Company insights

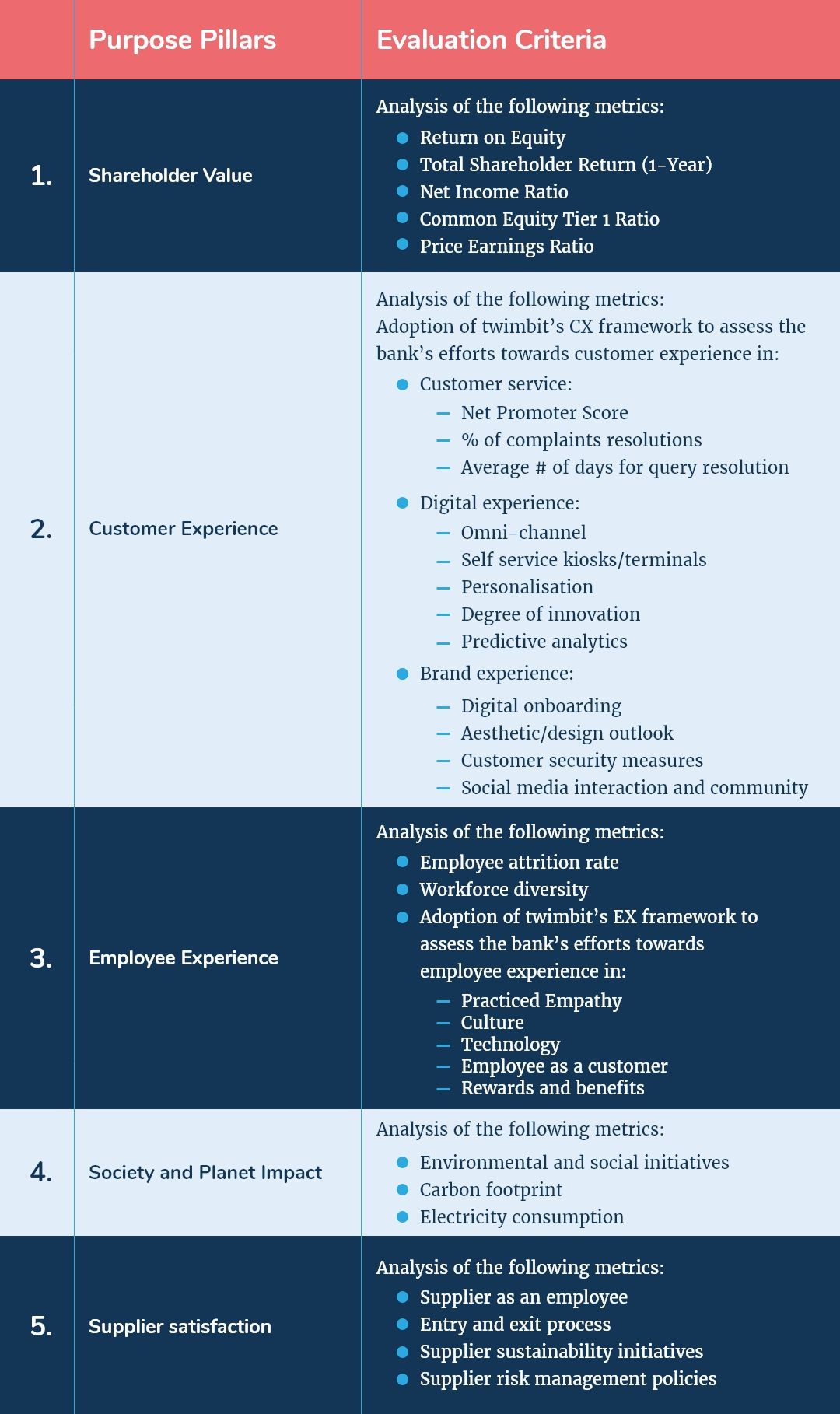

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

National Australia Bank (Group financials) – An overview as of 30th September 2020

| Bank name | National Australia Bank (NAB) |

| Headquarters | Melbourne, Australia |

| Operating income (30th September 2020) | USD 13.1 billion |

| Net Profit after Tax (30th September 2020) | USD 2.6 billion |

| Total Assets | USD 659.5 billion |

| Employees | 34,000 |

| Country of operation | 10 |

| Number of branches | 850 |

| Information and Communication Technology (ICT) Spend (30th September 2020) | USD 0.6 billion |

