Company Insights

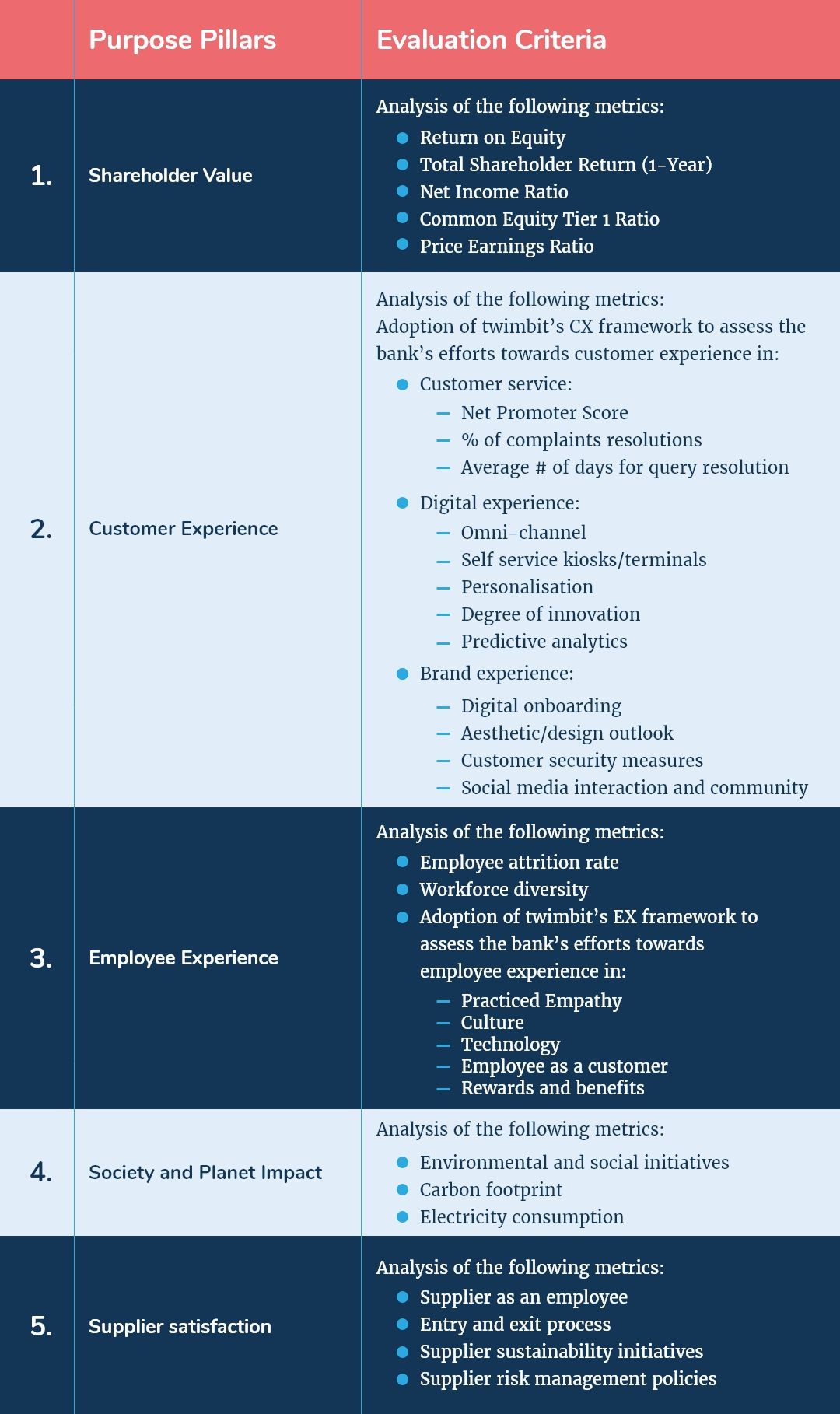

twimbit Purpose Benchmark

Source: Refer to the methodology in Appendix A below

OCBC (Group financials) – An overview as of 31st December 2020

| Bank Name | Oversea-Chinese Banking Corporation |

| Headquarters | Singapore |

| Operating income (31st December 2020) | USD 7.6 billion |

| Group net profit (31st December 2020) | USD 2.7 billion |

| Total Assets | USD 394 billion |

| Employees | 29,706 |

| Countries in operation | 18 |

| Number of branches | 600+ |

| Information and communication technology (ICT) expenditure (31st December 2020) | USD 369 million |

| Bank ranking in a particular country | 2nd in Singapore |

| Number of customers | 3 million |

| Market capitalisation (30th December 2020) | USD 34.5 billion |

| Operating revenue CAGR growth (2015-2020) | 2.5% |

Singapore’s accounting period follows a cycle from January – December. The above financials are as per accounting year 1st January 2020 – 31st December 2020.

