Executive summary

- Asia Pacific telcos sustain revenue growth: In Q2 2023, Asia Pacific (APAC) telcos continued their growth trajectory, with a total revenue exceeding USD 150 billion, marking a 4.1% YoY increase.

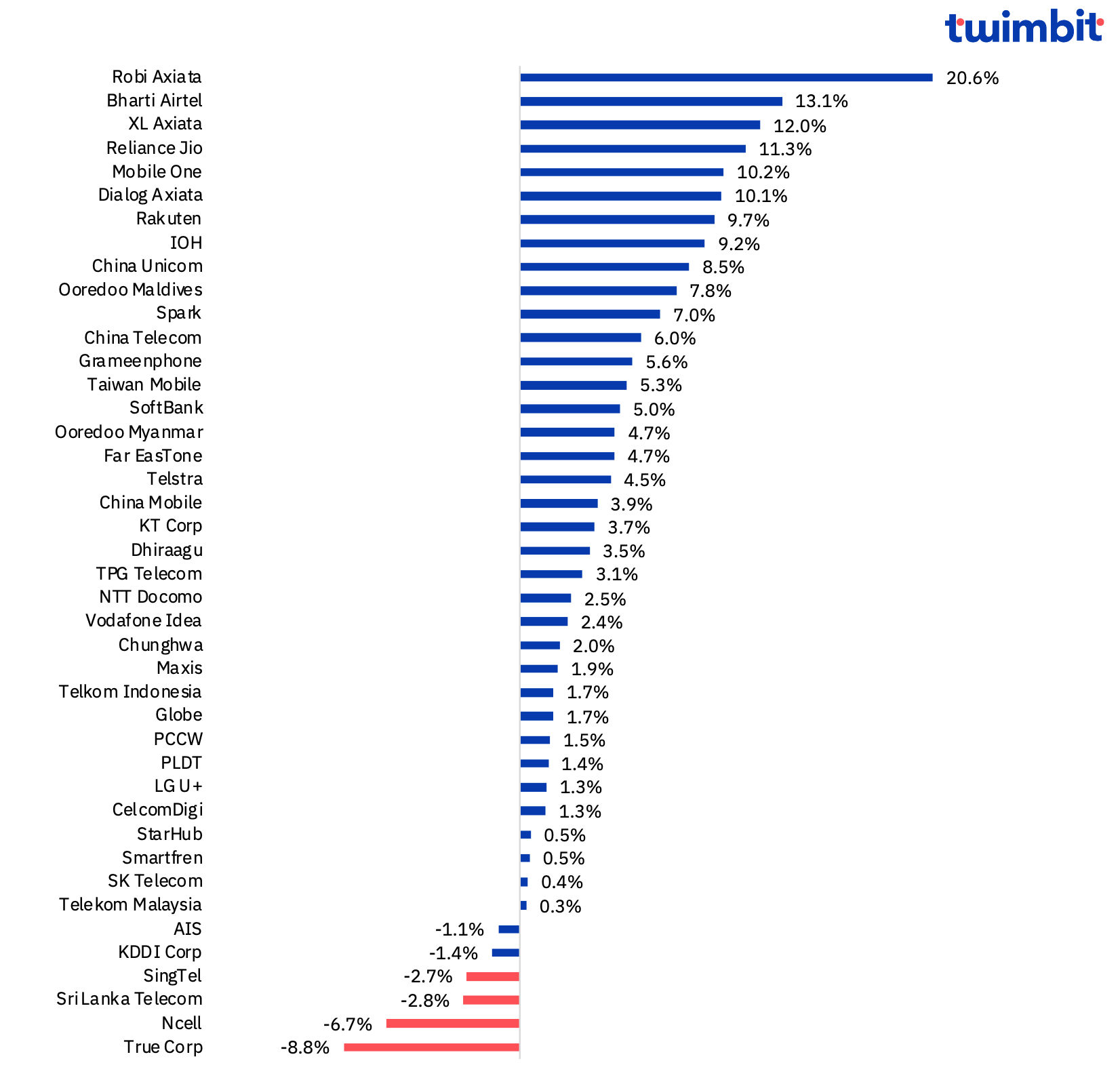

- Consistent revenue growth: For the period Q2 2023, APAC telcos collectively added USD 5.9 billion in incremental revenue, as compared to Q2 2022. 85% of the telcos experienced positive YoY growth. Notably, six telcos achieved double-digit revenue growth, showcasing the region’s vitality.

