Company insights

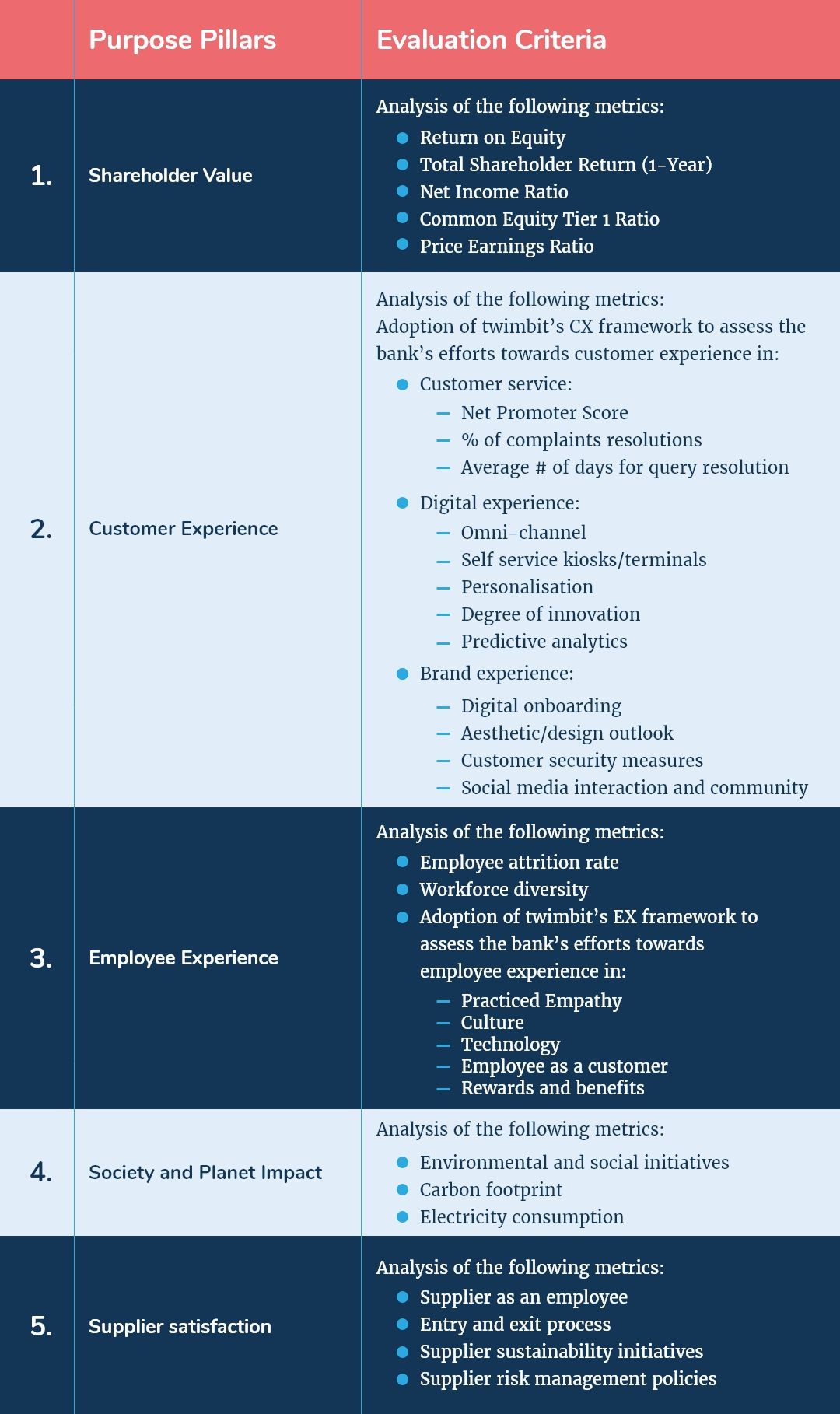

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

ANZ Banking Group (Group financials) – An overview as of 30th September 2020

| Bank name | Australia and New Zealand (ANZ) Banking Group |

| Headquarters | Melbourne, Australia |

| Operating income (30th September 2020) | USD 13.5 billion |

| Net Profit after Tax (30th September 2020) | USD 2.7 billion |

| Total Assets | USD 793.3 billion |

| Employees | 39,060 |

| Countries in Operation | 34 countries |

| Number of Branches | 1200 |

| Information and Communication Technology (ICT) Spend (30th September 2020) | USD 1.4 billion |

