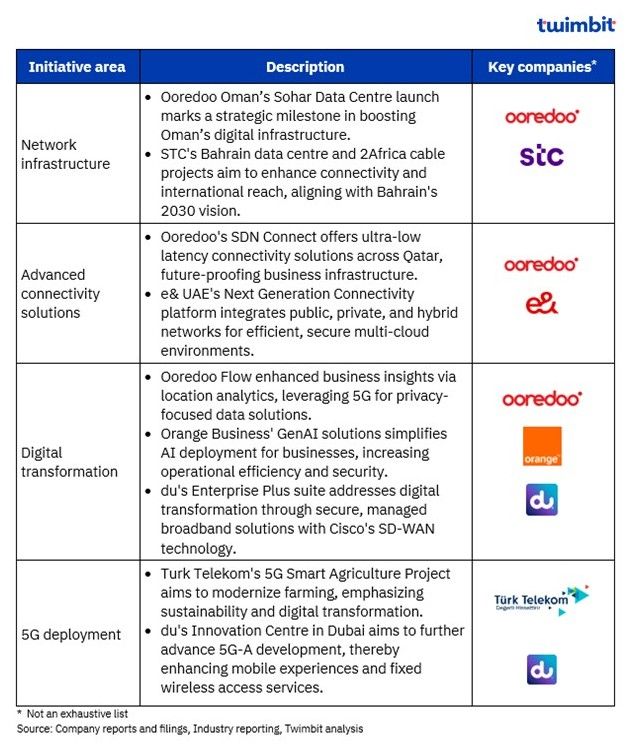

Key strategic initiatives: Q4-2024

The Middle East telecom industry is swiftly advancing with strategic initiatives by telcos aimed at enhancing telecommunications through 5G deployment, digital transformation, network infrastructure, connectivity innovation, and AI-driven solutions, reflecting significant global technological progress and investment.

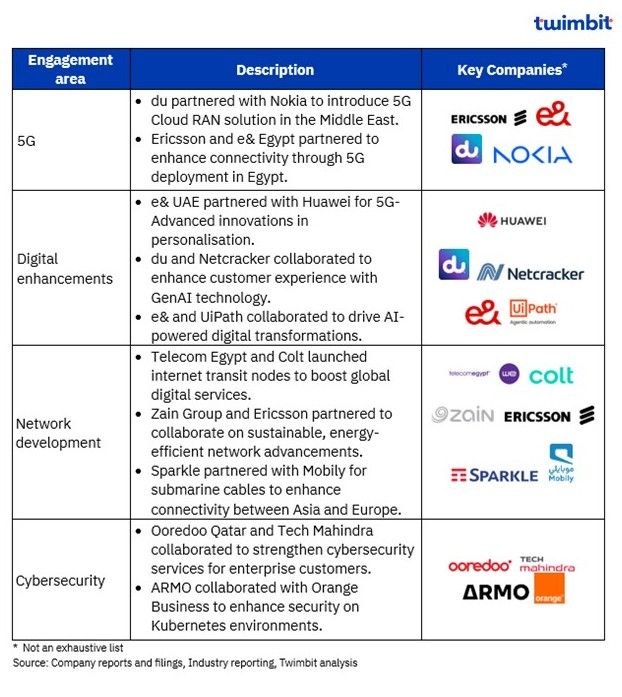

Key contract wins: Q4-2024

Leading telcos in the Middle East region have established significant collaborations, enhancing their influence in 5G deployment, digital transformation, network infrastructure, and cloud services. These alliances are driving technological innovation and progress across the region, positioning them as key players in the telecommunications sector.

Research Methodology and Assumptions

- The “Middle East Telcos Performance Benchmarks: Winter 2025” report offers crucial insights into the performance of telecom companies. It analyses key financial indicators such as Revenues, EBITDA, CAPEX, ARPU, Net Profit, ROCE and TSR for the period January – December 2024.

- This report leverages data collected from telecom firms and extensive secondary research. Twimbit follows a calendar year for its data analysis, with FY representing January to December.

- To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate, reflecting the average USD exchange rate for January – December 2024.

- The report evaluates Revenue and EBITDA for 33 and 27 telecom companies, respectively. CAPEX and ARPU analyses cover data from 27 and 19 companies, respectively. Net profitability assessment is based on data from 16 telecom firms. ROCE and TSR assessment are based on 14 and 10 telcos respectively.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.