Small Finance Banks (SFBs) are uniquely positioned to extend formal financial services to India’s unbanked population—an estimated 190 million individuals, primarily across rural and semi-urban regions. With 95% of their branch networks in underserved areas, SFBs play a crucial role in advancing financial inclusion by offering credit, savings, and insurance products tailored to low-income households, small businesses, and farmers.

Their core mandate, financing micro-enterprises and priority sectors, facilitates job creation, stabilizes rural economies, and reduces regional disparities. This strategic allocation of capital strengthens community-level financial resilience and supports broader objectives of sustainable, inclusive growth.

As Small Finance Banks (SFBs) continue to scale, their role in India’s financial architecture is shifting from mere access enablers to pivotal system-level contributors, supporting grassroots development and driving long-term economic transformation through enhanced financial inclusion and digital growth.

Exploring growth opportunities for SFBs in India

SFBs can tap underserved rural and semi-urban markets with customized financial products, driving financial inclusion.

Source: Twimbit analysis, IBEF 2024 , PWC, Annual reports

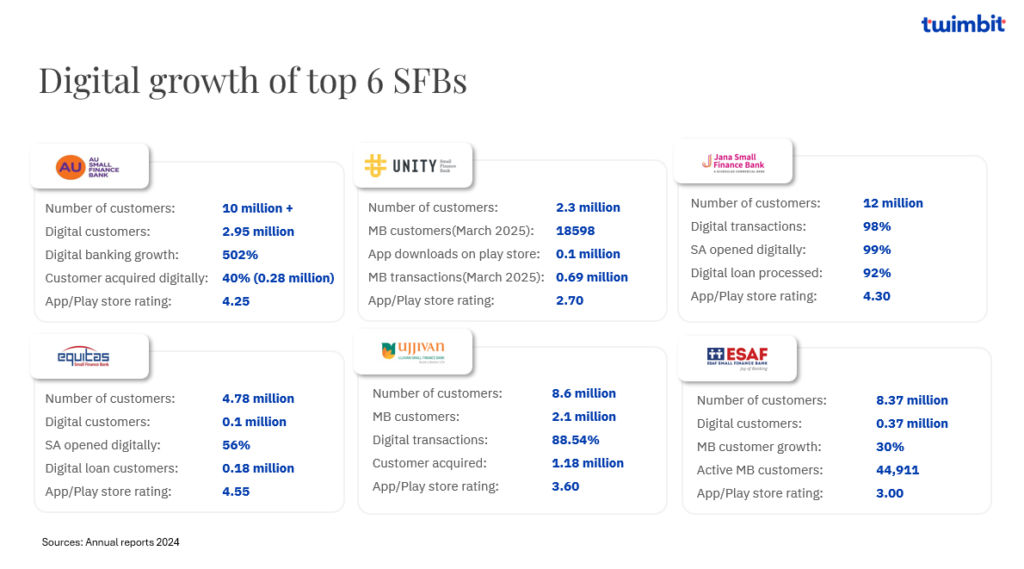

Digital growth of top 6 SFBs

The digital growth of SFBs is being driven by increased adoption of mobile banking, digital wallets, and UPI integration, enabling wider customer outreach at lower costs.

