Company Insights

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Bank Central Asia (Group financials)- An overview as of 31st December 2020

| Bank Name | Bank Central Asia |

| Headquarters | Jakarta, Indonesia |

| Operating income (31st December 2020) | USD 5.38 billion |

| Group net profit (31st December 2020) | USD 3.24 billion |

| Total Assets | USD 77 billion |

| Employees | 24,603 |

| Countries of Operation | Not available |

| Number of Branches | 1,248 |

| Computer software asset value (31st December 2020) | USD 18.2 million |

| Number of customers | 19 million |

| Market capitalisation (31st December 2020) | USD 51.7 billion |

| Operating revenue CAGR growth (2016-2020) | 6.92% |

The IDR to USD dollar conversion rate used is 0.00007165.

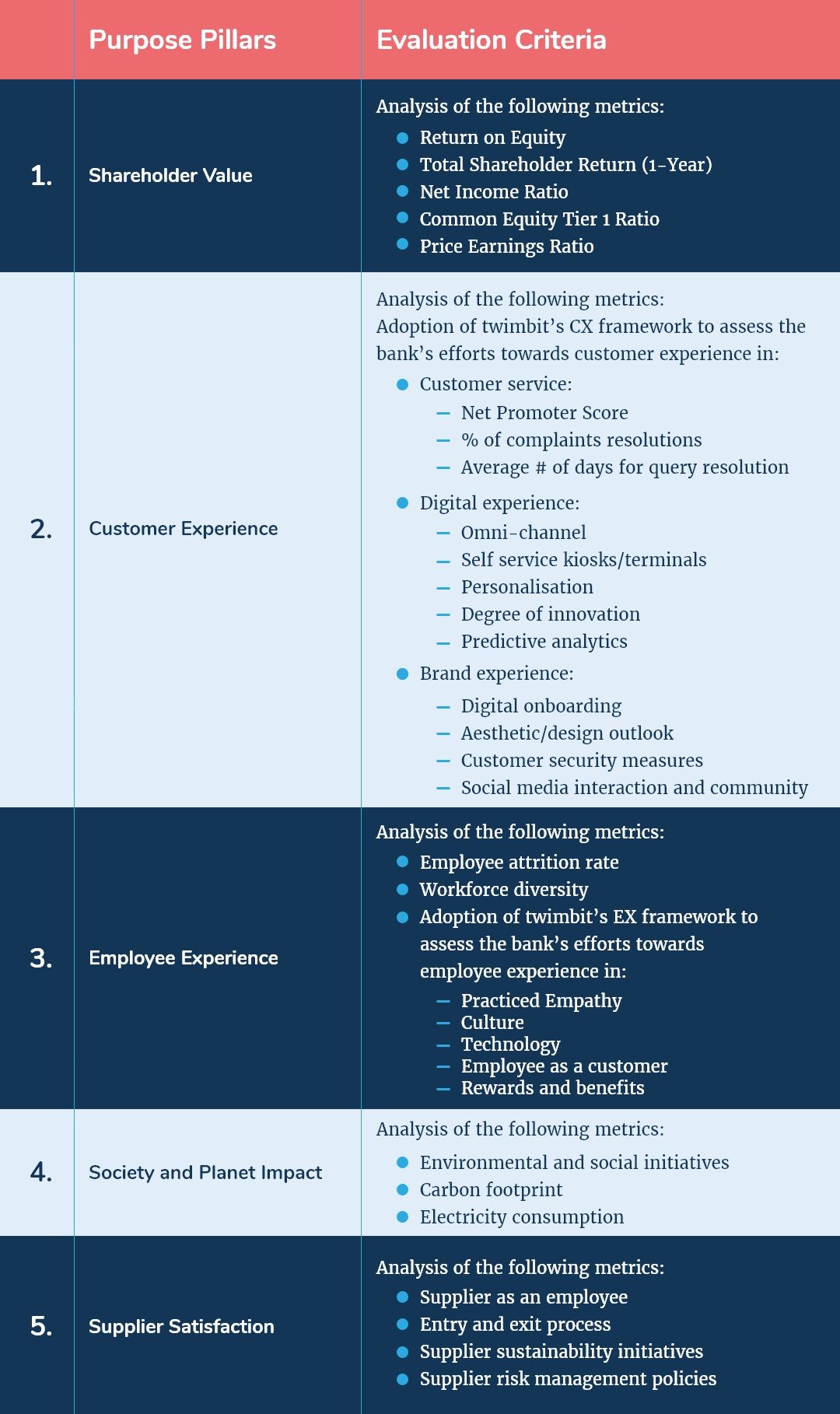

Shareholder value (31st December 2020)