- Robi Axiata stood out with the highest revenue growth rate of 20.6% (YoY basis), whereas China Mobile contributed the highest incremental revenue of USD 1.4 billion

- Despite the prevailing high competition intensity, the top three Indian telcos achieved a 10% YoY revenue growth rate in Q2 2023.

- XL Axiata and Indosat Ooredoo Hutchison (IOH) in Indonesia exhibited notable revenue progress in Q2 2023, which is expected to persist throughout 2023.

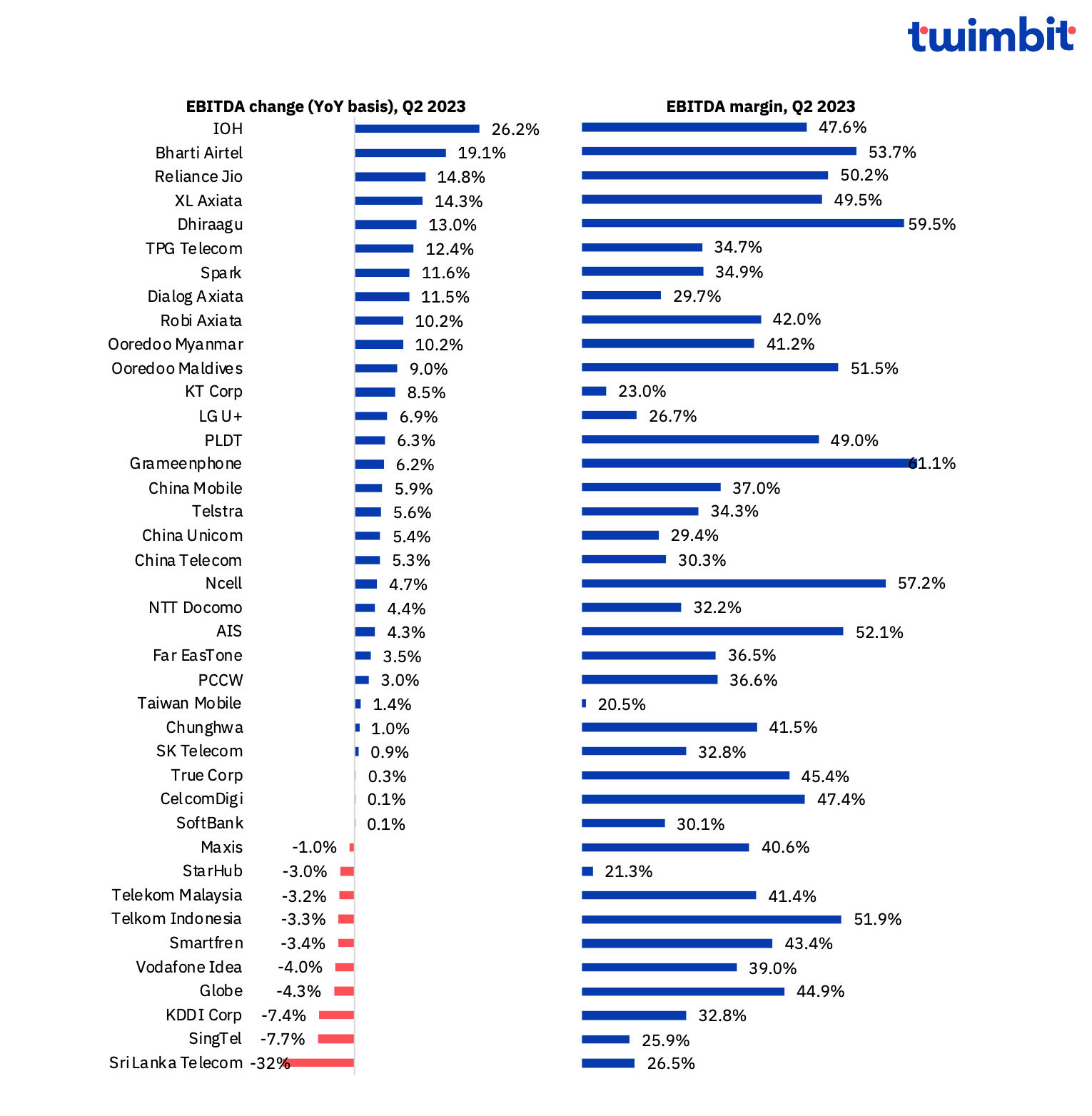

- Record EBITDA margin: Q2 2023 witnessed the highest average EBITDA margin of 34.6% as compared to the past five quarters. Additionally, 75% of the telcos reported a positive EBITDA change.

- In Q2 2023, IOH reported the highest increase (+26.2% YoY basis) in EBITDA, while Grameenphone boasted the highest EBITDA margin at 61.1%.

