Company Insights

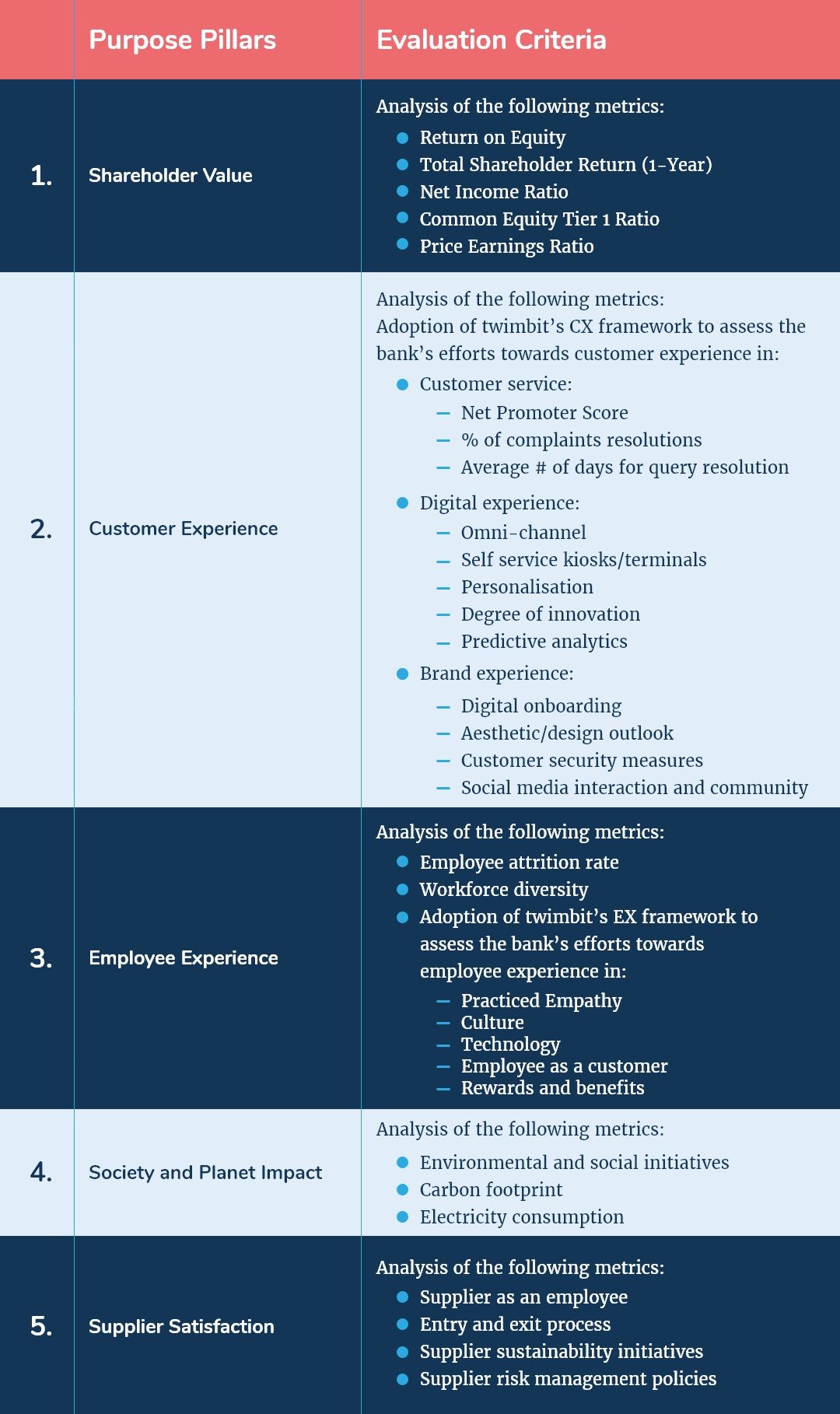

twimbit Purpose Benchmark

Source: Refer to the methodology in Appendix A below

Westpac Banking Corporation (Group financials) – An overview as of 30th September 2020

| Bank name | Westpac Banking Corporation |

| Headquarters | Sydney, Australia |

| Operating income (30th September 2020) | USD 14.4 billion |

| Net Profit after tax (30th September 2020) | USD 1.6 billion |

| Total Assets | USD 653.3 billion |

| Employees | 40000 |

| Country of operation | 7 |

| Number of branches | 1,204 |

| Information and communication technology (ICT) spend (30th September 2020) | USD 1.8 billion |

| Bank ranking in a particular country | 3rd in Australia |

| Number of customers (Retail, SME, Wholesale, and Wealth) | 14.1 Million |

| Market capitalisation (30th September 2020) | USD 43.7 Billion |

| Operating revenue CAGR growth (2016-2020) | -0.64% |

Note:

