Company insights

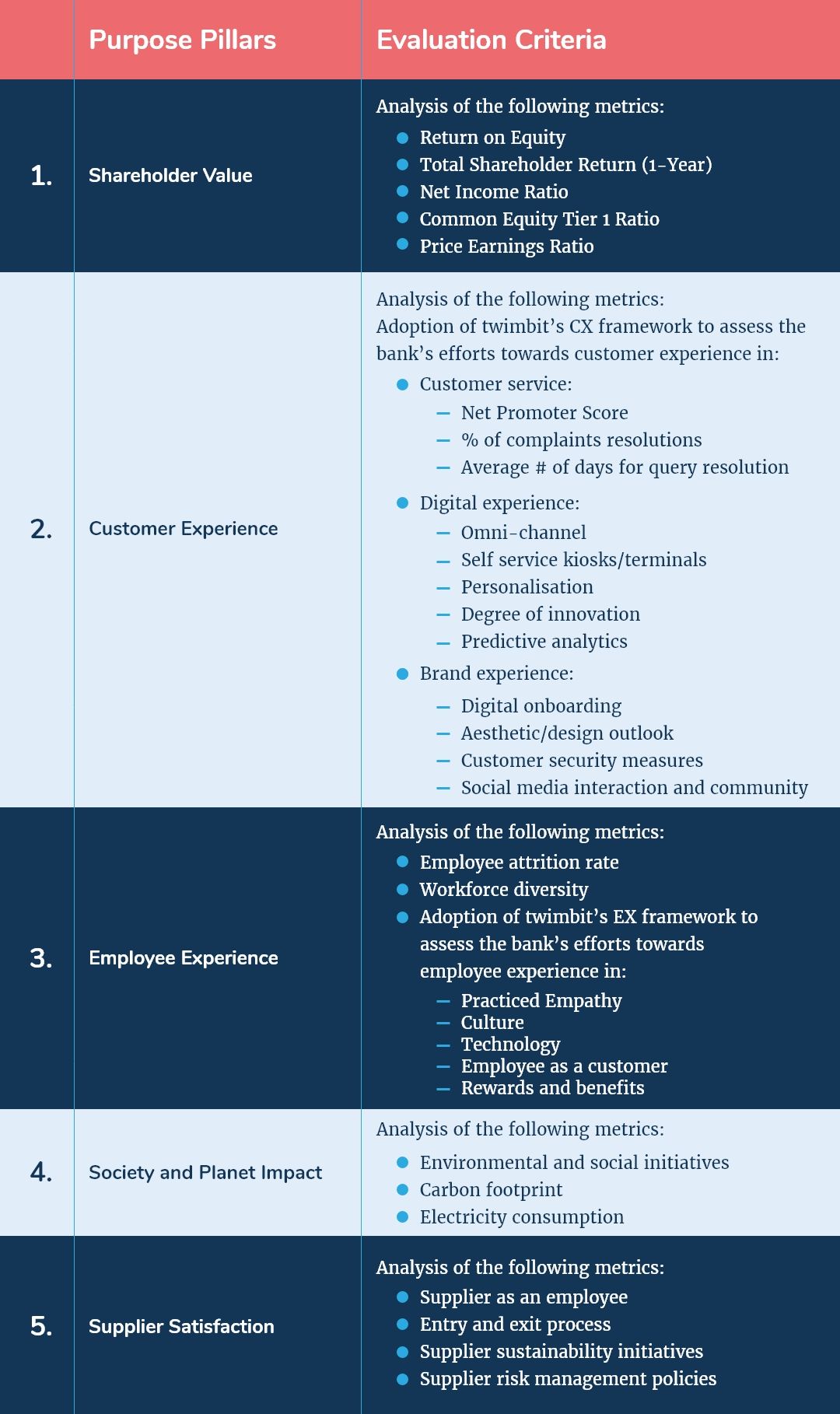

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

United Overseas Bank (Group financials) – An overview as of 31st December 2020

| Bank name | United Overseas Bank (UOB) |

| Headquarters | Singapore |

| Operating income (31st December 2020) | USD 3.1 billion |

| Total Assets | USD 326 billion |

| Employees | 26,000+ |

| Country of operation | 19 |

| Number of branches | 500+ |

| Information and communication technology (ICT) spend (31st December 2020) | USD 440.2 million |