| Bank ranking in a particular country | 1st in Australia* |

| Number of customers (retail, business and Institutional) | 8.7 million |

| Market capitalisation (30th September 2020) | USD 37.2 billion |

| Operating Revenue CAGR growth (2016-2020) | -2.9% |

Shareholder value (30th September 2020)

| Return on Equity (30th September 2020) | 6.2% |

| Total Shareholder Return (1-Year) | -36.90% |

| Net Income Ratio | 20.15% |

| Common Equity Tier 1 Ratio | 11.3% |

| Price Earnings Ratio (30th September 2020) | 20.09% |

Awards

| 2020 | Global Finance Best Treasury & Cash Management Providers Awards 2020 – Best Trade Finance Provider in Australia & New Zealand 2020 – World’s Best Bank for Structured Trade Finance 2020 No.1 ranking for relationship strength and overall market-and-lead-bank penetration. No.11 domestic and offshore transactional bank in Australia and New Zealand No.11 for AUD-NZD Bank-to-Bank services and banking partner of choice in the Asia Pacific |

ANZ Banking Group and its strategic focus areas

- Customer experience

The bank is implementing digital banking solutions designed to improve financial well-being and protect customers from cyberattacks by:

- Measuring a customer’s experience through the strategic Net Promoter Score (NPS). Customers rate their likelihood to recommend ANZ bank on a 0–10 scale, and the score calculation happens by subtracting the detractor percentage from the promoter percentage.

- Enhancing customers’ financial well-being through customer contact programs.

- Delivering customer experience through a flexible and resilient digital infrastructure that enables customers to stay on top of their day-to-day banking through the ANZ app.

- Helping customers to create transition plans for climate risks and opportunities and report them publicly on ANZ bank’s channels or other public platforms.

Initiatives taken by ANZ bank to enhance the customer experience in 2019-2020:

- Rolled out several new self-service features to the ANZ App, including the ability to open new accounts, activate a card, set or change a card’s PIN and temporarily block or unblock a card to protect an account from theft and fraud.

- Invested heavily to open digital branches and providing customers with new self-service options, including smart (deposit-taking) ATMs and business cash deposit machines.

- Employee experience

The bank aims to build a safe, diverse, and inclusive workplace that encourages engagement, collaboration, and development. Furthermore, it aims to create competitive remuneration and benefits, effective performance management and recognition for employees by:

- Organising training and development programs to up-skill and re-skill employees across all regions (by providing almost 970,000 hours of training) to build a resilient, adaptable, and inclusive workforce with a strong sense of purpose and ethics.

- Bringing diversity into the workforce to drive innovation. This move brings a diverse set of experiences, perspectives, and backgrounds which is key to innovation and the development of new ideas.

Initiatives taken by ANZ bank to enhance capabilities and promote a healthy work environment 2019-2020:

- The ‘Speak up’ culture: To create a healthy and supportive environment for employees to share their ideas, opinions, and concerns. The strong speak-up culture has helped ANZ in uplifting its internal engagement score by 5% from 2019 to 2020.

- Workforce capability building: A social learning platform, providing free access to ANZ bank employees to learn from internal subject matter experts, external content providers, and user-generated content.

- Integrating data-analytical talent: A focus on investing in data and engineering talent with new roles and development opportunities in data analysis and science.

- Employee Assistance Program (EAP): The EAP provides confidential, free counselling and guidance for work and personal problems and includes online resources covering topics such as managing stress, mindfulness and relaxation.