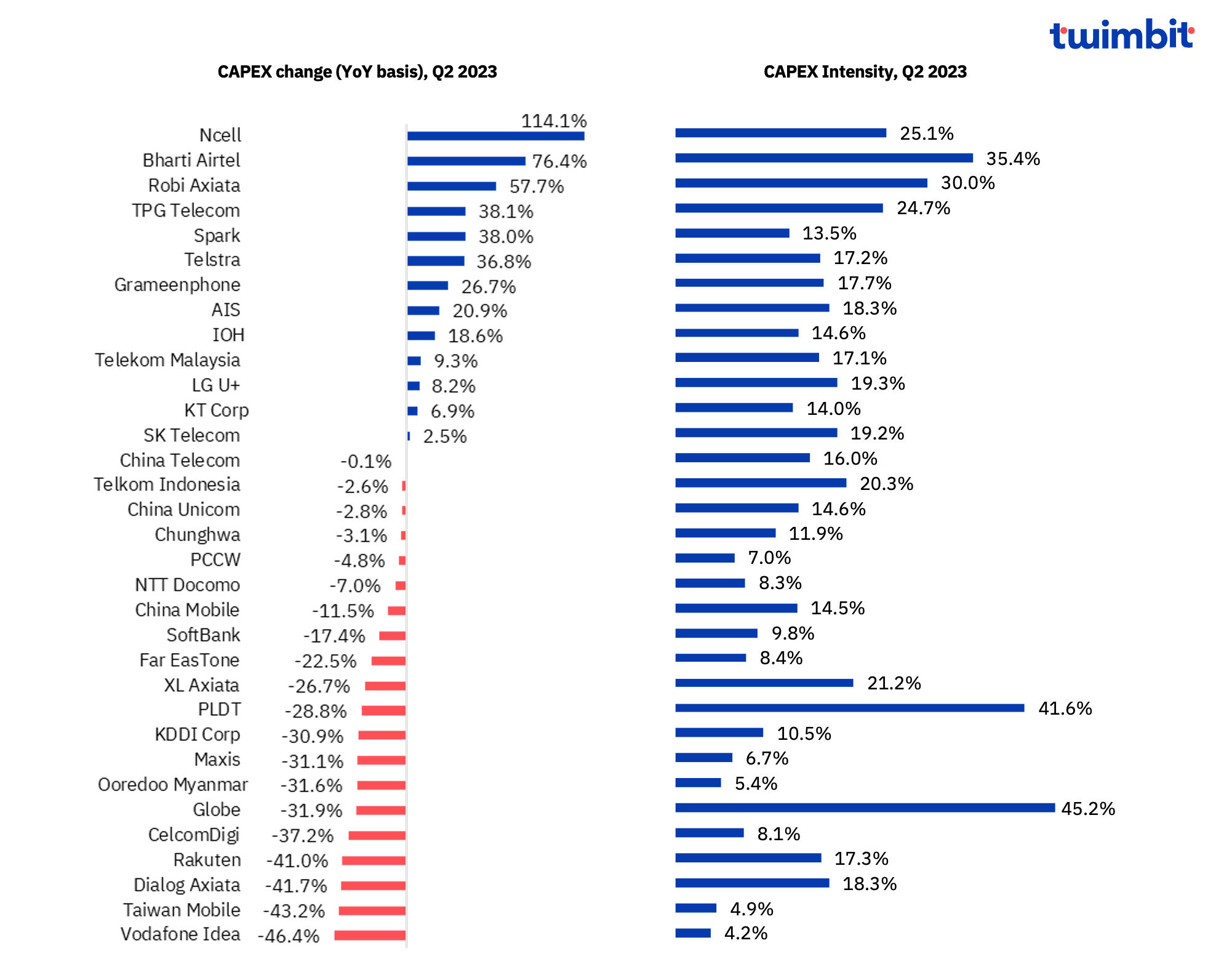

- CAPEX spending continues to decline: The trend for reduced capital spending continued as most APAC markets are in mature 5G stage. Overall, APAC telcos reported a lower average CAPEX intensity of 14.4% in Q2 2023 compared to the previous five quarters

- Ncell recorded the highest CAPEX change at 114.1% YoY, while Globe exhibited the highest CAPEX intensity of 45.2%