| Bank ranking in a particular country | 3rd in Singapore |

| Number of customers | 5.25 million |

| Market capitalisation (31st December 2020) | USD 44 billion |

| Operating revenue CAGR growth (2016-2020) | 2.72% |

The above financials are as per accounting year 1st January 2020 – 31st December 2020.

The SGD to USD dollar conversion rate used is 0.7564.

Shareholder value (31st December 2020)

| Return on Equity (30th December 2020) | 7.4% |

| Total Shareholder Return (1-Year) | -6.9% |

| Net Income Ratio | 30% |

| Common Equity Tier 1 Ratio | 14.7% |

| Price Earnings Ratio (30th December 2020) | 13.46 |

Awards

| 2020 | Best Cash Management Bank in Singapore by The Asian Banker Best SME Bank in Asia Pacific by The Asian Banker Best Transaction Bank in Singapore by The Asian Banker |

| 2019 | Best Digital Bank (Singapore) by Asiamoney Best Domestic Bank (Singapore) by Asiamoney Asia’s Most Innovative Digital Bank by Global Finance Asia’s Best Bank Transformation by Euromoney Best Transaction Bank by The Asset Asia’s Best Treasury and Finance Strategies by Corporate Treasurer |

UOB and its strategic focus areas

Through its investments, the UOB group claims to have an optimal position for capturing the opportunities inherent in the three megatrends that will drive ASEAN’s growth for decades by:

- Supporting surging economic flows and increased connectivity between ASEAN and Greater China;

- Creating wealth and investment solutions for ASEAN’s burgeoning middle class;

- Riding the digitalisation wave by attracting, serving, and enabling customers through its digital platform, omnichannel reach, and ecosystem partnerships.

- Regional expansion and integration

UOB aims to connect its customers in ASEAN and Greater China seamlessly through sector specialisation and forging strong ecosystem partnerships. It intends to expand its regional network in Greater China, Indonesia and Vietnam apart from further strengthening operations in its core countries- Singapore, Malaysia, Indonesia, Thailand and China. To achieve these expansion goals, the bank focuses on both retail and corporate banking by:

- Corporate banking initiatives:

- Helping businesses achieve sustainable growth by offering more environmentally-friendly financing products, such as green loans

- Building strategic alliances to deepen client relationships across its network

- Helping companies manage the increasing cross-border risks

- Aiding businesses to succeed in the constantly-changing environment by investing in digital capabilities

- Developing products and forging partnerships that accelerate the SME’s e-commerce transformation across all regions

- Retail banking initiatives:

- Provide convenient overseas banking solutions and connectivity to travellers

- Enable multicurrency accounts and transactions across its network

Initiatives taken by UOB to strengthen retail banking in 2019 are:

- UOB introduces Mighty FX in Singapore, which allows customers to review current and historical rates for 11 major currencies and to set their preferred rates alerts or automatic currency conversions

- Launched the Travel Insider, an online travel marketplace that offers cardmembers in Indonesia, Malaysia, Singapore, and Thailand more than 1,000 travel deals across 23 destinations worldwide

- Customer experience

UOB aims to stay attuned to its customers’ needs by adapting to the ever-changing environment and providing them with the right solutions to achieve their financial goals through digital innovation. Steps in place include:

- Engaging customers through an omnichannel approach and giving them access to a global network across 19 countries.

- Transforming its customers’ branch experience by seamlessly integrating technology and testing innovative digital solutions.

- Simplifying and securing digital transactions by forging strategic partnerships with internet service providers and corporate security service providers.