- Product innovation

ANZ bank focuses on delivering improved customer outcomes by rationalising products and services, developing new and compelling services, and introducing fresh initiatives to enhance its homeowner and small business owner propositions. The bank is creating an integrated trade, cash and markets experience within its institutional business by:

- Simplifying and digitalising products and services for better convenience to the customer during and post-pandemic

- Extending analysis of flood-related risks to incorporate bushfire and other risks related to retail customers

- Showing financial resilience of home loan customers with flood risks by test-piloting socio-economic indicators

Initiatives taken by ANZ bank in 2019-2020 for product and service innovation:

- Launched ANZ Online Business Lending, a platform that provides conditional approval for up to USD 150,000 in unsecured lending within 20 minutes and access to funds within four days

- Simplified business by introducing a targeted approach in the Financial Advice business to focus on affluent and high net-worth clients

- Society and planet impact

The new environmental footprint target suite for ANZ Bank commenced on 1 July 2020 and will run until 30 June 2025. The bank’s focus remains on energy, water and waste due to its relevance to the people, customers and the markets in which it operates.

The bank has set targets to reduce the direct impact of its business activities on the environment by:

- Reducing Scope 1 and Scope 2 emissions by 24% in 2025 and 35% in 2030

- Increasing renewable electricity use to 100% by 2025

- Reducing potable water consumption by 25% in 2025

- Reducing waste to landfill by 30% in 2025

- Reducing paper consumption (office and customer paper use only) by 60% in 2025

Digital Strategy

The bank focuses on simplifying and digitalising the overall banking processes for better convenience to its customer and employees.

Initiatives taken by ANZ bank to support its digital strategy in 2019-2020 include:

- The launch of the ‘set a savings goal’ feature in the ANZ App to help customers better manage their money and develop savings habits:

- Customers receive personalised in-app notifications, encouraging them to set a goal, stay on track and celebrate milestones along the way

- One in 10 active app users must set a goal using the new feature in 2020

- The bank introduced several new self-service features within ANZ goMoney and internet banking, including fixed-rate rollovers:

- Customers with a fixed-term home loan or a flexi home loan can now request a personalised rate for their loan facility and term (based on the current market rates)

- One-third of all home loan fixed-rate requests can go digital

- The bank aided farmers in their decision-making through proprietary digital tools, including dairy and red meat dashboards, as well as a geospatial tool that analyses weather, soil, and contour data

- Data and digital initiatives include the launch of electronic verification and the use of data to identify customers who may be experiencing hardship

IT Strategy

- The bank is investing heavily in cybersecurity to be in a solid position to keep its systems, data, and customers safe from the increasing sophistication of cyberattacks.

- Technology expenses increased to USD 220 million (19%) mainly because of an accelerated amortisation of USD 150 million

- The increased expenses were due to a change in the software amortisation policy, a change in the accounting treatment associated with the new leasing standard (comparatives not restated), an increase in the investment spend and customer remediation (USD 10 million)

ANZ Banking Group and its ICT contracts

- ANZ Bank renewed its contract with Optus and Singtel. The agreement will see Optus and Singtel provide domestic data and international data network services, mobility, collaboration, contact centre services, and managed services for the bank.

- Knosys has signed a contract worth USD 640,000 with ANZ Bank New Zealand to provide software services to the bank, as part of the bank’s efforts to comply with the Reserve Bank of New Zealand (RBNZ) regulations.

9 Growth and Innovation Opportunities

- #1 Cost to serve

- The cost to income ratio for ANZ is 53.7% which is exceptionally high compared to its Asia Pacific competitors. The bank should maintain an average cost-to-income ratio in the range of 40% – 43% to achieve strong bottom-line growth.

- Currently, staff cost is USD 3.8 billion, accounting for 52% of the total expenses and 28% of total revenue. This cost increased by 2% from 2019 to 2020, arising from wage inflation, headcount growth, retail and commercial division as well as customer remediation.

