Company Insights

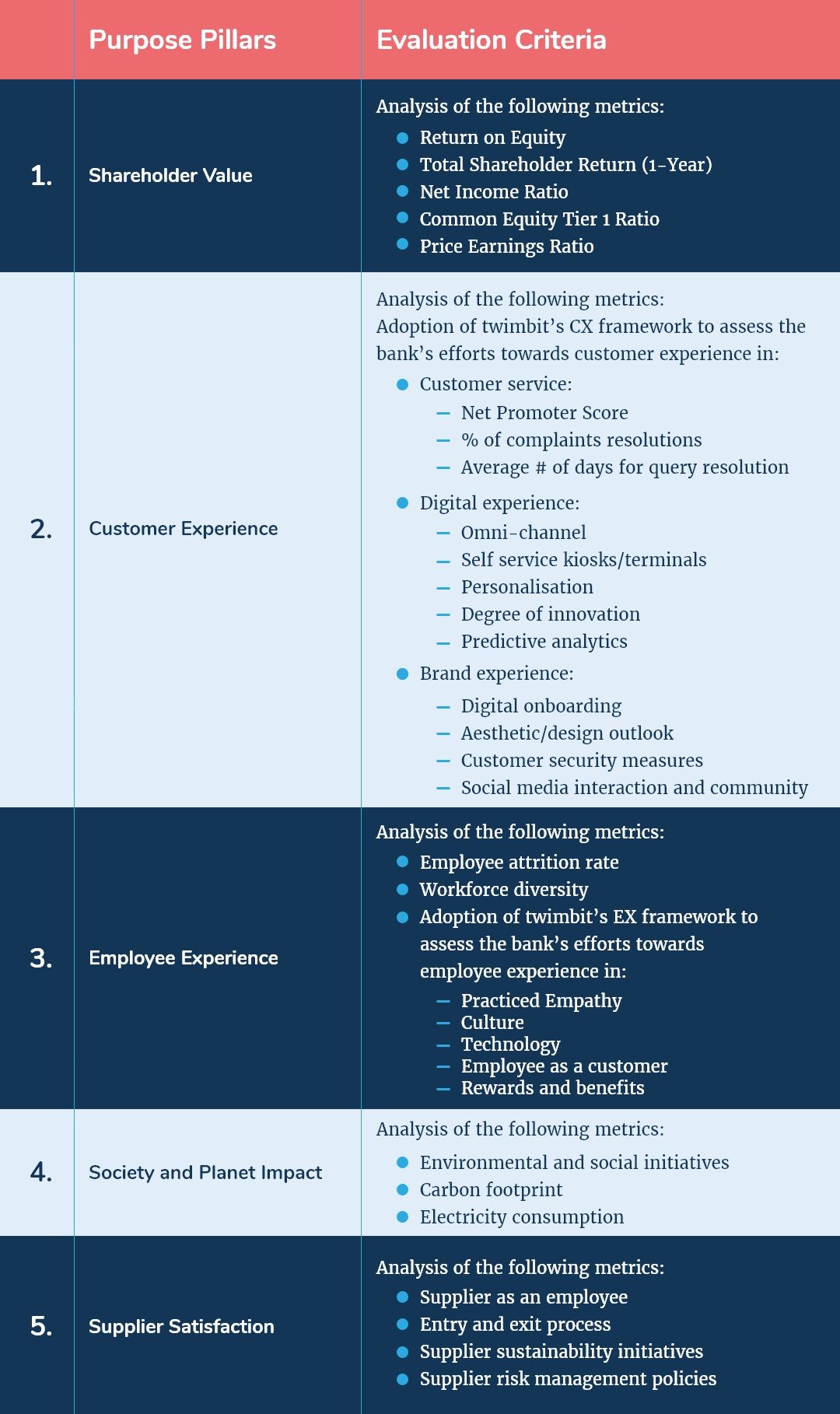

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Commonwealth Bank (Group financials) – An overview as of 30th June 2020

| Bank name | The Commonwealth Bank of Australia (CBA) |

| Headquarters | Sydney, Australia |

| Operating Income (30th June 2020) | USD 18 billion |

| Net Profit after Tax (30th June 2020) | USD 5.6 billion |

| Total Assets | USD 772 billion |

| Employees | 41,778 |

| Countries in Operation | 10 |

| Number of Branches | 1,118 |

| Information and Communication Technology (ICT) Spend (30th June 2020) | USD 1.4 billion |