- Providing customised investment and fund solutions to its corporate clients.

- UOB Art of Service Recovery programme aims to equip employees with the skills to resolve customer complaints efficiently.

- The UOB ‘Group Customer Experience and Advocacy (GCEA) function aims to monitor key performance indicators and metrics relating to customer experience at strategic and operational levels.

- Developed a customer review framework that enables business units to assess actionable feedback, propose follow-up solutions, and track targeted outcomes. This framework further helps UOB drive tangible and timely improvements on its products and services to benefit customers.

- UOB, through its omnichannel approach, offers customers choices on how they wish to bank with the bank. The bank continues to strengthen its omnichannel approach by investing in technology capabilities, ranging from Artificial Intelligence (AI), data analytics, and robotic process automation to cloud computing – making banking seamless, simpler, smarter, and safer.

Initiatives taken by UOB in 2020 to enhance its customers’ banking experience by launching innovative products and services are:

- 67 per cent of customers were served digitally in 2020, with two in three customers using digital or multiple banking touchpoints.

- 48 per cent of new individual customers in Thailand and Indonesia, where it launched TMRW, were onboarded digitally, with more than two in five new customers opening banking accounts online.

- Met the customer issue resolution target, with 95 per cent of complaints resolved within five business days in Singapore.

- Express and satellite branches at accessible and convenient locations in Singapore that act as community hubs for young professionals and young family customers to bank and play.

- A Privilege banking centre in Xujiahui, Shanghai, a major commercial centre in the city, to serve high-net-worth customers in China.

- TMRW, the bank’s mobile-only digital bank, is available in Thailand and Indonesia to attract digitally-savvy millennials who prefer to bank on their mobiles, anywhere and at any time.

- Employee experience

UOB provides its colleagues with various training and career development opportunities to ensure that they possess the right skills and mindsets to remain relevant to customers and the banking industry. UOB aims to:

- Drive value-based performance that rewards excellent performance and encourages employees to perform better and promote lifelong learning.

- Equip employees with the right skills needed to compete in a tech-driven world by conducting specialist training and personal development workshops.

- Promote a safe, healthy and harmonious workplace to inspire employees daily.

- Lay out the expectations for its people in the UOB Code of Conduct (Code). The group plans to update its Code periodically to stay relevant with the times, as well as address regulatory requirements and policy changes.

- Reward performance in an objective and fair manner, and support career development through its integrated performance management framework- PEAK, i.e., Plan, Engage, Appraise and Keep Track.

- Build a streamlined leadership development and succession planning framework through the Development Council, which its Group CEO chairs. The framework aims to drive and strengthen the process of identifying future talents for the Bank and ensure meaningful development opportunities are available to them. In addition, the Bank also provides dedicated support in the form of career advisory and coaching to provide identified talents with clarity on their career trajectory.

- Build a prudent, progressive, and high-performing organisation to fulfil and uphold the expectations of its customers through the Professional Conversion Programme (PCP). UOB developed the first PCP in 2017 in collaboration with Workforce Singapore, the Monetary Authority of Singapore (MAS), as well as the Institute of Banking and Finance (IBF). PCP enables branch employees in Singapore to strengthen their digital capabilities and prepares them for future roles in the financial sector.

- Ensure workplace safety, health and wellbeing by providing high-performance work settings focused on ergonomics and comfort. These settings aim to induce collaboration, innovation, productivity, and personal wellbeing for its people.

- Ensure employee wellness by providing them with both inpatient and outpatient coverage. The outpatient coverage in Singapore includes teleconsultations, where employees can consult a doctor virtually through video conference by using a mobile application.

- Provide comprehensive medical and healthcare coverage along with flexible wellness benefits for eligible employees in Singapore, Malaysia, and mainland China, through the HEAL programme (Healthy Employees, Active Lifestyles). In addition, the group also has corporated tie-ups with external providers to offer corporate rates for health and wellness services – such as health screening and gym memberships, to encourage employees to take care of their wellbeing.