| Bank ranking in a particular country | 4th in Australia* |

| Number of customers | 9 million + |

| Market capitalisation (30th September 2020) | USD 56.85 billion** |

| Operating revenue CAGR growth (2015 – 2020) | -11.45% |

** NAB:ASX · AUD, Market Index

Shareholder value (30th September 2020)

| Return on Equity (30th September 2020) | 5.98% |

| Total Shareholder Return (1-Year) (30th September 2020) | -36.40% |

| Net Income Ratio | 20.34% |

| Common Equity Tier 1 Ratio | 11.47% |

| Price Earnings Ratio (30th September 2020) | 29.24% |

NAB and its strategic focus areas

- Customer experience

The bank aims to deepen its relationship with existing customers and attract new customers. It will efficiently manage costs as the bank continues to digitise the business and improve on customer experience:

- Increasing virtual chats to optimise the customer support system–~15% of chat sessions transferred to contact centres

- Offering customers the flexibility to book appointments (in a branch, on the phone, in their own home, office or virtually)

NAB initiatives to enhance the customer experience in FY2020:

- Launched Australia’s first no interest credit card (StraightUp), with a no use, no pay feature.

- Enabled the Federal Government’s First Home Loan Deposit scheme

- Increased the maximum account value threshold for which UBank customers can earn bonus interest to USD 190,500. This rise resulted in 99% of UBank customers now receiving bonus interest on their savings.

- Launched an in-app activity tracker at BNZ, designed to help customers be good with their money.

- Employee experience

The health, safety and wellbeing of 34,000 NAB colleagues remain the bank’s highest priority.

- Investing in NAB workforce to be trained in the fundamentals of banking

- Focus on upskilling technology capability with >1,400 industry-certified colleagues in Amazon Web Services (AWS), Microsoft Azure and Google Cloud Platform

- Conducts regular pulse checks to get timely feedback on colleague needs

NAB has taken the following initiatives to enhance capabilities and promote a healthy working environment:

- Committed USD 38 million in investment over the next three years for all colleagues to complete the Career Qualified in Banking certification through the Financial Services Institute of Australasia, an industry-first in Australia and New Zealand

- Offered 65 new traineeships to Indigenous Australians and recruited 40 African-Australians as part of the African Australian Inclusion Program

- Developed a new leadership program that will provide all managers with a consistent set of skills, understanding, and leadership expectations at NAB

- Product innovation

In FY2020, NAB is organising the bank around customers’ needs by improving products and services as well as increasing digital enablement:

- Implemented a new customer-centric organisation structure with clear accountability.

- Strong technology foundations led to improved resilience, lowered costs, and an enhanced customer experience.

- Accelerated the roll-out of digital tools and new partnerships to enhance data and analytics capabilities.

NAB took various initiatives to launch innovative products and services, including:

- Introduced Australia’s first no-interest credit card, the NAB StraightUp Card, in response to Australians wanting more control over their finances. It gives customers access of up to USD 2,280 credit for a flat monthly fee, charged only when the card has activity

- Introduced a single customer onboarding system for Corporate and Institutional Bank globally

- Continued to streamline product and service offerings across the group by removing 12 products, consolidating eight products, and removing 88 fees.

- Society and planet impact

The bank recognises that addressing environmental challenges like climate change, resource scarcity, natural capital loss, and degradation is crucial. As regulations evolve and markets change, NAB understands that its relationships with customers, suppliers, and other stakeholders, as well as the growth of the organisation, will partially depend on how the bank manages the environmental aspects, impacts and dependencies of its business.

The bank’s environmental agenda incorporates strategies covering:

- Climate change – increasing the impact of climate change and climate-related policies on its business, customers, and the communities in which the bank operates.

- Resource scarcity – the increasing competition for finite resources has the potential to limit economic growth and business operations.

- Natural value – increasing pressure on the natural capital that underpins the economic system could impact future asset and business value.