Australia’s accounting period follows a cycle from October-September. The above financials are as per accounting year 1st October 2019– 30th September 2020.

The AUD to USD dollar conversion rate used is 0.71641.

Shareholder value (30th September 2020)

| Return on Equity (30th September 2020) | 3.36% |

| Total Shareholder Return (1-Year) | -12.6% |

| Net Income Ratio | 11.35% |

| Common Equity Tier 1 Ratio | 11.13% |

| Price Earnings Ratio (30th September 2020) | 27.83% |

Awards

| 2020 | Aspect Recognition Awards 2020 Advancement Award in recognition of the innovative autism hiring program by Westpac, Tailored Talent Green Building Council of Australia Awarded the highest scoring 6 Star Green Star rating in Australia for the Group’s fit-out at Tower Two of Barangaroo’s International Towers, Sydney. |

Westpac and its strategic focus areas

The strategic priorities for Westpac revolve around simplifying core businesses, redefining the customer experience, and engaging the workforce to improve their overall performance.

- Customer experience

Westpac is simplifying processes and operations to provide a more seamless customer experience. It is also trying to migrate existing customers to new and more flexible products.

- Customer grievance management: Westpac aims to reduce customer pain points by constantly improving its complaint management system.

- Customer remediation: The company is committed to reviewing products, processes, and policies to remediate and refund customers where necessary.

- Product simplification: Westpac is rationalising products and streamlining processes to make services easier for customers

Initiatives taken by Westpac to improve customer experience in 2020:

- Launched ‘Resolve’, a centralised customer complaints management platform, and have already reduced the complaint resolution time from 9 days in FY19 to 6.5 days by the end of September 2020

- Provided USD 200.5 million worth of refunds to over 2 million customers in FY2020

- Removed 40 out of 200 fees from over 40 systems and aims to remove 20 more in FY2021

- Introduced a chatbot for coronavirus-related queries for Australian customers

- Created a new digital process for New Zealand customers, which includes digital credit submissions, complaint capture and COVID assistance-related online forms

- Provided elderly customers with card access and opening of new accounts digitally, so they do not have to enter the branch

- Business strategy

The company’s business strategy for 2021 aims to fix shortcomings by transforming the risk management framework, simplifying activities by exiting non-core businesses, and building customer loyalty.

Key business strategies for 2021 are:

- Business consolidation: Exiting non-core businesses, consolidating international locations and focusing on customers in Australia and New Zealand to add additional capital strength

- Mortgage growth: Streamlining loan repayments, mortgage assessment criteria, and operational issues in processing applications

- Operational efficiency: Improving productivity by resetting the cost base

Initiatives taken by Westpac to support business strategies in 2020:

- Despite regulatory changes lifting capital requirements, the bank’s large loan and deposit books continue to deliver a robust net fee income.

- Saved over USD 286.5 million of costs as an offset from inflationary cost increases, higher risk and compliance costs, and additional resources devoted to COVID-19 response

- Employee experience

Westpac aims to improve services by constructing a highly motivated and engaged workforce:

- Strengthening risk culture: Ensuring everyone identifies the risks they are responsible for and can proactively address risks as they emerge

- Maintaining workforce wellbeing: Creating a secure, flexible, and supportive workplace to attract, retain and develop people

- Upskilling workforce: Providing employees with access to learning opportunities to help build the skills needed for the workforce of the future

Initiatives taken by Westpac in 2020 to strengthen their employee experience:

- Launched an online tool to access the divisions’ current risk culture in comparison with the target

- Rolled out a new risk fundamentals training program for all employees

- Devised a program focusing on creating a simpler and stronger business with high-performing teams, where everyone knows their role in delivering for customers. This program led to an increase in employee commitment from 73% in September 2020 to 72% at the end of FY2019.