The SGD to USD dollar conversion rate used is 0.7564.

The ICT spend calculated is based on the average increase in contribution to total operating expenses in the last three years

Shareholder value (31st December 2020)

| Return on Equity (31st December 2020) | 7.6% |

| Total Shareholder Return (1-Year) | -3.7% |

| Net Income Ratio | 35.4% |

| Common Equity Tier 1 Ratio | 15.2% |

| Price Earnings Ratio (31st December 2020) | 9.65 |

Awards

| 2020 | – Best Digital Trade Finance Platform Initiative, Application or Programme for “Velocity@OCBC”, awarded by The Asian Banker – Best Transactional Banking Online Platform, awarded by Alpha Southeast Asia – Best Transactional Banking Online Platform, awarded by Alpha Southeast Asia – Excellence in Digital Innovation, awarded by The Digital Banker – Best Retail Bank, Singapore, awarded by The Digital Banker 2020 – The Enterprise Risk Technology Implementation of the Year, awarded by The Asian Banker Risk Management Awards 2020 – Best Transactional Banking Online Platform, awarded by Alpha Southeast Asia |

OCBC and its strategic focus areas

OCBC aims to help individuals and businesses across communities achieve their aspirations by providing innovative financial services that meet their needs.

- Regional expansion and integration

OCBC is looking to penetrate regional markets with its extensive mass-market financial and wealth-management products. In small to midsize and corporate banking, the bank is well-positioned for increasing regional trade in Asia. Moreover, the bank’s presence in multiple Asian countries allows it to facilitate its customers’ (SMEs and corporate clients) ambition in expansion across the Greater China and Southeast Asian regions. These markets are large and offer OCBC substantial room for expansion. For fulfilling its regional expansion strategy, the bank is aiming to:

- Deepen its presence not only in Greater China but Europe as well.

- Build-transfer approach – An approach to develop financial products for its home market in Singapore before extending them to subsidiaries across the region.

- Strong balance sheet – Leverage its strong capital, funding, and liquidity positions, giving the bank the flexibility to capitalise on market expansion opportunities.

- In their core business segments, the bank is planning to expand in the following areas:

- Retail banking

- Support domestic economic activities and cross border trade, investment, and wealth flow with a comprehensive consumer, retail and commercial banking franchise across well-connected businesses and regional networks.

- OCBC focuses on serving individuals across the different stages of their lives:

- Children and young families with their Child Development accounts and OCBC

- Mighty Savers Account

- Youth between 16 and 29 years old through FRANK by OCBC

- Working adults with products such as OCBC Life Goals

- Pre-retirees and retirees through OCBC Silver Years

- Wealth management

- OCBC captures rising Asian wealth through an integrated model across private and premier banking, bancassurance, securities brokerage, and asset management with regional presence and digital offerings.

- Retail banking

Initiatives taken by OCBC in line with its expansion strategy in 2020:

- Tthe Bank of Singapore officiated its wealth management subsidiary, BOS Wealth Management Europe, in Luxembourg and an additional branch office in London. This step positioned OCBC better in capturing opportunities across Europe.

- OCBC formed a strategic partnership with Edelweiss Group, one of India’s largest diversified financial services groups. This partnership gave clients of both entities access to a wide range of global investment solutions with OCBC and wealth solutions and investment opportunities with Edelweiss.

- Granted loan moratoriums to existing customers in Singapore, Malaysia, Indonesia, and Hong Kong SAR.

- Provided additional working capital financing to customers across core markets for cash liquidity. Leveraged data to offer pre-approved Temporary Bridging Loans to existing customers in Singapore, enabling faster access to credit.

- Enabled digital acceptance of loan offers in Singapore, thereby minimising face-to-face interactions between customers and bank staff during the pandemic.

- Launched an online version of its wealth advisory process – a complex face-to-face process involving over 50 pages of documents and a comprehensive Financial Needs Analysis (FNA).

- OCBC saw a 45 per cent increase in the sale of wealth management products in the first 10 days of launch compared to the 10 days before the launch occurred.

- Customer experience

- OCBC claims to be in a position that enables it to engage customers in new, productive activities. The said activities include supply chain transformation, advanced manufacturing, sustainability and renewable financing, digital services, and business transformation.

- Supporting SME customers:

- OCBC group worked in partnership with companies like Enterprise Singapore, Amazon, Google and Shopee, to create a series of webinars to equip SMEs with the digital know-how to prepare SMEs for future opportunities, such as strengthening business resilience post-COVID-19 new normal.

- The bank integrated cash flow and invoicing capabilities into its digital business banking platform. This step provides SMEs with a seamless experience and quick access to complete and up-to-date views of their business finances for improved cash flow management.