- Build a diverse workforce that extends beyond age and gender via UOB Scan Hub. UOB partners with the Autism Resource Centre and SPD30 in Singapore in a structured training programme for persons with special needs to ensure that work processes and office environments are suited to their needs.

Initiatives taken by UOB to enhance capabilities and promote a healthy work environment include:

- Launch of Better U, a group-wide learning and development programme to prepare its colleagues for roles of the future.

- Ensuring a conducive environment for employees by rolling out part-time work arrangements to support those with multiple responsibilities, such as parents who are working, part-time students, and employees looking after elderly parents.

- By the end of 2020, UOB transformed close to 200,000 square feet of office space in Singapore into high-performance workspaces located across various core buildings.

- Women accounted for 61.4 per cent of permanent employees as of end-2020 and 55.0 per cent of all the hires in 2020. Women also held 50.3 per cent of senior and middle management roles.

- Society and planet impact

The four pillars under UOB’s society and planet impact are:

- Drive growth sustainably by contributing economically to communities’ progress and embed environmental, social and governance risks in its risk management policies.

- Keep Customers at the Centre by protecting customer data and privacy through secure and robust systems and practices as well as ensuring fair dealing.

- Develop professionals of principle by establishing high-performing teams and future-focused individuals and promoting work-life harmony.

- Uphold Corporate Responsibility by maintaining the highest standards of governance and risk culture and ensuring regulatory compliance.

Some initiatives taken by UOB to facilitate sustainable development include:

- Establishing a Group Corporate Social Responsibility Policy to ensure that philanthropic activities, community partnerships and volunteering have check-and-balance.

- Organised six eco-excursions in 2019 to educate children and colleagues about environmental sustainability.

Digital Strategy

UOB focuses on developing its digital competencies by focusing on the ethical use of digital capabilities. UOB plans to achieve 75 per cent digitally-registered individual customers with a monthly active rate of more than 35 per cent by 2025. The bank aims to do so by enhancing its digital capabilities and technology systems to simplify banking solutions with the following strategies:

- Investment in agile technologies such as AI and machine learning to offer customised and innovative financial services to its customers

- Strengthen its data analytics and capabilities to become a data-first organisation

- Apply comprehensive data governance and enhance monitoring and risk systems continually to combat cybersecurity threats and maintain a secure banking environment

- Investments in future learning, skills development, market relevancy and employability

UOB Mighty: The bank’s all-in-one mobile banking app available in Malaysia, Singapore and Thailand:

- In 2020, UOB extended Mighty Insights from Singapore to Malaysia. Mighty Insights became an industry-first AI-based digital banking service that uses advanced data analytics, machine learning and pattern recognition algorithms to provide customers with hyper-personalised insights into their savings and expenses.

- In Malaysia, Singapore and Thailand, UOB Mighty also integrates national e-payment initiatives, namely DuitNow, PayNow, and PromptPay, to make cashless payments more convenient.

TMRW by UOB:

- In 2019, UOB launched TMRW, ASEAN’s first mobile-only digital bank, in Thailand. In 2020, TMRW expanded into Indonesia as well.

- TMRW aims to make banking simpler, more transparent, and more engaging for digitally-savvy customers. It personalises the banking experience for each and every individual, from account opening to their day-to-day needs.

- With a data-centric operating model, TMRW translates transactional data into actionable ‘Smart Insights’ that make the banking experience for customers interesting and fun, while enabling them to be smarter at saving and spending.

- TMRW also incorporates payment options such as PromptPay in Thailand and the QR Code Indonesia Standard to ensure that its customers have access to the payment networks of their choice.

Initiatives taken by the UOB group to strengthen its digital strategy:

- UOB GetBanker: An app that enables a property buyer or an agent to search for a mortgage banker based on the property’s type, location, and price.