- Society and planet impact

Every year, Westpac, through its sustainability materiality assessment process, identifies the business opportunities and challenges that matter most to its stakeholders. This assessment helps the bank form its approach towards creating a long-term sustainable value for customers, employees, suppliers, shareholders, and communities.

- Climate change strategy

- Provide finances to back climate change solutions

- Support businesses that manage their climate-related risks

- Help customers navigate their climate change risks

- Improve and disclose the bank’s climate change performance

- Advocate for policies that stimulate investment in climate change solutions

- Supporting communities in need: As an integral service provider in the communities operated, the bank aims to help those in need, including in times of emergency and recovery. Westpac also supports initiatives that address complex societal and economic issues.

Initiatives taken by Westpac in 2020 to strengthen their contribution towards the society and planet:

- Impact of the bank’s climate change strategy:

- Increased lending to climate change solutions, taking total committed exposure to USD 7.2 billion, thereby exceeding their target of USD 7.1 billion by 2020

- Reduced emissions intensity of its lending to the electricity generation sector from 0.36 tCO2-e/MWh in 2017 to 0.25 tCO2-e/MWh in 2020, also exceeding the company’s 2020 target of 0.30 tCO2-e/MWh

- Provided over 3,400 natural disaster relief packages to assist customers affected by floods, bushfires and other disasters over the year

- Commenced renewable electricity supply from Bomen Solar Farm in the fourth quarter of 2020. The bank expects to source over 45% of its annual electricity requirement from renewables in 2021 and are on track to meet fully meet this commitment by 2025.

- Supporting local communities:

- Over USD 107.4 million placed in community investment

- More than one million participants in financial education

- Westpac Foundation grants to social enterprises and helped create 719 jobs for vulnerable Australians

Digital Strategy

Westpac aims to modernise and simplify its digital proposition and streamlining processes to ultimately construct a better risk management system and provide state-of-the-art customer service.

- Centralised data management: Constantly aim to improve data quality and data management by introducing a more central oversight, as well as implementing data quality measurement and a new data certification process.

- Revamp mobile interface: Preparing to roll out a new and simpler mobile banking app in collaboration with Google and Apple

- Dedicated customer management: With market-leading front-end systems, Westpac is focusing on the development of its Customer Service Hub

Initiatives taken by Westpac in 2020 to become a more digitalised bank:

- Simplifying the balance sheet portfolio of corporates through the company’s Institutional Bank digital banking platform

- Digitising the bank guarantee process by launching a new blockchain technology

- As a part of the Open Banking initiative, allowing access of data to third parties

IT Strategy

Westpac is redoubling efforts to reduce IT complexity by prioritising the upgradation of its technology infrastructure:

- Implementing 50 changes to the mortgage process to streamline applications

- Simplifying the global transaction service product platform and refocusing on core capabilities

- Spent USD 1,893.4 million on technology, which is USD 136.1 million or 18% higher than 2019 numbers. This increase was mainly due to:

- Higher amortisation, including the full-year impact of the Customer Service Hub

- Higher telecommunication and software licensing cost, mainly due to an increased capacity and the capability to support staff that work from home

Break down of the company’s Technology expenditure (USD millions)

| Amortisation and impairments of software assets | 695 |

| Depreciation and impairments of IT equipment | 195 |

| Technology service | 500 |

| Software maintenance and licensing | 285 |

| Telecommunication | 155 |

| Data processing | 64 |

| Total | 1,894 |

Westpac and its ICT Contracts

- 10x Future Technologies:

- Westpac signed an agreement with UK vendor 10x Future Technologies to build a standalone banking-as-a-service platform.

- The bank plans to make a minority equity investment in 10x as part of the agreement.

- This initiative will involve building a platform that will enable the company’s institutional customers and fintech partners to distribute Westpac banking products to their own customers.

- Oracle

- Plans to introduce a centralised customer service hub that would sit in the middle of the banking group’s IT infrastructure.

- Oracle Customer Hub will bring together all the business logic and data that currently sits in separate systems at Westpac. This move will provide the bank’s staff with a holistic customer view.

