Executive Summary

- Enterprise segment revenue for APAC telcos covered in this analysis, reached USD 56.6 billion, showcasing remarkable growth of 11% YoY. This substantial progress has surpassed the overall business growth rate of 7.4% YoY in H1 2023, highlighting the success of telcos’ strategic initiatives in expanding their new enterprise offerings in cloud and IoT.

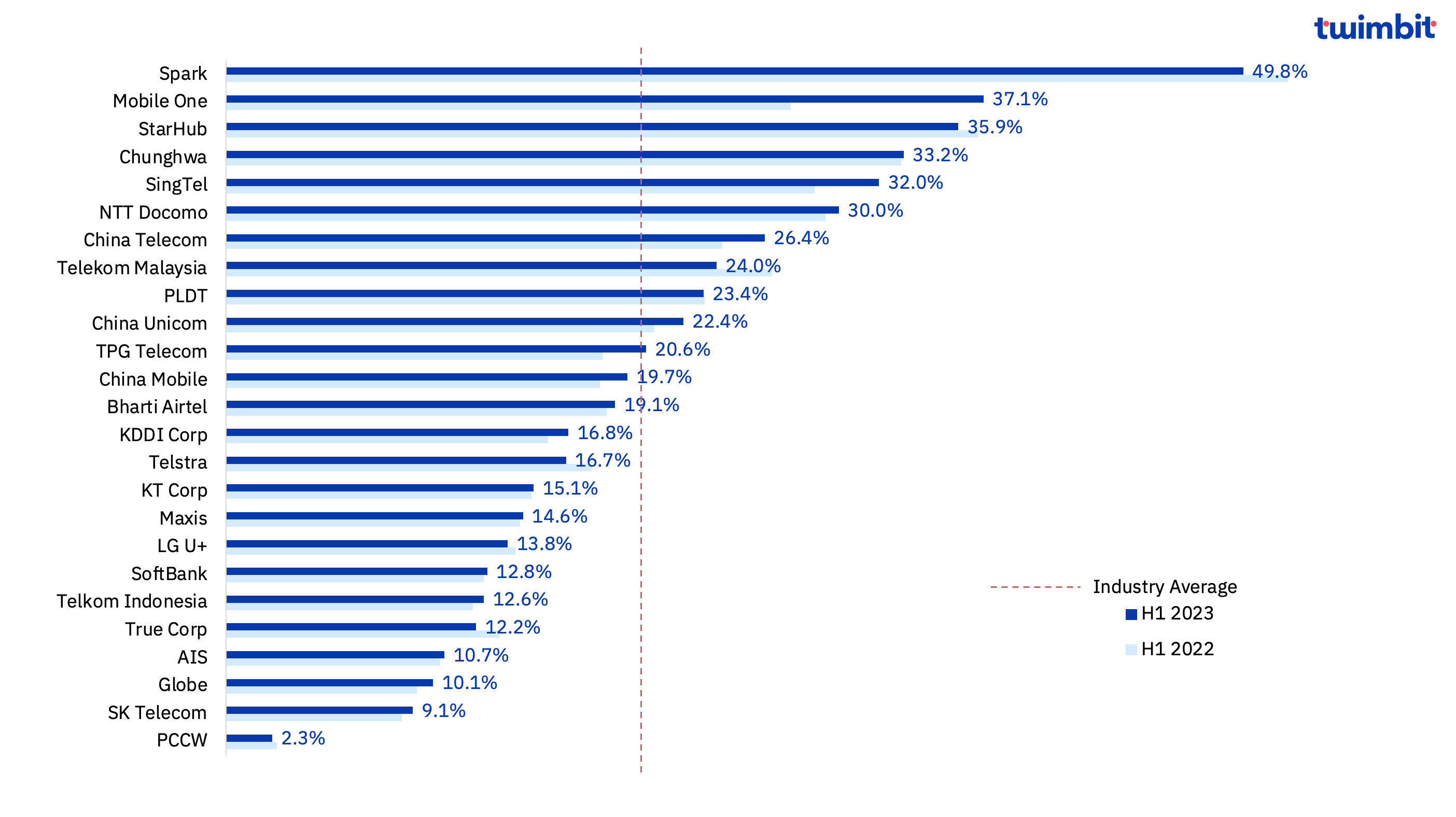

- In H1 2023, enterprise revenue constituted a substantial 20.5% of total revenues, compared to 19.4% in H1 2022.