- Launched OneCollect Merchant services in Singapore and Malaysia. This launch allows SMEs to accept digital payments through Paynow QR for real-time collection of payments, instant notifications, and automated reconciliation of transactions for both their online and physical stores.

- Launched video authentication for SMEs, enabling remote account opening during the pandemic.

- Product innovation:

- Inculcated the practice of Human-Centred Design (HCD) to build products and services that are functional, easy to understand, and emotionally engaging.

- Customer redressal mechanism:

- The bank monitors and measures the quality of the delivered experience. This monitoring is achieved by systematically and rigorously measuring customer satisfaction levels, the number of customer complaints (the fewer, the better), and customers’ willingness to recommend the bank (Net Promoter Score).

- To ensure continuous improvement, OCBC also aims to monitor and measure the quality of the delivered experience. The bank actively uses complaints to learn and improve its people, systems, and processes to retain customers and grow new business.

- OCBC has a Complaint Management Council, which comprises representatives across businesses and operations. The tool makes sure all complaints received are reviewed and tracked to resolution.

- OCBC ensures that the bank’s complaint data is shared with senior management and the board regularly.

Initiatives taken by OCBC to enhance customer experience in 2020:

- OCBC offered USD 20.4 billion of moratorium relief and more than USD 2.04 billion of new SME government-assisted loans to help customers and corporates across the region tide through COVID-19 at the onset of the crisis. This moratorium relief was available to over 165,000 individuals, SMEs, and corporate customers across their core markets.

- OCBC group saw an improvement in its overall Net Promoter Score ranking amongst competitor banks in Singapore from 3rd place in 2019 to 2nd place in 2020.

- OCBC activated backup work locations, rolled out digital enablers, and adjusted operating hours in branches to ensure uninterrupted customer service.

- OCBC deployed digital ambassadors to help less tech-savvy customers migrate to the digital channels to conduct their transactions.

- In Singapore, OCBC rolled out several new digital solutions at the onset of the Circuit Breaker (Lockdown implemented by the Singapore Government due to COVID-19) in April 2020 so that individual customers received continued support with financial services.

- Employee experience

For OCBC, employees are critical assets. Employee experience is the company’s key driver in attracting, retaining, and investing in the best talent to sustain its leading market position. The bank is at the forefront of building superior employee experiences by:

- Digital Training– The training of staff in new disciplines such as design thinking, digital technology, data analytics and artificial intelligence.

- Career progression– The development of employees throughout their career at OCBC, thereby helping them realise their full potential and thrive in the ever-changing economy.

- Digital-driven solutions – Actively leveraging technology to equip sales staff with data analytics tools to attain better customer service and engagement.

Initiatives taken by OCBC to enhance employee experience in 2020:

- In 2018, OCBC launched the Future Smart initiative, its grandest scale and most ambitious digital transformation initiative to date. The bank committed to investing USD 15.12 million in employee development for over three years.

- In its branches, OCBC converted many bank tellers to digital ambassadors. Customers obtained assistance from ambassadors on the latest digital channels and services.

- OCBC claims that all their product managers are conversant with API management and customer experiential design, which aligns with their staff development’s main goal.

- OCBC conducted more than 6,000 virtual training with more than 442,000 attendance groupwide.

- The bank continued its USD 15.12 million investment in training programmes over three years (from 2018-2020) to equip its 30,000 employees with digital skills.

- OCBC launched a Culture Stewardship Programme to reinforce and entrench a strong OCBC culture.

- Society and planet impact

- Environment sustainability: Giving back to society seems to be an integral part of the OCBC corporate culture. The bank aims to create a sustainable society by supporting the communities they operate in and playing a role in environmental protection. The bank is undertaking the following step toward environment sustainability:

- Low carbon emission- Promoting the climate change agenda and supporting its customers by adopting low-carbon projects and funding community initiatives that have a meaningful environmental impact.

These are the initiatives taken by OCBC to create a sustainable society in 2020:

- It has helped set up the OCBC Arboretum: A first in high-tech arboretum that taps on an Internet of Things (IoT) system to monitor tree growth.

- The #OCBCCares Environment Fund, introduced in 2017, supported four projects ranging from plastics reduction, recycling to aquaponics.

- OCBC was the first bank in Southeast Asia to announce that it would stop financing new coal-fired power plants and redirect its focus on funding the development of renewable energy projects.

- Community building:

- Partnership-based community – Forging good strategic partnerships to diversify its financial services and wealth management products, thereby increasing accessibility of its services to customers

- OCBC-NTUC First Campus Bridging Programme – As part of the newly launched Programme, the Bank organises financial literacy workshops for parents to manage their family finances better

- Business Venture loans – OCBC has offered venture loans to SMEs with innovative business models or companies that adopt emerging technologies. Born Digital-An initiative by the bank for SMEs where bank accounts are opened digitally on the day of incorporation

Initiatives taken by OCBC in the direction of community building in 2020:

- OCBC launched the Financial Wellness Index, a comprehensive study of Singaporeans’ financial health. They aimed to continue the Index every year and extend it over the next few years to their core regional markets as well.