- Westpac says that the core solution utilises the Oracle Banking Platform with development primarily focused on integrating the platform into the existing Westpac and St. George ecosystem.

Westpac and its fintech business investment

| New technology capabilities | |

| Kasada | Enterprise cybersecurity company that protects businesses from malicious bot attacks |

| Codelingo | Enabling software development teams to scale processes and improve code quality |

| Polychain Capital | A fund of funds for cryptocurrency and blockchain technology |

| Doshii | Connects ordering apps, payment devices, loyalty and reservations platforms to any point of sale |

| Indebted | Digitised debt collection, leveraging modern communications, automation and machine learning |

| SLYP | Smart receipts that automatically link purchase receipts to a customers’ bank accounts |

| Forte | Pioneering a new asset class called Tradeable Income-Based Securities (TIBS) |

| Immutable | Creating real-game assets for developers, using blockchain technology |

| Data, AI and Analytics | |

| Hyper Anina | A natural-language AI system for data analysis targeting relatively simple business queries that comprise 70% of an analyst’s work in a large organisation |

| Basiq | Open Banking API platform that provides connectivity to over 100 financial sources across Australia and NZ |

| Data Republic | A trust framework and secure platform that allows users to exchange data safely and securely |

| Curious Thing | Conversational voice-based AI for digital interviewing, powered by machine learning |

| Akin | An AI company that integrates neuroscience into its platform, creating a capability that not only manages complex problems but can form intrinsic relationships with humans |

| Flybits | The AI-powered, context-as-a-service platform to deliver personalised experiences to customers |

| Fillr | Standardises mobile forms into an easily readable format and fillable at the tap of a button |

| Kepler Analytics | B2B platform for physical retail stores that provides insights through their AI engine and in-store sensors |

9 Growth and Innovation Opportunities

- #1 Cost to serve

- Westpac suffered a 66% drop in their net profit, i.e., USD 4,860.1 million in 2019 to USD 1,640.5 million in 2020. The sharp decline in net profit results from unfavourable operating environments, including low-interest rates, materially high impairment charges and low non-interest income due to COVID-19.

- Another key factor contributing to an extremely high cost-to-income ratio of 63% was the remediation costs, asset write-downs, as well as high risk and compliance costs arising from Australian Transaction Reports and Analysis Centre (AUSTRAC) charges:

- Impairment charges of USD 2,276.7 million, reflecting an increase in provisions for expected credit losses due to COVID-19

- Tax in provisions for customer refunds of USD 1,033 million

- A civil penalty of USD 931 million

- Additional provisions for customer refunds, repayments, associated costs, and litigation items of USD 315.2 million, after-tax

- Westpac must undertake stringent measures to sustain itself in the low-interest environment while managing high-cost implications and the impact of the AUSTRAC settlement. It can focus on the following key areas to optimise the cost structure:

- A sound net interest margin management in a low-interest rate climate is achievable by identifying repayment risk in loans and attrition risk in deposits. The bank can use predictive behavioural models to continuously revise its interest-rate risk models and hedging strategies.

- Increase focus on non-interest income and complementary revenue streams to offset the impact of high impairment charges.

- Investing in intelligent document processing (IDP), powered by robotics process automation (RPA) and AI. This step involves character recognition and an integrated customer verification ability, reducing the manpower cost of conducting customer remediation.

- Implementation of transaction-level transparency through RPA-enabled audit trails for red-flagging any high-cost inflexions

- Divestments in non-core specialist businesses, bringing in negative cash earnings of USD 362.5 million. These divestments include superannuation, wealth platforms, investments, auto finance, general insurance, life insurance, and lenders mortgage insurance.

- #2 Transformation of the branch and its branch networks

- Westpac currently has over 900 branches and 1400 ATMs. Their physical infrastructure cost accounts for 5% revenue, which is about 20% higher than their regional competitors. This data implies that the bank has the potential to reduce its cost by focusing on the digital transformation of its branch network by:

- Reducing the overall count of fully-fledged bank branches based on low footfall and business volume of a particular branch

- Creating self-service kiosks at fast-moving work complexes, student hangouts and market lanes

- Shutting down fully operational bank branches with negative cash earnings in Fiji and Papua New Guinea and replacing them with self-service kiosks to support the customers’ basic banking needs

- Promoting online engagement with the bank’s staff in the form of in-app video conferencing or virtual assistants, rather than a physical branch visit

- Initiating limited working hours across regional branches

- #3 Customer experience

- Westpac requires a deep scrutinisation of its existing product portfolio to suit the needs of customers. The bank must build immersive experiences with strong transactional transparency of costs to gain customer trust in its offerings.