Digital Strategy

NAB has planned to invest USD 988 million (Discretionary spend 30% and Other spend 70%) in FY2021 on its digital priorities, as mentioned below:

- Discretionary investment spends focused on core projects to support growth:

- Simplify business lending processes and policies

- Invest in bankers, processes, and technology to improve customer experience

- Simple and digital transactional banking

- Simplify end-to-end home lending process – initial focus on proprietary channels

- Grow UBank (an Australian direct bank that operates as a division of NAB offering digital banking products) as its digital proposition to attract tech-savvy customers

- Enhance the use of data and analytics to deliver customer solutions and improve the control environment

- Continue to enhance technology resilience via insourcing and migration of apps to the Cloud

- Other spends include:

- Investments to uplift systems, processes and control the environment

- Focus on financial crime detection and prevention and cybersecurity capability

- Sydney and Melbourne commercial property fit-outs

Initiatives taken by NAB in lieu of the digital strategy:

- NAB announces agreement to acquire 100% shares in 86 400 Holdings Ltd:

- NAB is bringing together UBank and 86 400 as its long-term strategy and growth plan, which will enable NAB to develop a leading digital bank that can attract and retain customers at scale and pace.

- This combined business will deliver accelerated innovation and an enhanced customer experience to create a stronger and more competitive banking alternative for Australian customers.

- Enhanced the NAB mobile app with a range of self-service features, including enabling a one-click application for transactions, opening or closing savings accounts, proof of balance, and interim and interest statements

- Expanded New Payments Platform (NPP) helped customers to have faster and simpler access, increased control, transparency, and greater data richness when making payments

- Corporate and institutional customers can easily view and manage their overall cash positions across multiple sub-entities on a single dashboard

- In New Zealand, the bank’s sub-brand, the Bank of New Zealand (BNZ) customers can better organise and understand their financial health with a new personalised spend tracking and categorisation tool in the Mobile BNZ app

- Implementing Basiq’s Affordability Report to gain a comprehensive view of customers’ financial positions. This implementation helps more than 100,000 customers who have deferred their mortgage repayments and are due for a hardship review

- Signed a cross-referral agreement with revenue-based financier Lighter Capital

IT Strategy

In 2019-2020 the bank invested in modernising its foundational infrastructure, including cloud migration, workplace technology refresh, a new workflow, document management platforms, and data hub establishment, along with improvements to its system’s resilience.

- Cloud migration, app reduction & resilience:

- Continuing the strategy of cloud migration and reduction in apps

- Announced strategic partnership with Microsoft – a plan to migrate 80% of apps to the Cloud

- NAB Connect migrated to the Cloud with benefits including secure and scalable capacity, improved platform resilience, and reliability for customers

- Continued focus on cyber, financial crime and fraud:

- Investment and continued focus on cybersecurity and fraud detection has yielded strong outcomes:

- Achieved 50% faster cyber detection and response capabilities

- A 40-fold increase in data protection efficacy through preventative control uplifts

- Invested USD 228 million to uplift financial crime capabilities, and now NAB has >1,000 colleagues dedicated to managing financial crime risks

- Investment and continued focus on cybersecurity and fraud detection has yielded strong outcomes:

- Partnerships to provide enhanced analytics to business customers:

- Announced partnerships with Pollinate and Vend to provide enhanced analytics to business customers

NAB and its ICT contracts

Through NAB Ventures (the bank’s wholly-owned Venture Capital investment arm) and the Mergers & Acquisitions team, NAB made five new investments in 2020:

- Athena – provides a proprietary cloud-native home loan platform aimed at disrupting the Australian prime mortgage market.

- Hometime – supplied a short-term rental management services (co-hosting) platform for Airbnb property owners.

- EdStart – provides financing solutions to support parents to pay private school fees through smaller increments or over an extended period.

- BioCatch – the developer of behavioural biometric technology for use in identity authentication and fraud detection.

- Pollinate – offers a cloud-based, merchant-friendly experience that enables businesses to view real-time sales data and track average transaction value.

The bank continues to invest in building market-leading services for customers:

The NAB mobile banking app has a digital receipt functionality integration from Slyp, which customers use to store over 200,000 receipts digitally.

10 Growth and Innovation Opportunities

- #1 Cost to serve

- The cost to income ratio for ANZ Bank is at 54%, which is exceptionally high compared to its Asia Pacific competitors. The bank should maintain an average cost to income ratio in the range of 40% – 43% to achieve robust bottom-line growth.

- Currently, staff cost is USD 3.45 billion, accounting for 47% of the total expenses and 25% of total revenue. This cost increased by 11% from 2019 to 2020, arising from wage inflation, headcount growth in retail and commercial divisions, and customer remediation processes.

- The bank spent USD 105 million in its customer remediation program and USD 83.45 million in payroll remediation as a charge to provide for operational risk event losses.