| Return on Equity (31st December 2020) | 16.5% |

| Total Shareholder Return (1-Year) | 32.10% |

| Net Income Ratio | 36.12% |

| Common Equity Tier 1 Ratio | 25.89% |

| Price Earnings Ratio (31st December 2020) | 33.44 |

Awards

| 2020 | Forbes Forbes’ List of The World’s Best Bank 2020- 1st in Indonesia AsiaMoney Best Domestic Bank 2020 The Economist TOP 8 of World Best Banker 2020 ASEAN-BAC ASEAN Business Award 2020- Awarded with the category of Combating COVID-19 Iconomics Indonesia Financial Award 2020 (Millennial’s Choice)- Brand Awareness, Brand Image, Customer Service Quality |

BCA and its strategic focus areas

- Business strategy

The bank aims to strengthen customer relationships by focusing on lending, developing comprehensive solutions, expanding in fast recovery sectors, and providing services in collaboration with its subsidiaries.

- Lending

- BCA aims to balance credit growth and credit quality by lending to customers with good track records and having a strong risk management system.

- The bank has implemented credit diversification to mitigate risk and is closely monitoring the development of its debtors’ credit quality.

- BCA will discover business potential from new industries and existing customers by deploying data optimisation and deepening tools.

- It aims to continue adopting technological developments for accelerating credit approval and the debtor acquisition process.

- Developing comprehensive solutions and services– BCA aims to provide its customers with various financial products and services that complement the bank’s core business of transaction banking. It intends to provide an array of cross-selling opportunities to support the bank’s overall performance.

- Encouraging growth in fast recovery sectors– The corporate banking segment aims to focus on industries that have a strong potential to recover and grow post the COVID-19 pandemic, namely healthcare, transportation and logistics, e-commerce, and property and building materials sectors.

- Collaborating with subsidiaries– BCA aims to collaborate with its subsidiaries to provide products and services such as:

- Vehicle financing (BCA Finance and BCA Multi Finance)

- Islamic banking (BCA Syariah)

- Brokerage and investment management services (BCA Sekuritas)

- Insurance (BCA General Insurance and BCA Life Insurance)

- Remittance (BCA Finance Ltd)

- Venture capital (PT Central Capital Ventura), including a new subsidiary, PT Bank Digital BCA, scheduled to start its business operation as a digital bank in 2021.

Initiatives taken by the bank to support its business strategy in 2020 were:

- Transaction banking- BCA showed solid growth of 21% in its current account and savings accounts (CASA) due to extensive investment in online and digital platforms.

- Commercial and SME banking – BCA continued to develop its API technology to strengthen collaboration with its commercial and SME partners. This technology connects the company partner’s system directly with the BCA banking system, offering a payment and collection solution for Business to Business (B2B) and Business to Customer (B2C). Therefore, online business growth potential sees a boost in the BCA payment ecosystem. Over 2500 customers have already collaborated with the API BCA network.

- Virtual account BCA– The bank created a unique account for customers of corporate companies for bill payments, making it easier for these companies to identify the funds they receive.

- BCA cash management services- This service aims to offer the right solution for corporate cash flow management, and its features include:

- Payable Management:

- Payroll

- Auto Credit

- Cash Delivery

- Bill Payment

- Tax Payment

- Outward Remittance

- BCA Visa Corporate

- Fleet Facility

- Receivable Management:

- Autodebet

- Autocollection

- BCA Virtual Account

- Cash Pick Up

- Inward Remittance

- Payment Gateway

- Business to Business (B2B)

- Business to Consumer (B2C)

- Liquidity Management:

- Account Sweeping

- Automatic Transfer System

- Opening of a Corporate Current Account

- Payable Management:

- Employee experience

The bank’s employee strategy prioritises maintaining highly competent and agile human capital. The said strategy is a combination of careful and diligent recruitment processes, ongoing professional development, and constant reinforcement of corporate culture and values at all levels:

- Developing quality human capital– The bank aims to take initiatives such as recruiting highly competent employees, providing mentoring programs, and conducting training and development for all employees. The upskilling, reskilling and redeployment of employees to take on different roles is under its business development and expansion plans. BCA is also encouraging the said provision through various training and development programmes.