- Notably, seven telcos had achieved enterprise revenue contributions, surpassing the 25 percent threshold. Leading this charge is Spark, with the highest contribution, followed by Singaporean telcos.

Exhibit 1: Enterprise revenue as a % of total revenue, H1 2022 – H1 2023

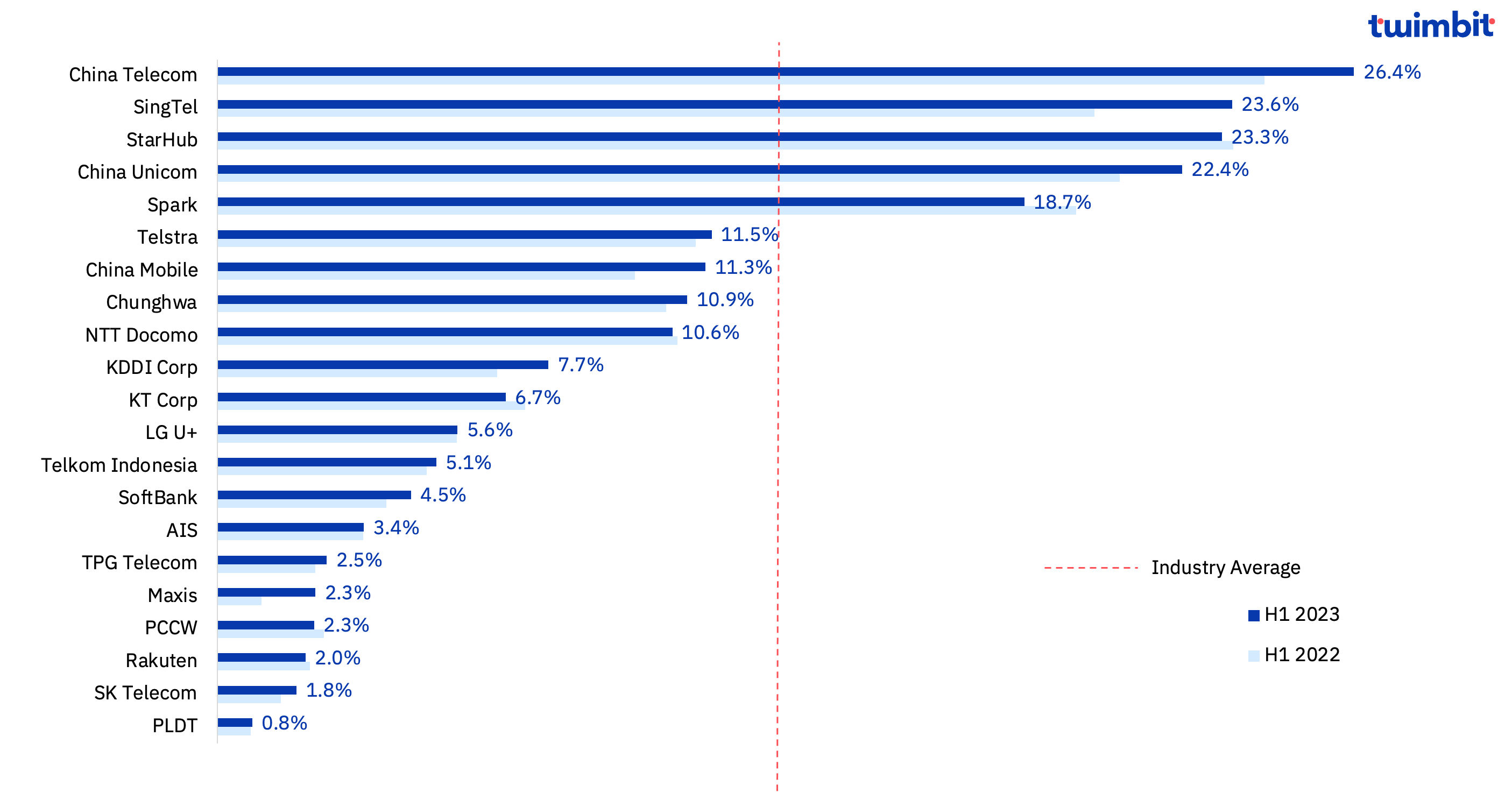

- In the scope of analysis of the 25 telcos examined, enterprise non-connectivity revenue for 20 telcos is considered from their overall enterprise revenue reporting.