| Bank Ranking in Particular Country | 2nd in Australia |

| Number of Customers (Retail, SME, Wholesale, and Wealth) | 17 million |

| Market Capitalization (30th June 2020) | USD 119 billion |

| Operating Revenue CAGR growth (2016-2020) | -0.82% |

Conversion Rate: 1 AUD= 0.69 USD

Shareholder value (30th June 2020)

| Return on Equity (30th June 2020) | 10.3% |

| Total Shareholder Return (1-Year) | -11% |

| Net Income Ratio | 31.39% |

| Common Equity Tier 1 Ratio | 11.6% |

| Price Earnings Ratio (30th June 2020) | 19.86% |

Awards

| 2020 | Wins Celent Model Bank 2020 Award for Customer EngagementWins ‘Bank of the Year’ in Mortgage Professional Australia 2020 Brokers on Banks Awards |

| 2019 | BAI Global Innovation Award for innovation in customer experience |

Commonwealth Bank and its strategic focus areas

The strategic priorities of Commonwealth Bank include retaining their position in retail and business banking, along with strengthening themselves as a digital bank.

- Customer experience

- Simplifying business: Aiming to reduce risk, cost, and complexity by focusing on core businesses

- Leading in business and retail banking: Investing in top customer service, distribution channels, technology, and operational performances

- Exceptional digital performance: Spending in customer-facing and back-end technology to deliver easy-to-use, personalised, value-added, and secure digital banking services for customers

Retail banking initiatives taken by Commonwealth Bank in 2020:

- Providing continuous additional support for retail banking customers under COVID-19 with 800% increase in calls to the financial assistance line and 154,000 home loans deferred

- Working with Home-in to provide customers with a simplified digital home-buying experience

- Creating simpler and effective processes for customers and their own business. For instance, invested in PEXA, which digitalises home loan settlements

- The signing device provided by Bankwest allows customers to sign their home loan contracts digitally. Bankwest is also innovating a digital portal and tools for brokers to allow real-time tracking of client’s applications.

Business banking initiatives taken by Commonwealth Bank in 2020:

- Investing in service, data, and technology with the aim to become Australia’s leading business bank

- Helping small businesses access their data through Vonto, an app that provides straightforward and actionable insights to small businesses. The aim is to optimise businesses.

- Streamlining and digitalising the process of providing secured and unsecured loans to businesses. Providing existing customers with same-day lending decisions through BizExpress for unsecured loans up to AU$250,000 and secured loans up to AU$1 million

- Launches ‘CommSec Pocket’ (an investing app for people who are new to the share market and want a simpler experience) to provide a new way to invest.

- Employee experience

- Employee engagement: The bank aims to work on their employee engagement index score by the Your Voice people and culture survey, and ultimately be a part of the global top 10% threshold

- Women in leadership: Targets to include 47-50% women in executive manager and higher-level roles by 2025

- Reskilling and upskilling people: Piloting opportunities to help its people be prepared for the future of work. The bank is engaging with educators, the government, and the community to inculcate changes in the workforce plan

Initiatives taken by Commonwealth Bank in 2020 to strengthen their employee experience:

- According to the Your Voice people and culture survey, the bank’s employee engagement is at 81%, which is 13% higher than its 2019 score.

- The bank achieved 41% in positions held by women in executive managerial roles and above.

- Society and planet impact

- Commitment to education: The bank has a longstanding commitment to financial education. The aim is to help the next generation make smarter financial decisions through school banking and Start Smart programs.

- Tackling financial abuse: Commonwealth Bank continues to invest in programs that support customers, employees and members of the community affected by financial abuse in domestic and family violence backgrounds

- Approach to climate change: The bank is committed to playing their part in limiting climate change. This is in line with goals of the Paris Agreement and supports the responsible goal transition to net zero emissions by 2050. The bank consumed 100% in renewable energy for its Australian operations.

Initiatives taken by the Commonwealth Bank in 2020 to strengthen their contribution towards the society and planet:

- Start Smart Digital: A financial education initiative, which was shifted online in 2020, owing to COVID-19. More than 11,000 students have participated in the online learning sessions.

- Community and Customer vulnerability: Trained frontline branch staff to give support to customers who were victims of financial abuse.