- Digital learning channel– BCA is constantly enhancing its digital training platform for facilitators, moderators and speakers to deliver learning materials and host webinars, as well as for video recording purposes. The bank also strives to support and improve employee capabilities and adapt to new ways of working.

- Technology adoption– The digitalisation and the migration of processes to an online platform will help improve HR management work processes and operational efficiency.

- Recruitment and succession planning– BCA continues to promote employer value proposition as well as conducive and a productive working environment to attract new joiners and maintain employee loyalty.

Initiatives taken by BCA for employee experience in 2020

- Conducted training that focuses on low code programming, design thinking, UI / UX (User Interface or User Experience), data analytics, machine learning (ML) and updated work patterns.

- Organised leadership programs to encourage agile leadership development.

- Digital buddy program- This program uses a reverse-mentoring method with a bottom-up approach. The digital buddies, mostly millennials, are selected to assist non-digital savvy workers as they embrace digital technology and learn about various digital platforms and new work trends.

- Established platforms and communities for sharing the latest innovations and best practices.

- Programs for career development and preparing future leaders:

- Scholarships for Masters degrees

- Career development programs

- Leadership development programs

- A matriculation program

- Branch Manager buddy program

- Initiatives for enabling high performance and productivity during COVID-19:

- COVID-19 crisis team- coordinates all health protocols to prevent, handle, and control COVID-19 transmission within the company.

- COVIV-19 call centre- To ensure that employees always have the latest information.

- BCA promotes a healthy work-life balance through initiatives such as financial planning advice, healthy lifestyle, smart parenting and others. These initiatives are conducted online in light of safe-distancing protocols.

- Society and planet impact

BCA is committed to implementing sustainable programs that promote alignment between the economic, social and environmental aspects following Indonesia’s sustainable development plan by:

- Reducing the impact of environmental damage and risks by cutting down its use of energy and natural resources.

- Inviting employees to take an active role in environmental protection via education and internal communication media.

- Making efforts towards external environmental preservation, including financing environmental, social, and governance (ESG) projects.

- Providing job opportunities in the surrounding communities based on the applicants’ competencies and suitability, as well as the bank’s needs.

Initiatives taken by BCA to create a society and planet impact in 2020:

- Sustainable financing– For the financing of non-MSME (Micro Small Medium Enterprises) Sustainable Business Activities (KKUB), especially in the plantation sector, BCA supported prospective debtors to obtain biodiversity management and sustainable land-use certification.

- Paper saving initiatives– e-statements for savings, current accounts, and credit card bills as well as cash withdrawal without a receipt option at ATMs, STAR tellers (self-assisted machines), e-branches, and digital banking solutions

- Climate change– BCA has formulated a climate change strategy and roadmap, which it will implement in 2021.

- Green building– All building operations use Building Automation System (BAS) technology to regulate air-conditioning, LED lights, and electricity consumption automatically. The buildings also use a sewage treatment plant (STP) system technology to treat colourless and odourless wastewater, making it more environmentally sustainable.

- “Bangga Lokal” (Proud Local) Program– As part of the national financial system, BCA commits itself to support the development of MSMEs in Indonesia. As such, BCA embraced MSMEs through the Bangga Lokal Program. The program targets MSME activists engaged in several industries, especially creative industries such as food and beverage, fashion, and hobbies.

Digital Strategy

As the customer preference for digital services and solutions continue to increase, BCA strives to provide a transaction banking ecosystem that can cater to the needs of millennials:

- Omnichannel experience– The BCA IT team continues to collaborate with other business units to support the bank’s plan to develop a new omnichannel system. The team aids by preparing the right infrastructure and technology to provide seamless experiences and transactions to customers.