- Telcos have strategically shifted their focus to deliver comprehensive enterprise solutions in addition to their traditional connectivity services. This strategic pivot has yielded impressive results, with total enterprise non-connectivity revenue surging to USD 34.4 billion, with a substantial YoY increase of 16.4% in H1 2023.

- Enterprise non-connectivity revenue constituted a noteworthy 13.1% of total revenues in H1 2023, reflecting an upward trend from 11.8% in H1 2022.

- Further highlighting this strategic shift, enterprise non-connectivity revenues reached a significant 63.3% share of total enterprise revenues in H1 2023, compared to 60.5% in H1 2022.

Exhibit 2: Enterprise non-connectivity revenue as a % of total revenue, H1 2022 – H1 2023

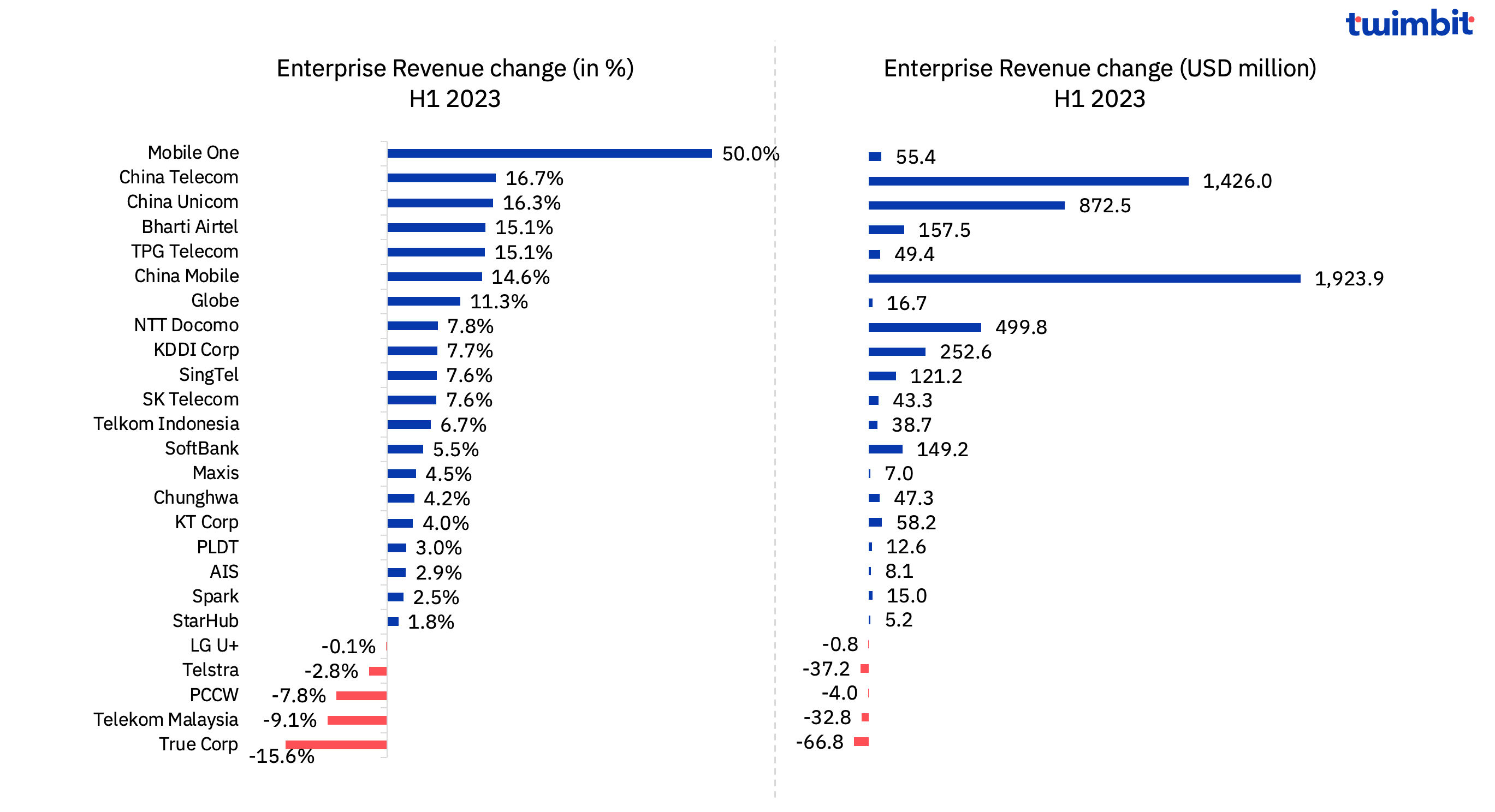

- Chinese telcos have demonstrated an outstanding performance, taking the lead in the enterprise revenue market by collectively generating an impressive USD 31.2 billion (RMB 216.1 billion) in enterprise revenue. This accounts for 22% of their total revenues and exhibits robust growth, surging at a rate of 15.6%.