- There is an opportunity for the bank to reduce these cost buckets substantially by:

- Removing duplication of tasks, roles, and functions by using blockchain, robotic process automation and quantum computing

- Replacing man-hours with cognitive process automation of routine, daily back-end tasks

- Adopting a holistic cloud implementation strategy that centralises business-as-usual activities and eliminates data centre management

- Digitising customers’ information screening and creating a distributed ledger to secure the transfer of information with an auto-generated audit trail using AI and blockchain

- Automating functions and processes that are currently human-intensive, such as branch relationship management, cashier, and customer grievances

- #2 Transformation of the branch and its branch networks

- NAB has a branch network of more than 850 branches and 1,572 ATMs. The majority of the bank’s financial services businesses operate in Australia and New Zealand. The infrastructural cost of the National Australia Bank (NAB) is increasing at a rate of 4.6% that compounds annually. This rise is due to the growing network of branches, maintenance of the said branches, and growing lease costs.

- To offset the hike in infrastructural costs, the bank should focus on transforming branches with high business volume and customer headcount into flagship digitalised community hubs. This step will enrich the in-branch experience and redefine customer engagement. To achieve such transformation, the bank should:

- Integrate augmented reality (AR) and virtual reality (VR) to create a virtual branch experience using AR/VR tools for remote support services

- Deploy smart robots in-branch to handle daily queries

- Create self-service kiosks to minimise the customer waiting time

- Set-up lounge rooms for networking and community building

- Enhance consumer experience with access to a wide range of services and touch screen UI, turning the ATM into a digital experience

- This strategy will also help the bank reduce the operational and personnel costs of running a branch. It can then utilise the freed-up capital for strengthening digital capabilities.

- The bank can further reconsider shutting down low business volume, regional centres that have limited footfall and instead institute self-service kiosks to manage transactional needs.

- #3 Customer experience

- NAB has shown the most significant improvement in customer satisfaction ratings1 among the major four banks in Australia. It has a customer satisfaction rate of 78.4% that increased impressively by 6.4% in the financial year 2019-2020, mainly due to the bank’s mobile and internet banking facilities.

- The bank has the potential to enhance its customer experience by transforming the sales and service approach to a more solution-oriented approach. NAB needs to focus on the following areas to ensure a seamless customer experience:

- Personalised contextualised data insights on customers’ spending and saving patterns through AI and ML

- A bill prediction feature that manages utilities, subscriptions, etc. with automated alerts on due dates and payments

- Byte-sized wealth management products for quick, hassle-free investments

- Low-cost remittances and foreign currency exchange services

- Micro-insurances for car rides, food deliveries, cycles, pets, etc.

- Omnichannel experience: The bank has a multichannel presence since it provides various touchpoints to consumers, including bank branches, mobile banking, ATMs, and contact centres. There is an opportunity to build an omnichannel experience across physical and digital domains for a seamless customer experience across all channels. This reformed presence will be a distinct competitive advantage compared to the many other neobanks.

- #4 Business segment expansion

- The bank has consistently held onto its large market share (21% market share in Australia) of business loans, and continued investment shows a clear intention to retain this position. This position ultimately led to a better understanding of the customers’ requirements, faster turnaround times, and higher approval rates. NAB has the capabilities to take investments into digital onboarding and provide fast access to unsecured lending. Doing so will ensure that the bank retains high satisfaction amongst small business owners. To remain strong and increase market share, the bank should create:

- A robust credit profiling mechanism that incorporates predictive analytics to assess loan credibility beyond financial statement analysis.

- A short turnaround time to apply, assess, and approve business loans, achieving conversions in less than 5 minutes for short-term business overdrafts or loans.

- #5 Employee experience and productivity

- NAB has an employee engagement score of 76%, which increased by 10% compared to 2019. This score, however, is less than the average employee engagement score of other operating banks in Australia. Apart from the employee engagement score, the bank spends USD 3.45 billion on personnel expenses.

- To increase employee productivity and performance, the bank should digitally transform its employee journey by focusing on radical improvement in the employee experience. NAB can channel its efforts toward:

- Using people analytics to check that unconscious bias is not unfairly impacting people promotion and compensation decisions.

- Integrating machine learning and data analytics to augment and deliver highly relevant recommendations to its employees.

- Clearly defining the expectations for all senior leaders to build a culture of clear accountabilities in its divisions.

- Designing personalised employee upskilling programs based on the employee level and adopting effective leadership development coaching to prepare them for future roles.