- Digital-onboarding– Improving the digital onboarding process to increase the customer base via new customer acquisitions. With the help of digital onboarding, BCA may continue to increase its customer base by responding to several unserved segments, as well as responding to its customers’ needs for banking transactions, anytime and anywhere.

- Fintech Collaborations– BCA continues to strengthen its collaboration with fintech and e-commerce industries, using Application Programming Interface (API) technology to allow seamless integration with these new tech platforms. BCA has connected with many leading e-commerce and fintech companies through this initiative.

- Future branch model– The bank is developing a more efficient branch model, one that optimises on technology application and adopts digital services. These banking solutions include a range of self-service facilities, such as self-service cash deposits and withdrawals, mobile or internet banking registration, and credit card applications.

BCA undertook the following digital strategy initiatives in 2020:

- Digital Express– Along with adding digital capabilities to its branch network, BCA is also expanding its physical footprint, focusing on a smaller branch format and non-permanent counters equipped with digital equipment.

- Sitecore– Partnered with Sitcore to create a one stop-shop digital website that integrates the customers’ journey and database to provide a seamless customer experience across offline and online channels.

- Element– Partnered with Element, a software-based biometric platform, to provide its customers with a digital authentication solution to smoothen the customer authentication and onboarding process.

- Online Banking– BCA enhanced its mobile and internet banking to provide more convenient and flexible online banking features. The following table highlights significant digital advancements that came about in its mobile app and internet banking.

Table 1: Digital advancements in mobile and internet banking

| Sakuku | An electronic money app that offers shopping payments, topping up credit and data packages, buying game vouchers, and other banking transactions. |

| OneKlik | An internet banking feature that makes the online shopping payment mechanism faster and easier, with funds sourced from a BCA account. OneKlik is also used to wrap up electronic money on various digital applications and be applicable as an alternative for virtual accounts. |

| BCA KlikPay | An internet banking feature that offers a practical and reliable way to make online shopping payments for customers who have KlikBCA or BCA Card facilities. |

| QR Code | A feature on BCA mobile that can pay for shopping transactions at merchants with QRIS payments. |

| Online Account Opening | This feature allows customers to open an account on BCA mobile at any time conveniently. |

| BagiBagi | A BCA mobile feature that customers can use to share money with family, relatives or friends who have the Sakuku app during holidays or as a token of appreciation. The amount of money distributed can be equal or at a random sum. |

| Flazz Gen 2 | The Flazz card is an e-money product for small value payments, such as toll roads, commuter lines, and Transjakarta fares. Customers can top up this card via BCA mobile. |

| Virtual Assistant Chat Banking (VIRA) | An app that provides interactive and real-time information, both financial and non-financial, using chatbot technology developed through ML. |

| Welma | An investment management and protection app that allows customers to transact mutual funds, bonds, and insurance conveniently. |

| Lifestyle | A ‘lifestyle’ feature on BCA mobile app through which customers can purchase game vouchers, aeroplane and train tickets, and also make hotel bookings. |

IT Strategy

- Leveraging technology to enhance customer experience

- The bank is constantly developing API technology to widen its digital connectivity and prepare for the open banking era.

- It continues to optimise the dataset it has to study customer behaviours, needs and preferences to create a more personalised experience.

- Strengthening IT Infrastructure capabilities and enhancing integration with subsidiaries

- Constructing new data centres to manage increased traffic caused by increased digital and electronic transactions.

- Customer Data Integration and Analytics through process data integration, including internal, external, alliances, and subsidiaries. This improvement is vital for deeper analysis using the media storage of Data Warehouse and Big Data.

- Improving security and increasing reliability

- In securing the applications with direct exposure to the internet, BCA monitors data traffic for malware detection and frequently conducts application vulnerability testing.

- BCA continues to optimise the use of ML and AI (Artificial Intelligence) technology to carry out the early detection of data traffic anomalies on its network and database.

Initiatives taken by BCA under its IT strategy:

- Invested in technologies such as Optical Character Recognition, AI, and Robotic Process Automation systems to reduce the requirements for human labour in certain work processes. These advancements allow employees to dedicate more of their time to deepening relationships with customers and delivering value-added work.