- The bank spent USD 62.5 million in customer remediation processes involving manual customer documentation management, verification, and onboarding.

- There is an opportunity for the bank to reduce these cost buckets substantially by:

- Removing duplication of tasks, roles, and functions by using blockchain, robotic process automation and quantum computing

- Replacing man-hours with cognitive process automation of routine and daily back-end tasks

- Adopting a holistic cloud implementation strategy that centralises business as usual activities and eliminates data centre management

- Digitising customers’ personal information screening and creating a distributed ledger to secure information transfer with an auto-generated audit trail using AI and blockchain technologies

- Automating functions and processes that are currently human-intensive, such as branch relationship management, cashier, and customer grievances

- #2 Transformation of the branch and its branch network

- ANZ bank has a branch network of 1200 branches and over 4000 ATMs across 34 countries. To maintain and run this branch network, the bank spends USD 615 million on its premises. This cost has decreased by 1% since 2019 due to a change in the accounting structure for international lease payments. However, the premises cost is still 4.5% of its operating revenue, creating an opportunity for the bank to reduce the underutilised and underperforming branches in the international and home regions.

- The bank should focus on transforming branches with high business volume and customer headcount into flagship digitalised community hubs that enrich the in-branch experience and redefine customer engagement. To achieve this, the bank should:

- Integrate augmented reality (AR) and virtual reality (VR) to create a virtual branch experience using AR/VR tools for remote support services

- Deploy smart robots in-branch to handle daily queries

- Create self-service kiosks to minimise customer waiting time

- Set-up lounge rooms for networking and community building

- #3 Customer experience

- Automation of the home loan process: ANZ bank takes 23 business days to complete a home loan process, which is 7-8 days longer than the average time taken by its regional peers. To reduce the home loan processing time, the bank should:

- Identify customer journey inflexion points for interest in buying a home to pre-empt loan requirements and create a preliminary digital document kit

- Reduce paper-intensive documentation and bottlenecks for approvals through a digital identity recognition and credit assessment program

- Allow customers to apply and access home loan application through the bank’s proprietary app

- Support the customers with in-app virtual assistants for any immediate queries and updates on the application

- Omnichannel experience: The bank has a multichannel presence since it provides various touchpoints to consumers, including bank branches, mobile banking, ATMs, and contact centres in 34 countries. There is an opportunity to build an omnichannel experience across physical and digital domains for a seamless customer experience across all channels. This move will give ANZ a distinct competitive advantage compared to the many other neobanks.

- #4 Employee experience and productivity

- The bank has an employee engagement score of 86%, which is comparatively higher than other operating banks in Australia. Apart from the employee engagement score, the bank should focus on people analytics. Directed focus on people analytics is vital is to check on the unconscious bias that may unfairly impact promotion and compensation decisions.

- 94% of employees stated that the bank supported them during the Covid-19 pandemic with guidance on work-life balance and resources that emphasise the importance of family and work relationships. The bank also launched HealthyMe Digital for expert well-being and psychological information:

- The bank should continue this effort even when the employees are in the recovery phase of the pandemic.

- It should build hybrid-working models that encourage flexibility in working-from-home and in-office, including onboarding and training.

- ANZ can create a monthly piggy bank for its employee to give away the subscriptions and memberships to Netflix, Spotify, and online gyms, among others, to manage entertainment and wellness at home.

- #5 Migration of workload to the cloud

- ANZ Bank has a narrow scope with its cloud strategy that involves only an internal engine assisting app migrations to the cloud infrastructure. The bank should formulate a holistic cloud adoption strategy, allowing them to take on more workload, with the potential for swift uptake. This step will help the bank achieve cost efficiencies and significant modernisations, such as:

- Decreasing data storage costs by reducing the capital expenditure on its in-house physical storage infrastructure

- Creating a robust, tightly-controlled delivery program that allows developers to scale and embed microservices in the cloud architecture

- A quick response to market shifts such as black swan events – Covid-19 and entry of multiple neobanks with the new APRA ADI licensing process

- Incorporating backup and redundancy capabilities to address security and compliance concerns

- #6 Neo banking

- The bank’s customer base is 40% lesser than other top operating banks in Australia. ANZ should focus on increasing and retaining its customer base in the millennial and Gen Z segment that is growing at a rate of 4% year-on-year.