Exhibit 3: Enterprise revenue trends, H1 2023

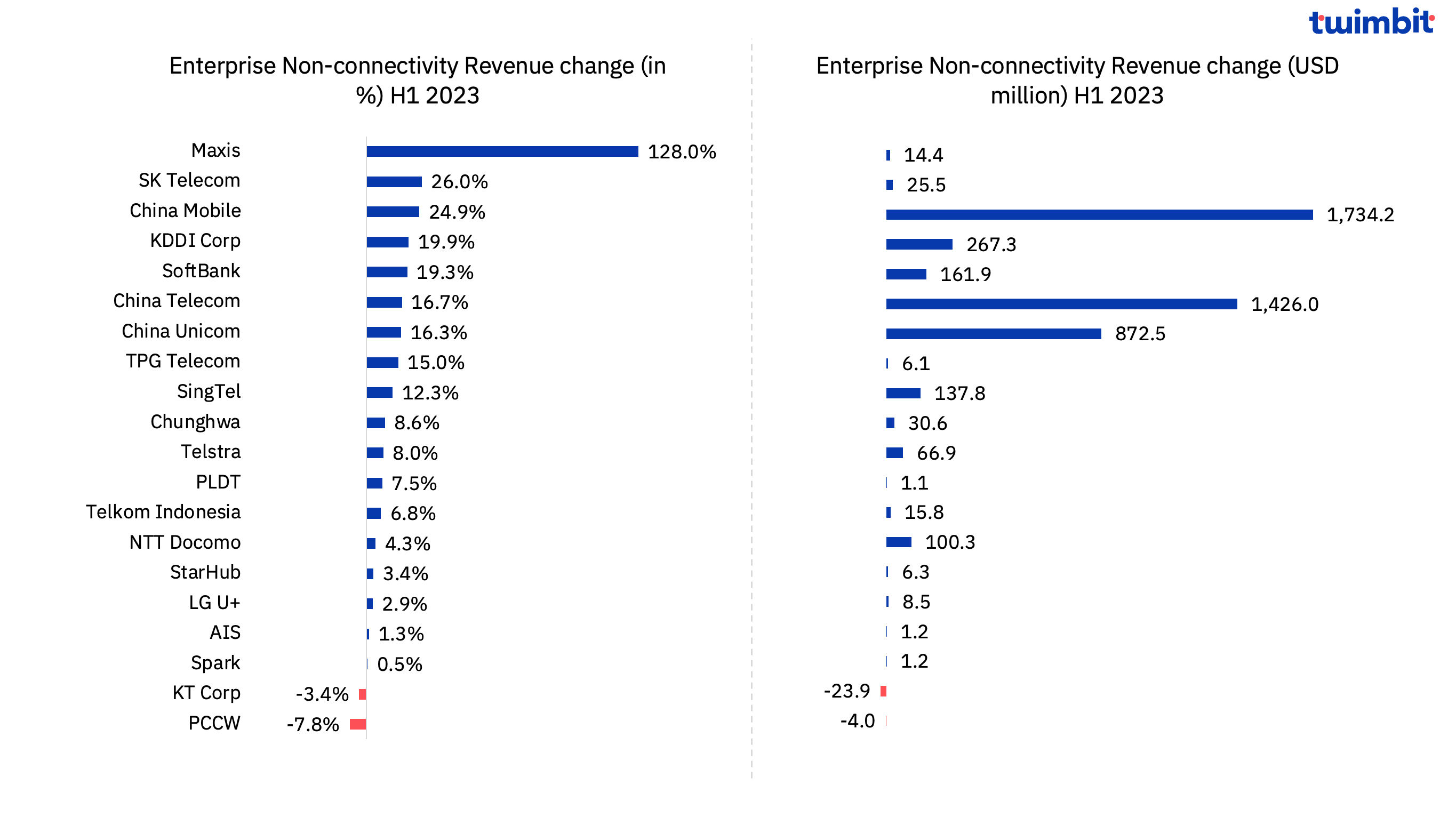

- Telcos have been consistently expanding their enterprise non-connectivity endeavours by introducing innovative solutions within sectors like cloud services, managed services, and cybersecurity. Notably, Chinese operators have taken the lead in enterprise non-connectivity revenue, with NTT Docomo and SingTel following closely behind.

Exhibit 4: Enterprise non-connectivity revenue trends, H1 2023

Enterprise Segment Performance

- In H1 2023, Spark experienced a shift in its enterprise revenue composition, with enterprise revenue as a percentage of total revenue declining to 49.8%, marking a decline of 2.2 percentage points. However, it’s worth noting that despite this shift, the enterprise revenue saw a growth of 2.5% YoY during the same period.

- The decrease in the share of enterprise revenue can be attributed to a 2.2% decline in cloud, security, and service management revenue. This decline was primarily driven by an ongoing shift in the mix between private and public cloud services.

- This decline was offset by a 1% increase in Future Market (defined to include IoT and digital applications) revenue. This growth was primarily fueled by a remarkable 33% YoY increase in IoT (Internet of Things) revenue. This surge was underpinned by a substantial 76% growth in connectivity, reaching 1.46 million connections in H1 2023.

- Singaporean telcos i.e. Mobile One and StarHub have demonstrated strong performance in the enterprise sector during H1 2023, with both telcos achieving a significant share of enterprise revenue as a percentage of total revenue, surpassing the 35% mark.

- Mobile One, Singapore’s second-largest operator, experienced substantial growth in its enterprise revenue, marking a remarkable 50% YoY increase in H1 2023, reaching an impressive 37.1% of total revenue.

- Mobile One enterprise revenue reached USD 116.2 million (SGD 222 million). Driven by the introduction of “Pinnacle,” an advanced Multi-Access Edge Computing solution designed to empower businesses with cutting-edge digital capabilities. Furthermore, the company strengthened its strategic partnerships with prominent cloud platforms like Microsoft and Amazon to offer comprehensive technology-as-a-service solutions.