- The bank’s existing digital framework focuses only on supporting customers with their transactional needs rather than building personalised engagements on physical and digital platforms. Westpac must invest in understanding the customers’ behavioural patterns, life journey needs, and spending areas through AI and machine learning tools to create unique persona-based product packages. The bank has already made progress in adopting AI tools such as the partnership with Flybits – a context-as-a-service platform for delivering personalised experiences.

- The bank should provide an all-inclusive multi-generational customer experience to cater to the growing Gen Y, millennial population and the existing older generations.

- #4 Employee experience and productivity

- The bank’s digital transformation journey must focus on radically improving the employee experience by channelising its efforts towards:

- Using people analytics to check that unconscious bias is not unfairly impacting people promotion and compensation decisions.

- Integrating machine learning and data analytics to augment and deliver highly relevant recommendations to its employees for the customer service hub.

- Design personalised employee upskilling programs based on the employee level and adopting effective leadership development coaching to prepare them for future roles.

- Expand its employee wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Giving their employees the option to work on cross-department projects for lateral career advancements

- Periodical career breaks and approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food and medical support work, as well as cleaning drives

- Extending pre-natal and child-bonding leaves with childcare assistance

- #5 Migration of workload to the cloud

- Westpac uses hybrid-platform-as-a-service (HPaaS), which aims to combine public and private cloud environments with its key strategy of migrating data to a new offsite private cloud environment operated by IBM.

- The bank’s efforts skew towards a regulatory compliance and customer service hub with cloud adoption by:

- Using consumer behaviour analytics to reduce complexity, costs and respond faster to customer needs by delivering timely and compelling offers, thus winning back their trust

- Providing complete end-to-end protection for all confidential data stored in the cloud. This protection enables the bank to maintain its customer’s trust. At the same time, there is confidence in obtaining, analysing and sharing the customer’s personal information.

- Incorporating backup and redundancy capabilities to address security and compliance concerns

- Enabling quick response to market shifts, such as black swan events – Covid-19 and the entry of non-bank players in the banking environment

- As the custodian of enormous legacy data, Westpac can become a competitive differentiator by harnessing data real-time on the cloud

- #6 Neo banking

- Westpac has made significant fintech investments to upscale its digital channel and create a mobile banking application, including third-party integration with Afterpay (buy-now-pay-later model) and SocietyOne (low-cost lending capabilities).

- The bank can reposition its banking application to one that resonates with the growing digital-savvy population. It can further strengthen the capability of its in-app virtual assistant

- Westpac can also evaluate the strengths of an upcoming neobank and its alignment with the incumbent’s strategy for a possible acquisition. The bank will be able to attract synergies in the form of a full-proof platform and have an established customer base, similar to an approach taken by the National Australia Bank (NAB) and its acquisition of 86400 Holdings Ltd.

- #7 Artificial Intelligence (AI) in everything

- Westpac has its AI strategy based on establishing third-party partnerships with those who have proprietary technology to tackle specific use cases (In reference to fintech business investments between Westpac and ICT Contracts).

- Westpac employed cognitive process automation, one that mechanises a set of tasks that in turn improvises on its previous iterations, such as monthly bill payments, changing subscription plans based on best offers, and alerts for stock updates, among others.

- The company automates labour-intensive, error-prone, and complex risk processes that deal with high volumes of structured and unstructured data for its cost-effectiveness.

- Incorporating predictive threat monitoring and risk detection mechanisms for fraud and money-laundering, insider-threat, cyber and compliance risks.

- #8 Cybersecurity

- The bank has put considerable efforts to tighten its cybersecurity measures, including partnerships with third-party cybersecurity specialists. It currently implements enterprise-wide bots to manage malicious attacks. To ensure a future-proof cybersecurity strategy, Westpac can adopt the following measures:

- Incorporate predictive risk intelligence using analytics and AI to provide advance notice of emerging risks, increased awareness of external threats, and improve the bank’s overall understanding of its risk exposure and potential losses.