- Implemented a data security strategy through Data Loss Prevention (DLP), data classification, 2-Factor Authentication (2FA), and an upgraded Security Information and Event Management (SIEM) tool to apply the latest technology in detecting fraud attempts.

- BCA developed microservices based on the architectural technology of many commonly-used banking transaction features. It focused on development efficiency and delivery changes.

10 Growth and Innovation Opportunities

- #1 Cost to serve

- Due to limited working activities in the year, BCA operating expenses reduced by 2.5% from 2019 to 2020. The bank’s cost to income ratio saw a slight jump from 43.35% in FY 2019 to 44.3% in FY 2020.

- The bank’s net profit after tax (NPAT) declined by 5% compared to FY2019. This decrease and the subsequent increase in cost efficiency was primarily due to a significant increase in the impairment losses on loans. The said impairment losses were due to economic challenges presented by the pandemic. BCA can focus on the following key areas to optimise the cost structure:

- A sound net interest margin management in a low-interest rate climate is achievable by identifying repayment risk in loans and attrition risk in deposits. The bank can use predictive behavioural models to revise its interest-rate risk models and hedging strategies continuously.

- Increase focus on non-interest income and complementary revenue streams to offset the impact of high impairment charges.

- Investing in intelligent document processing (IDP), powered by robotics process automation (RPA) and AI. This step involves character recognition and an integrated customer verification ability, reducing the manpower cost of conducting customer remediation.

- The implementation of transaction-level transparency through RPA-enabled audit trails for red-flagging any high-cost inflections.

- #2 Transformation of the branch and its branch networks

At the end of 2020, BCA had a physical network comprising 1,248 branches, 17,623 ATMs and over 550,000 EDCs (Electronic Data Capture). Overall, 99% of all transactions went through digital and electronic channels. However, BCA realises that the physical branches still continue to have a significant role in transaction banking. 43.7% of the transactions, in terms of value, were still performed at the branch. Therefore, the bank is expanding its branch network by adopting a more efficient branch model, such as BCA Express, which combines digital services with limited human touch. BCA is also expanding its ATM network investment to include Cash Recycling Machines (CRMs), which significantly reduces cash management costs. While the bank has taken some measures to digitalise its physical footprint, it can further modernise its branches in the following ways:

- Cash offices and ATMs are replaceable with Interactive teller machines (ITMs) capable of providing the same services without in-person tellers. ITMs can contribute to reducing the bank’s branch size and consequently lower real-estate costs for BCA.

- Promoting online engagement with the bank’s staff through in-app video conferencing and virtual assistants, rather than visiting a branch physically.

- Revamping the bank branch into a community hub where individuals can connect with executives and socialise while accessing banking services and facilities. Options include cafes, lounges, pop-up stores.

- #3 Customer experience

- Omnichannel experience: The bank has a multichannel presence since it provides various touchpoints to consumers, including bank branches, mobile banking, ATMs, and contact centres in Indonesia. There is an opportunity to build an omnichannel experience across all physical and digital touchpoints for a frictionless customer experience. This experience will be a distinct competitive advantage compared to the many other neobanks and incumbents operating in the region.

- Personalised insights: Under its existing digital framework, the bank has heavily focussed on including features that make transactional banking more simplified for customers, such as a digital personal assistant and Welma (wealth management tool). The bank should invest in understanding the customer’s behaviour patterns, life journey needs, and spending through AI and ML tools. An expanded understanding could aid in creating unique persona-based product packages:

- Giving customers personalised insights into their saving and spending patterns with specific recommendations to help them meet their financial goals

- Employing predictive analytics and algorithms to show customers relevant products based on their preferences and savings or investment habits

- Gamifying the user interface to make the customer experience more interactive and less monotonous

- Improving the capabilities of its virtual assistant, VIRA, to handle front-end customers

- #4 Business segment expansion

- Amidst the COVID-19 recovery stage for small and medium enterprises (SMEs), the demand for working capital could increase. To further enhance the SME financing strategies, the bank can:

- Develop business advisory and management tools that will allow SMEs to make smart investment and banking decisions over digital platforms.

- Collaborate with e-commerce websites to extend credit to small vendors who wish to enter the Indonesian market.