- Risk management

OCBC has established a risk management framework that encompasses good governance, sound policies, robust defence lines, the right expertise, and significant technology investments. Singapore-incorporated banks also need to meet: Common Equity Tier (CET1), Capital Adequacy Ratio (CAR) and total CAR of 9.0%, 10.5% and 12.5%, respectively (from 1st January 2019 onwards)

OCBC Bank’s CET 1-15.2%, Tier 1-15.8%, Total-17.9% as of December 2020 is well above the required minimum limit. However, to sustain its risk management practices, OCBC can further:

- Repo and collateral management – Liability management with pro-active repo and collateral optimisation.

- Capital adjustments – Conduct annual capital planning exercise to forecast capital demands and assess its capital adequacy over three years. This process takes the bank’s business strategy, operating environment, regulatory changes, target capital ratios and composition, and expectations of its various stakeholders into consideration.

- Capital Conservation Buffer (CCB) – The introduction of a CCB of 2.5 percentage points above the minimum capital adequacy ensures that the bank builds up adequate capital buffer outside stress periods.

Digital Strategy

OCBC holds a strong market position with its digital transformation initiatives. The bank does not just differentiate itself through purely products and channels but also understands its customers’ expectations through a robust digital framework. OCBC is continuously improvising on digital capabilities with a strong focus on customer experience. Eight in 10 of the bank‘s digital customers rely on their mobile devices, and nearly two-thirds of their SME and Corporate customers perform transactions on their digital platform. The bank targets 60% of its retail and 70% of business customers to be digital customers by 2023.

- Human-Centred Design (HCD) practice – OCBC embraces the HCD practice to build products and services that are functional, easy to understand, and emotionally engaging. This move has led to the development of a structured design approach that starts with a deep understanding of the customer’s needs.

- Customer experience – The bank monitors and measures the quality of the delivered experience. This monitoring is achieved by systematically and rigorously measuring customer satisfaction levels, the number of customer complaints (the fewer, the better), and customers’ willingness to recommend the bank (Net Promoter Score).

- Analytics-driven solutions – The use of customer analytics and comprehensive product understanding provides customers with bespoke solutions and ideas to optimise investment returns. Analytics-driven solutions- The use of customer analytics and comprehensive product understanding provides customers with bespoke solutions and ideas to optimise investment returns.

OCBC already took initiatives to increase customer experience through their digital strategy in 2020:

- Instant customer onboarding:

- Enabled online acceptance for home, renovation, and automobile loans, as well as the use of SingPass to access digital banking services by leveraging National Digital Identity.

- Payments and ecosystems:

- The first bank to partner and integrate with Google Pay to enable peer-to-peer payments.

- Launched HealthPass by OCBC, a platform that works directly with general practitioners and specialists to serve consumer healthcare needs.

- Integrated lifestyle features into its Pay AnyoneTM App, including food delivery services and STACK ( a digital loyalty platform powered by OCBC for tracking and exchanging rewards points across multiple reward programmes)

- The first bank in Southeast Asia to allow instant encashment of cheques at next-generation ATMs.

- Redesigned mobile banking:

- Launched a suite of card control services on its Mobile Banking app, allowing customers to perform activities such as reporting the loss of and replacement of cards. This step reduces the need for requests to go through contact centres and branches.

- Democratising wealth management:

- Launched a full suite of goal-based digital advisory and execution at scale, leveraging OCBC Life Goals and Robo-advisory.

- OCBC Financial OneView, enabled by SGFinDex, allows customers to understand their overall financial health by viewing all their finances across participating banks and government agencies that they have a relationship within one place. It also enables them to achieve financial wellness goals by making financial planning holistic, personalised, and straightforward.

- The bank officially launched an Accredited-Investor platform– OCBC Premier Private Client, to serve the high-net-worth individuals with more sophisticated investment needs.

- RoboInvest: Digital advisory at-scale platform with 34 thematic portfolios

- Innovative services on ATMs:

- The first bank in Southeast Asia to allow instant encashment of cheques at next-generation ATMs.

- Digitalisation at the Bank of Singapore:

- Launched a self-sign up tool for instant activation of digital banking.

- Enhanced Secure Communication channel, enabling Private Banking clients to interact with their relationship managers conveniently on a secure platform.

- With digital channels such as the bank’s chatbot, Emma, OneAdvisor Home, and other online sources, OCBC increased its loan take-up by almost four times.