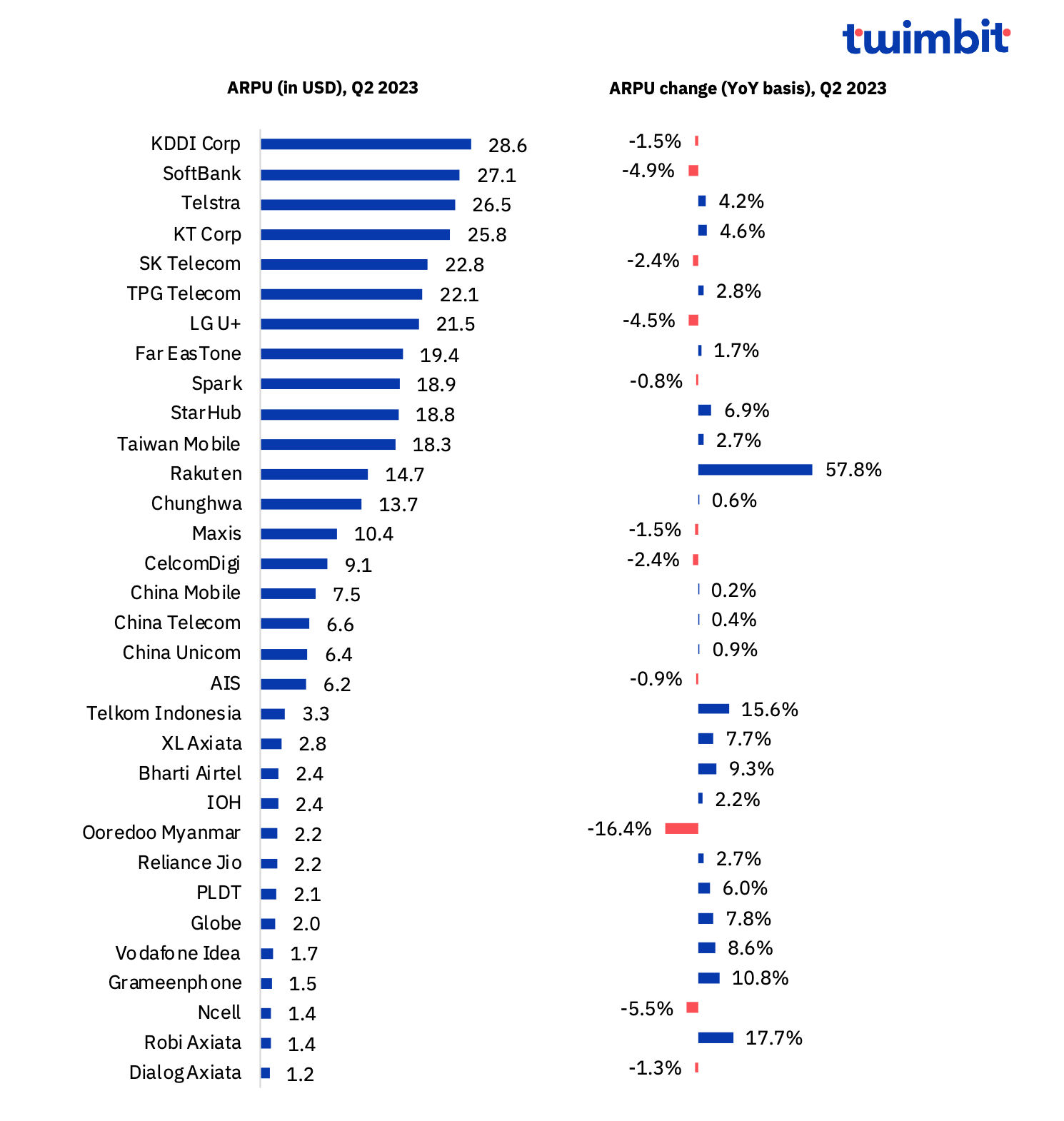

- Stabilisation of ARPU: 16 APAC telcos reported a change in ARPU ranging from -3 to 3% YoY in Q2 2023. Rakuten and Robi Axiata experienced significant ARPU growth, with Japanese operators maintaining the highest mobile ARPU.