- Green mortgage initiative: To help customers benefit from more sustainable energy, the bank ran a pilot program that offered AU$ 500 cashbacks to retail customers who installed a certified solar PV system of 5 Kilowatts or greater.

- Incentivising the transition to a low carbon economy: Provided AU$150 million in debt funding to Queensland Airports Limited for the Gold Coast Airport redevelopment, with AU$ 75 million provided via a sustainability-linked loan.

Digital Strategy

Commonwealth Bank aims to provide competitive customer service and is preparing itself to be the bank of the future for its customers. Based on this principle, the bank divides their digital strategy into six key areas:

- Deep Personalization: Deploying artificial intelligence, machine learning and data insights to drive personalized and seamless services across channels

- Integrated digital experience: Working on new digital banking services, partnering with leading market providers, and building the X15 venture to deliver the finest integrated digital banking experience for consumers and businesses. X15, is an Australian technology venture-building entity designed to deliver modern digital solutions that benefit the Australian market.

- Digitising the end-to-end process: Automating and digitising processes to make things simpler, faster, and more user-friendly for both customers and employees

- Intelligent protection: Using real-time intelligent analytics to detect suspicious activities, send real-time alerts and automatically block fraudulent transactions

- Modern, resilient platform: Leveraging platform-as-a-service to deliver a resilient system, cutting applications and moving 95% of computing to the public cloud

- Globally leading capability: Partnering with global technology leaders and talent to support 24/7 operations

Initiatives taken by the Commonwealth Bank in 2020 to strengthen their digital strategy:

CommBank app:

- Delivers personalised services and alerts to help customers manage their money better and make smart financial decisions

- Provides transaction notifications, budgeting tools and a monthly spending tracker

- Reinforcing security and fraud detection

- Bill prediction feature using machine learning to identify recurring bills and provide a timeline for upcoming payments

- A Benefits finder tool that connects customers to more than 230 government and third-party benefits

- Provides an integrated shopping experience within the app, along with personalised offers and cashback rewards

- Sends over 27 million smart alerts through the CommBank app and NetBank to help retail and business customers avoid unnecessary overdraft and credit card fees

- Partnering with Klarna to offer a shop-now and pay-later experience. Customers can shop through the Klarna app at almost any online store, and make payments in instalments using their Commonwealth Bank credit or debit card

IT Strategy

- Customer Engagement Engine: Continued investment in the engine, which uses artificial intelligence, machine learning and traces customer behaviour to deliver relevant and personalised experiences

- Reimagining banking: Focusing innovation on core business practices, such as everyday banking, home buying and business banking

- Reengineering processes: Approaching existing processes in a new way to deliver simpler yet effective services

- Growing strategic partnerships: Partnering with start-ups, fintechs, scientists, research institutes and large market-leading companies to strategically pool talent, resources, and expertise

Commonwealth Bank and its ICT Contracts

- Collaborating with organizations such as the CSIRO’s Data61 and Harvard STAR Lab to develop solutions that improve the customers’ financial well-being.

- Establishing their own innovation vehicle, the X15 venture, in partnership with Microsoft and KPMG to build a portfolio of new digital businesses. Backr’s, developed through the same X15 venture, will help small businesses simplify the process of setting up their business using in-app tools that support registrations, business plan formulation, and invoice creation.

- Partnering with SquarePeg and Zetta to identify and launch future digital solutions for customers.

- Partnering with PegaSytems to Pega Customer Decision Hub™ as a customer engagement engine that uses pre-recorded past conversations (including frequently asked questions) with the customer along with the customer profile to have guided, intelligent, and personalised conversations through multiple physical and digital touchpoints.

9 Growth and Innovation Opportunities

- #1 Cost to serve

- The bank currently operates on a marginally good cost-to-income ratio of 46% compared to its peers. However, it should focus on reducing its cost allocation to staff and personnel expenses, which constitute 51% of total expenses and 23% of total revenue.