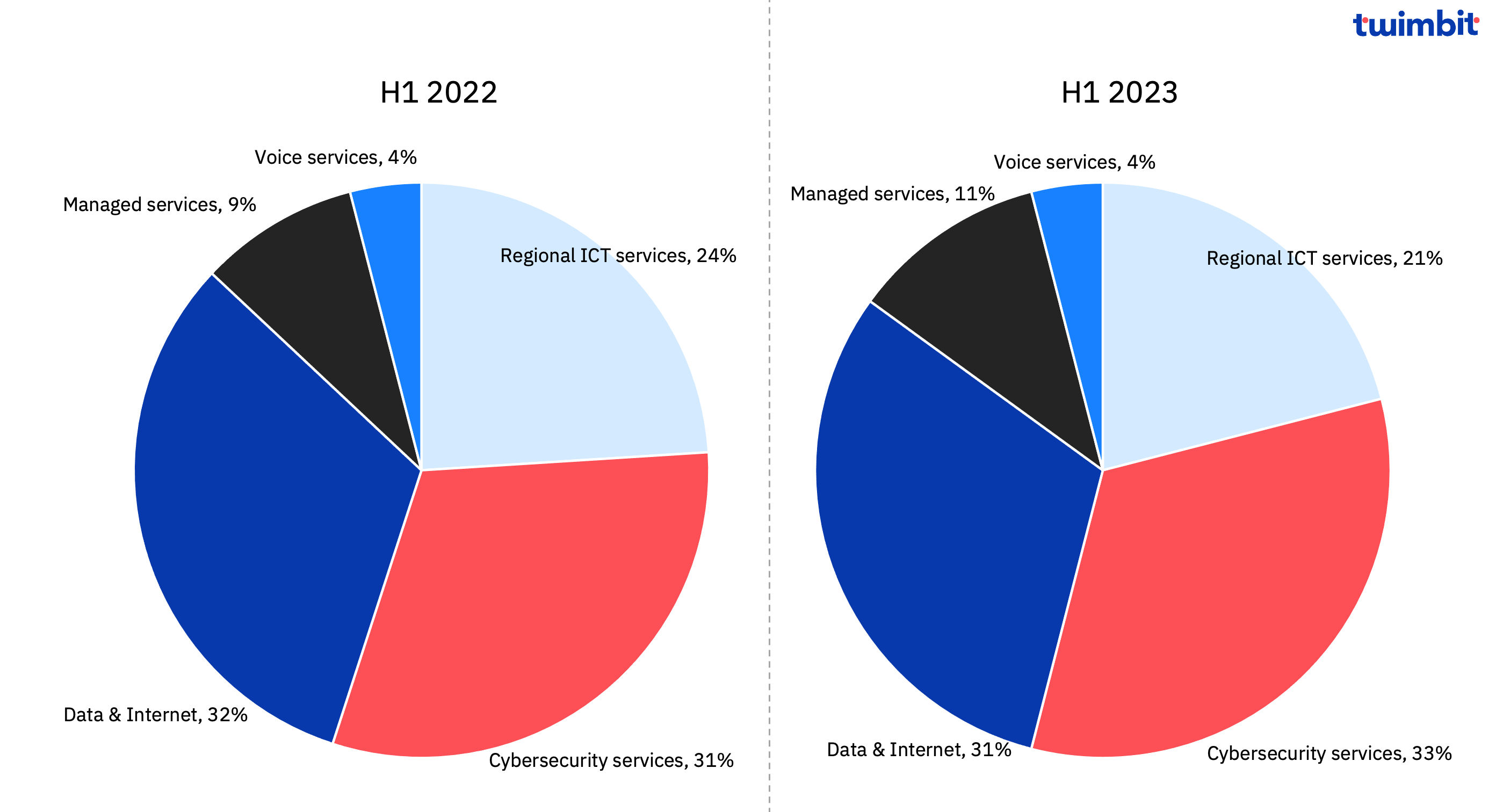

- In contrast, StarHub saw a minor decline in its enterprise revenue as a percentage of total revenue, slipping by 1 percentage point to 35.9% in H1 2023. However, the company’s enterprise revenue witnessed a commendable 1.8% YoY increase, driven by the consolidation of My Republic broadband into its portfolio.