- Mighty Fx: It offers customers in Singapore the ability to review current and historical rates for 11 major currencies and set their preferred rates alerts or automatic currency conversions.

- UOB Jonus: A chatbot used to engage candidates and onboard the right talent seamlessly and quickly.

- UOB Infinity: The new digital banking service for corporate clients to manage their day-to-day banking transactions in a simple and personalised manner.

- UOB BizSmart: An integrated set of business solutions that helps small business customers automate their day-to-day administrative processes for better productivity.

- Collaborated with Stellavingze Global (a women empowerment organisation in Malaysia) to offer wealth management solutions to its members, as well as easy instalment payment and travel protection plans.

- Partnered with Fave, Fitbit Pay, Grab, Shopee, Singapore Airlines, SP Group, and Visa to make its customer’s digital payment and rewards redemption experience easier.

- Partnered with StarHub to develop and provide digital solutions for SMEs.

- Signed a Memorandum of Understanding with Shopee to offer customers more value when using the bank’s flagship UOB One credit and debit cards.

- Partnered with The FinLab to launch the Jom Transform Programme (Malaysia) to help local businesses digitalise their operations.

IT Strategy

Over the last six years, the bank has invested USD 2 billion in information technology to develop the internal and external banking infrastructure. The bank plans include continued reinvestment to maintain efficiency in its operational activities and gradually optimise the cost-to-income ratio.

- UOB plans to build an embedded finance ecosystem for its customers through technology-based partnerships and collaborations.

- UOB aims to harness customer insights through AI and machine learning as it enables the bank to build customer-centric propositions and sustainable relationships.

UOB and its ICT contracts

- Partnered with VMware to enable safe and effective remote working for its team of IT developers.

- Co-developed an AI-powered anti-money laundering (AML) solution with Singaporean regtech company Tookitaki.

- Partnered with SAS Europe to attack computation problems with a high-performance analytics solution that combines grid computing, matrix-based calculations and in-database analytics.

- Collaborated with Intel to use leading technology and advanced data analytics to provide greater clarity about transactions made across countries.

- Implemented Personetics’ AI-powered personalised insights to offer bite-sized information to the bank’s TMRW customers.

- Collaborated with Stellavingze Global (a women empowerment organisation in Malaysia) to offer wealth management solutions to its members alongside easy instalment payment and travel protection plans.

- Collaborated with Meniga to advance data enrichment and categorisation capability to offer real-time updates on savings and expenses.

9 Growth and Innovation Opportunities

- #1 Cost to serve

- UOB has a cost-to-income ratio of 45.6%, which is higher than the bank’s 44.6% from the previous year (2019) and the industry average of 40%. The increase in the cost-to-income ratio is largely due to the bank’s expenditure increase on technology investment and its bank personnel acquisition. In addition to this, the bank has dealt with a significant 8% drop in its net interest income along with a 2% decrease in net fee and commissions. Hence, these factors contribute to the higher cost-to-income ratio compared to the previous year.

- The bank did make efforts to tighten its spending in the recovery phase from Covid-19 with a decrease in operational expenditure by 6%, from USD 3.3 billion in 2019 to USD 3.1 billion in 2020. However, with the sharp decline in non-interest income, it could not control the efficiency’s overall impact.

- In 2020, UOB’s staff costs were at USD 1,892 million, which accounts for 25.7% of its total revenue. The bank can further control its staff costs by:

- Automating iterative back-end tasks by using cognitive-process automation to save man-hours.

- Identifying repayment risk in loans and attrition risk in deposits by using predictive behavioural models to continuously revise its interest-rate risk models.

- Controlling data management costs by continuing investments in a robust cloud infrastructure.

- With a low-interest macroeconomic environment and rising competition from emerging neobanks, the bank’s near-term priority should be to come out of the low-interest rate environment without taking a serious hit on its net interest margin. It can sustain its net interest margin levels by:

- Continuing to focus on regional expansion in the ASEAN region by leveraging the omnichannel product delivery approach.