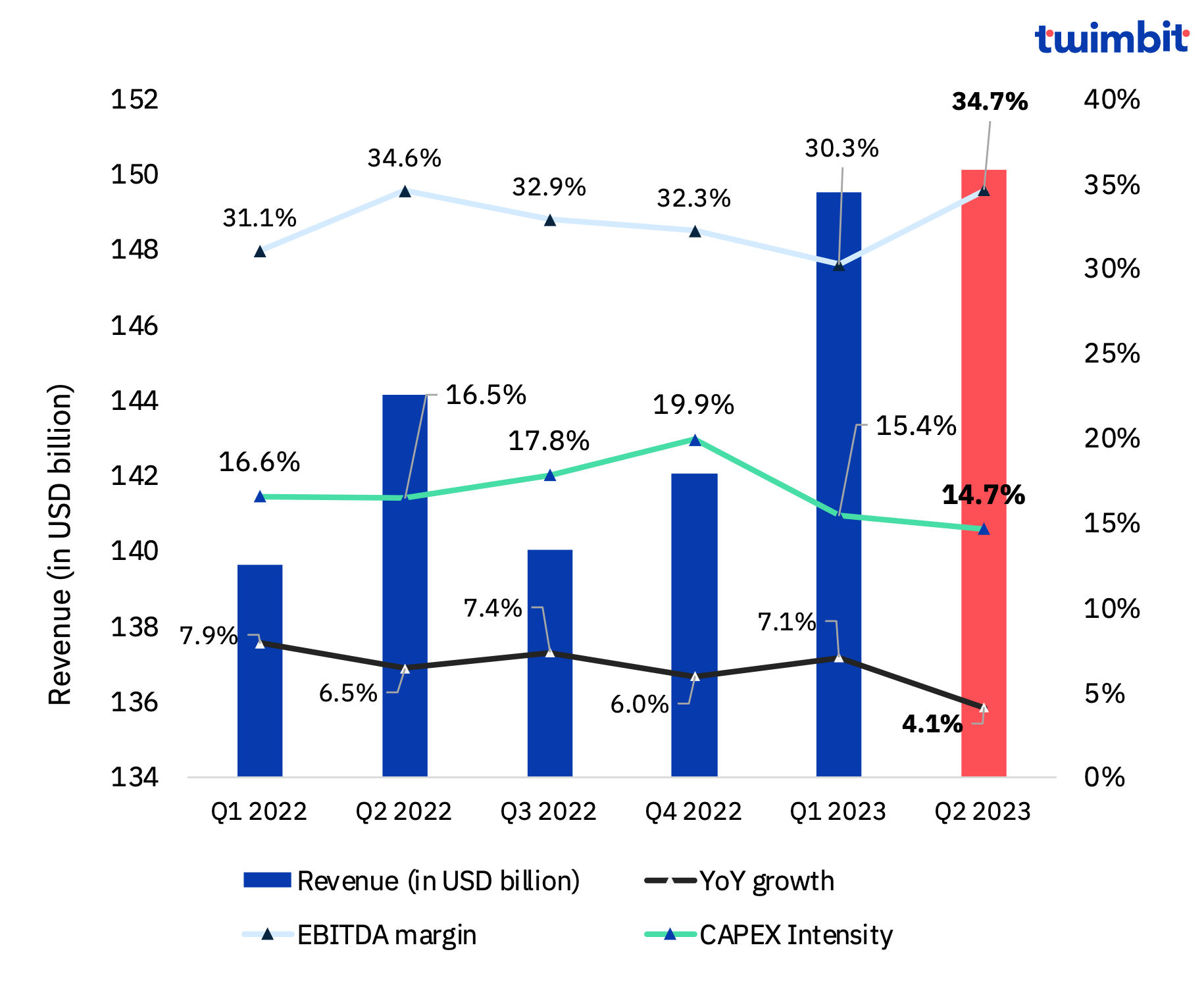

Exhibit 1: Overall performance of APAC telcos in Q2 2023

The overall APAC telco figures for the previous quarters may not align precisely with the current reported numbers, owing to an increase in the number of telcos covered for analysis in Q2 2023.

Revenue analysis of APAC telcos: Q2 2023

APAC telcos surpass the USD 150 billion mark in Q2 2023

In Q2 2023, APAC telcos reported a revenue growth rate of 4.1% YoY, marking the lowest in the past five quarters. During this period, the total revenue of 42 APAC telcos reached USD 150.1 billion (up by ~USD 5.9 billion from Q2 2022). Six telcos achieved double-digit growth and 85% of the telcos recorded a positive change

Exhibit 2: Revenue trends (% change) for APAC telcos (YoY basis), Q2 2023

Robi Axiata

- Robi Axiata noted the highest revenue growth of 20.6% (YoY basis) in Q2 2023, totalling to BDT 25.4 billion (~USD 237.2 million) fuelled by increase in data revenue.

- Growth in data revenue was driven by an addition of 1.0 million data subscribers totalling 43.1 million, marking a 25% YoY

- Data Revenue grew by 29.6% to reach BDT 9.9 billion (USD 92 million) in Q2 2023, accounting for 39% of total revenue up from 36% last year. The growth is also accredited to subscriber and data ARPU growth.

Bharti Airtel

- Bharti Airtel achieved the second-highest revenue growth at 13.1% YoY in Q2 2023 reaching INR 263.8 billion (~USD 3.2 billion). The revenue growth was driven by 12.4% YoY increase in mobile revenues, on account of 4G customer additions and improved realizations.