Exhibit 5: Enterprise revenue mix of Star Hub, H1 2022 – H1 2023

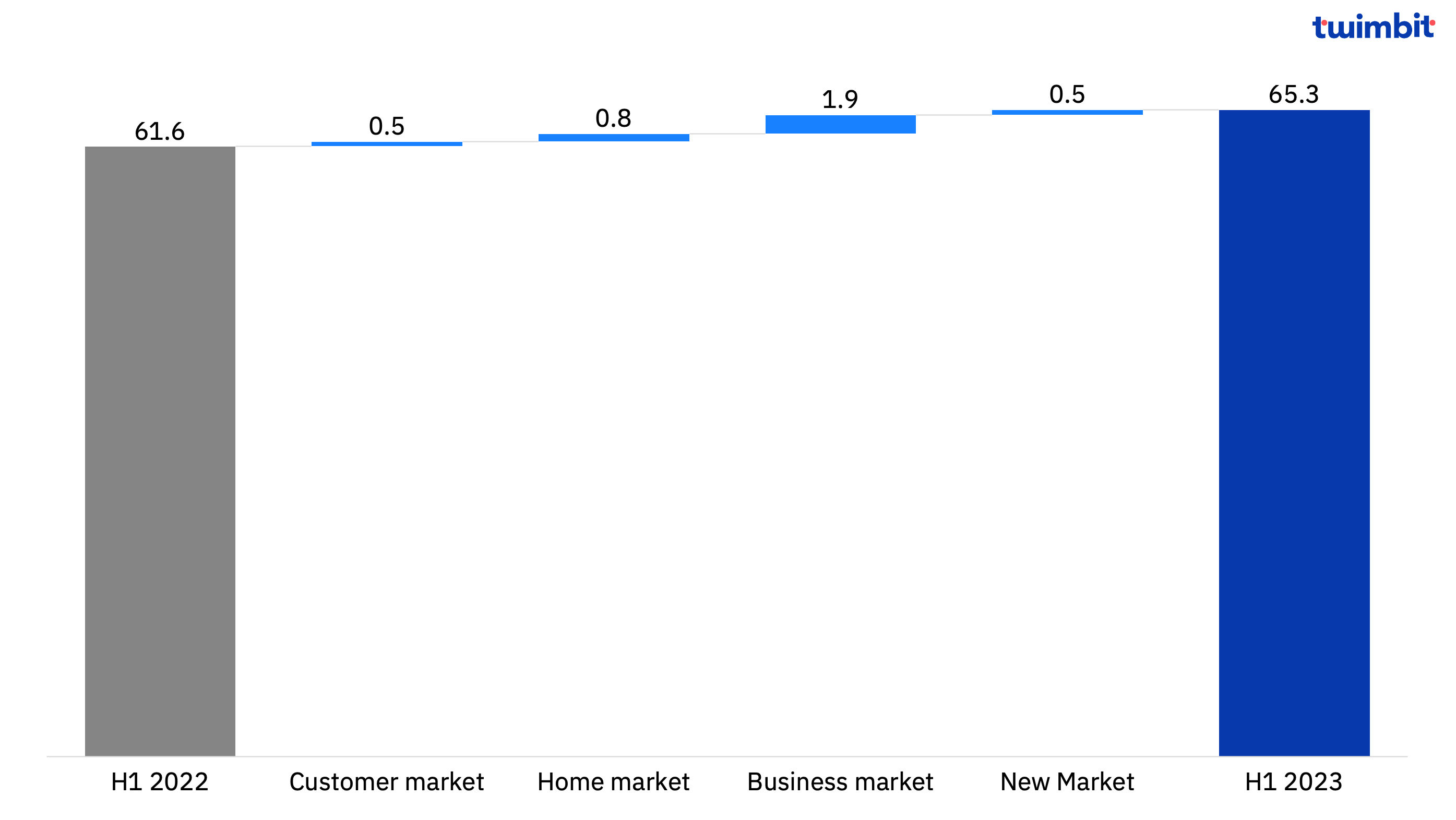

- In H1 2023, China Mobile achieved remarkable results in the enterprise business, recording revenue of USD 15.1 billion (RMB 104.4 billion). This impressive 14.6% YoY growth was driven by a strategic emphasis on the integrated network, cloud, and DICT (data, information, and communications technology) development, capitalizing on its unique strengths in cloud and network resources.

- Key highlights of China Mobile’s achievements in H1 2023 include a focused approach to Mobile Cloud and 5G industry applications, resulting in significant scale breakthroughs. The digital transformation revenue as a percentage of service revenue reached 29.3%, marking a substantial 3.7 percentage point increase.

- Furthermore, enterprise non-connectivity revenue experienced robust growth, surging by 24.9% to reach USD 8.7 billion (RMB 60.2 billion) in H1 2023. This growth was supported by the expansion of China Mobile’s corporate customer base, which reached 24.30 million, reflecting a net increase of 1.10 million customers during the same period.

- China Mobile also achieved significant growth in Mobile Cloud revenue, which increased by an impressive 80.5% YoY, reaching USD 6.1 billion (RMB 42.2 billion). Within the Mobile Cloud segment, the revenue market share of IaaS – secured a top-three ranking in China, with proprietary IaaS+PaaS revenue demonstrating exceptional growth, exceeding 100%.

Exhibit 6: Breakdown of revenue growth (USD billion) of China Mobile, H1 2023

- In H1 2023, China Telecom’s enterprise business revenue reached USD 9.9 billion (RMB 68.8 billion), a significant increase of 16.7% YoY. This growth was primarily fueled by a substantial 92% increase in contract revenue generated from enterprise 5G solutions, further augmented by a notable 75% rise in IoT (Internet of Things) revenue.