- Invest in digital-only banking services for SMEs to reduce the issue of outreach and inadequate distribution infrastructure.

- Reduce the in-merchant interchange reimbursement fee, and roll out tactical card acquisition and usage campaigns, including offering low merchant discount rates.

- #5 Employee experience and productivity

- The bank has deployed a number of training programs to inculcate digital competencies in its staff. However, the bank should also focus on using technology to enhance employee experience by channelising its efforts towards:

- Using people analytics to check that unconscious bias does not unfairly impact promotion and compensation decisions.

- Integrating ML and data analytics to augment and deliver highly relevant recommendations to its employees.

- Build hybrid-working models that encourage flexibility in working from home and in-office, including onboarding and training.

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Giving its employees the option to work on cross-department projects for lateral career advancements

- Periodical career breaks and approved leave for social cause contributions, such as volunteering in relief camps for teaching, food and medical support work, as well as cleaning drives

- Extending pre-natal and child-bonding leaves with childcare assistance

- Expanding its employee wellbeing plan with targeted mental, emotional, spiritual, and physical programs

- #6 Migration of workload to the cloud

BCA has plans to migrate to the cloud under its IT strategy for 2021. However, the bank is slightly behind its regional competitors who have already adopted hybrid models of cloud technology. Therefore, the bank should not only effectively work towards adopting a private cloud but also build a long-term strategy for building a hybrid cloud model, where a significant part of the workload would be on the public cloud. These steps will allow the bank to mitigate its expenses on building new data centres and effectively manage the increasing traffic from digital platforms:

- Microservices architecture deployed by the bank is best hosted on the cloud, as it can significantly minimise management challenges brought about by the proliferation of services.

- Provide complete end-to-end protection of all confidential data stored in the cloud. This protection enables the bank to maintain its customers’ trust and confidence in obtaining, analysing, and sharing personal customer information.

- Incorporate backup and redundancy capabilities to address security and compliance concerns.

- Quick response to market shifts such as black swan events – COVID-19 and the entry of non-bank players in the banking environment with the grant of digital banking licenses.

- #7 Artificial Intelligence in everything

BCA has already deployed AI to streamline document verification processes and detect anomalies in data at an early stage. To further broaden the application of AI, BCA can focus on the following areas:

- Deploy cognitive process automation (CPA) to create more digitalised transaction banking solutions that go beyond online payment services. CPA can mechanise a set of tasks that, in turn, improvises on its previous iterations, such as monthly bill payments, changing subscription plans based on best offers, and alerts for stock updates, among others.

- Replace traditional means of identification with facial and voice recognition for a quick and robust security mechanism.

- A robust and forward-looking credit profiling mechanism for business banking customers that incorporates predictive analytics to access loan credibility beyond the financial statement analysis. The profiling mechanism could include other key parameters, such as economics KPIs, market and industry trends, bank and system facilities overviews, and more.

- #8 Neo banking

BCA has added significant features into its mobile banking app to make it more appealing to millennials, such as purchasing game vouchers, hotel bookings, as well as train and aeroplane tickets. The bank also improved its user interface to make it more user-friendly and included online account opening and e-branch reservation features. BCA needs a transformational neo banking strategy to keep pace with other rising neobanks in the Indonesian market (TMRW by UOB, Digibank by DBS and Jenius by BTPN). BCA can focus on rolling out a digital spin-off to position itself in the millennial and GenZ customer segment optimally by:

- Partnering with a suitable fintech firm to position itself amongst millennials strategically.

- Strengthening the capability of its in-app virtual assistant, VIRA, to provide proactive alerts, budgetary recommendations, as well as lending and investments options to the customer.

- Aiming for a hyper-personalisation of its products to address the unspoken and latent needs of customers.

- Recreating the design outlook of existing products by introducing features like trendy ATM card designs, virtual cards, and an animated banking app interface.

- Introducing byte-sized loan and investment products which gives customers increased flexibility to navigate through different product options.

- Innovating product delivery channels by combining multiple product offerings as per the customers’ preferences

- Gamifying various customer touchpoints, like awarding badges with the increased use of products, giving discount coupons to loyal customers, leader board between friends and colleagues based on product purchases and highlighting trending products.