- Rather than creating a separate brand identity for the next-gen population, ANZ bank can exercise these two options:

- Consider an upcoming popular neobank in the market for consolidation, such as the example by National Australia Bank and its acquisition of 86 400 Holdings Ltd

- Reimagine their existing digital propositions to resonate with this customer segment, bringing together gamification elements, convenience, and frictionless banking.

- #7 Artificial Intelligence (AI) in everything

- Using AI and machine learning can help ANZ bank to reduce the lengthy home loan process by:

- Integrating the national database with the bank’s customer data and learn about unique customer personal information for its home loan application process

- Mimicking live employees through chatbots and voice assistants to help customers understand the home loan application process, eligibility of loan amount, collateral management, and sanction timelines

- ANZ bank should also invest in consumer behaviour analytics to identify preferences and deliver timely and compelling offers. This move will help the bank to add revenue from non-interest income sources through third-party integration.

- To achieve deeper insights on customer behaviours, the bank must set up a robust open architecture following the Consumer Data Right (CDR) that enables the bank to create personalised products and services using AI on third-party data

- Apply cognitive process automation to self-initiate a set of tasks that improvises upon its previous iterations, such as monthly bill payments, changing subscription plans based on best offers, alerts for stock updates, etc. This mechanism will, in turn, help customers improve their existing lifestyle choices and optimise their monthly bills.

- The bank can implement AI within middle-office functions to detect and prevent payment frauds, improve processes for anti-money laundering (AML), and combat the financing of terrorism (CFT).

- #8 Cybersecurity

The bank’s effort toward cybersecurity enhances preventive, detective, and responsive capabilities to manage advanced cyber threats. It currently has a threat intelligence mechanism and a 24/7 security operations centre. The centre analyses millions of data events every day to contain cyber threats. To ensure a future-proof cybersecurity strategy, ANZ bank can adopt the following measures:

- Experiment with its hypothesis generation using advanced AI tools to assess cyber threats and identify recommended mitigation strategies

- Monitor the existing security framework to identify any misconfiguration in firewalls, proxies, and data loss prevention tools.

- #9 Society and planet contribution

- The bank has the highest carbon emission (ktCo2e) of 203.7-kilo tonnes and electricity consumption of 180,340 MWh, i.e., approximately 370% and 462% higher than the average of other operating banks in Australia, respectively.

- The bank should reduce 50% of its carbon emission and 60% of the current electricity consumption by:

- Adopting renewable sources of electricity (solar powerplants and windmills) inbranch operations

- Using eco-charges, smart sockets, programmable thermostats, and indoor motion sensors to reduce electricity consumption

- Shifting toward green products such as virtual cards, pulper cards, eco ink, and carbon control press machines will help ANZ bank reduce the direct impact of its business activities on the environment.

- Minimising the amount of paper and plastic waste within the branches and instituting the ‘3R’ policy of reducing, reusing, and recycling for waste management.