- Measure its risk performance by facilitating the development of critical risk and performance indicators and associated threshold measures.

- Develop and maintain the bank’s integrated security controls framework in line with regulatory guidelines like the Australian Prudential Regulation Authority (APRA), Financial Sector (Transfer and Restructure) Act (FSTRA), and The Anti-Money Laundering and Counter-Terrorism Financing Act.

- Monitor existing security framework to identify any misconfiguration in firewalls, proxies, and data loss prevention tools.

- #9 Society and planet contribution

- As a part of the bank’s Human Rights Position Statement and 2023 Action Plan, it should focus on financial literacy programs that help customers understand the scope of cyber fraud and crimes. These programs also create awareness on the optimum use of data stored, shared, and managed by the bank to build trust and confidence among customers.

- Westpac’s services to create tangible human impact may be unfairly exploited. Hence, it should screen the receivers of its social services and protect the most vulnerable people, such as marginalised communities and people living in impoverished areas.

- As a part of the bank’s support initiatives and policies to achieve goals of the Paris Agreement, aligned to net zero emissions by 2050, the bank should focus on:

- Using green products such as virtual cards, pulper cards, eco ink, and carbon control press machines to reduce the direct impact of their business activities on the environment.

- Introduce innovative banking services to encourage the consumption of renewable resources. Examples include low-interest loans and credit facilities for green building and renewable energy financing for SMEs.