- Simplifying its onboarding process and giving its employees a clear career development trajectory.

- Expanding its employee wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs.

- Incorporate rewards and benefits beyond insurance, stock options, house rentals, and leases, which will eventually increase employee engagement and create a friendly working environment. Ideas include:

- Giving employees the option to work on cross-department projects to make them more versatile and productive

- Periodical career breaks and approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food drives, medical support, and cleaning drives

- A liaison for mental health and meditative programs

- Extending pre-natal and child-bonding leaves with childcare assistance

- Creating a monthly piggy bank for Netflix, Spotify, gyms, etc.

- #6 Migration of workload to the cloud

- NAB Group has set a goal to migrate 100% to the Cloud. NAB has invested in building a multi-cloud ecosystem that will host 1,000 of the banks’ applications to the primary Cloud while ensuring that the same applications can be moved to or run across a secondary cloud if necessary.

- NAB Group already moved more than 800 applications to public cloud providers as part of its Cloud-first, multi-cloud strategy. The bank’s proportion of apps on the public Cloud will move from one third to around 80 per cent by 2023.

- The bank has the opportunity to use its cloud architecture to:

- Apply advanced analytics, AI and machine learning on the available data sets to get meaningful segment-specific insights to identify operational inefficiencies.

- Adopt a customer-centric cloud-based strategy that allows the bank to create a productive environment for developers to seamlessly create, test, and deploy various services through a microservices mesh architecture. NAB can easily pilot these services with soft launches and manage its successes or failures without hitting cost structures.

- Provide complete end-to-end protection of all confidential data stored in the Cloud. This protection enables the bank to maintain the customers’ trust and confidence in obtaining, analysing, and sharing its customers’ personal information.

- Responding to market shifts such as black swan events – examples include Covid-19 and the entry of non-bank players to the banking environment with the grant of digital banking licenses

- #7 Neo banking

- Post the acquisition of 86 400, NAB is in the process of integrating the neobank with its digital proposition – Ubank. The combination of both will help NAB to target the growing millennial population in Australia.

- 86 400 bank has features such as customisable dashboards, personalised cash management suggestions and a user-friendly interface. These capabilities will bring a competitive edge over the upcoming neobanks in the region.

- NAB can further incorporate the following elements in its neo banking strategy:

- Transparent and simple fee structure without any hidden fees for debit Visa cards and MasterCard, as well as foreign currency fees when using an overseas credit card

- Enable multicurrency accounts with zero-to-minimal cross border remittance fees

- Gamify various customer touchpoints like awarding badges with increased use of products, giving discount coupons to its loyal customers, leader board between friends and colleagues based on product purchases and highlighting trending products

- #8 Artificial Intelligence (AI) in everything

- NAB uses AI to triage customer complaints and detect money-laundering activities. To stay at par with its competitors, the bank needs to expand the scope of Artificial Intelligence and Machine Learning by focusing on the following areas:

- Automating labour-intensive, error-prone, and complex risk processes that deal with high volumes of structured and unstructured data by incorporating predictive threat monitoring and detection of risks like fraud, insider threat, cyber and compliance risks

- Combining customised banking products and other services such as insurance, wealth management, treasury services, and the like, as well as pursue new API-enabled propositions

- Building augmented data insights using customer behaviour analytics to roll out personalised products for its customers

- Apply cognitive process automation to automate a set of tasks that improvises upon the bank’s previous iterations, such as monthly bill payments, changing subscription plans based on best offers, alerts for stock updates, etc. Such automation will help customers improve their existing lifestyle choices and optimise monthly bills

- #9 Cybersecurity

- NAB invests heavily in data security by incorporating predictive risk intelligence to provide advance notice of emerging risks, increase awareness of external threats, and improve the bank’s overall understanding of risk exposure and potential losses. These investments helped NAB in reducing 33% of critical and high priority incidents.

- To enhance its cybersecurity capabilities, including new data protection controls, NAB can adopt the following measures:

- Objectively measure risk performance by facilitating the development of key risk indicators, key performance indicators, and associated threshold measures.

- Develop and maintain the bank’s integrated security controls framework, extracting information from multiple regulatory sources and guidelines like Australian Prudential Regulation Authority (APRA), Financial Sector (Transfer and Restructure) Act (FSTRA), The Anti-Money Laundering and Counter-Terrorism Financing Act, etc.