- Ban plastic use within office premises

- Use of own cups, bottles, and cutlery

- Recycle water in washrooms and pantry

- Reduction in paper used for documentation

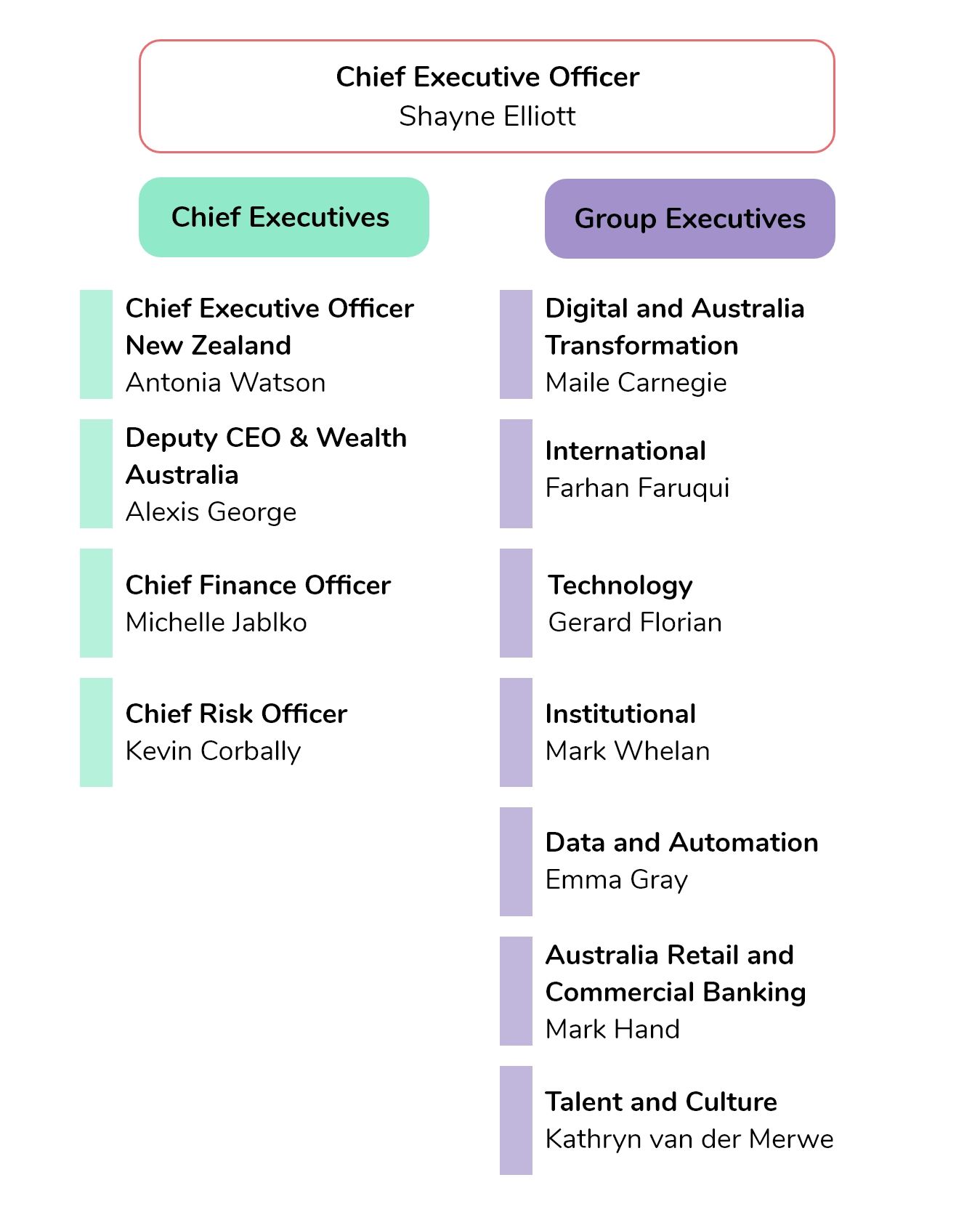

Organisation structure: Leadership

Executive profile

Shayne Elliott

Chief Executive Officer

Shayne Elliott was appointed as the Chief Executive Officer of Australia and New Zealand Banking Group Limited (ANZ) on 1 January 2016. He joined ANZ as the CEO of Institutional Banking in June 2009 and thereafter appointed as its Chief Financial Officer in 2012.