- Customers can now scan a QR code using the OCBC Pay Anyone app to withdraw cash at the bank’s ATMs in Singapore, enabling the convenience of going cardless.

- Employed AI-powered voice banking to offer proactive, personalised, and automated money management.

- OCBC was the first bank to launch a full suite of goal-based advisory and financial planning solutions on digital platforms via OCBC Life Goals.

- The first bank to launch Market Same-day Online Business Incorporation and Instant Account Opening for ‘Born Digital’ start-ups in Singapore.

- The OneAdvisor Home portal became an essential enabler for OCBC to serve its customers and real estate ecosystem partners better. Through this portal, consumers can assess the affordability of their home purchase and select their dream home.

- Instant access to secured loans for homes and cars through the MyInfo platform.

- Open Banking/SGFinDex for augmenting financial and retirement planning using aggregated, holistic data.

IT Strategy

OCBC is redefining its core technology architecture by shifting from a monolithic infrastructure to a nimbler microservices platform. This strategy is in place via:

- Open infrastructure – An open & scalable architecture with a new enterprise data science platform to drive efficiency, speed, agility, and advanced data analytics.

- Cybersecurity – Continued enhancement on cyber threat analysis, vulnerability exploitation and fraud detection capabilities to strengthen data loss prevention measures, create awareness and train staff to manage threats. For instance, OCBC recently launched the Cyber Certification Pathway for its bank staff.

Initiatives taken by OCBC to institute a world-class IT strategy in 2020:

- Built data science and data lake platforms and deployed solutions supported by Artificial Intelligence (AI) across its wealth advisory, risk management, cybersecurity, and compliance units.

- An industry-level Working Group, comprising of more than 70 professionals across 16 organisations, co-created via the new Technology Risk Management Guidelines with the Monetary Authority of Singapore (MAS).

- OCBC embraced collaboration with fintech companies through The Open Vault and harnessed new technologies— from biometrics to artificial intelligence (AI) —in a discerning manner.

- The bank eliminated the use of physical hardware tokens with digital OCBC OneToken.

9 Growth and Innovation Opportunities

- #1 Cost to serve

- OCBC has a cost-to-income ratio of 43.8%, which is higher than the bank’s 42.7% from the previous year (2019) and the industry average of 40%. There was a fall in operational expenses by 4% in 2018 due to lowered staff costs and lessened discretionary expenses. OCBC has dealt with a massive 6% drop in its net interest income. The higher cost-to-income ratio is its primary contributing factor.

- The near-term priority for OCBC is to navigate a low-interest rate economic climate, which has almost eliminated margins on deposits. Competition from upcoming neobanks and fintech is constraining the bank’s ability to compensate by increasing fees.

- Currently, staff cost is US$ 2078 million, which accounts for 27% of its total revenue. The bank witnessed a decrease of 3.2% of overall staff cost from 2019. In 2019, the bank saw a 9% increase in staff cost, mainly due to headcount growth. However, due to low-income levels in 2020, the bank has significantly cut its cost from staff acquisition and management.

- As the bank enters the recovery phase from last year’s income setbacks, there is an opportunity for the bank to reduce this cost base through substantially:

- Replacing man-hours with cognitive process automation of routine and daily back-end tasks

- Adopting a holistic cloud implementation strategy that centralises business for regular activities and eliminates data centre management

- Adding new revenue streams through cross-selling complementary financial products in partnership with fintech companies such as byte-sized insurance, split payments, and micro-investments.

- #2 Transformation of the branch and its branch networks

- OCBC operates more than 600 branches and 37,500 ATMs, constituting a physical infrastructure cost of USD 652 million, i.e., 8.5% of the total revenue and 58% higher than its regional competitors. This data implies that the bank can significantly reduce its cost by focusing on digital transformation to the branch network.

- The bank can achieve about 50% reduction in its overall infrastructural costs by:

- Reducing the overall count of the fully-fledged bank branches based on the low footfall and business volume of a particular branch

- Creating self-service kiosks at fast-moving work complexes, student hangouts and market lanes

- Adopting the FRANK model of branches that promotes a community-based engagement, where individuals can connect with executives, socialise, and access banking services anytime

- Promoting online engagement with the bank’s staff in the form of in-app video conferencing or virtual assistants rather than a physical branch visit

- #3 Customer experience

- Given the bank’s agenda of serving the communities around them and forging lasting customer relationships based on trust and respect, technology investments should now steer toward helping:

- Blind and low-vision clients gain better access to financial services through virtual voice assistants, paperless onboarding, and multi-language services

- Strengthen its omnichannel strategy to integrate a more detailed view of customer preferences and upgrade to ambient multi-design platforms for frictionless scalability and experiences

- OCBC can add interactive functionalities in the FRANK model beyond the FRANK account’s core products, such as customised debit and credit cards for students and executives. Adding new banking solutions will increase the per capita consumption of services to more than five, keeping the brand’s quirky and vibrant touch in mind. These services can include:

- Personalised contextualised data insights on a students’ spending and saving patterns

- A bill prediction feature that manages utilities, subscriptions, etc. with automated alerts on due dates and payments

- Byte-sized wealth management products for quick and hassle-free investments

- Low-cost remittances and foreign currency exchange services

- Micro-insurances for car rides, food deliveries, cycles, pets, etc.