- In Q2 2023, ARPU improvements and addition in postpaid customer base further enhanced revenue growth. ARPU increased to INR 200 (~USD 2.4) as compared to INR 183 (~USD 2.2) in Q1 2023. The telco added 0.8 million postpaid customers, reaching 40.4 million, and powered over 20 million connected devices.

XL Axiata

- Revenue for XL Axiata increased by 12% YoY in Q2 2023 to reach IDR 8.2 trillion (~USD 551 million).

- The telco benefitted from higher XL Home subscribers, which increased by 50% YoY to 154,000 and a 56% convergence penetration rate in Q2 2023. XL Axiata targets to achieve a 70% convergence penetration rate by 2025 and plans to expand XL Home subscribers to 500,000 by the end of 2023.

Reliance Jio

- Reliance Jio achieved 11.3% YoY revenue growth in Q2 2023 to reach INR 261.2 billion (~USD 3.2 billion) on account of 9.2 million net subscriber additions.

- It is investing heavily in True5G and plans to complete a pan-India 5G rollout by December 2023. It also introduced the JioBharat phone to advance the ‘2G-MUKT BHARAT’ vision in Q2 2023.

True Corporation

- True’s revenue dropped by 8.8% YoY to THB 49.1 billion (~USD 142 million) primarily due to a seasonal decline in product sales.

- Additionally, the decline in revenue was also attributed to a reduction in interconnection revenue after a one-time Q1 2023 litigation benefit.

- In contrast to the overall revenue decline, service revenue improved by 1.1% QoQ, driven by market rationalization and convergence.