Elliott holds the experience of more than 30 years in international banking, covering Australia, New Zealand, the USA, UK, Asia Pacific, and the Middle East. Before joining ANZ, Shayne held senior executive roles, including that as Chief Operating Officer at EFG Hermes, the biggest investment bank in the Middle East. Elliott started his career with Citibank New Zealand and worked with Citigroup for 20 years, holding various senior positions across Egypt, Australia, the UK, the USA, and Hong Kong.

Quote

- Technology advancement, Itnews – 31st October 2019

There’s going to be a shift in the way we spend our money, and more and more of it’s going to be on technology.

Kevin Corbally

Chief Risk Officer

Kevin Corbally is responsible for the ANZ Group’s Risk Management, overseeing global Credit, Market and Operational Risk as well as Compliance teams, risk-related strategies, policies, and processes.

He has held several other senior roles at ANZ since joining in 2009, including those of Head of Institutional Relationship Banking Australia and Head of Diversified Industrials.

Before joining ANZ, Corbally was the Managing Director, Head of Corporate and Commercial Banking, Australia & New Zealand at Citibank, and worked at Deutsche Bank. He began his career at PricewaterhouseCoopers.

Corbally holds a Bachelor of Commerce (Honours) from University College Galway, Ireland, a Master of Applied Finance from Macquarie University and a Graduate Diploma in Professional Accounting from University College Dublin, Ireland. He is a Fellow of the Institute of Chartered Accountants in Ireland and also a Fellow of the Financial Services Institute of Australasia.

Quote

- Risk management, Annual report 2019 – 2020

The strength and adaptability of the bank’s risk function have played a key role in helping navigate the organisation through the current changing environment.

Gerard Florian

Group Executive, Technology

Gerard Florian has been Group Executive Technology at ANZ since January 2017.

He is responsible for defining the bank’s technology strategy, as well as building and managing its technology infrastructure. Responsibilities include overseeing the development of new technologies, implementing existing technologies to help the bank reach its strategic goals, and creating systems and processes to make the best use of resources.

Florian has worked in technology for more than three decades. He was previously Chief Strategy Officer for the Global Cloud Business Unit at Dimension Data, where he was instrumental in establishing a portfolio of cloud-enabled managed services operating on a global platform. Prior to that, Florian was Chief Technology Officer and Chief Marketing Officer for the Australian division of Dimension Data. He has also been a member of the Technology and Digital Business Advisory Panel for ANZ since its initiation in 2015.

Michelle Jablko

Chief Financial Officer

Michelle Jablko joined ANZ as Chief Financial Officer on 18 July 2016.

Before ANZ, Jablko served a 15-year stint in investment banking, working across different industries, including financial services, as well as an advisory role for Australian companies on strategy, capital management and funding, and investor relations.

Most recently, Jablko was at Greenhill Australia, where she was its Managing Director and Co-Head. She was jointly responsible for leading its Australian business. She spent almost 15 years at UBS, Australia.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiencies align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them:

Endnotes

Australia and New Zealand (ANZ) Banking Group, (2020, September 30). 2020 Annual Report.

https://www.anz.com/shareholder/centre/reporting/annual-report-annual-review/

Australia and New Zealand (ANZ) Banking Group, (2020, September 30). 2020 Annual Review.

https://www.anz.com/shareholder/centre/reporting/annual-report-annual-review/

Australia and New Zealand (ANZ) Banking Group, (2020, September 30). 2020 ESG Report.

https://www.anz.com/shareholder/centre/reporting/annual-report-annual-review/

Australia and New Zealand (ANZ) Banking Group, (2020, September 30). Awards and recognition.

https://www.anz.com/corporate/our-expertise/awards-recognition/

Statista, (2020, September 2). Largest banks in Australia in financial year 2019, by assets.

https://www.statista.com/statistics/434596/leading-banks-in-australia-assets/

Sourav Kumar, Research Intern, contributed to the research in conducting preliminary literature review, creating infographics, and conceptualising the article.