- Constantly monitor its existing security framework to identify any misconfiguration in firewalls, proxies, and data loss prevention tools.

- #10 Society and planet contribution

- NAB relies on conducting business activities in a healthy environment and is committed to source 100% of electricity from renewable sources by 2025. The bank has set objectives to reduce the environmental impact of its business activities by 2025. To achieve these objectives, the banks should focus on:

- Using green products, such as virtual cards, pulper cards, eco ink, and carbon control press machines. The usage of such items will help NAB reduce the direct impact of its business activities on the environment

- Compensating for unavoidable emissions by launching projects in impoverished areas which help to preserve biodiversity, drive reforestation, and further local economic mobility

- Introducing innovative banking services to encourage the consumption of renewable resources, such as low-interest loans and credit facilities for green building and renewable energy financing for SMEs

- Minimising the amount of paper and plastic waste within the branches and instituting a ‘3R’ policy of reduce, reuse, and recycle for waste management:

- Ban on plastic use within office premises

- Use of own cups, bottles, and cutlery

- Recycled water used in washrooms and the pantry

- Reduction in paper used for documentation

Organisation structure: Leadership

Executive Profile

Ross McEwan

Chief Executive Officer and Managing Director

Ross McEwan became Group Chief Executive Officer and Managing Director of National Australia Bank Limited in December 2019.

He has over 30 years of experience in finance, insurance, and investment industries, and before joining NAB, he was Managing Director of First NZ Capital Securities. McEwan was also Chief Executive Officer of National Mutual Life Association of Australasia Ltd / AXA New Zealand Ltd.

Quotes

- Supporting Customer, NAB sustainability report 2020

We work directly with our customers to find the right solution or refer them to free and independent services if that’s what they need. We won’t deal with fee-charging debt management providers looking to take advantage of customers already under pressure. Going forward, we want to be known for being easy to deal with, a safe bank, relationship-led and for our long-term view.

- Managing climate change, NAB sustainability report 2020

Climate change is one area where we will play our part. We are evolving our business to help manage the effects of climate change and support the transition to a low-carbon economy. Critically, we are doing this mindful of energy security, the challenges and opportunities of our major customers and the potential impacts on the communities in which they employ many Australians.

Gary Lennon

Chief Financial Officer

Gary Lennon became the Group Executive, Finance in March 2016.

Lennon also worked as Executive General Manager Finance, leading the Group’s Finance function globally with accountability for all finance and tax-related activities for the group, from June 2010.

Prior to joining NAB in 2008, Gary spent eight years holding several senior finance executive roles at Deutsche Bank in Australia, Japan and Singapore. Before Deutsche Bank, Gary was with KPMG for 10 years and held senior management roles in Sydney and London.

Shaun Dooley

Chief Risk Officer

Shaun Dooley has been working with NAB for more than 26 years. He held senior roles across the bank in Finance, Risk, and Corporate and Institutional Banking.

Dooley appointed as Group Chief Risk Officer in October 2018 and responsible for the Risk functions across NAB. He is also a member of the Executive Leadership Team in NAB.

He was recently the Group Treasurer, where for the past three years, Dooley was responsible for capital, funding, liquidity and risk management.

Nathan Goonan

Group executive, strategy and innovation

Nathan Goonan joined the Executive Leadership Team in April 2020 in the newly created position of Group Executive Strategy and Innovation. Before this role, he was the Executive General Manager Group Strategy and Development for NAB and responsible for the global execution of its corporate strategy and mergers and acquisitions activities. Goonan has also held the role of Executive General Manager for Corporate Affairs.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

National Australia Bank, (2020, September 30). Annual Financial Report.

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2020-annual-financial-report-pdf.pdf

National Australia Bank, (2020, September 30). Annual Review.

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2020-annual-review-pdf.pdf

Roy Morgan, (2020, September 30). CBA leads bank satisfaction but NAB the big improver in 2020.

http://www.roymorgan.com/findings/8487-consumer-banking-satisfaction-june-2020-202008170625

Statista, (2020, September 2). Largest banks in Australia in financial year 2019, by assets.

https://www.statista.com/statistics/434596/leading-banks-in-australia-assets/

Market Index, (2020, September 30). NAB:ASX. AUD.

https://www.marketindex.com.au/asx/nab

Sourav Kumar, Research Intern, contributed to the research in conducting preliminary literature review, creating infographics, and conceptualising the article.