- #9 Cybersecurity

BCA has a Risk Oversight Committee that ensures the bank’s risk management system protects it against credit, market, liquidity, operational, legal, compliance, and insurance risks. The committee held nine meetings in 2020, including the review of credit portfolios and the assessment of operational risk, as well as cybersecurity and business continuity plans. The bank should integrate technology into its traditional security practices by:

- Incorporating Cognitive process automation (CPA) to develop and test new security strategies. It also determines the appropriate response mechanisms to account for the dynamic and varied nature of security threats.

- Using predictive analytics in its cybersecurity strategies to identify risk trends and streamline its operational model to pre-empt and find the locus of inadvertent risks.

- Automating regular security functions, threat monitoring, identity access management, internal benchmark compliance, as well as controlling and reporting mechanisms. Such automation will ensure that the overall security framework is more transparent and smoother.

- Regularly screening data silos by using AI-ML to check for the misconfiguration of firewalls, data leakage, and data manipulation to ensure data integrity at all time.

- #10 Society and planet impact

The bank has a comprehensive strategy to save electricity and fuel via its environment-friendly green office infrastructure. However, BCA should aim to reduce 50% of its energy consumption from renewable sources by:

- Building on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid, as well as focus on paperless transactions by investing in the digitalisation of services.

- Launching supporting projects in impoverished areas, which help preserve biodiversity and drive reforestation while furthering local economic mobility.

- Reducing carbon footprint by consciously creating green products such as virtual cards, pulper cards, eco ink, and carbon control press machines.

- Introduce innovative banking services to encourage consumption of renewable resources. Examples include low-interest loans and credit facilities for green building and renewable energy financing for SMEs.