- This creates an opportunity for the bank to substantially reduce this cost base through:

- The reduction of call centre use for customer query management and sales, and instead investing in AI-driven virtual assistants and chatbots for iterative functions

- Replacing man-hours with cognitive process automation of routine and daily back-end tasks

- Adopting a holistic cloud implementation strategy that centralizes business for regular activities and eliminates data centre management

- Digitalization of more functions and processes that are currently human intensive, such as branch relationship management, cashier, and customer grievances

- #2 Transformation of the branch and its branch networks

- The bank operates 1118 branches and over 4300 ATMs, which constitutes a physical infrastructure cost of 4.4% of its total revenue. This is 14% higher than their regional competitors. It implies that the bank has an opportunity to save nearly US$ 1 billion annually through branch transformation strategies.

- The bank should focus on undergoing an overall branch transformation to achieve about 50% reduction in their overall infrastructural costs by:

- Reducing the branch network

- Initiating limited working hours across regional branches

- Creating self-service kiosks and minimizing the wait time

- Building branches as part of a community centre or café

- #3 Customer experience

- Omni-channel experience: The bank has a multichannel presence, since it provides various touchpoints to consumers including bank branches, mobile banking, ATMs, and contact centres in Australia. There is an opportunity to build an omnichannel experience across physical and digital domains for a seamless customer experience across all channels. This will be a distinct competitive advantage compared to the many other neobanks.

- Personalized insights: As the bank provides a bill prediction feature to assess the monthly targeted expenditure and integrates an e-commerce shopping experience within the app, it can expand on this and add other functionalities such as:

- Budgetary tools for personal financial management

- Re-investment of savings in byte-sized wealth products

- Evidence-backed recommendations to reduce spending and manage savings

- #4 Business segment expansion

- The bank boasts of a large loan book, one that is diverse by the customer, region, and section. It also has the resources and data to support robust credit decisions, while sustaining a low bad debt/gross loan ratio.

- However, the Commonwealth Bank has seen a low conversion rate in the SME business loan market. At present, the bank has 20% of share of business deposits, but only 17% percent in the business loan market.

- Commonwealth Bank should fasten and simplify the loan processing journey and approval. This is to encourage the conversion of transaction banking and payment customers to borrowers. Steps include:

- A robust credit-profiling mechanism that incorporates predictive analytics to assess loan credibility beyond the financial statement analysis.

- A short turnaround-time to apply, assess and approve business loans, with an aim in achieving conversions in less than 5 minutes for short-term overdrafts and loans.

- #5 Employee experience and productivity

- Apart from the employee engagement index score, the bank should focus on people analytics. This is to check on the unconscious bias that is unfairly impacting promotion and compensation decisions.

- Build hybrid-working models that encourage flexibility in working-from-home and in-office, including onboarding and training.

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Providing personal development allowances

- A liaison for mental health and meditative programs

- Extending pre-natal and child-bonding leaves with childcare assistance

- Creating a monthly piggy bank for Netflix, Spotify, gyms, etc.

- Building customizable compensation plans to include flexible share incentives, as well as fixed and variable components

- #6 Migration of workload to the cloud

- At the Commonwealth Bank of Australia, applications that involve regulated transactions, sensitive data or need low-latency performance nearly always remain on-premises.

- The Bank should upgrade the public cloud portion of its hybrid cloud to take on more workload, with the potential for swift uptake. This will help the bank achieve cost efficiencies and significant modernisation, such as:

- Building a scalable digital platform as a service and develop proprietary software for core functions

- Creating a robust, tightly controlled delivery program that allows developers to scale and embed microservices onto the cloud architecture

- Incorporating backup and redundancy capabilities to address security and compliance concerns

- As the custodian of enormous legacy data, it can become a competitive differentiator by harnessing data real-time on cloud

- #7 Neo banking

- 50% of the bank’s total customers are millennials, who want simple, fast, and personalised services. The bank should consider a revitalised digital brand that connects with millennials.

- This could be done by reimaging its existing ‘CommBank’ app to one that resonates with millennials. It can be done by positioning the app with a new digital spin-off to connect with the segment.

- An aggressive digital spin-off that brings together elements of gamification, convenience, and frictionless banking is key to combat the competition from rising neo banks.