- Leveraging on its wealth management fee and focusing on maintaining competitive net transactional fee levels.

- #2 Transformation of the branch and its branch networks

- As UOB has more than 500 branches and 16,500 ATMs, its physical infrastructure is considerably low compared to peers; it accounts for 3.3% of the total revenue. The bank can further marginalise the infrastructure cost with a continued focus on robust bank transformation across all countries, especially Singapore, its core operation base.

- It should replicate the operational model of TMRW, its millennial centric neobank in Singapore, as well as reduce the physical footprint with its existing strategy of express and satellite branches.

- Only 40% of its Singapore customers use digital touchpoints for interacting with the bank and prefer physical interface through a branch. The bank should continue its efforts in actively migrating these customers to use digital channels by:

- Promoting online engagement with the bank’s staff in the form of in-app video conferencing or virtual assistants rather than a physical branch visit

- Replacing ATMs with ITMs (Interactive teller machines), thereby increasing the ambit of its self-service kiosks to offer a wide range of services like money transfers, address and email updates, cheque encashment, large check deposits and withdrawals that could previously be accessible only via traditional physical branches.

- #3 Customer experience

- Enhancing the omnichannel experience: The omnichannel strategy is already at the bank’s core platformification strategy, but the bank can make the phygital (physical and digital) experience more hassle-free by:

- Introducing a real-time virtual chat assistant that is well versed with the branch’s regional language and can adapt to the variable nature of customer queries. The real-time virtual chat assistant will also help in reducing complaint resolution time for basic to complex cases from 5 business days to 1-2 business days in Singapore.

- Adopting a ‘pay for what you use’ consumption model in its product and service offerings to give customers the flexibility to seamlessly switch to other products as and when their preferences change.

- Building an immersive customer experience: UOB has already adopted customer analytics in the UOB Mighty app to give customers contextualised and personalised data insights on their saving and spending patterns, periodic cash flows, and subscription management. UOB can make its customer experience more intuitive by:

- Offering versatile micro-investment products to help the customer better manage their idle savings.

- Pitching low-cost loan products by leveraging on the customer insights it receives from AI capabilities.

- #4 Employee experience and productivity

- UOB must practice a human-centric and prototype-driven approach to build an employee force that optimally fulfils customer expectations and simultaneously provides a superior employee experience.

- UOB launched Group U, a group-wide learning and development programme to prepare its colleagues for the roles of the future. To increase the effectiveness of this training and development programme, UOB should consider incorporating the following measures:

- Introduce design thinking to maximise the ambit of learning, improve employee interaction and engagement

- Break down its training modules into byte-size content forms so that the employees can complete modules at their own pace and according to their experience and knowledge

- Use people analytics to get contextualised insights on its learners’ performances and their preferred learning styles for setting internal learning benchmarks

- To improve the financial well-being of its employees, UOB should go beyond basic financial aids like staff loans, special allowances, reimbursements and insurances to include things like:

- A comprehensive AI-enabled compensation mechanism to ensure fair and equitable distribution of promotion and fringe benefits

- A liaison for mental health and meditative programs

- Providing hassle-free student loans to new hires for controlling attrition rates among the said hires, hence increasing employee loyalty

- #5 Migration of workload to the cloud

The cloud infrastructure for UOB is jointly developed by VMware and AWS and majorly focuses on the bank’s strict security requirements. UOB can further expand its cloud attention towards:

- Breaking down and simplifying structured and unstructured data sets across all business segments and migrating them to a dedicated cloud storage

- Applying advanced analytics, AI and machine learning on the available data sets to get meaningful segment-specific insights to identify operational inefficiencies

- Adopting a customer-centric cloud-based strategy that allows the bank to create a productive environment for developers to seamlessly create, test, and deploy various services through a microservices mesh architecture. The bank can easily pilot these services with soft launches and manage success or failures without hitting cost structures

- Provide complete end-to-end protection of all confidential data stored in the cloud. This protection enables the bank to maintain the customers’ trust and confidence in obtaining, analysing, and sharing its customers’ personal information.