Ncell

- Ncell revenue decreased by 6.7% YoY in Q2 2023 to reach NPR 9.7 billion (~USD 74.3 million). The decline was primarily attributed to an 8.3% YoY drop in the voice segment revenue, which was impacted by reduced domestic interconnect rates.

- Despite the overall revenue decline, International Long Distance (ILD) revenue noted a healthy 5.6% YoY increase

Sri Lanka Telecom

- Sri Lanka Telecom group reported a 2.8% revenue decline YoY basis in Q2 2023 totalling to LKR 26.2 billion (~USD 84 million), due to a significant 1 million YoY contraction in its subscriber base.

- Additionally, a 90.3% YoY decrease in international transit revenue and delays in monetizing the fibre network, along with customer churn also negatively impacted the revenue growth.

- Despite this, they noted growth in broadband, IPTV, and enterprise revenue streams.

SingTel

- SingTel’s overall revenue declined by 2.7% YoY in Q2 2023 reaching SGD 3.5 billion (~USD 2.6 billion)

- Despite a 2.7% YoY growth in mobile service, a 21% YoY drop in Singtel TV revenue coupled with a 7.1% YoY decrease in fixed voice revenue also impacted the overall revenue

- Additionally, Singtel Singapore experienced a challenge in the legacy carriage business.

- Singtel is actively driving enterprise 5G adoption and transitioning to the digital world. They’re also integrating consumer and enterprise businesses to enhance revenue and cost synergies, aiming for positive growth momentum.

EBITDA analysis of APAC telcos: Q2 2023

APAC telcos set EBITDA record at 34.7% in Q2 2023

In Q2 2023, APAC telcos achieved their highest EBITDA margin as compared to the past five quarters, reaching an impressive 34.7% (average basis). This trend signifies a commitment to cost efficiency and lower OPEX across the board. Additionally, 75% of the telcos recorded positive changes in EBITDA.

Exhibit 3: EBITDA and EBITDA margin trends for APAC telcos (YoY basis), Q2 2023

Indosat Ooredoo Hutchison

- Indosat Ooredoo Hutchison’s EBITDA grew by 26.2% YoY in Q2 2023 to reach IDR 6.1 trillion (~USD 677.9 million).

- Their EBITDA margin improved by 6.4 percentage points to 47.6% in Q2 2023, owing to cost optimization efforts and a 2.6% YoY reduction in operating expenses.

- Additionally, seasonal effects during the Lebaran festive period also contributed to revenue and EBITDA growth.

Bharti Airtel

- Bharti Airtel reported an EBITDA increase of 19.1% YoY in Q2 2023 to reach INR 141.5 billion (~USD 1.7 billion). EBITDA margin improved by 2.70 percentage points to 53.7% in Q2 2023.

- The increase in EBITDA margin was also positively impacted by their “War on Waste” cost optimization program, which successfully reduced operating expenses, leading to improved EBITDA margin.

Reliance Jio

- Reliance Jio’s EBITDA margin grew from 48.7% (Q2 2022) to 50.2% (Q2 2023), with EBITDA up 14.6% YoY in Q2 2023 a total of INR 131.2 billion (~USD 1.6 billion).

- Despite a 9% YoY rise in total expenses, consistent subscriber additions and ARPU growth boosted its operating revenue, which helped to achieve better EBITDA margin.

Vodafone Idea

- Vodafone Idea’s EBITDA narrowed by 4% YoY to INR 41.6 billion (~USD 506.1 million) in Q2 2023.

- EBITDA margin declined by 2.6 percentage points to 39% in Q2 2023, due to increased network and customer acquisition costs.

Sri Lanka Telecom

- Sri Lanka Telecom group’s EBITDA dropped 32% YoY in Q2 2023 to LKR 6.9 billion (~USD 22.3 million), due to a 15.1% increase in group operating expenditures.

- Furthermore, increase in operating expenditure was driven by factors like sales-related commissions, AMC/license costs due to devaluation of LKR, and rising electricity and fuel prices.

SingTel

- SingTel group reported a 7.7% YoY decline in EBITDA to SGD 902 million (~USD 673.5 million) in Q2 2023 due to inflationary cost pressures.