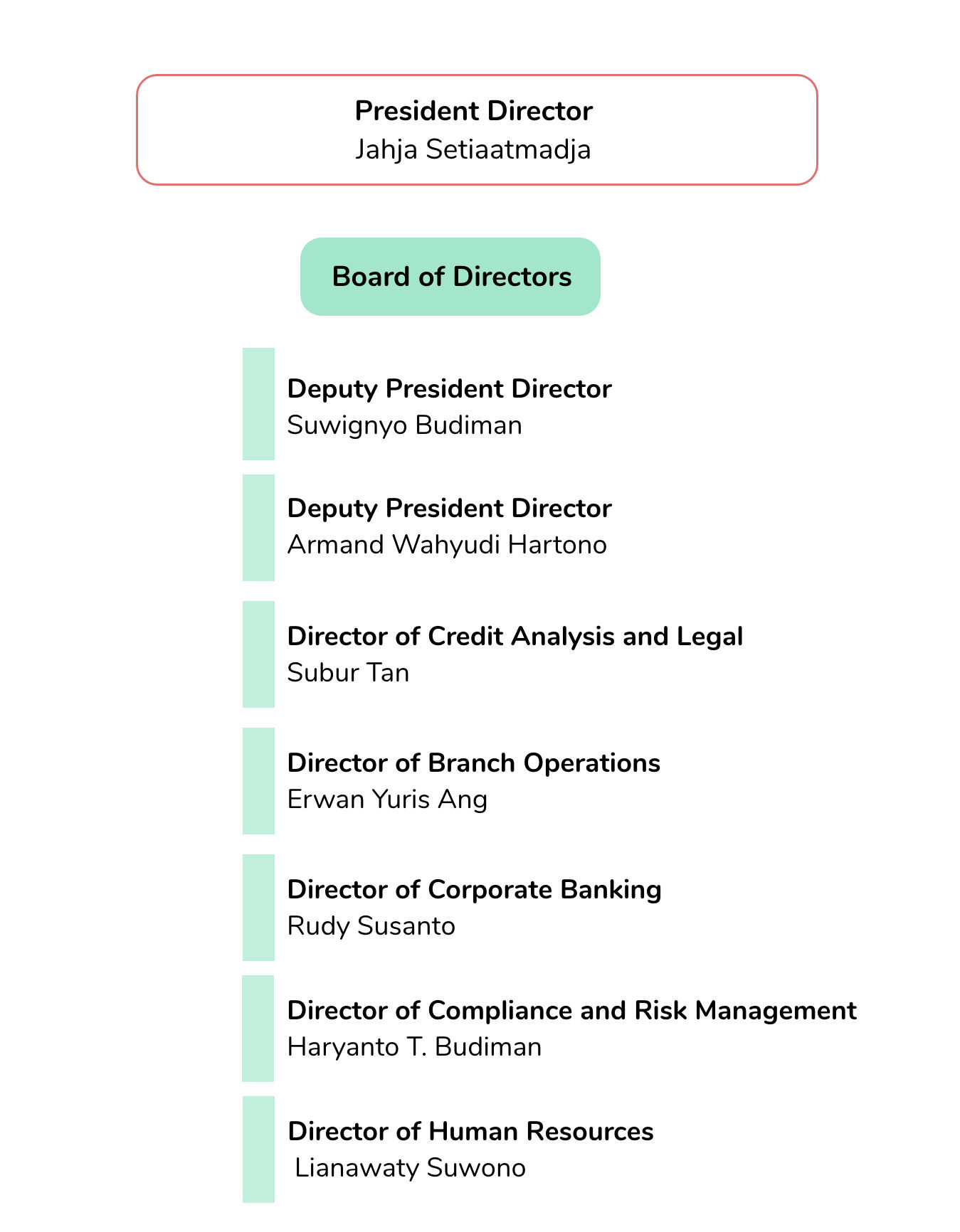

Executive Profile

Jahja Setiaatmadja

President Director

Setiaatmadja is the President Director responsible for the general coordination. He also oversees the Internal Audit Division, Corporate Social Responsibility Work Unit and Anti-Fraud Bureau.

Quotes

Despite the challenges, we took the opportunity to transform and strengthen BCA’s business capabilities. Owing to the support of our customers, regulators, and all parties, the bank and its subsidiaries have navigated this difficult time and delivered a satisfactory performance.

Suwignyo Budiman

Deputy President Director

Budiman is the Deputy President Director responsible for the credit consumer, Individual Customer Business Development and wealth management businesses and coordinates/ supervises the Commercial & SME and Human Resources departments. He monitors the development of PT BCA Syariah, a BCA subsidiary engaged in Syariah banking, and PT Asuransi Umum BCA (BCA Insurance) dan PT Asuransi Jiwa BCA (BCA Life), subsidiaries engaged in general and life insurance.

Armand Wahyudi Hartono

Deputy President Director

Hartono is the Deputy President Director in charge of general supervision of the Regional Network and Branch Director and Transaction Banking Director, and responsible for the Information Technology Group and operational work units. The units include Strategy and Operational Development Division, Domestic Payment Services, Electronic Banking Services, International Banking Services and Digital Services. Hartono also monitors the development of PT Central Capital Ventura, a subsidiary engaged in venture capital.

Subur Tan

Director

The BCA Director responsible for Credit Analysis, Credit Rescue and Legal.

Henry Koenaifi

Director

Koenaifi is the BCA Director responsible for commercial and SME Business, cash management and credit services. He also monitors the development of a wholly-owned subsidiary, BCA Finance, engaged in vehicle financing, and BCA Multi Finance, engaged in industry, factoring financing, consumer financing and leasing.

Erwan Yuris Ang

Director

Ang is the BCA Director responsible for managing, supervising and monitoring regional and daily branch operations. He is in charge of the Branch Support Divisions, Building and Logistic Division, and Branch and Region Management Division.

Rudy Susanto

Director

Susanto is the BCA Director responsible for the Corporate Banking and Corporate Finance Group, Corporate Branch, Treasury Division and International Banking Division. He also supervises the bank’s wholly-owned subsidiary in remittance services, BCA Finance Limited (Hongkong), and the securities subsidiary, PT BCA Securitas.

Appendix A

twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Bank Central Asia, (2020, December 31). Group annual report.

https://www.bca.co.id/-/media/Feature/Report/File/S8/Laporan-Tahunan/20210226AR-2020-BCAInggris-Medium-Res.pdf

PT Bank Central Asia PE Ratio, (2020, December 31). YCharts.

https://ycharts.com/companies/PBCRY/pe_ratio

Gurinayat Brar, Research Intern, contributed to the research in conducting a preliminary literature review and conceptualising the article.