Neobanks have become mainstream among the tech-savvy, young population. These banks also create a significant impact in reaching the unbanked and underbanked population of APAC. Small-medium enterprises are another customer segment that neobanks are trying to make their mark with journey-led support from business registration to payroll and reconciliation. However, most of the neobanks struggle in driving scale and achieving the break-even revenues to develop a profitable business model.

To demystify the topic and its relevance to ASEAN & Indian context, we have Vaibhav Joshi – Global Top 100 CDOs & Top 30 Fintech Influencers in India and David Jimenez Maireles – Chief Experience Officer, Deputy CEO, TNEX Bank. While we encourage you to listen to the entire 60 minutes of our engaging conversation, here is a quick summary of the session.

We covered the following three themes in the session:

- What is the path to profitability?

- Potential long-term impact on market and industry

- What are the CX measures of success?

How do we define the path to profitability?

Most traditional banks are undergoing massive digital transformation initiatives. They have dedicated digital channels to provide banking products. But neobanks are mushroomed to become a one-shop stop for delivering holistic customer experiences. The big question is “What is the differentiated offering of a neobank from the traditional banks?”

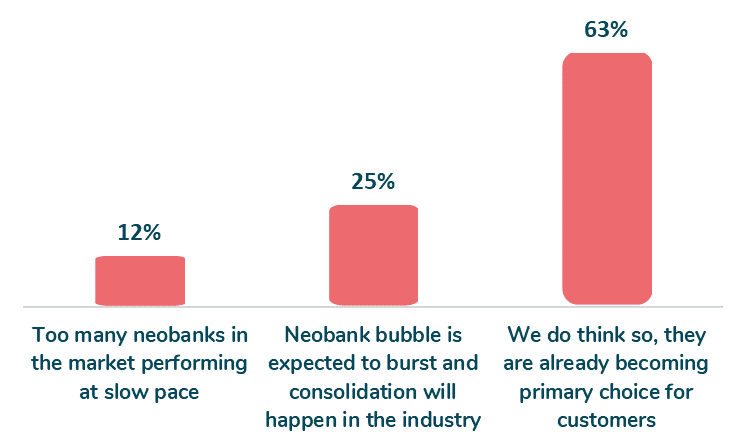

Poll question: Do you think neobanks will become profitable entities?

The largest neobank in India today is not Niyo, Jupiter or Fi. The largest neobank in the country today is SBI YONO. And the second largest neobank is Kotak811. They are both traditional banks, but they have mastered the art of neobanking and bundling the proposition in a manner that the consumer understands.

Most neobanks understand that to be profitable, they need a banking license and the only way to make money is out of lending. It can be from credit cards, unsecured loan or mortgages. The profitability of neobanks lies in reaching a standard deposit ratio (CASA ratio), where they will be able to plug in lending products at a cheaper cost and higher interest rate. This will be the biggest growth driver.

Five best practices to pave a path to profitability

- #1 Embedded finance generates ecosystem value

The future of neobank profitability will come from embedded banking. They seek to embed banking into their customer’s existing lifestyle based journeys. They go to where the customer is, instead of asking the customer to come to them, and in a seamless manner.

Most of the digital banks in Asia are on the lending side, but they are providing an ecosystem where they have embedded services such as insurance, travel trips, bus services, micro investment and games.

- #2 Digital banking license framework is critical for customer and revenue ownership

Looking from a regulatory standpoint, banks want to grow based on great customer experience. The neobank in India cannot own a customer from a banking perspective. The neobank becomes a customer acquisition partner or a co-brand partner or business correspondent. And once you acquire the customer, they can explore the banking platform, even potentially ignoring the neobank at some point in time. This is where the neobanking licenses are going to be important in India.

From a revenue standpoint, a neobank in India can provide a CASA (Current Account Savings Account), lending and various products but every product is going to need a bank at the back end. And that bank at the back end is going to take a sizeable chunk of the revenue that the neobank is making from the customer. And this is what eats into the profitability. But the banker would argue that chunk of profitability share is actually from an infrastructure and hosting technology. Now, if India was to look at the West and bring in banking licenses and once this customer ownership puzzle gets solved, then the route to profitability would be 3X to 5X of what it is today.

The key differentiator between India and other markets is that entities in foreign markets have got the digital banking licenses, which means that they fundamentally own the customer and ownership of the customer is extremely critical. Ownership cannot be a grey area.

- #3 Sustain freemium models in neobanks

Today traditional banks are charging customers for premium services. For example, for a higher version of a credit card, an annual subscription fee is attached. Similarly, for a premium account, a minimum monthly balance needs to be maintained, or else the bank charges you. So the freebies are only limited to a certain set, anything over and above comes with a charge. Whereas the value that neobanks bring is that they have data intelligence with them and push products to the right segment.

The challenge that most traditional banks are facing is when they charge a fee, it is to penalize customers for not doing the right thing. But in this subscription economy, customers pay only for the services that they perceive will generate value for them. And this is how neobanks become game-changers, they provide all the tools to manage customers’ money, to save/invest in the right way, and help create value.

- #4 Increase attach rates

Most of the neobanks target customer segments with specific products. They are offering bite-size wealth management solutions and also integrate crypto investments. This is increasing the overall consumption of services per customer. We also see innovative lending mechanisms like Buy Now Pay Later, completely disrupting the micro-lending experience.

- #5 Becoming a Superapp

A Superapp is like a mall, where you can get all the services from different vendors. Just like in a superstore, you are able to buy groceries, cosmetics, and a variety of things. Similarly, in a Superapp various services are provided by a third party in a white label format or say API integrated format where services belong to the third party but the Superapp is rendering it.

Now, suppose you get into a food delivery app and are able to carry out banking. Inherently that will be provided either by a FinTech or bank at the backend. Only the rendering part is going to happen through that particular interface. While in the case of a neobank, the ownership, and servicing is the responsibility of the neobank.

In the future, we will be observing two scenarios:

- Either new banks will try to build their ecosystem, or

- Older apps will manage to scale up to a point where financial services take a huge chunk of the revenues in terms of payments charge or debit/credit card charges just like Google, Facebook. And eventually look for a banking license.

What will drive the future sustainability of neobanks

Neobanking is here to stay, it is not going anywhere. Neobanking has already started creating the dent in the market. Traditional banking poised to change, they are not going to become extinct. Banks will continue to operate in a hybrid manner and will continue to challenge the challenger banks.

Two key trends to observe in banking industry along with providing seamless and embedded lifestyle services:

- An obsession about rethinking the customer experience, and

- The personalization in terms of data, giving the right product at the right time, the right message at the right location, and for the right person.