- #8 Artificial Intelligence (AI) in every aspect

- One key area where Commonwealth Bank struggles with is in its compliance risk management. To strengthen its risk management framework, the bank should further explore AI capabilities by:

- Harnessing internal data, ranging from employee interactions and emails to trade transactions, and using it to offset compliance risks across business verticals via machine learning tools

- With the bank’s continued effort towards building personalised experiences, it should leverage on the multitude of customer data gathered from legacy years with the aim of embedding finance into customer journeys. Both AI and machine learning can be used to build augmented data insights that:

- Automate and optimise typical daily tasks using virtual assistants and chatbots, which is currently managed by humans

- Replace traditional means of identification with facial and voice recognition for a quick and robust security mechanism

- #9 Society and planet contribution

With the bank’s commitment to support global net transition to a net zero emissions economy by 2050, they should focus on:

- Using green products such as virtual cards, pulper cards, eco ink, and carbon control press machines to reduce the direct impact of their business activities on the environment.

- Compensate for unavoidable emissions by launching projects in impoverished areas. This helps to preserve biodiversity and drives reforestation, while furthering local economic mobility.

- Introduce innovative banking services to encourage the consumption of renewable resources. Examples include low-interest loans and credit facilities for green building, and renewable energy financing for SMEs.

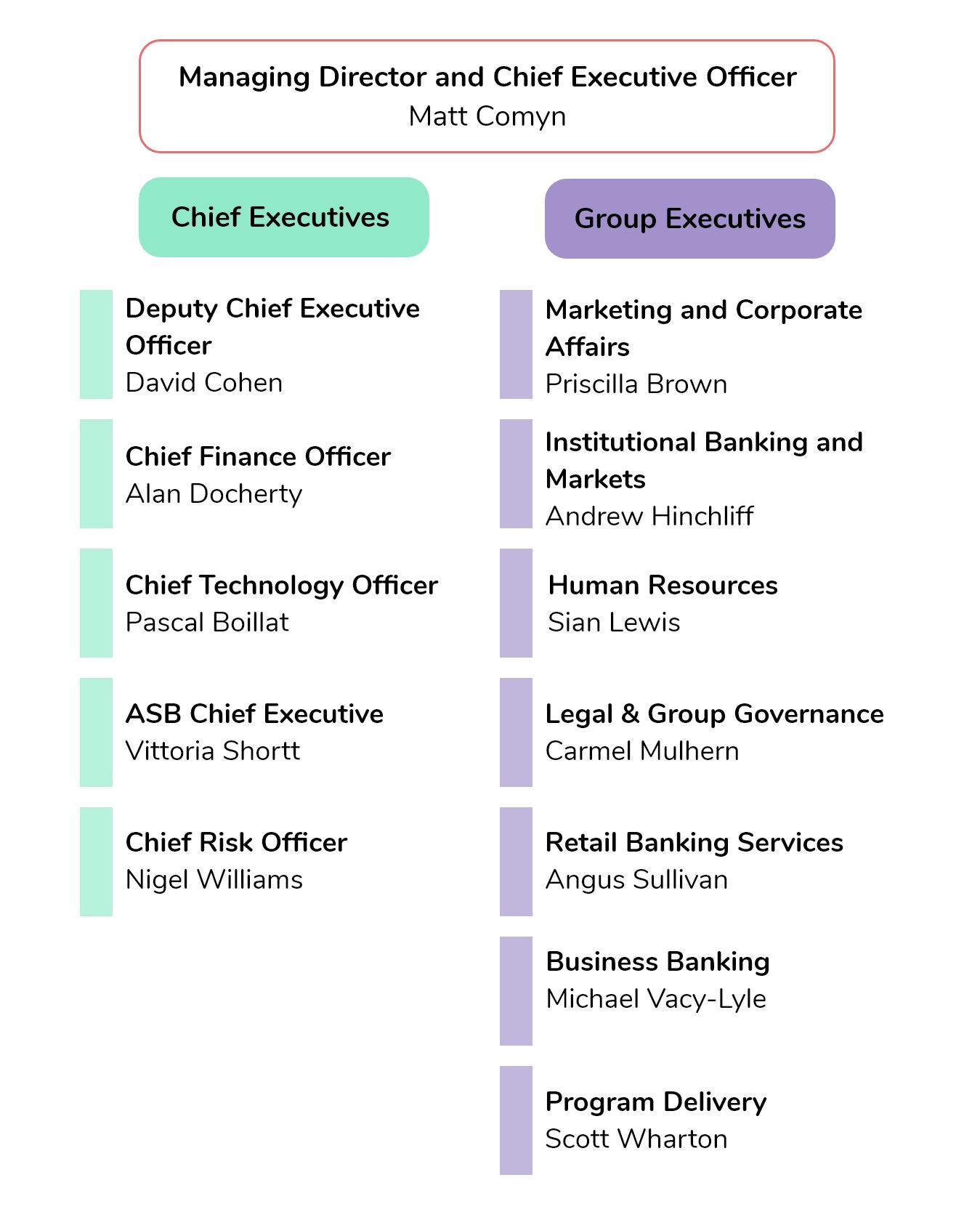

Organisation structure: Leadership

Executive Profile

Matt Comyn

Chief Executive Officer

Matt Comyn has been the Chief Executive Officer and Managing Director of the Commonwealth Bank of Australia (CBA) since 9th April 2018.