- #4 Employee experience and productivity

- The bank’s digital transformation journey must focus on radically improving the employee experience by channelising their efforts towards:

- Using people analytics to check that unconscious bias does not unfairly impact promotion and compensation decisions.

- Integrating machine learning and data analytics to augment and deliver highly relevant recommendations to its employees

- Increasing the scope of their “We see you” platform via personalised training and development programs for each employee segment, including face-to-face scenario-based workshops, thus improving cohesion within the organisation

- Expanding its employee wellbeing plan with targeted mental, emotional, spiritual, and physical programs

- There should be an incorporation of rewards and benefits beyond insurance, stock options, house rentals, and leases. Ideas include:

- Approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food, and medical support, as well as cleaning drives

- A liaison for mental health and meditative programs

- Extending pre-natal and child-bonding leaves with childcare assistance

- Creating a monthly piggy bank for Netflix, Spotify, gyms facilities and the like

- #5 Migration of workload to the cloud

- A critical pillar for OCBC is using consumer behaviour analytics to identify the latter’s preferences and deliver timely, compelling offers, hence boosting the percentage of cross-selling product conversion.

- To achieve more in-depth insights into customer behaviour, the bank should focus on a robust cloud strategy.

- This cloud-based strategy allows the bank to create a productive environment for developers to seamlessly create, test, and deploy various services through a microservices mesh architecture.

- The bank can easily pilot these services with soft launches and manage success or failures without hitting cost structures.

- The Bank should upgrade the public cloud portion of its hybrid cloud to take on more workload, with the potential for swift uptake. This step will help the bank achieve cost efficiencies and significant modernisation, such as:

- Provide complete end-to-end protection of all confidential data stored in the cloud. This protection enables the bank to maintain the customers’ trust and confidence in obtaining, analysing, and sharing its customers’ personal information.

- Incorporate backup and redundancy capabilities to address security and compliance concerns

- Quick response to market shifts such as black swan events – examples include Covid-19 and the entry of non-bank players to the banking environment with the grant of digital banking licenses

- #6 Neo banking

- OCBC has achieved significant success with FRANK in Singapore, especially with the country’s millennial and Gen Y population. The bank should continue its competitive strength as it needs to offset the risk of customers moving to a competitor, especially with two digital retail banking licenses granted: one to SEA and another to a consortium between Grab and Singtel.

- The bank should also focus on introducing FRANK to the unbanked and underbanked countries of the Asia Pacific, where the millennial and Gen Y populations are high, such as Malaysia, The Philippines, Indonesia, and Thailand. The bank can leverage its existing physical presence in these markets by launching FRANK to quickly onboard customers and create a buzz in the market. With the ease of regulation and a favourable environment for establishing neobanks, FRANK can achieve significant success in the emerging Asian market.

- #7 Artificial Intelligence (AI) in everything

With the bank’s continued effort towards building personalised experiences, it should leverage the multitude of customer data gathered from legacy years to embed finance into customer journeys. Augmented data insights can be built with machine and AI learning:

- Daily tasks automated and optimised using virtual assistants and chatbots, which humans currently manage

- Replace traditional means of identification with facial and voice recognition for a quick and robust security mechanism

- A robust credit-profiling mechanism that incorporates predictive analytics to assess loan credibility beyond the financial statement analysis.

- Cognitive process automation automates a set of tasks that improvises upon their previous iterations, such as monthly bill payments, changing subscription plans based on best offers, alerts for stock updates, etc.

- #8 Cybersecurity

The bank’s effort towards cybersecurity enhances preventive, detective, and response capabilities to manage advanced cyber threats. It currently implements the safe adoption of robotics process automation (RPA) and the Internet of Things (IoT) technologies to create resilience against cyber threats. To ensure a future-proof cybersecurity strategy, OCBC can adopt the following measures:

- Use machine learning to improve the ability of predictive risk intelligence that identifies any emerging risks for the bank

- Experiment with own hypothesis generation via advanced AI tools to assess cyber threats and identify recommended strategies for mitigation

- Invest in cybersecurity talent to perform expertise-driven interpretations of upcoming threats and circumvent control to reduce any vulnerability significantly

- Monitor existing security framework to identify any misconfiguration in firewalls, proxies, and data loss prevention tools

- #9 Society and planet impact

- As a part of the bank’s community-building efforts, it should focus on financial literacy programs that help customers understand the scope of cyber fraud and crimes. These programs also create awareness on the optimum use of data stored, shared, and managed by the bank to build trust and confidence among customers.