- A significant driver of this growth was the strategic deployment of AI , Big Data, and edge cloud technologies in conjunction with their existing 5G enterprise solutions. This approach resulted in the acquisition of approximately ~6,000 new contracted 5G 2B projects (independent private networks) during H1 2023, contributing to a cumulative total of around ~20,000 5G 2B customers.

- In H1 2023, China Unicom achieved noteworthy performance in the enterprise business, with enterprise business revenue surging to USD 6.2 billion (RMB 43 billion). This impressive growth of 16.3% YoY was primarily driven by a substantial 36% increase in Unicom cloud revenue.

- China Unicom maintains its dominance in Big Data with an increase of 54% YoY in Big Data revenue in H1 2023.

- Additionally, the company experienced significant growth in its Big Security (Network security services) segment, with revenue soaring by an impressive 178% YoY.

- Notably, China Unicom’s security cloud market now offers more than 80 products, showcasing the company’s commitment to providing comprehensive and robust security solutions in the enterprise sector.

- Globe achieved notable success in H1 2023, with an 11.3% increase in enterprise revenue, resulting in it constituting 10.1% of the total revenue. This remarkable growth can be attributed to Globe’s strategic transition from telco to techco. This shift has led the company to broaden its vision and prioritize digital solutions, which have proven to be instrumental in driving revenue expansion.

- Japanese telecommunications companies achieved substantial YoY growth in their enterprise revenue during H1 2023, exceeding 5%.

- NTT Docomo demonstrated robust performance with a remarkable 7.8% YoY increase in enterprise revenue. Notably, enterprise revenue now accounts for nearly 30% of NTT Docomo’s total revenue, with enterprise non-connectivity contributing 10% and growing by 4.3% YoY. This growth can be attributed to NTT Docomo’s strengthened focus on DX (Digital Transformation) solutions, aimed at addressing social and industrial challenges.

- KDDI Corp also experienced significant growth, with enterprise revenue increasing by 7.7% YoY in H1 2023. This surge was primarily driven by an impressive 8.5 million YoY increase in IoT connections, reaching a total of 34.5 million connections.

- Softbank witnessed a 5.5% YoY increase in enterprise revenue, leading to enterprise revenue accounting for 12.8% of the total revenue in H1 2023, marking a 0.2 percentage point increase.

Research Methodology and Assumptions

- Data collection has been done leveraging secondary research methodologies and the information provided by the respective telcos. Twimbit follows the calendar year approach for the analysis in this report (meaning H1 is equivalent to the period Jan-June of the year).

- As a part of the research, 50 telcos across 18 Asia Pacific countries were studied. The countries were selected based on their economic significance and the availability of reliable data for the telcos. 25 out of the 50 telcos have reported their enterprise segment revenue, out of which we have recorded enterprise non-connectivity for 20 telcos.

- For fair representation and analysis, a constant currency rate has been used for the conversion from local currency to USD value. The USD conversion rate is the average calculated value for the period Jan-June 2023.

- Enterprise segment revenue includes services provided to the business customers (large, mid and small businesses). It excludes all the B2C revenue. For the analysis, the telco enterprise segments include the below-mentioned sub-segments

- Total enterprise (connectivity+ non-connectivity): Includes voice, fixed-line, and data communications (including leased lines, IP-VPN, SD-WAN, etc.) provided explicitly to enterprise customers. It also includes connectivity services like managed services, IoT, etc., provided to businesses.

- Enterprise non-connectivity: This is defined as beyond core connectivity services provided to the enterprise customers. It mainly comprises of cloud, managed services (collaboration, contact centres, other IT services and applications), IoT, cyber-security, etc. It excludes all the connectivity solutions provided to business customers.

- The analysis primarily focused on understanding the contribution of enterprise segment performance and revenue to total revenue. Further, a detailed peer comparison of the telcos has been also provided as a part of the analysis for the identification of leading telcos and the best practices being adopted by them.

- The data collected may be subject to reporting discrepancies, and the analysis is based on publicly available information.

Thank you for reading! Reach out to us for any feedback

You might also like:

Top 20 Global Telco Update – Q2 2023

APAC telco update – Q2 2023

Cloud stories – Q2 2023

Global Telecom vendors – Q2 2023