- Their EBITDA margin decreased by 1.4 percentage points to 25.9% due to increased operating expenses. The increase in operating expense was impacted by higher maintenance, staff, and administrative costs from Digital InfraCo.

Globe

- Globe EBITDA declined by 4.3% YoY to PHP 1.96 billion (~USD 359.1 million) whereas EBITDA margin declined by 2.8 percentage points to 44.9% in Q2 2023.

- This decline in EBITDA margin can be attributed to higher operating expenses and subsidy.

CAPEX analysis of APAC telcos: Q2 2023

APAC telcos dedicate 14.4% of revenue to CAPEX in Q2 2023

APAC telcos reported a declining trend in CAPEX intensity, with Q2 2023 registering the lowest intensity at 14.7% in the past five quarters. In contrast to this, the Indian telecom market is expected to see increased spending due to ongoing 5G developments.

Exhibit 4: CAPEX and CAPEX intensity trends for APAC telcos (YoY basis), Q2 2023

Ncell

- Ncell recorded the highest increase in CAPEX of 114% YoY in Q2 2023, reaching NPR 2.5 billion (~USD 18.6 million).

- This was majorly directed towards adding 3G and 4G BTS’s as a part of its service expansion and improvement drive.

Bharti Airtel

- Bharti Airtel reported a CAPEX increase of 76.4% YoY in Q2 2023 reaching INR 93.3 billion (~USD 1.1 billion). The telco expanded its network coverage in Q2 2023 by rolling out 9,200 new towers.

- Additionally, the telco’s commitment to deliver an exceptional network experience is evident due to its investment in network infrastructure expansion, which included an addition of 38,600 towers on an YoY basis.

Robi Axiata

- CAPEX investments increased by 57.7% YoY totaling BDT 7.6 billion (~USD 71.2 million) in Q2 2023. These were directed towards the enhancement of 4G networks

ARPU analysis of APAC telcos: Q2 2023

ARPU stabalises for APAC telcos

Almost 50% of the telcos reported stability in ARPU levels, with the reported change in ARPU ranging from -3% to 3% YoY in Q2 2023. The Indian market experienced a significant increase in ARPU levels in 2022, which continued in 2023 as well.

In Japan, the impact of tariff reduction and regulatory pressure on ARPU is expected to diminish, with growth anticipated from early next year. Japan still boasts the highest ARPU in the region.

Four telcos achieved double-digit growth in ARPU – Rakuten (57.8%), Robi Axiata (17.7%), Telkom Indonesia (15.6%), and Grameenphone (10.8%). Indian operators Bharti Airtel (9.3%) and Vodafone Idea (8.6%) also demonstrated notable growth.

Exhibit 5: ARPU trends for APAC telcos (YoY basis), Q2 2023

Source: Telco financials, Twimbit analysis

Rakuten

- ARPU levels increased driven by accelerated data consumption with the SAIKYO Plan (translation: Strongest Plan), which was launched in June 2023. This plan removes the previous data limit for domestic roaming partners, providing unlimited high-speed data across the entire nationwide network.

- In addition to the above, growth in Option ARPU (whereby under Option plan services like unlimited calls for specified duration, Guidance support etc. is being offered) along with Advertising services with material upside launched at beginning of Q2 2023, fuelled the surge in ARPU, which increased by 57.8% YoY in Q2 2023

- Further, an increase in telecommunication fees for the mobile segment resulted in revenue growth, thereby having a positive impact on the ARPU levels.

Robi Axiata

- The telco reported an ARPU growth of 17.7% YoY in Q2 2023. The surge in data revenue by 30% YoY in Q2 2023 accounted for the ARPU upliftment.

Telkom Indonesia

- Telkom Indonesia’s strategy of industry pricing rationalization has been successful, with higher payload and payload/data use reflecting the quality of their customer base.

Grameenphone

- Grameenphone achieved a 17.1% YoY growth in data revenues in Q2 2023, driven by a 32.5% YoY increase in data usage.

Explore more content on telecoms: here

Read our country update- Indonesia Telecoms Update 2023