- Responding to market shifts, such as black swan events – examples include Covid-19 and the entry of non-bank players to the banking environment with the grant of digital banking licenses

- #6 Neo banking

- Apart from TMRW- its millennial-centric neo banking platform in Thailand and Indonesia, UOB is planning to launch a digital-only platform, UOB infinity, for Singapore customers. The bank can learn from the success of TMRW and apply it to attract customers to the UOB Infinity platform. It can further expand TMRW’s regional reach to Singapore and attract the country’s growing millennial and Gen Z population. The gamification of TMRW’s platform is an absolute “hit” among the tech-savvy population. The neobank’s features, such as its customisable dashboards, personalised cash management suggestions and a user-friendly interface, will bring in a competitive edge over other upcoming neobanks in Singapore.

- UOB can further incorporate the following elements in its neo banking strategy:

- A transparent and simple fee structure without any hidden fees for debit Visa cards & MasterCard as well as foreign currency fees when using an overseas credit card.

- Enable multicurrency accounts with zero-to-minimal cross-border remittance fees

- Introduce short-term interest-free loan products or loans at lower rates than its current traditional proposition to match the customer acquisition strategies of emerging neobank competitors

- Gamify various customer touchpoints such as awarding badges with the increased use of products, giving discount coupons to loyal customers, and a leaderboard between friends and colleagues based on product purchases and highlighting trending products

- #7 Artificial Intelligence (AI) in everything

- UOB incorporates AI in multiple aspects, such as data analytics in its wealth advisory tools to recommend suitable investment solutions, build anti-money laundering solutions, and create byte-size personalised insights for its neobank customers. To further broaden the application of AI, UOB can focus on the following areas:

- Actively use virtual assistants and chatbots to resolve customer queries at various touchpoints, reducing the need for human interaction and helpdesks.

- Innovating its product offerings by combining its existing AI framework, product innovation capacities and customer data insights and experimenting in making hyper-personalised banking solutions.

- Enhancing existing data quality and unifying the data sets by supporting proactive and reactive data maintenance to make the data silos more conducive for machine learning and AI algorithms.

- #8 Cybersecurity

UOB’s cybersecurity capabilities are focused on enhancing its operating models to strengthen the overall security framework and keep pace with the dynamic threat landscapes. The bank should continue its focus on making its security policy more adaptive by:

- Using predictive analytics in existing security frameworks to identify risk trends and optimise its operational model to pre-empt risks.

- Evaluating and benchmarking its existing security standards and aligning them with its existing risk appetite to keep security practices up to date.

- Applying RPA (Robotic process automation) to automate iterative security functions like threat monitoring, identity access management, and vendor management.

- Experiment with own hypothesis generation via advanced AI tools to assess cyber threats and identify recommended mitigation strategies.

- Investing in cybersecurity talent to perform expertise-driven interpretations of upcoming threats and circumvent control to reduce vulnerability significantly.

- #9 Society and planet contribution

- The bank’s sustainability strategy is in line with the Singapore Exchange (SGX) Sustainability Reporting Guide and the Global Reporting Initiative (GRI) Standards in governance and compliance, health and well-being of its employees, diversity, and inclusion, as well as talent acquisition.

- UOB can focus on the following areas to make its ESG (Environmental, Social and Governance) framework more inclusive:

- Use green products such as virtual cards, pulper cards, eco ink, and carbon control press machines to reduce carbon emissions by 15% – 20% (as achieved by fellow competitors), thereby earning their customers’ credibility and transitioning towards a lower-carbon economy.

- Introduce innovative banking services to encourage renewable resources consumption, such as low-interest loans and credit facilities for green building and renewable energy financing for SMEs.

