Superapps have become the next battlefield for dominance across the Asian technology giants. Grab, Goto (Gojek), and SEA Ltd are names featured most prominently to claim titles to become the region’s largest Superapp. Large conglomerates, telecom companies, and financial institutions are not behind either with plans to transform end-to-end customer journeys through digital engagement platforms.

To demystify the topic and its relevance to ASEAN & Indian context, we invited Sachin Mittal, Executive Director DBS who shares an investment analyst’s view of the opportunities and challenges. While we encourage you to listen to the entire 60 minutes of our engaging conversation, I am presenting a quick summary of the session.

We covered the following three themes in this session:

- What is happening in the digital economy in ASEAN?

- Is Superapps the way forward for your digital strategies?

- Is there an opportunity for telcos?

Before we deep dive, here is a pulse on what the audience thought about the topic.

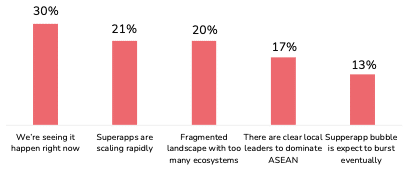

Poll 1 question: Is there an opportunity for Superapps in ASEAN & India?

Key highlights from the session

# Local market context is important for the success of Superapps

Given that the Superapp concept finds its roots in Asia’s largest mobile economy, China, many tend to believe the ASEAN superapps can well be on the path to replicating the success seen by the likes of WeChat and Alipay. Superapp success in China was fuelled by very distinct market forces

- Strong and segmented ecosystems for Alipay and WeChat

- Cross-platform content search restrictions and no common search aggregators like Google

- Two large competing platforms with an equally large subscriber base

These market forces do not exist in ASEAN or India and as such it will be harder to replicate the success seen in China.

# Every Superapp is an Orchestrator, but every orchestrator is not a Superapp

There are multiple references that are being drawn while referring to Superapps. Market confusion exists between two distinct concepts used interchangeably:

- An Orchestrator: extends existing customer journeys by the way of offering related services

- A Superapp: offers at least 3-4 completely unrelated services catering to different business segments (such as mobility, e-commerce, entertainment, and deliveries)

# Start with a single vertical while you partner with the best service providers for others

Most successful Superapp business models have been built around one strong key vertical, and gradually evolving into related & unrelated service segments. A key proposition is the ability to provide a cost-effective solution. They follow a 3-pronged approach:

- Gain insights into their customers

- Identify relevant revenue opportunities

- Take informed business decisions on launching new service segments

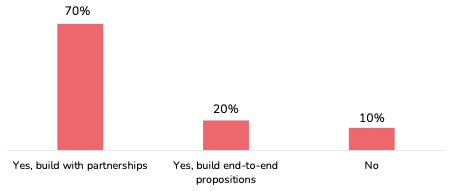

Poll 2 question: Should telcos, banks, and conglomerates look at Superapps as a digital growth strategy?

# Having a financial play alone does not ensure success

Is financial services an end-game for all successful Superapps? Don’t fall spiral into the promise of building a lending business on top of a wallet play.

Since this is a high cash-burn strategy, relying only on revenues from financial services may not suffice.

# Telco Superapp ambitions must ride on improving CX & through partnerships

Digital adjacencies make sense for telcos, if not for new revenues but for building customer stickiness through improved customer experience.

Telcos have the right assets to launch a Superapp – subscriber base, access to consumers’ data, and a strong balance sheet. However, networks remain the number one priority from an investment perspective.

A telcos roadmap for building superapp should leverage its core assets in partnership with new economy players who are well equipped to deliver better customer experience as well as bring fresh capital.