He has 20 years of experience in banking across business, institutional, retail and wealth management, and has held several senior leadership roles since joining CBA in 1999.

As CEO, Comyn is focused on building a simpler bank, one that is fully aligned to meeting the needs of customers in core markets. This is underpinned by stronger risk management and a continuing commitment towards innovation and customer service.

Quotes

- Strategy, Annual report 2020

Delivering a simple and better bank that leads in retail and business banking – supported by the best digital experience for customers.

- Setting customers as priorities, Annual report 2020

This year, in response to the coronavirus pandemic, our priority has been to do what we can to support our customers through the financial and business impact of the crisis. We were able to act quickly because of the commitments of our people, our technology capabilities, and our strong financial position.

- Customer experience, 12 February 2020

A big part of our strategy is delivering exceptional customer service, but also doing so with leading technology. And it is not just about the digital experience, it’s about a real-time and high availability system.

- Digital strategy, 12 February 2020

Digital is an incredibly important part of technology-driven business focus, but actually, our ambitions are really about making sure that we have a modernised, real-time and very resilient top to bottom technology stack.

David Cohen

Deputy Chief Executive Officer

David Cohen is the Commonwealth Bank’s Deputy Chief Executive Officer. He commenced this role in November 2018.

He is responsible for the Group’s Customer and Community Advocacy team, as well as the Group’s Mergers and Acquisitions team and PT Bank Commonwealth. Cohen also oversees Colonial First State, Aussie Home Loans and, until its sale’s completion, CommInsure Life.

His key priority is in supporting the Chief Executive Officer on Group-wide initiatives to build a simpler and better bank for the future. The focus is on enhancing the Bank’s engagement with the government, regulators, industry, and community groups. He also chairs the Bank’s Royal Commission Implementation Taskforce. Cohen is a member of the Executive Leadership Team.

Previously, Cohen was the General Counsel of AMP and a partner with Allens Arthur Robinson for 12 years.

Alan Docherty

Chief Financial Officer

Alan Docherty became Chief Financial Officer on 15 October 2018, having acted in the role since May 2018.

He joined Commonwealth Bank of Australia in 2003. Docherty was previously the Chief Financial Officer of the Institutional Banking and Markets division, which is responsible for managing the Group’s relationships with major corporate, government, and institutional clients. The division also provides a full range of transactional and risk management products and services. Docherty led CBA Group’s regulatory and economic capital function.

He has more than 20 years of experience in working with blue chip financial services organisations in the UK and Australia. Prior to joining CBA, Docherty worked for PwC in the UK, and Arthur Andersen and Ernst & Young in Australia.

Pascal Boillat

Executive of Enterprise Services and Chief Information Officer

Pascal Boillat is the Group Executive of Enterprise Services and Chief Information Officer at the Commonwealth Bank of Australia. He is an experienced technology and operations professional and has more than 30 years of experience in financial services.

Boillat joined Commonwealth Bank in October 2018, and is responsible for information technology, cyber security, technology infrastructure and digital delivery for all divisions across the bank. He is also responsible for banking and markets operations, group regulatory operations, as well as procurement and supplier partnerships.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency are aligned with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on 5 purpose pillars and score each bank on them.

Endnotes

Commomwealth Bank of Australia, (2020, June 30). Group Annual Report.

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/results/fy20/cba-2020-annual-report.pdf

Largest banks in Australia by assets, (2019). Statista.

https://www.statista.com/statistics/434596/leading-banks-in-australia-assets/

Commomwealth Bank of Australia, (2020, June 30). Market Index.

https://www.marketindex.com.au/asx/cba

Gurinayat Brar and Sourav Kumar, Research Interns, contributed to this research.