- Encourage its employees by providing paid leaves to employees who volunteer for different causes and initiatives undertaken by the company, including the UOB Heartbeat Run/Walk.

- Initiate an effective climate risk management system that accounts for the mitigation of harms caused to the environment by the bank’s activities and controlling the financial risk exposure of UOB while financing green projects.

Organisation structure: Leadership

Executive Profile

Wee Ee Cheong

Deputy Chairman and Chief Executive Officer

Wee Ee Cheong got his bachelor’s degree in Business Administration and subsequently master’s degree in Applied Economics, both from the American University, Washington DC. Wee joined United Overseas Bank in 2000, was appointed deputy chairman and president. He has been CEO of UOB since April 2007.

Quote

Even with the array of digitalised banking options, many of our customers prefer to make their significant financial decisions in person with their bankers. In Singapore, 39 per cent of our customers use our omni-channel touchpoints.

Wong Kim Choong

Chief Executive Officer, Malaysia

Mr Wong stepped as the Director and Chief Executive Officer of UOB Malaysia on 1 October 2012. He has 36 years of experience in the banking industry and started his career with UOB in 1983, where he committed himself for over 14 years. During his tenure with UOB, he held various management and senior roles across Corporate Banking, Commercial Banking and Consumer Banking.

Quotes

- Banking during COVID, 24 June, 2020

At UOB Malaysia, we care for our communities and believe in giving to those in need, especially at a time when everyone is worried about their livelihoods, health and safety. The impact of the pandemic has been far-reaching and will continue to have prolonged effects on all communities, particularly children and families from challenging socio-economic backgrounds. Through the UOB Heartbeat COVID-19 Relief Fund, we hope to help these vulnerable groups of children and their families by providing them with the daily necessities they need to tide over these difficult times.

- Customer-Centricity, 15 July, 2020

“UOB has always stood by our customers over the years, and we will continue to do what is right by them in today’s extremely trying times. We have been proactively working with them to come up with the right solutions in meeting their cash flow requirements and aim to ensure their financial needs are supported.”

Lee Wai Fai, Group

Chief Financial Officer

Mr Lee started his journey at UOB in 1989. He spearheads the Group Finance, Investor Relations, Central Treasury, Data Management, Corporate Investments, Corporate Real Estate and Asset Management functions. He is an alumnus of the National University of Singapore and Nanyang Technological University, Singapore and has spent over three decades absorbing the ins and outs of the banking industry.

Dean Tong Chee Kion

Group Chief Human Resources Officer

Mr Tong is a relatively new addition to the UOB team as he joined UOB in 2018. He is the Group Head of Human Resources as of now. Mr Tong is an alumnus at Wharton School, University of Pennsylvania, USA, where he did his Master’s in Business Administration. He has more than 20 years of leadership, talent and transformation project experience across Asia, Europe and the Americas in the financial services, consumer goods and telecommunications industries.

Susan Hwee Wai Cheng

Head-Group Technology and Operations

Ms Hwee joined UOB in 2001. She is the Head of Group Technology and Operations, overseeing the global technology infrastructure and operations for the Group. She is an alumnus of the National University of Singapore, where she did her Bachelors in Science. Ms Hwee has more than 30 years of experience in banking technology and operations.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

United Overseas Bank Limited, (31st December 2019). Annual Report 2019

https://www.uobgroup.com/investor-relations/assets/pdfs/investor/annual/UOB_Annual_Report_2019.pdf

United Overseas Bank Limited, (31st December 2020). Financial Report 2020

https://www.uobgroup.com/investor-relations/assets/pdfs/investor/financial/2020/gp-financial-4q-2020.pdf

Lam Tania,(2020, June 24). Bank raises RM300k for charity. New Sarawak Tribune

https://www.newsarawaktribune.com.my/bank-raises-rm300k-for-charity/

Akshita Maruthavanan and Vinayak Gandhi, Research Intern, contributed to the research in conducting preliminary literature review and conceptualising the article.