Source: Twimbit analysis, Annual reports

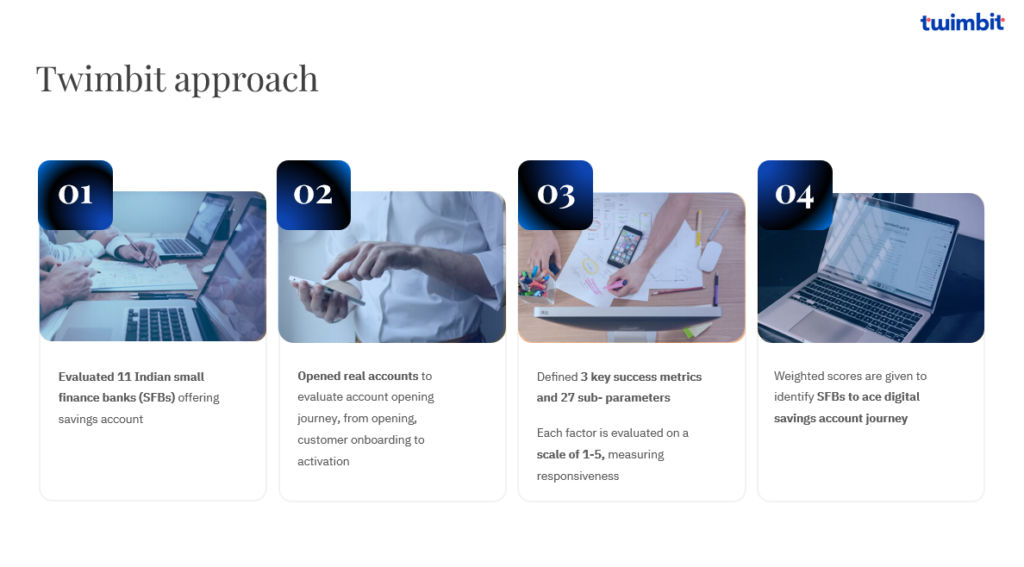

Twimbit methodology

Source: Twimbit analysis

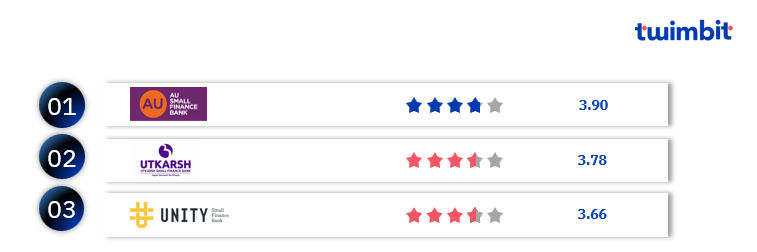

Top SFBs to ace digital savings account journey

Here are the top 3 Small Finance Banks (SFBs) in India that are leading the way in the digital savings account journey:

Source: Twimbit analysis

Find out the top 10 SFBs to ace digital savings account journey in our report.

- #1 Mobile app experience

The mobile app experience comprises an assessment of three sub-parameters to gauge the app’s user-friendliness and effectiveness.

| Mobile app experience |

| Mobile application availability and capabilities |

| App activation convenience |

| App security and Privacy |

AU Small Finance Bank topped the chart in this parameter, with its top best practices being:

- Cross-selling integration: Including CTAs for other banking products during onboarding capitalizes on high user engagement moments and can improve customer lifetime value.

- Minimal steps: Limiting registration to just 2 steps follows mobile-first design principles where customers expect quick, streamlined experiences.

- Time efficiency: The sub-2-minute registration target aligns with customer attention spans and competitive benchmarks in fintech apps.

- Dual authentication options: Offer both PIN and biometric authentication to accommodate customer preferences and device capabilities.

- Registration-integrated setup: Allowing biometric setup immediately eliminates extra steps later and improves customer adoption of stronger authentication methods.

- #2 Application process experience

The application process experience comprises an assessment of three sub-parameters to gauge how user-friendly, informative, and efficient a bank’s process is for onboarding new customers.

| Application process experience |

| Discovery Journey |

| Clarity of products or services |

| Ease of account opening |

AU Small Finance Bank topped the chart in this parameter, with its top best practices being:

- Personalized engagement: Welcome greetings, upfront offers, and “Apply now” CTAs drive immediate user action with tailored experiences.

- Streamlined application: Simple product descriptions, clear fees/terms, comparison tools, and 4-click form completion with comprehensive document collection (Aadhar, PAN, selfie, signature).

- Efficient verification: Video KYC integration eliminates branch visits and accelerates account opening while maintaining regulatory compliance.

- #3 Onboarding experience

The onboarding experience comprises an assessment of 1 sub-parameter to gauge how easy and efficient a bank’s process is for account activation.

| Onboarding experience |

| Activation convenience |

Both Unity and Utkarsh Small Finance banks topped the chart in this parameter, with their top best practices being:

- Minimal-step activation: Both banks require 7-8 steps for account activation, indicating less steps required to activate account than are industry standard.

- Instant activation: Both Unity and Utkarsh banks offer instant account activation, showing efficient backend processing.

To gain detailed insights on the digital savings account customer journey for the top 10 small finance banks

As SFBs across India embrace digital transformation and revolutionize mobile banking experiences, the significance of today’s technological evolution in financial services has never been more evident, with institutions striving to meet the dynamic expectations of India’s rapidly growing digital-first customer base.

Through our report, we explore the transformative landscape of India’s SFB sector.

Discover how these agile institutions are pioneering innovative app solutions and customer-centric digital experiences that will define the future of inclusive banking across the diverse Indian market.