- The bank should support zero-carbon transmission efforts by consciously creating environmental-friendly green products such as virtual cards, pulper cards, eco ink, and carbon control press machines.

- The introduction of innovative banking services to encourage the consumption of renewable resources. Examples include low-interest loans and credit facilities for green building and renewable energy financing for SMEs.

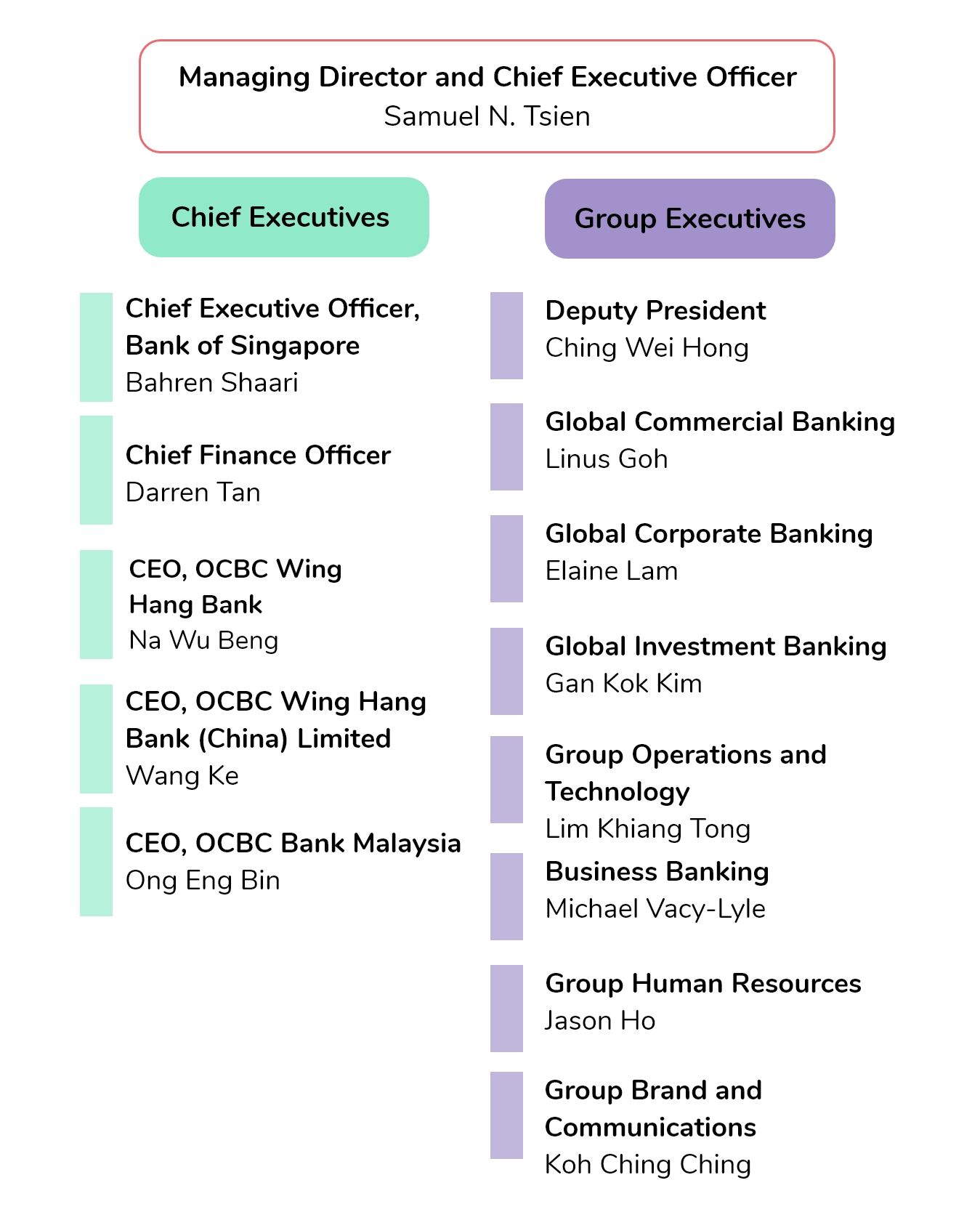

Organisation structure: Leadership

Executive Profile

Mr Samuel N. Tsien, Group CEO

Mr Tsien was appointed to the OCBC Board on 13th February 2014 and re-elected as a Director on 29th April 2019. He was elected the Group Chief Executive Officer (CEO) on 15th April 2012.