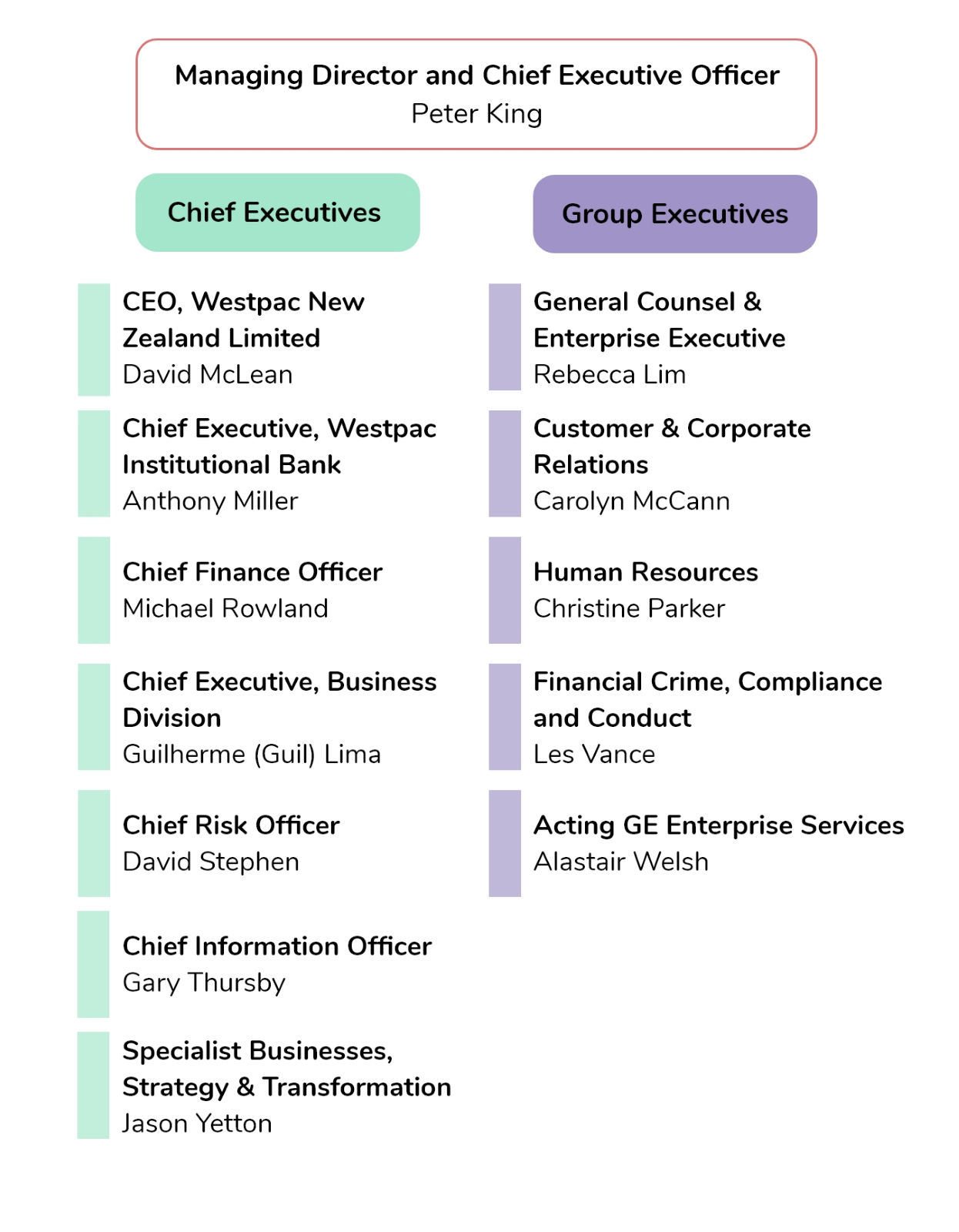

Organisation structure: Leadership

Executive Profile

Peter King

Managing Director and Chief Executive Officer, Westpac Group

In April 2020, Peter took on the role of Group Chief Executive Officer of Westpac. The appointment was after he held this role on an interim basis between December 2019 and March 2020.

Having completed his silver jubilee at Westpac, Peter has rich experience in handling the bank’s Finance, Group Audit, Tax, Treasury and Investor Relations functions. Before being appointed as CEO, Peter worked in the capacity of Deputy Chief Financial Officer for three years and senior positions across the Group, including Group Finance, Business and Consumer Banking, Business and Technology Services, Treasury and Financial Markets.

Quotes

- Business process, 2 November 2020

Notwithstanding the challenges, the bank had made several important changes, including introducing its new lines of business operating model, adding more than 400 people to its risk, compliance and financial crime team, and installing a new executive team. We unveiled three key priorities – fix, simplify, perform.

David McLean

Chief Executive Officer, Westpac New Zealand Limited

In February 2015, Westpac appointed David as Chief Executive Officer for its New Zealand operations. He has been with Westpac since February 1999, and held several senior roles during this tenure viz, Head of Debt Capital Markets New Zealand, General Manager, Private, Wealth and Insurance New Zealand and Head of Westpac Institutional Bank New Zealand, and most recently, Managing Director of the Westpac New York branch.

Anthony Miller

Chief Executive, Westpac Institutional Bank

Anthony Miller is a new addition to Westpac after accepting the role of Chief Executive, Westpac Institutional Bank in October 2020. He is the bank’s liaison to create and sustain international relationships with corporate, institutional and government clients, as well as all products across financial and capital markets, structured finance, transactional banking and working capital payments. Besides this, he is also in charge of the bank’s branches in Asia, London and New York.

Before joining Westpac Group, Anthony was CEO (Australia and New Zealand) and Co-Head of Investment Bank, Asia Pacific at Deutsche Bank from 2017.

Michael Rowland

Chief Financial Officer

Michael is another new face at Westpac Group and has held the position as the bank’s Chief Financial Officer since September 2020. His responsibilities include handling Westpac’s Finance, Group Audit, Investor Relations, Tax and Treasury functions.

Before joining Westpac, he was a Partner in Management Consulting at KPMG. Prior to KPMG, he held several senior executive positions at ANZ. These positions include CFO Institutional Banking, CFO Wealth, CFO New Zealand, CFO Personal Financial Services, and business leadership roles as CEO Pacific, Managing Director Mortgages and General Manager, Transformation. Michael commenced his career at KPMG, where he became a Tax Partner in 1993.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Westpac Banking Corporation, (2020, September 30). Group annual report.

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/Westpac_AU_2020_Annual_Report.pdf

Largest banks in Australia by asset, (2019). Statista.

https://www.statista.com/statistics/434596/leading-banks-in-australia-assets/

Westpac Banking Corporation PE Ratio, (2020, September 30). YCharts.

https://ycharts.com/companies/WBK/pe_ratio

Sourav Kumar, research intern contributed to this research by conducting preliminary literature review, creating infographics, and conceptualising the article.