He has been a part of OCBC Bank since July 2007, formerly joined as Senior Executive Vice President. He was managing the bank’s corporate and commercial banking business. Mr Tsien became the Global Head of the Corporate Bank in 2008, where his role was to manage the financial institution and transaction banking business. Mr Tsien has 42 years of banking experience. Before joining OCBC Bank, he was the President and CEO of China Construction Bank (Asia) at when China Construction Bank acquired Bank of America (Asia). Former to this, Mr Tsien served as the President and CEO of Bank of America (Asia) from 1995 to 2006. He studied at the University of California, Los Angeles, graduating with a Bachelor of Arts (BA) Honours in Economics from 1995 to 2006. He studied in the University of California, Los Angeles, graduating with a Bachelor of Arts (BA) Honours in Economics

Quotes

- Key trends in the banking industry, OCBC Annual report 2019-20

The adage ‘hoping for the best, prepared for the worst and unsurprised by anything in between’ is particularly apt in the current economic cycle phase.

Regulations and technology continue to impact the way banks do business. It is imperative for us to continuously balance the competing demands of regulations and technology so that OCBC remains competitive and relevant, now and in the future

Mr Vincent Choo, Group CRO

In August 2014, Mr Vincent Choo took the position of Head of Group Risk Management

Mr Choo oversees the bank’s entire risk and governance framework, including credit, technology and information security, liquidity, market and operational risk management. He was formerly a part of Deutsche Bank AG as the Managing Director and CRO in the Asia Pacific. Mr Choo is jointly accountable to Mr. Tsien and the bank’s Board Risk Management Committee. . He has graduated from the University of Akron with a Master of Arts in Economics degree.

Quotes

- Risk management, OCBC Annual report 2019-20

Risk management is becoming increasingly complex. Businesses are no longer just impacted by economic cycles but also by unanticipated event risks. There is also a growing need to address non-financial risk, brought about by evolving consumer demands and behaviours, as well as digitalisation.

- Cyber risks, OCBC Annual report 2019-20

To manage these risks, we have a comprehensive cyber and information risk awareness programme that includes intensive training and testing curricula for our staff. A new guide on the management of data loss incidents was also established to enhance the robustness of data loss prevention controls and measures.

Mr Jason Ho, Group CHRO

Mr Jason Ho joined OCBC Bank as Head of Asset Liability Management in January 2013. After he was appointed Deputy Head, effective January 2015, he assumed the Head of Group Human Resources’ role in July 2015. As a part of the senior leadership at KBC Bank, Standard Chartered Bank, and Volvo Group Treasury Asia, he has acquired 30 years of banking experience. Mr Ho has studied a Bachelor of Business Administration at the National University of Singapore and completed a master’s degree in applied finance from Macquarie University.

Quotes

- OCBC’s HR philosophy, OCBC Annual report 2019-20

Our purpose is to contribute to the vision, mission and financial success of the business by investing in our human capital, technology and HR processes to drive new value and experiences for our employees more effectively. This purpose supports the OCBC Employer Brand Promise of being caring, progressive and being able to deliver a difference.

- Upskilling employees, OCBC Annual report 2019-20

We take a long-term view and invest in upskilling and reskilling our people for the future so that we are well prepared for the ever-changing economy. Taking care of people, for now and the foreseeable future is our business. The more relevant their skills are, the more successful the business will be. We are committed to investing in each person’s career, and not just for their time with us. By equipping our people with key skill sets that prepare them for the future, we are developing a talent pool not just for our company, but for the community at large

Mr Lim Khiang Tong, Group CTO

Mr Lim Khiang Tong has been a part of OCBC Bank since September 2000 and became the Head of IT Management in January 2002. From December 2007, Mr. Tong was the Executive Vice President and Head of Group Information Technology until May 2010, when he assumed the role of Head of Group Operations and Technology.

Lim has over 30 years of management experience in strategic technology development, information technology and banking operations. His experience includes driving regional processing operations, strategic technology initiatives and project management. He holds a Bachelor of Science in (Computer Science and Economics) from the National University of Singapore.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

OCBC Bank, (2020, December 31). Group annual report.

https://www.ocbc.com/assets/pdf/annual%20reports/2019/ocbc_ar2019_english.pdf

OCBC Bank, (2020, December 31). Quarterly Result.

https://www.ocbc.com/iwov-resources/sg/ocbc/gbc/pdf/investors/quarterly-results/ocbc%20fy20%20financial%20results.pdf

OCBC, (2020, December 31). Management Team.

https://www.ocbc.com/group/about-us/our-leadership#management-team

Vinayak Gandhi and Akshita Maruthavanan, Research Interns, contributed to the research in conducting preliminary literature review and conceptualising the article.